DBS & STE: Why I'm NOT Buying Temasek's Top Stocks (Yet)

Why two government-backed blue chips are quietly dominating Singapore’s market cap rankings, and how the global economy is pushing them even higher.

Singapore’s stock market has a quiet secret: two companies dominate everything. DBS and Singapore Technologies Engineering aren’t just big—they’re reshaping what big even means. And the force behind their growth? Temasek Holdings, the state investment firm that sits at the center of Singapore’s wealth.

This matters because if you own Singapore stocks, you’re probably already exposed to at least one of these names. The question isn’t whether they’re worth watching. The question is whether they’re worth buying, holding, or selling at today’s valuations.

In This Article:

• Temasek’s Historic Growth—And Why It Matters to Your Portfolio

• DBS: The Bank That Just Won’t Stop Winning

• ST Engineering: The Dark Horse That’s Now Running Hard

• The Real Story: Temasek’s Bet on Market Leaders

• What This Means for Singapore Investors Right Now

• The Risks You Need to See

• Your Action Items This Month

• The Bottom Line

Temasek’s Historic Growth—And Why It Matters to Your Portfolio

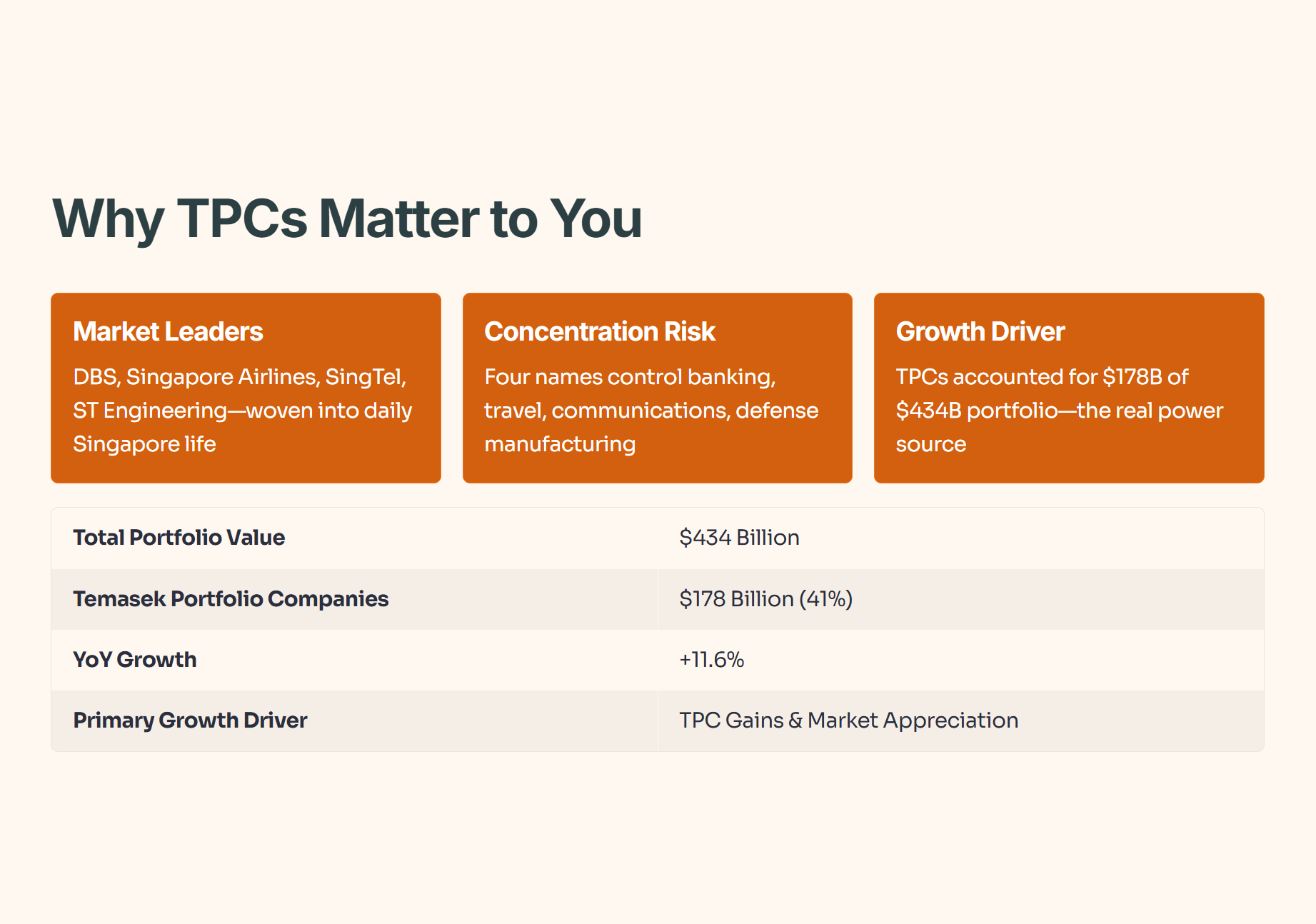

Temasek just dropped its annual report for the year ended March 31, 2025, and the numbers are eye-watering. The fund reported a record portfolio value of $434 billion, up 11.6% year-over-year. That’s not just growth—that’s momentum at scale.

But here’s what most investors miss: the real power isn’t evenly distributed across Temasek’s global holdings. The heavy lifting comes from Temasek Portfolio Companies, or TPCs—businesses where Temasek holds a controlling stake. These TPCs alone accounted for $178 billion of that $434 billion, or 41% of the entire portfolio.

Why does this matter to you? Because TPCs aren’t random. They’re Singapore’s most established market leaders. DBS, Singapore Airlines, Singapore Telecommunications, and Singapore Technologies Engineering aren’t just listed on the Singapore Exchange. They’re woven into the daily fabric of Singapore life—banking, travel, communications, and defense manufacturing all concentrated in four names.

Temasek’s portfolio growth is driven primarily by gains in its controlling-stake holdings. Nearly half of the $434B portfolio is concentrated in TPCs—a sign of both focus and dependency on a handful of mega-cap stocks. This concentration creates opportunity for sharp investors but also risk if sentiment shifts.

DBS: The Bank That Just Won’t Stop Winning

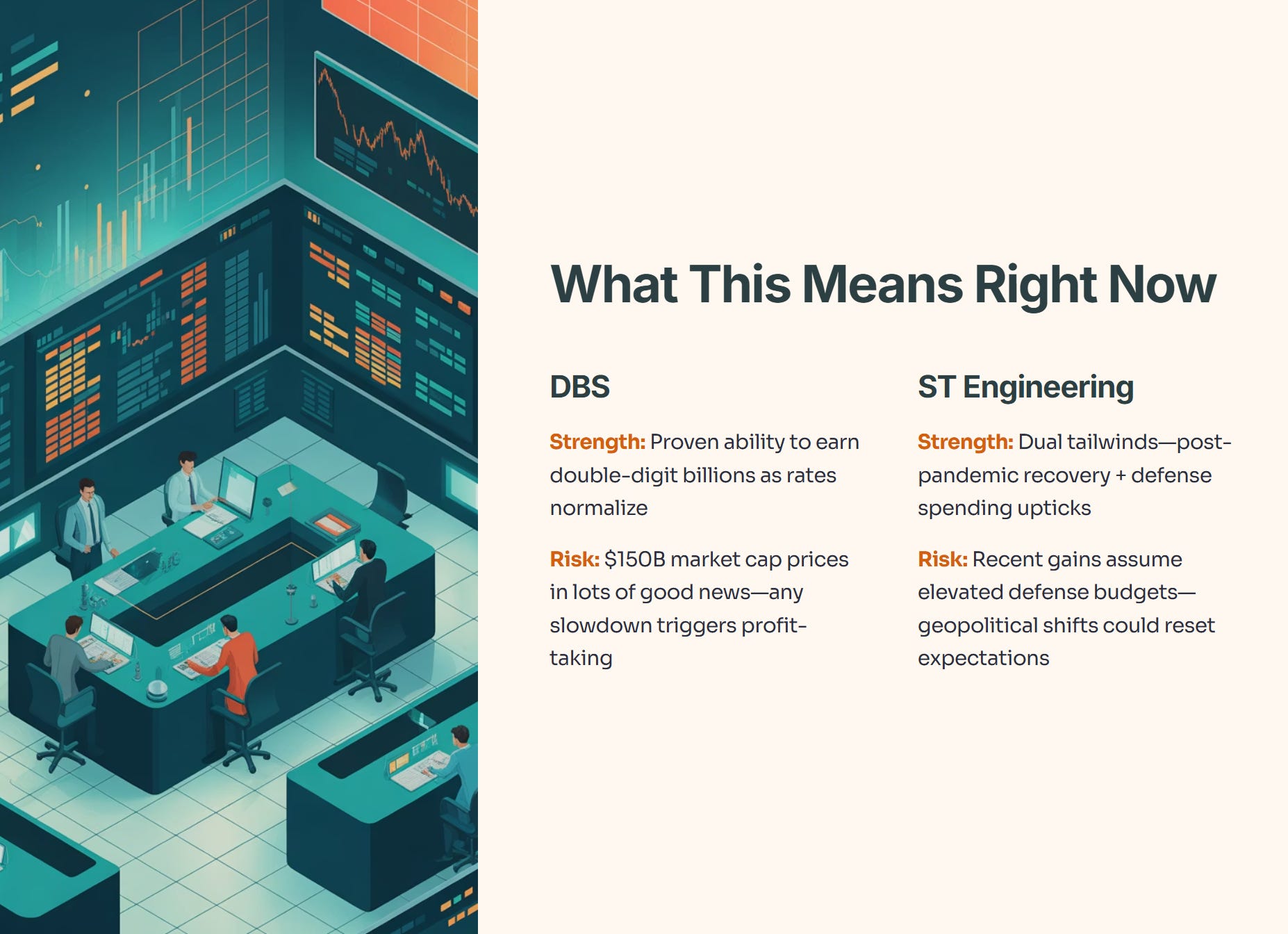

DBS is the golden child of Singapore’s stock market. With a market cap now exceeding $150 billion, it has widened its lead over every other Singapore-listed company. This is a level of dominance that shouldn’t be possible in a diversified market, yet here we are.

At last year’s Billion Dollar Club awards, DBS swept every category in the super big cap sector (companies valued at $10 billion and above). This year, it had to share the spotlight slightly with ST Engineering—but DBS still took home wins for profit after tax growth and overall sector performance.

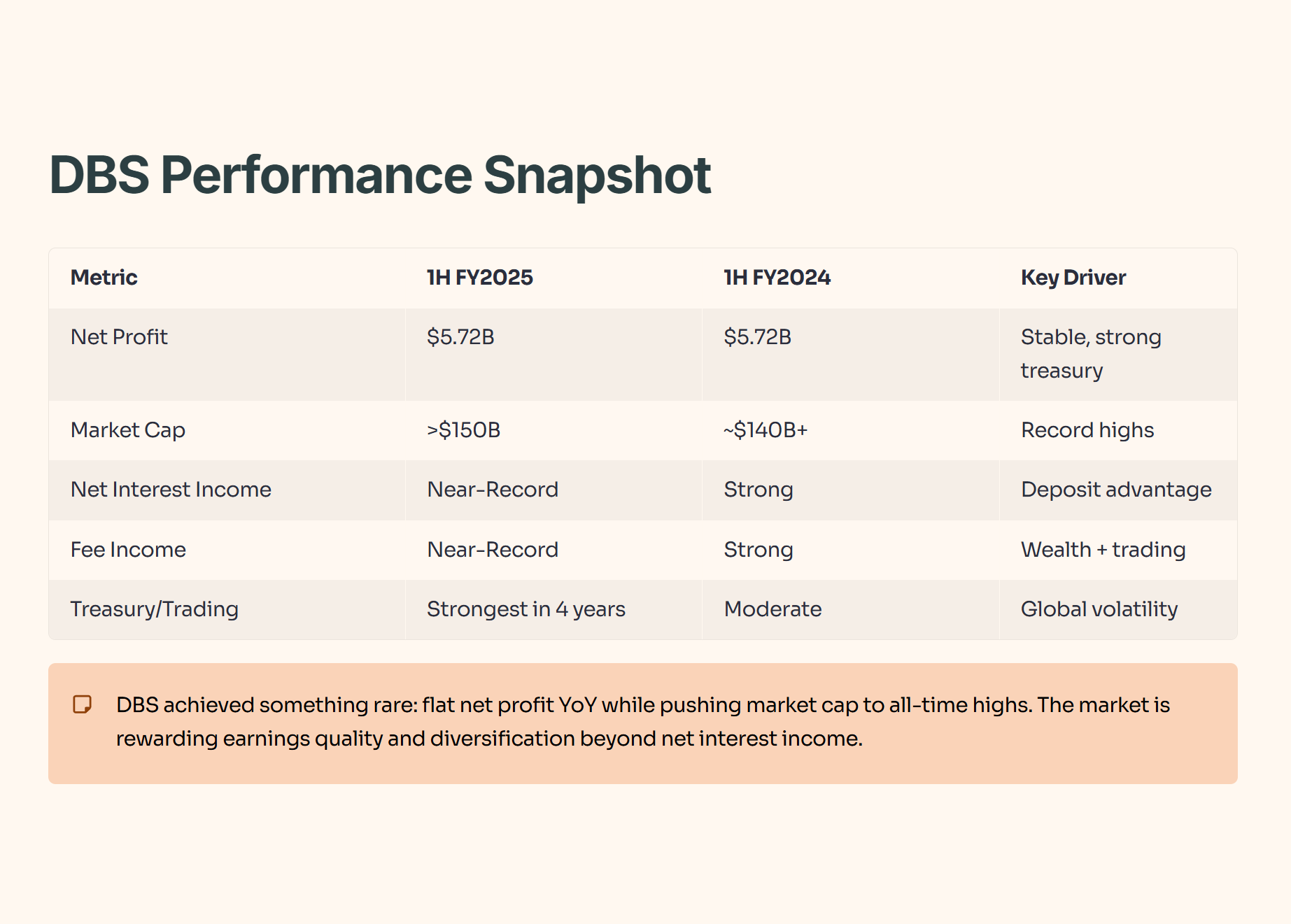

Why is DBS so dominant? Start with interest income. When US rate hikes were combating inflation over the past few years, banks had a field day. DBS captured this better than most. The bank commands a particular advantage because of its access to a vast pool of Singapore dollar deposits. This kept funding costs down and allowed DBS to earn fat margins on lending.

But here’s what separates DBS from your typical bank: it didn’t rely solely on the rate environment. As rate cuts began in 2024, DBS proved it could grow earnings through other channels. Non-interest income from trading, wealth management, and treasury operations became a serious contributor. In the first half of fiscal 2025, DBS reported near-record fees and some of its strongest trading performance in four years.

The result? DBS posted a net profit of $5.72 billion for just six months. On this pace, the bank is on track to defend its $10 billion annual net profit target for the third consecutive year. Investors have noticed. From September 2009 to September 2025, DBS outperformed HSBC, Standard Chartered Bank, and the other two major Singapore banks. Over this 16-year period, DBS delivered returns comparable to the S&P 500 on an annual basis—and that’s in SGD, not USD.

DBS has achieved something rare: flat net profit year-over-year while pushing market cap to all-time highs. This suggests the market is rewarding the bank’s earnings quality and diversification beyond just net interest income. If rates stabilize or fall further, DBS’s other revenue streams become even more critical to defending shareholder returns.

ST Engineering: The Dark Horse That’s Now Running Hard

Singapore Technologies Engineering is not a name that excites casual investors. But it’s the story of 2025 so far, and for good reason.

Like DBS, ST Engineering was born from a government need. In the 1970s, Singapore needed to become self-sufficient in weapons manufacturing for national defense. From there, the company evolved. It expanded into aircraft maintenance, repair, and overhaul (MRO)—a business that got hammered when COVID grounded global aviation but has bounced back strong.

Today, ST Engineering operates across multiple segments: military weapons and platforms, commercial aircraft MRO, shipbuilding, electronics, artificial intelligence, and traffic management systems. It’s diversified enough to weather sector downturns but focused enough to maintain deep expertise.

Two things just happened that matter for investors. First, the Russia-Ukraine war and shifting US politics have triggered a global rearmament cycle. Defense budgets are rising worldwide. Second, ST Engineering has been announcing record orders and record earnings growth. As those orders convert to sales and profits, investors have taken notice. The stock has posted substantial gains, especially after the company set ambitious growth targets across multiple business units.

This matters because ST Engineering won the Billion Dollar Club award for both weighted return on equity and returns to shareholders. That’s not a fluke—it’s a sign that management is executing.

ST Engineering’s multi-segment structure acts as a growth engine and a hedge. While military demand is hot right now due to geopolitical tensions, the company’s other divisions provide stability. The key risk: if defense spending contracts or geopolitical tensions ease, military revenue growth could plateau. That’s why the other segments matter.

The Real Story: Temasek’s Bet on Market Leaders

What ties DBS and ST Engineering together is simple: Temasek owns them. And Temasek’s strategy is becoming clearer by the year.

Rather than chase hot sectors or emerging industries, Temasek doubles down on market-leading businesses in essential sectors. Banks, defense, airlines, telecom—these aren’t glamorous. But they’re irreplaceable in an economy. They generate stable cash flows, pay dividends, and appreciate over the long term.

The $434 billion portfolio value and 11.6% growth in a single year shows this strategy is working. The portfolio companies that dominate Singapore’s market cap rankings are working even harder.

For investors, this reveals a pattern: when you own Singapore stocks, you’re essentially buying into Temasek’s thesis. That thesis is: invest in the best-in-class operator in each essential industry, hold for the long term, and compound returns through dividends and capital appreciation.

What This Means for Singapore Investors Right Now