Sentosa Mansion Investor TRAPPED in Private Credit Quicksand

Your offshore dividend is choking on a 2.0x coverage ratio while you are busy paying for CDC voucher meals.

The Private Credit Cocktail Hour: A Forensic Audit of Asia’s Locked Doors

1. The Global Headline (The Storm)

The physical tension currently vibrating through the private banking suites of Raffles Place and Hong Kong’s Central district mirrors the collective panic when the MRT doors jam shut during the evening peak hour. Wealth bankers are frantically pouring champagne at hastily arranged luncheons, desperately trying to calm high-net-worth clients who are demanding answers.

These sophisticated investors just realized their capital is trapped inside the US$1.8 trillion private credit market. The gating mechanisms of massive United States evergreen funds have suddenly slammed shut. They were promised a VIP express lane to double-digit yields, shielded from the volatility of public markets. Now, they are stuck in a dark tunnel, surrounded by asset managers blaming software sector volatility and artificial intelligence disruption for the sudden lack of liquidity.

And look, on the surface, that makes sense. The financial textbook explicitly states that you must accept less liquidity in exchange for a higher yield premium. You buy private credit for the illiquidity premium.

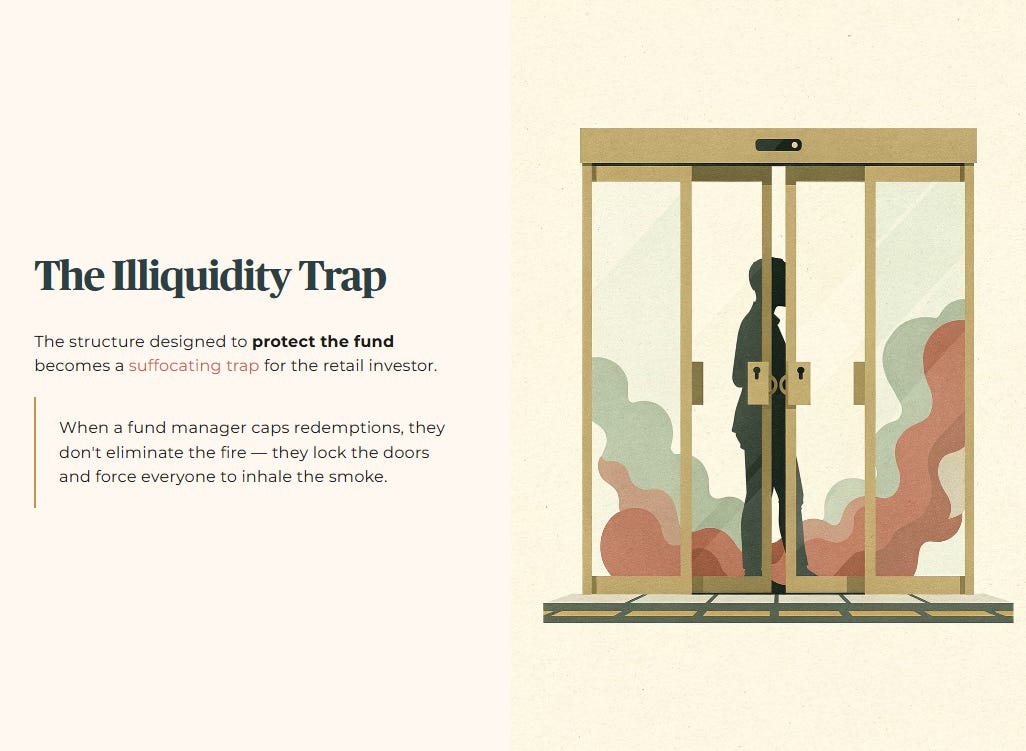

But here is the uncomfortable truth: the very structure designed to protect the fund is now a suffocating trap for the retail investor. When a fund manager caps redemptions to prevent a fire sale of unlisted loans, they do not eliminate the fire. They simply lock the doors, barricade the exits, and force everyone to inhale the smoke.

The underlying assets are bleeding, and the retail investor is acting as the sandbag. For our growing base of Iggy’s Elite Investors, who receive zero-day intel to navigate these shifts before the 7-day lag hits the public, this sudden panic is not a surprise. We warned about the liquidity illusion months ago, tracking the divergence between managed narratives and raw cash flow.

🦎 Iggy’s Insight: The Smart Money understands the psychology of the “Cocktail Hour Diversion.” When massive asset managers start hosting casual drinks and Zoom calls in Singapore just to reassure you about their balance sheets, the institutional money has already sprinted for the exits.

The mechanism is brutally simple: retail investors in Asia are being utilized as the foundational liquidity buffer for American private debt. The psychological shock of a redemption queue triggers primal fear. You realize the “private” in private credit simply means the manager does not have to show you the actual deteriorating price of the asset until it is entirely too late to sell.

In This Article:

The Global Headline (The Storm)

The Local Impact (The Wallet)

The Data Proof (The Evidence)

The Strategic Landscape (Scenario Matrix)

The Singapore Investor Playbook (Forensic Compliance Standards)

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite Investors

The Crash Wasn’t a Surprise. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided before the opening bell — not after the damage is done. The red flags are always there. The question is whether you had the forensic framework to read them in time.

Iggy’s Elite Investors didn’t chase the headline yield. They had the full forensic breakdown — the gearing ratios, the occupancy gaps, the debt overhang — before the market opened and before the price moved. Zero-day reports, the complete “Red Zone” watchlist, and institutional-grade cheatsheets that flag the landmines disguised as opportunities.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

2. The Local Impact (The Wallet)

Translate this macro divergence into the local wallet, and the danger becomes visceral. We are witnessing three specific local consequences that will redefine retirement planning for the Singaporean household.

The first impact strikes directly at the heart of job and income stability within our financial sector. The wealth management industry in Singapore is scrambling to contain the psychological fallout. Relationship managers are working aggressive overtime, frantically trying to draw historical parallels to the 2022 real estate gating events, hoping their clients will simply remain patient and stop demanding withdrawals.

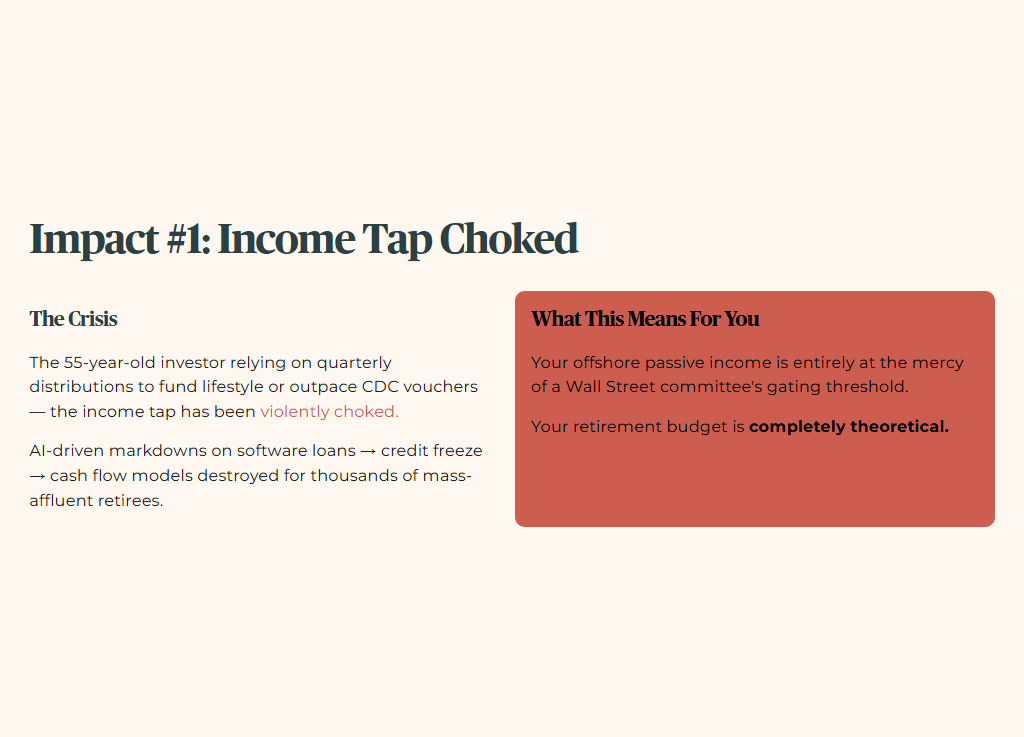

For the 55-year-old investor relying on these quarterly distributions to fund their lifestyle or outpace the shrinking purchasing power of CDC vouchers, the income tap has been violently choked. If a major sub-sector like software loans continues to face artificial intelligence-driven markdowns, the resulting credit freeze will destroy the cash flow models of thousands of mass-affluent retirees. So what does this mean for you? It means your offshore passive income is entirely at the mercy of a Wall Street committee’s gating threshold, rendering your retirement budget completely theoretical.

The second consequence exposes the profound structural irony of our local pension architecture. For years, aggressive financial advisors urged affluent clients to deploy their personal capital into exotic, offshore credit vehicles because the Central Provident Fund and Supplementary Retirement Scheme frameworks were deemed far too restrictive.

Yet, as the offshore private credit market burns and gates slam shut, the rigid, boring structure of the CPF Special Account suddenly looks like the ultimate financial fortress. The risk-free floor of the CPF Special Account (4.0%) remains robust and liquid for its intended purpose, shielding you from the sheer terror of an illiquid mark-to-market bloodbath. So what does this mean for you? It proves that chasing an opaque, unlisted yield while ignoring your foundational domestic sanctuary is a catastrophic miscalculation of risk.

The third impact fundamentally reshapes the dynamics of your domestic SGX portfolio. As frightened capital desperately attempts to flee the gated United States credit funds, we are seeing the beginnings of a safe-haven rotation back to domestic stalwarts. Frightened money does not seek leveraged growth; it seeks structural certainty. The major Singapore banks and blue-chip industrial real estate investment trusts, governed by strict capitalization rules and transparent non-performing loan ratios, represent the ultimate sanctuary. So what does this mean for you? The local stock market, often dismissed by the younger crowd as boring and stagnant, is quietly absorbing the panic-driven capital of the Asian wealth class who simply want to see their money safely accounted for every single day.

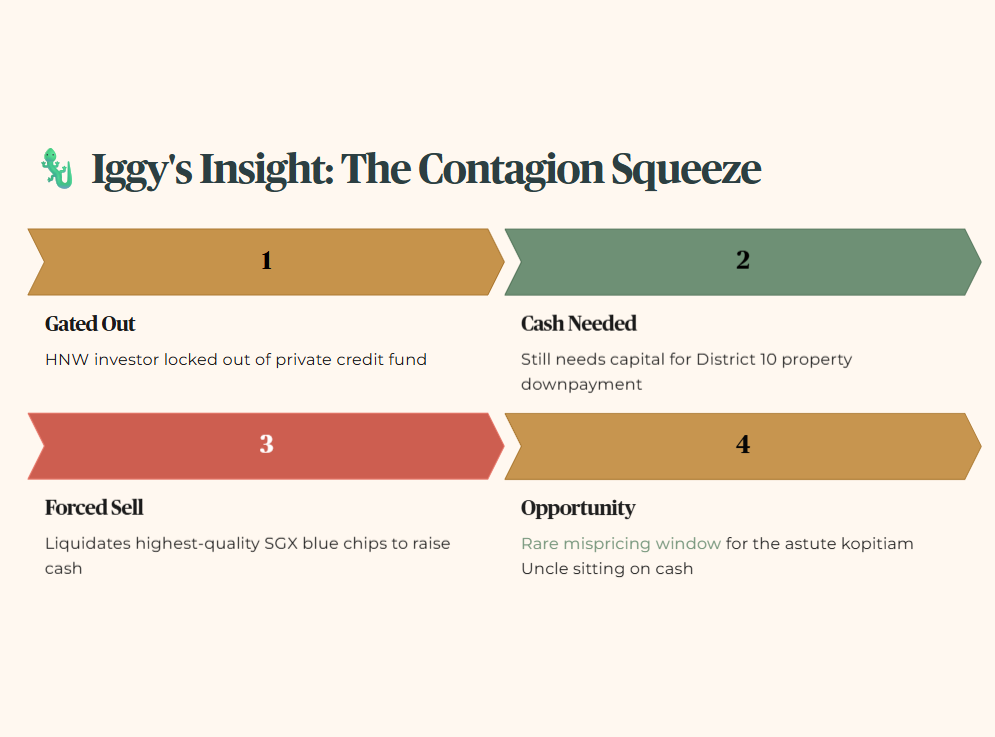

🦎 Iggy’s Insight: The second-order effect retail investors completely miss is the “Contagion Squeeze.” When a high-net-worth individual is gated out of their private credit fund but still needs immediate cash for a property downpayment in District 10, what do they do? They are forced to liquidate their most liquid, highest-quality public assets to raise capital. This means we might see sudden, irrational price drops in pristine SGX blue chips as wealthy investors sell whatever they can, rather than what they want to. This creates a rare, temporary mispricing window for the astute kopitiam Uncle sitting on cash.

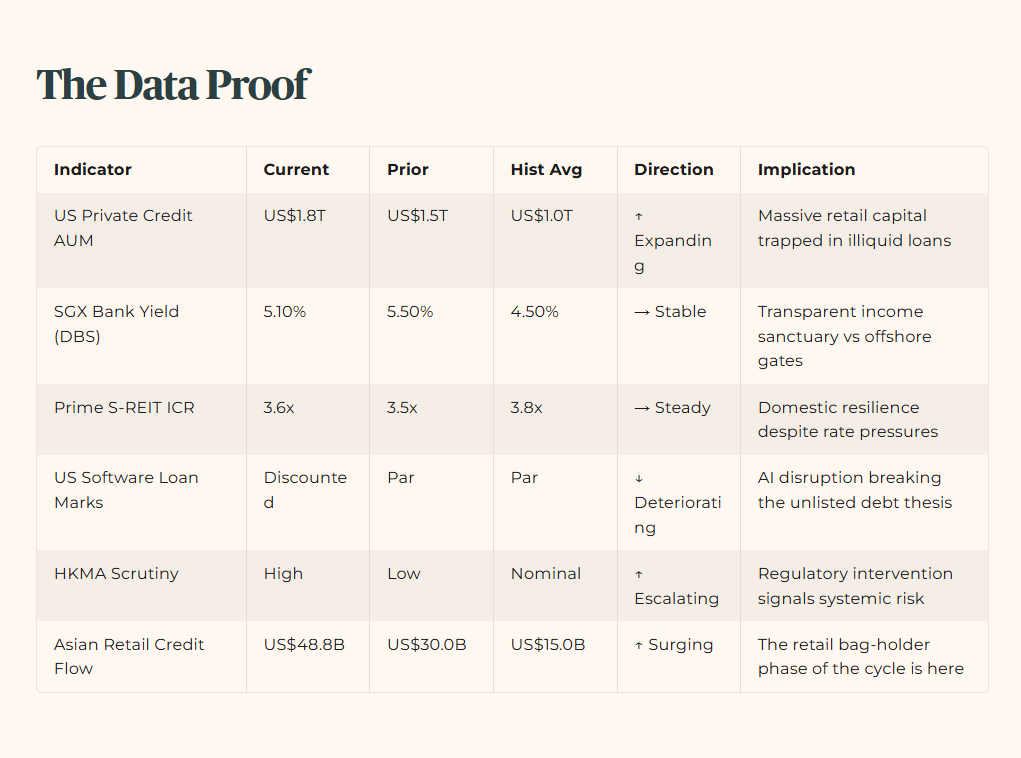

3. The Data Proof (The Evidence)

Are these offshore private credit funds entirely toxic? No. But we must filter their opaque reporting through the institutional math of our public markets to understand the true risk premium. I use the InvestingPro Fair Value model as my stress-test tool for public equities. In this environment, the most vulnerable stocks are those with the widest gap to fair value, heavily dependent on external debt. Use my affiliate code INVESTINGIGUANA to track these metrics yourself.

Table 1: Macro Evidence Dashboard

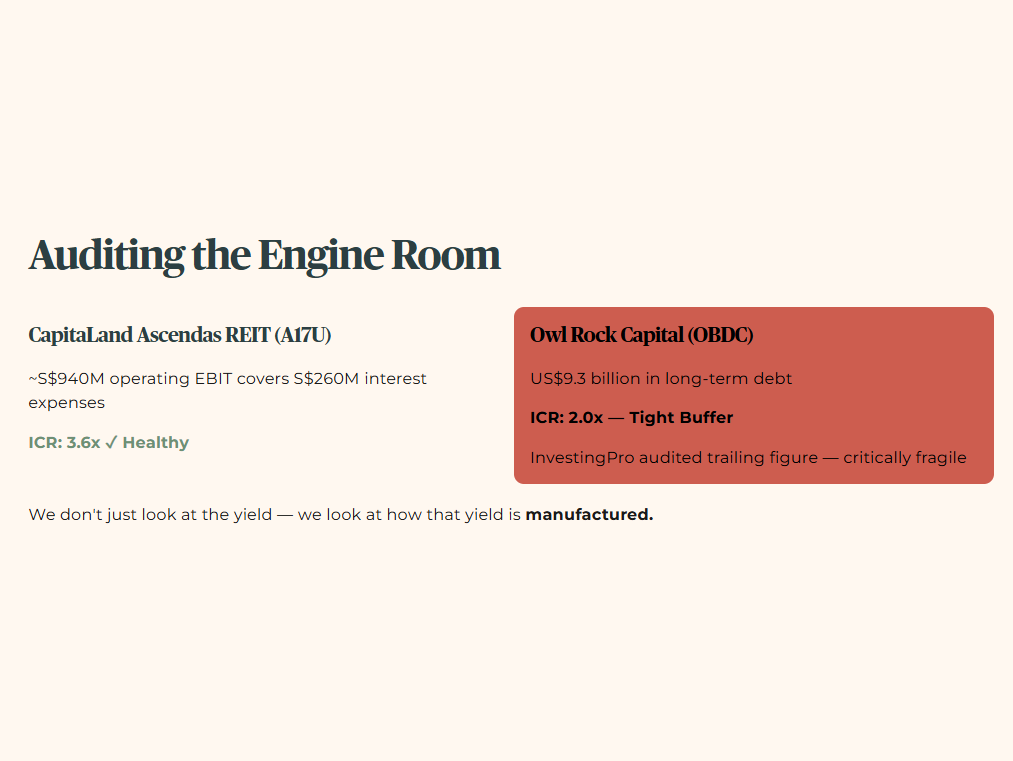

Now, let us audit the actual engine room. A true forensic auditor does not just look at the yield; we look at how that yield is manufactured. Because we are comparing different vehicle structures, we calculate the Interest Coverage Ratio (ICR) directly from the raw Income Statements.

For CapitaLand Ascendas REIT (A17U), the approximately S$940 million in operating EBIT easily covers the S$260 million in interest expenses, generating a healthy, verified 3.6x ICR. Meanwhile, our private credit proxy, Owl Rock Capital Corp (OBDC), is operating with an InvestingPro audited trailing ICR of exactly 2.0x against its US$9.3 billion in long-term debt.

Table 2: Financial Health Checklist (Solvency and Cash Flow Audit)

The number that matters most here is 2.0x, because it exposes the raw fragility of the offshore private credit dividend payout. When an offshore fund sees its interest coverage ratio compress to exactly 2.0x, the double-digit yield is no longer generated by organic business strength; it is a mechanical illusion. InvestingPro’s health checks explicitly flag OBDC for a “poor free cash flow yield.” If just a fraction of those software loans default, that 2.0x buffer evaporates, the dividend is slashed, and the fund gates your capital.

If you’re holding even a single offshore income fund today, there’s a simple 3-check “forensic compliance” test that tells you—within 60 seconds—whether you’re protected… or whether you’re about to become someone else’s exit liquidity.