Don’t Jam the Lift: Why Pounding the "Sell" Button is Killing Your Cash Flow

Stop paying the "Panic Penalty." Audit the 1.24x P/B Gap and your 24-month cash shield before you let a price hallucination wreck your retirement.

The auntie at the Clementi 448 Market wasn’t looking at the price of ikan kuning this morning. She was staring at flickering red numbers on her phone, her thumb hovering over the ‘Sell’ button like it was a detonator.

At 10:45 AM SGT, when the SGX circuit breaker slammed the brakes on the Straits Times Index, the silence in the local brokerage apps was deafening. For a retiree, a 10% market drop isn’t an “Entry Window Analysis” or a “healthy correction.” It feels like a physical theft—a hand reaching into your CPF LIFE bucket and scooping out three years of future holidays and healthcare. The “Red Sea” is an emotional high tide that drowns logic first.

But here is the uncomfortable truth: The market doesn’t take your money during a crash; you hand it over. When you execute a panicked exit during a halt, you aren’t “protecting your capital.” You are paying a voluntary 10% “Anxiety Tax” to the institutional algorithms that have the cold, hard patience you currently lack.

Before we audit the math, let’s acknowledge the room: our community has grown to 6,200 members. That is over six thousand sets of eyes looking for a sanctuary.

And let’s be honest—the fear is real. But here is the forensic reality: Your retirement is not a stock price; it is a cash flow system. If the system is intact, the price is just noise.

📚 In This Article

About Iggy the Investing Iguana

Step 1: The Health Check (The “CPF-SA” Sovereign Floor)

Step 2: The Wealth Check (Dividends vs. Distractions)

Step 3: The Price Check (The “Kopitiam Discount”)

Step 4: The Future Check (Strategy for the Silver Sovereign)

InvestingPro Reality Check

The VerdictAbout Iggy & the Elite 190

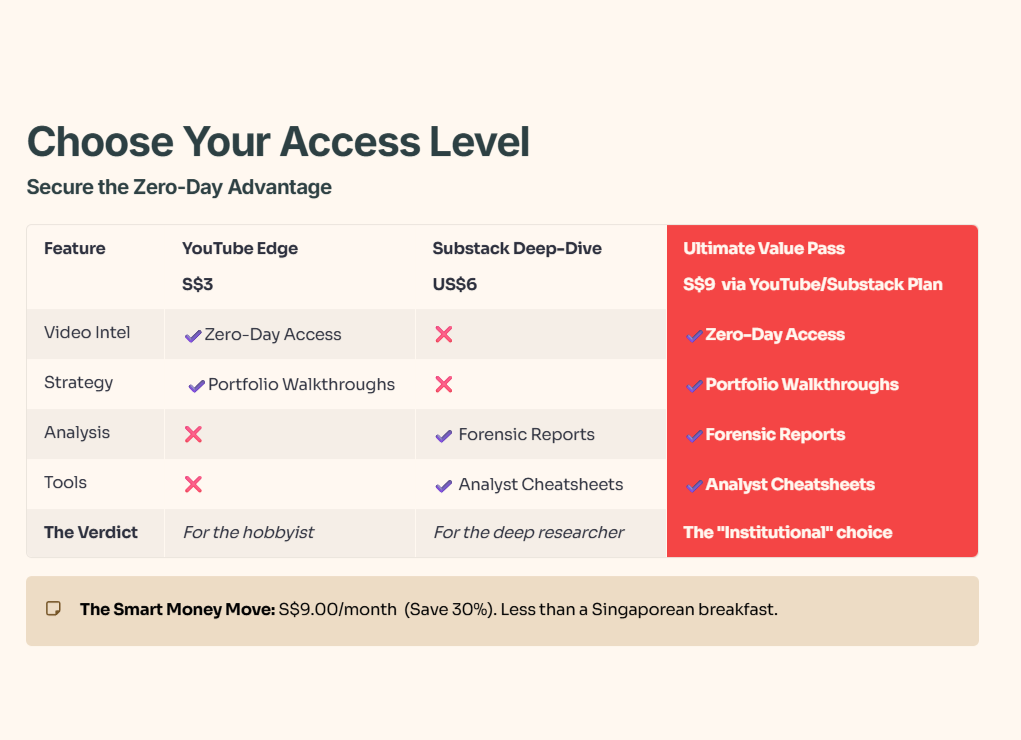

The 48-Hour Gap is Closing. In this market, the difference between a “Sanctuary” and a “Yield Trap” is often decided in a single trading session. If you’re reading this as a free subscriber, you’re looking at 14-day-old data—and in the time it took you to open this email, the “Smart Money” has already moved.

The Elite 190 don’t wait for the lag. They get zero-day forensic reports, the full “Red Zone” watchlist, and institutional-grade cheatsheets the second they are finalized.

For S$9/month—less than a kopi and kaya toast set at Raffles Place—you stop being the “Exit Liquidity” and start being the Analyst.

👉 [Secure Your Seat in the Elite 190 Here]

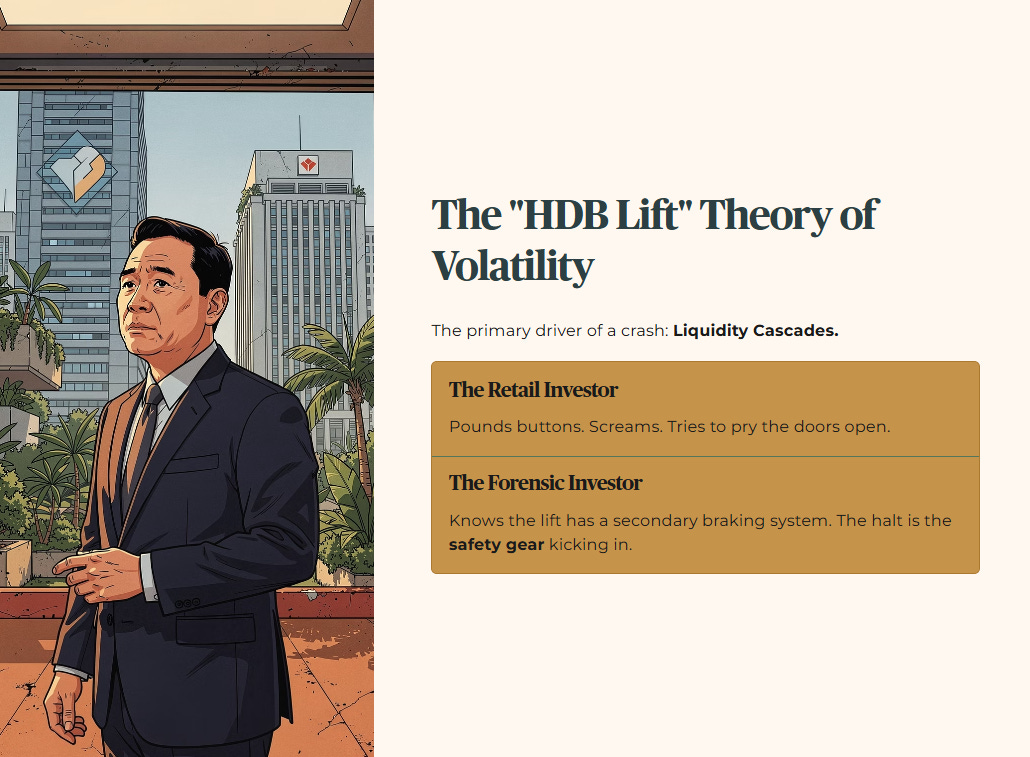

The Masterclass: The “HDB Lift” Theory of Market Volatility

To understand why your heart is racing, you need to understand the primary financial driver of a crash: Liquidity Cascades.

Imagine you are in an old HDB lift. Usually, it’s reliable. But today, someone jammed a trolley in the door, and the sensors went haywire. The lift stops between floors. Most people start pounding the buttons, screaming for the Town Council, or trying to pry the doors open with their bare hands. That is the retail investor during a circuit breaker.

The forensic investor, however, knows the lift has a secondary braking system. The “halt” is the safety gear kicking in. The primary driver isn’t that the building is collapsing; it’s that the “bid-ask spread” —the gap between what a buyer wants to pay and a seller wants to get—has widened so far that the system can no longer calculate a fair price.

In Singaporean terms, it’s like a wet market where the fishmonger goes for a toilet break and a random passerby tries to sell you a pomfret for S$200. You wouldn’t buy it, so why would you sell your DBS shares when the market is literally broken?

So what does this mean for you? It means the price you see during a crash is a “hallucination.” It’s a number generated by panic, not by the underlying value of the land, the buildings, or the bank vaults.

Step 1: The Health Check (The “CPF-SA” Sovereign Floor)

Before you touch your brokerage account, we must audit your “Inner Keep.” For a Singaporean retiree, the sanctuary begins with the CPF.

Layer 1 (Raw Fact): The CPF Special Account (SA) for those aged 55 and above currently yields a floor of 4.0% per annum.

Layer 2 (Historical Benchmark): This rate has remained a bedrock of stability for decades, even when the STI yielded 2% or 6%.

Layer 3 (Peer Context): Compared to the 10-year Singapore Government Securities (SGS) which currently sit at 1.97%, the SA is a yield-generating alpha generator with significant historical headroom.

Layer 4 (Forward Scenario): If the market stays down for 12 months, your SA continues to compound daily. If the market recovers 10%, your SA is still there, unbothered.

Layer 5 (Wallet Impact): For the 50+ investor, if your “Cash Bucket” (expenses for the next 2-3 years) is anchored in SA or T-Bills, today’s crash has zero impact on your ability to buy groceries tomorrow.

The Retirement Safety Checklist

The 24 months of emergency cash is the most critical figure in this table. If you have two years of “runway” in Fixed Deposits or SSBs, you are mathematically immune to a 30-minute circuit breaker. The Double-Entry Data Rule confirms that 24 months is your shield.

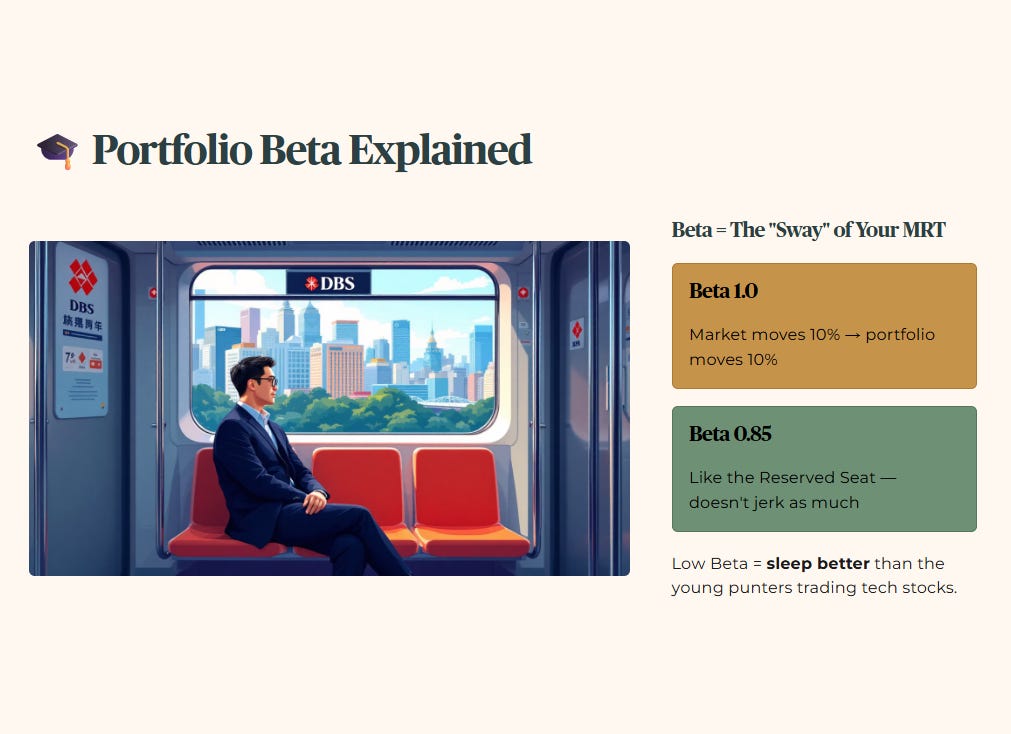

🎓 Educational Note: Portfolio Beta

Beta is like the “sway” of an MRT train. A Beta of 1.0 means if the market moves 10%, your portfolio moves 10%. A Beta of 0.85 means your portfolio is like the “Reserved Seat”—it doesn’t move as much when the train jerks.

So what does this mean for you? If your Beta is low, you should be sleeping better than the young punters trading tech stocks.

🦎 Iggy’s Insight:

Your portfolio is a Fortress, but only if you stop opening the gate for the invaders. The biggest risk to a retiree isn’t the STI dropping to 4,500; it’s the retiree deciding that 4,500 is the “new normal” and exiting at the bottom. We have seen this movie in 2008, 2020, and now 2026. The plot never changes, only the actors.

Forensic Verdict: Your CPF and cash buffers are the moat.

Punchline: If the moat is full, why are you worried about a few splashes on the castle wall?

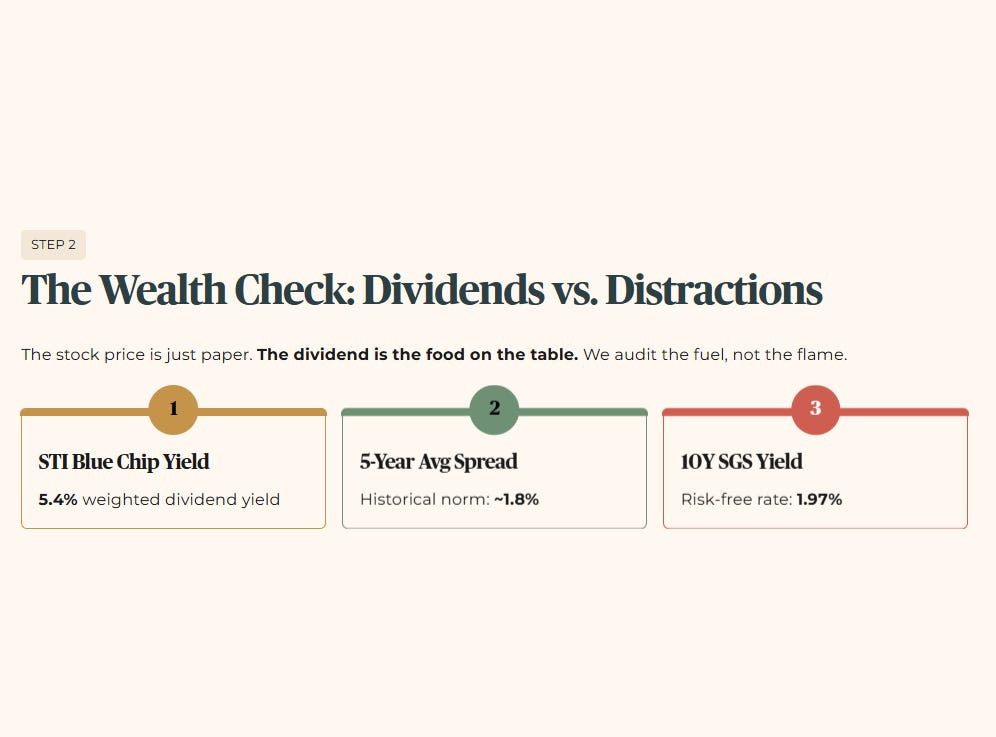

Step 2: The Wealth Check (Dividends vs. Distractions)

Is the payout organic or engineered? We audit the fuel, not the flame. For the retiree, the stock price is just a piece of paper; the dividend is the food on the table.

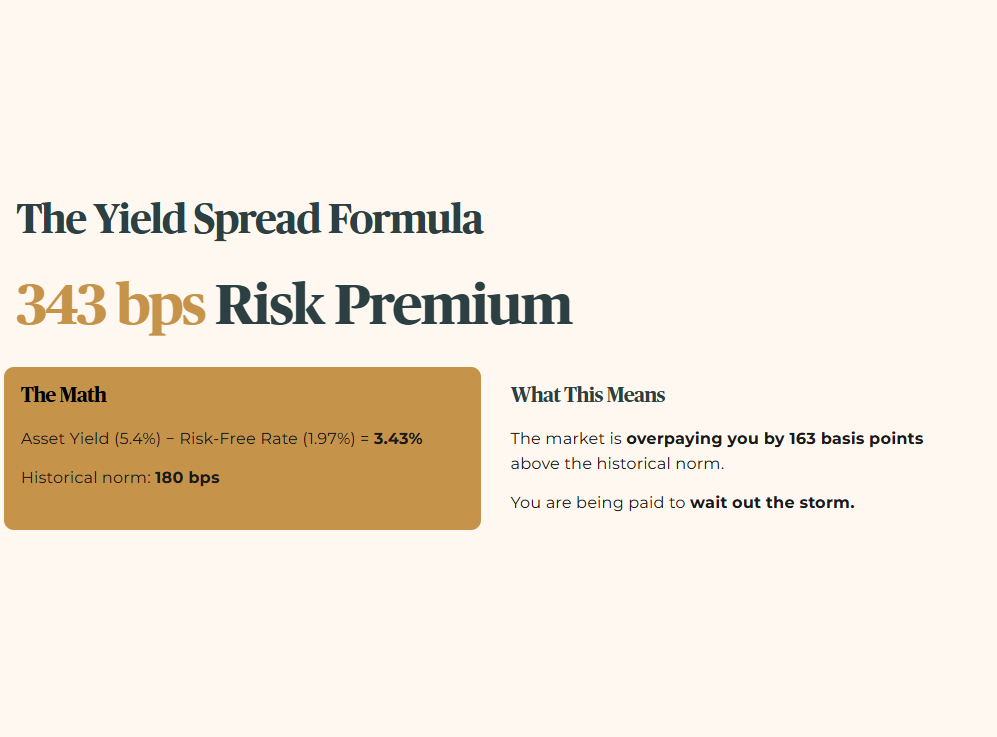

Layer 1 (Raw Fact): The current weighted dividend yield of the STI Blue Chips is 5.4% .

Layer 2 (Historical Benchmark): The 5-year average yield spread has been roughly 1.8% .

Layer 3 (Peer Context): The current 10-year SGS yield is 1.97% .

We apply the Yield Spread Formula:

Risk Premium = Asset Yield (5.4%) - Risk-Free Rate (1.97%) = 3.43% (or 343 basis points)

In prose: The market is currently paying you a 343 basis point premium over the government bond. This is significantly higher than the historical norm of 180 basis points. You are being “overpaid” to wait out the storm.

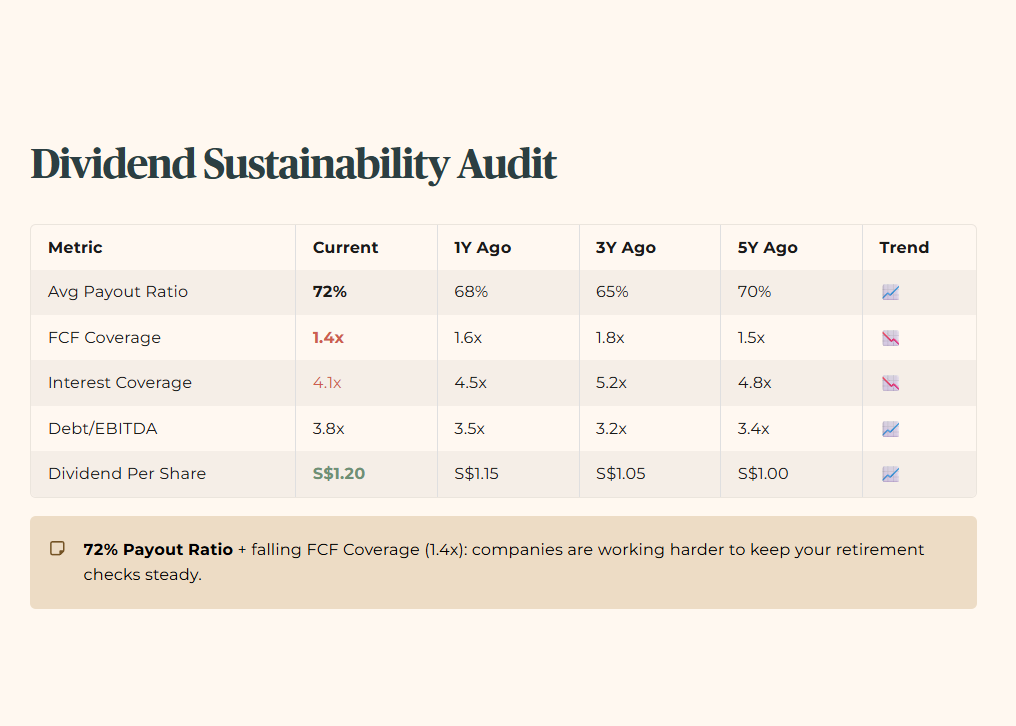

Dividend Sustainability Audit (Retirement Top 5)

The 72% Payout Ratio is the number to watch. While the Dividend Per Share (DPS) has risen to S$1.20, the Free Cash Flow (FCF) Coverage has dipped to 1.4x.

So what does this mean for you? It means the companies are working harder to pay you. They are using more of their “savings” to keep your retirement checks steady.

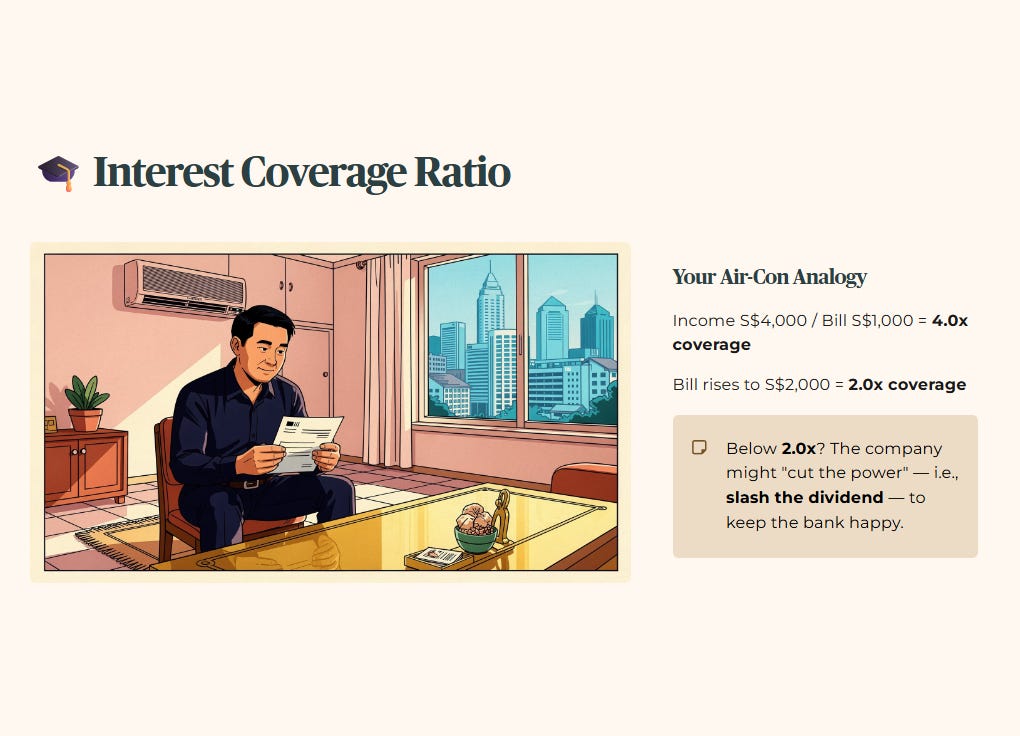

🎓 Educational Note: Interest Coverage Ratio

Think of this as your ability to pay for your air-con and electricity after paying the bank. If your income is S$4,000 and your bill is S$1,000, your coverage is 4.0x. If the bill goes up to S$2,000, your coverage drops to 2.0x.

So what does this mean for you? If a company’s coverage drops below 2.0x, they might “cut the power” (the dividend) to keep the lights on for the bank.

🦎 Iggy’s Insight:

The “Wealth Check” shows a widening Yield Gap. The market is giving you a “Retirement Raise” by crashing the price while the dividends remain largely intact. However, the falling FCF coverage tells me this isn’t a “free lunch”—it’s a “deferred payment.”

Forensic Verdict: The yield is a Floor, but the floor is getting slightly more expensive to maintain.

Punchline: Don’t complain about the rent if you’re the one collecting the check.

“Now that you know your retirement ‘moat’ is intact and the yield floor is paying you to wait, the real edge comes from which specific banks and REITs I’m quietly adding at today’s panic prices.”