CPF vs. SGX Stocks: The $75,000 "Safety" Cost (Iggy's Insights)

Inflation is eating your bond yields alive. Here’s the mathematical case for an equity-focused retirement, despite the risks.

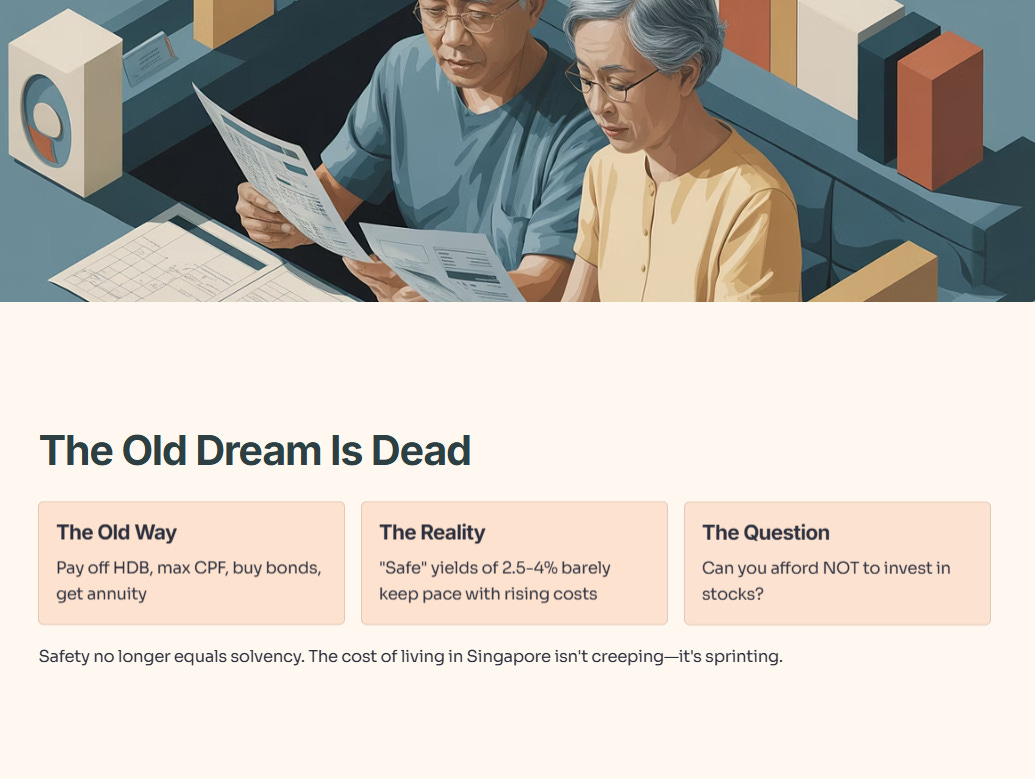

The dream of the Singaporean retirement used to be simple: Pay off the HDB, max out the CPF, buy a few bonds, and perhaps an annuity. It was a strategy built on the assumption that safety equals solvency.

But looking at recent analysis from The Smart Investor regarding retirement on stocks alone, a harsh reality is setting in for many of us in the 45+ bracket. The cost of living in Singapore isn’t just creeping up; it’s sprinting. The “safe” yield of 2.5% to 4% is barely keeping your head above water.

The question isn’t “Is it risky to retire on stocks?” The real question is: “Can you afford not to?”

Today, we are stripping away the emotional comfort of cash and looking at the raw mathematics of an equity-focused retirement.

The Inflation Hedge: Dividends vs. The “Cai Fan” Index

Most investors focus on yield (the percentage paid today). Smart investors focus on growth (the purchasing power of tomorrow).

If you are retiring today, your biggest enemy isn’t a market crash; it’s the slow erosion of your purchasing power over 20 years. Bonds pay a fixed coupon. If inflation rises, your real income drops. Equities, specifically quality dividend growers, are the only asset class that naturally adjusts for this.

Let’s look at the data on SGX (Singapore Exchange) as a proxy for this mechanic.

Iggy’s Insight:

This gap of nearly 1% between dividend growth and inflation is the difference between a comfortable retirement and a downgrade in lifestyle. You aren’t buying stocks for the price appreciation; you are buying them because they are the only machine capable of printing money faster than the central bank devalues it.

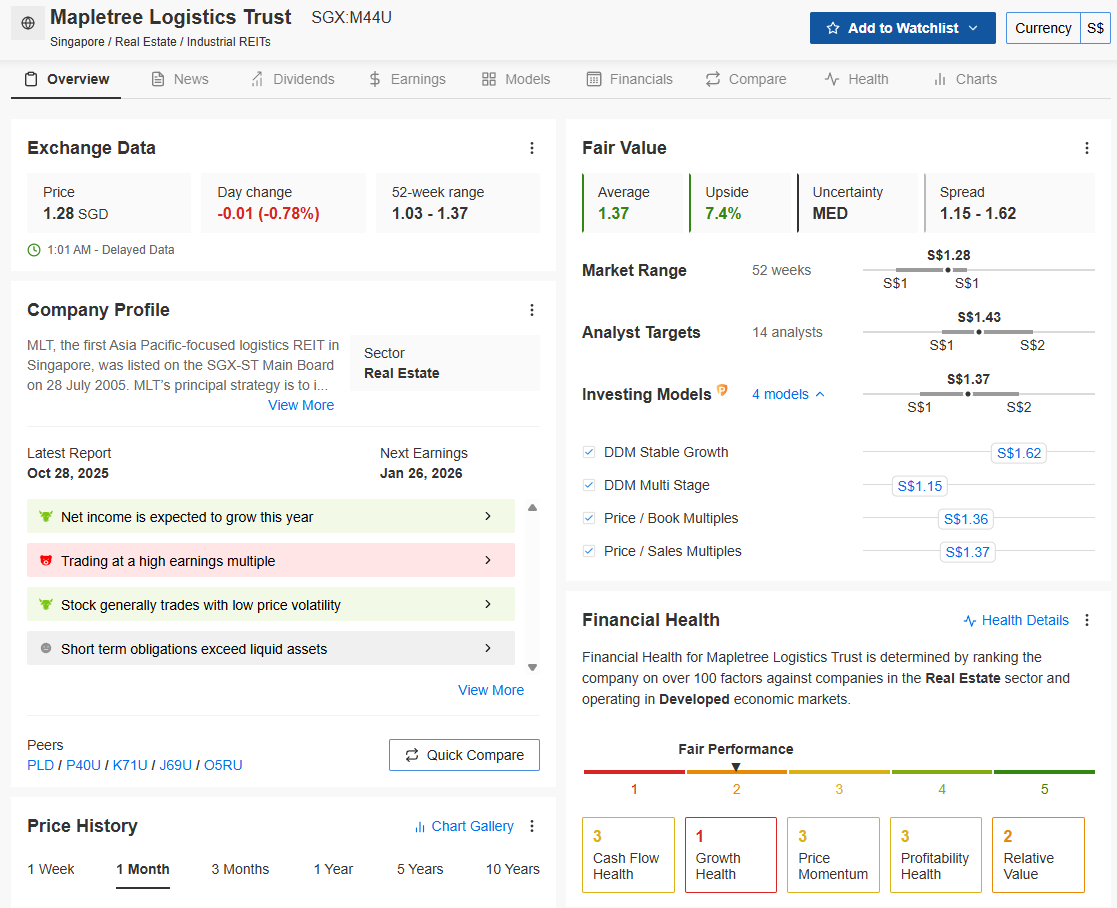

However, this growth isn’t guaranteed. We saw Mapletree Logistics Trust (MLT) pushing 5% growth annually, only to hit a wall when interest rates spiked. This brings us to the critical necessity of analyzing the quality of that dividend.

The “Deep Dive” into Valuation and Safety

It is easy to chase a 6% yield. It is much harder to find a 6% yield that will be here in ten years. When we look at retirement stocks, we cannot guess. We need to look at the payout ratios and the balance sheet health.

Iggy’s Take:

A high yield is often a distress flare, not a gift. If a REIT is yielding 8% while the risk-free rate is 3%, the market is pricing in a cut. Never buy headline yield without checking the cash flow plumbing.

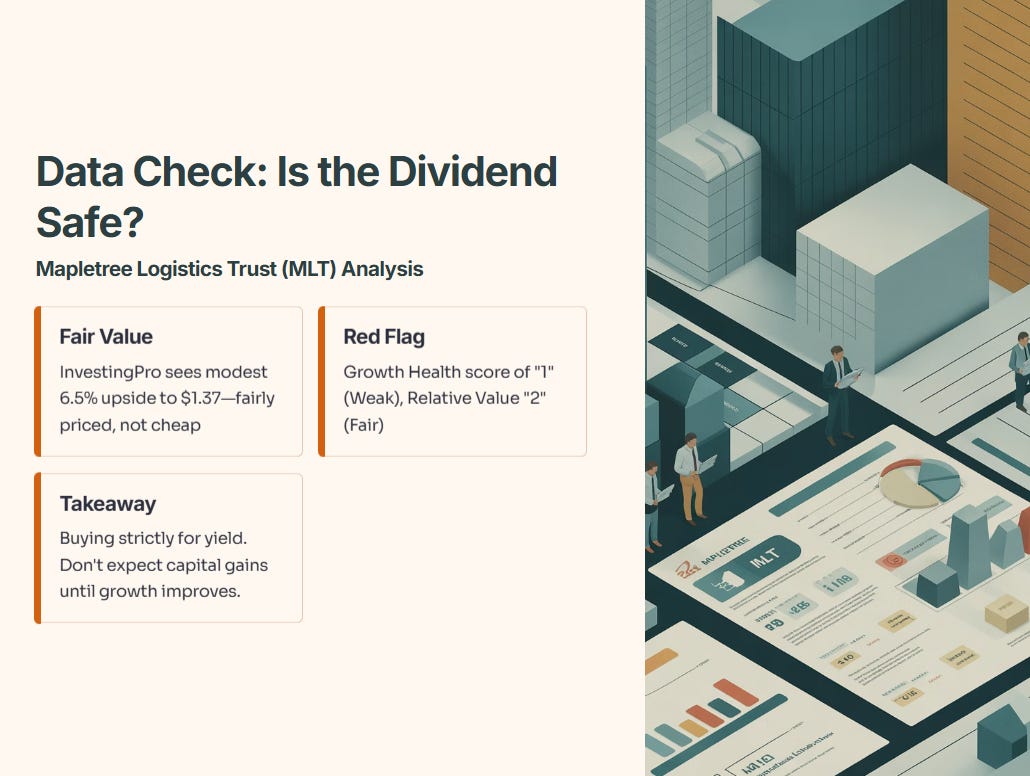

DATA CHECK: IS THE DIVIDEND SAFE?

I don’t just guess at valuations. I check the institutional models to see if the growth story is intact. Let’s look at Mapletree Logistics Trust (MLT), which many of you are holding for recovery.

Source: InvestingPro (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: The models paint a cautious picture.

Fair Value: InvestingPro sees a modest 6.5% upside to $1.37. It’s not screaming “cheap,” it’s screaming “fairly priced.”

The Red Flag: Look at the Financial Health scores at the bottom. Growth Health is a “1” (Weak) and Relative Value is a “2” (Fair). This confirms why the stock has struggled—the growth engine has stalled due to high rates, even if the assets are good.

The Takeaway: When the “Growth Health” is this low, you are buying strictly for the yield. Do not expect capital gains until that score improves.

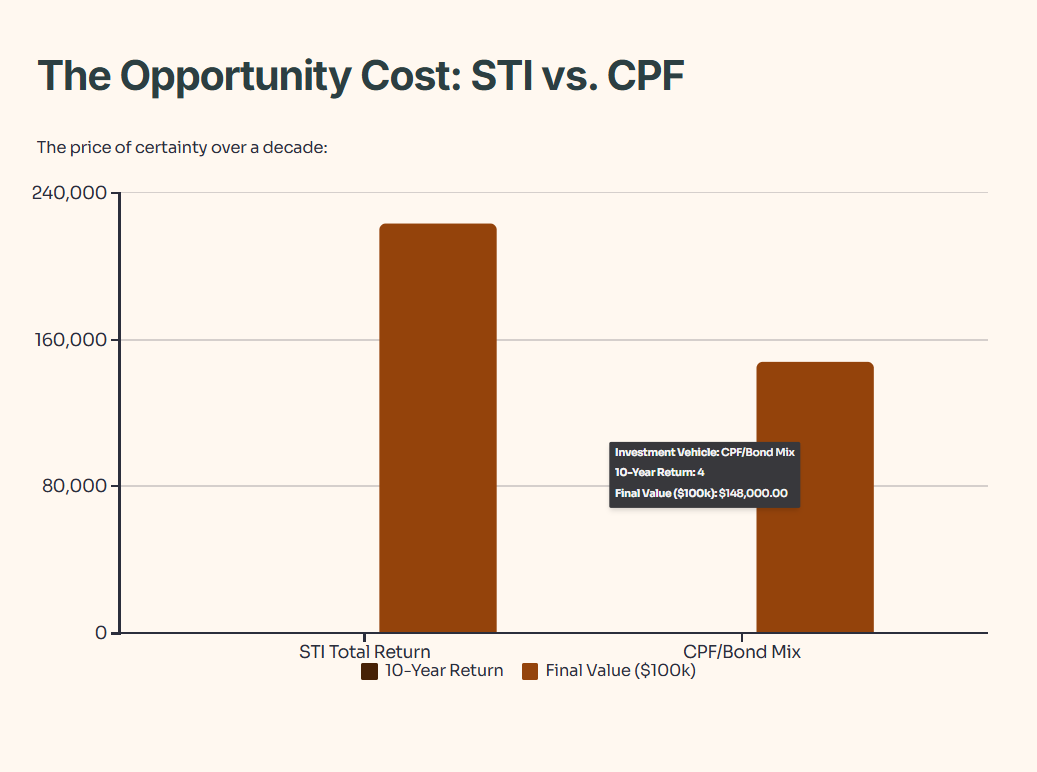

The Opportunity Cost: STI vs. CPF

Many of you prefer the certainty of CPF Special Account (4%) or T-Bills. That is understandable. But let’s look at the cost of that certainty over a decade.

If we compare the Straits Times Index (STI) total return (including reinvested dividends) against the “Risk-Free” rate, the divergence is massive.

Iggy’s Insight:

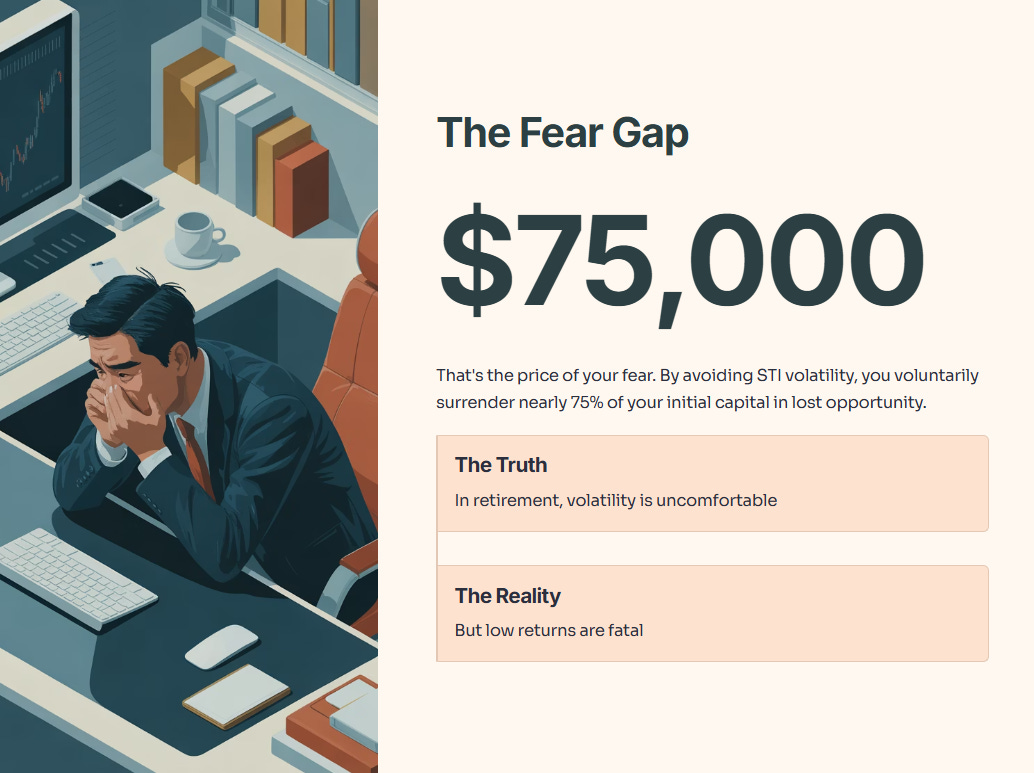

That $75,000 difference is the price of your fear. By avoiding the volatility of the STI, you are voluntarily surrendering nearly 75% of your initial capital in lost opportunity. In retirement, volatility is uncomfortable, but low returns are fatal.

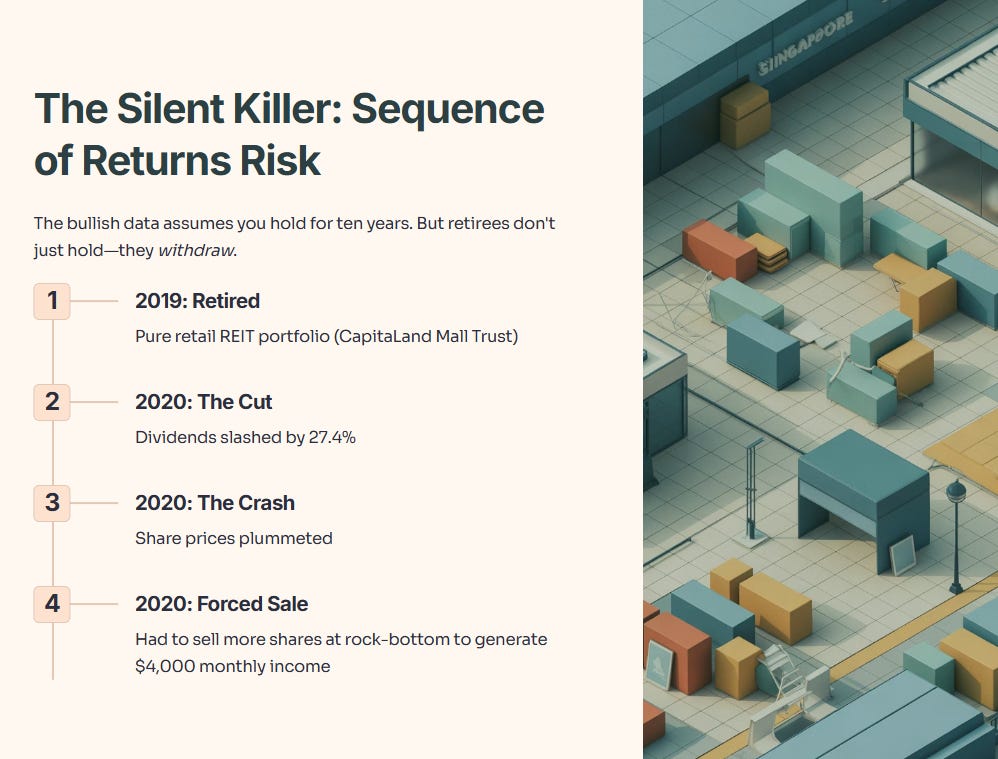

The Silent Killer: Sequence of Returns Risk

The bullish data above has a major caveat. It assumes you hold for ten years. But retirees don’t just hold; they withdraw.

If you retired in 2019 holding a pure retail REIT portfolio (e.g., CapitaLand Mall Trust), and you needed to withdraw cash for living expenses in 2020:

The Cut: Dividends were slashed by 27.4%.

The Crash: Share prices plummeted.

The Forced Sale: You had to sell more shares at rock-bottom prices to generate the same $4,000 monthly income.

This is Sequence Risk. Even if the market recovers (as CICT did), your portfolio doesn’t, because you sold the assets that would have driven the recovery.

Iggy’s Take:

Diversification is not just about “not putting eggs in one basket.” It is about ensuring that when one sector (Retail) is effectively illegalized by a pandemic, another sector (Banking or Logistics) is still cutting you a check. You need uncorrelated cash flows.

The Investor’s Playbook: How to Execute This