The 35-Year Lion: Is This Bond Fund a Fortress or Just a Fancy Parking Lot?

Auditing the 4.54% "Mirage"—Why beating the benchmark is a win at the kopitiam but a math puzzle for your CPF.

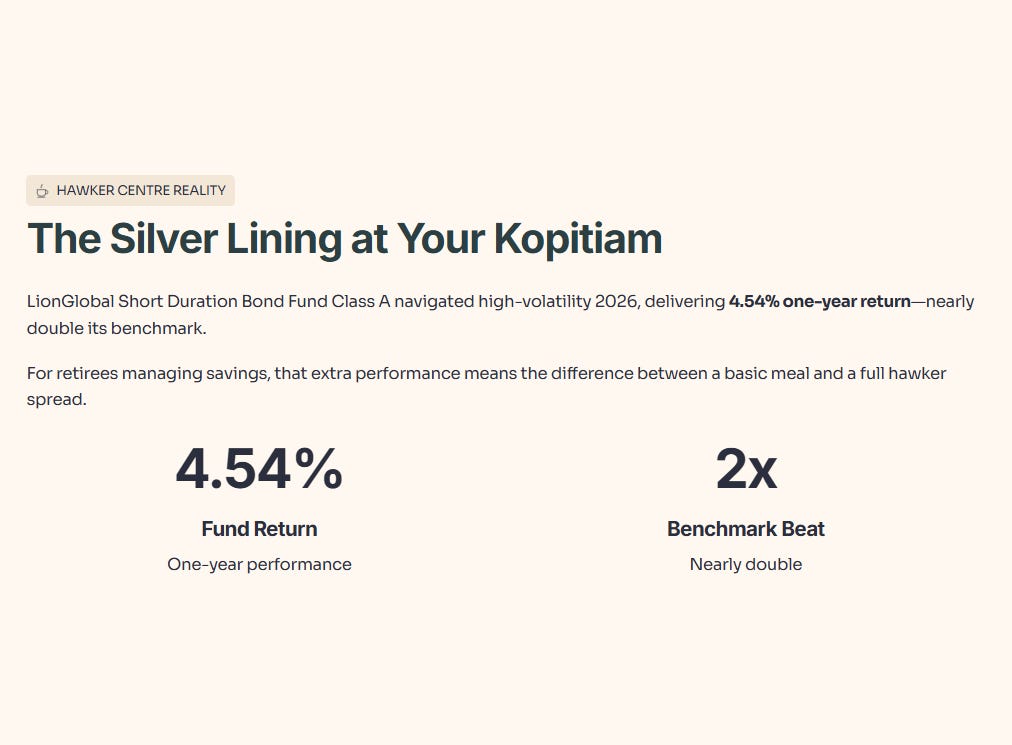

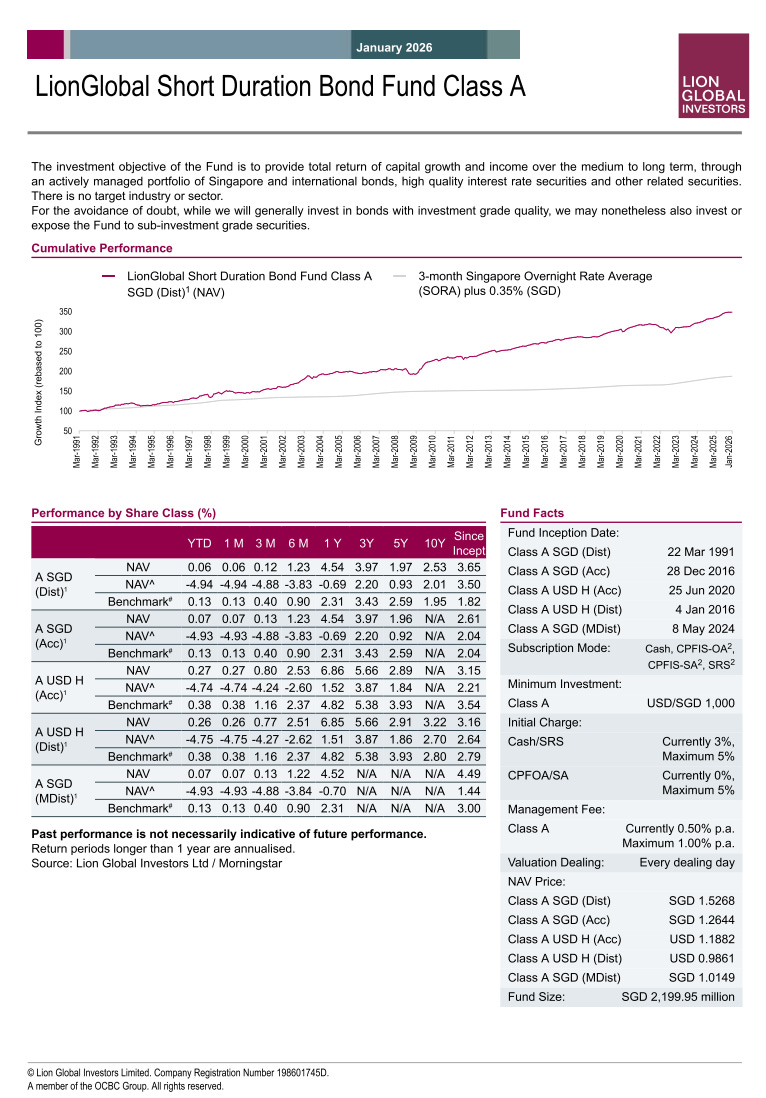

The LionGlobal Short Duration Bond Fund Class A has successfully navigated a high-volatility 2026 environment to deliver a one-year return of 4.54 percent, which is nearly double its benchmark. For a retiree managing their savings, that extra performance is not just a number on a page; it is the difference between a basic meal and a full spread at the hawker centre.

We are now a community of over 170 Paid Elite Members and 6,000 Free Subscribers who look for the truth behind the numbers. This audit highlights the strategic wins and the income stability that management has managed to produce in a tough market. I am a neutral observer providing forensic education, not a licensed adviser.

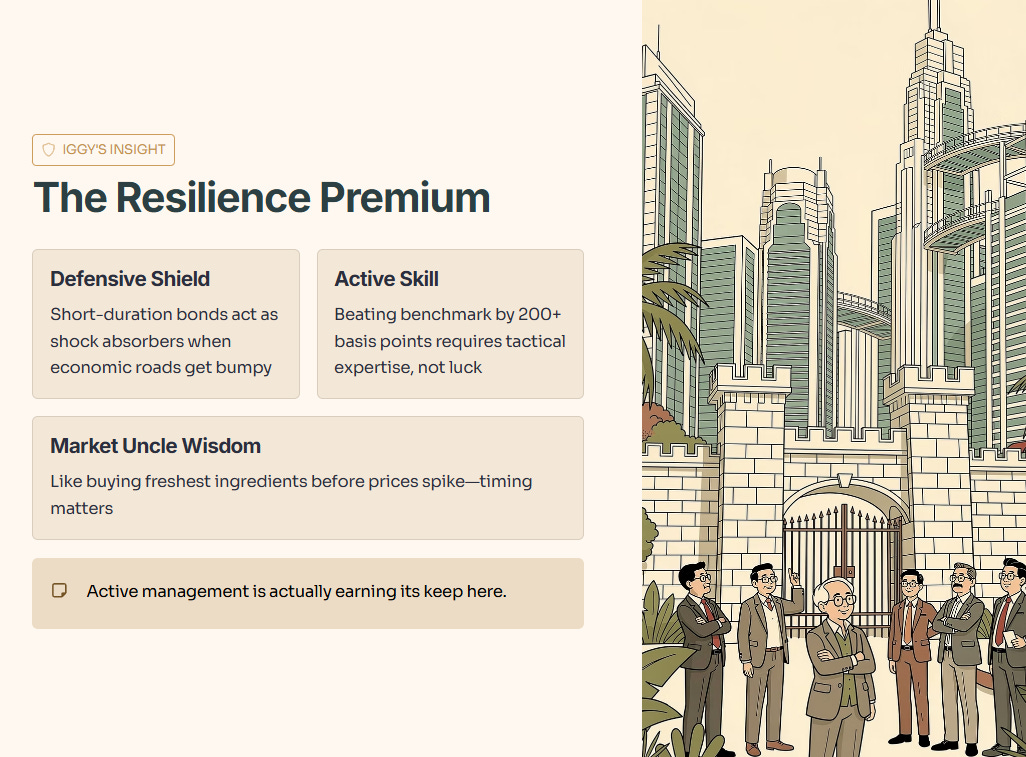

Iggy’s Insight: The Resilience Premium Management has turned this fund into a defensive shield by focusing on the short-duration nature of its bonds, which acts like a shock absorber when the economic road gets bumpy. By keeping the duration short, they have limited the price drops that usually hit long-term bonds when rates stay high, allowing the 4.54 percent return to shine through.

While I am usually the first to point out the impact of fees, we must acknowledge that beating a benchmark by over 200 basis points requires active tactical skill rather than just luck. In the world of global finance, this fund is like the market uncle who knows exactly when to buy the freshest ingredients before the prices spike. The verdict is that active management is actually earning its keep here.

In This Article:

The Slide-by-Slide Audit: Finding the Fortress

Performance and NAV Audit: The Benchmark Beat

Asset Allocation: The Quality Pivot

Top Holdings Audit: The Strategic Mix

The Performance Scorecard: Income You Can Count On

Debt Health Audit: The Refinancing Shield

The Forward Outlook: A Vision of Stability

InvestingPro Reality Check

The VerdictAbout Iggy & the Elite 170

In the Singapore market, the gap between a smart entry and becoming someone else’s exit liquidity can be as little as 48 hours. That’s the cost of informational lag.

Free subscribers get my analysis up to 14 days later. The Elite 170 get it the moment it’s ready.

Your Edge:

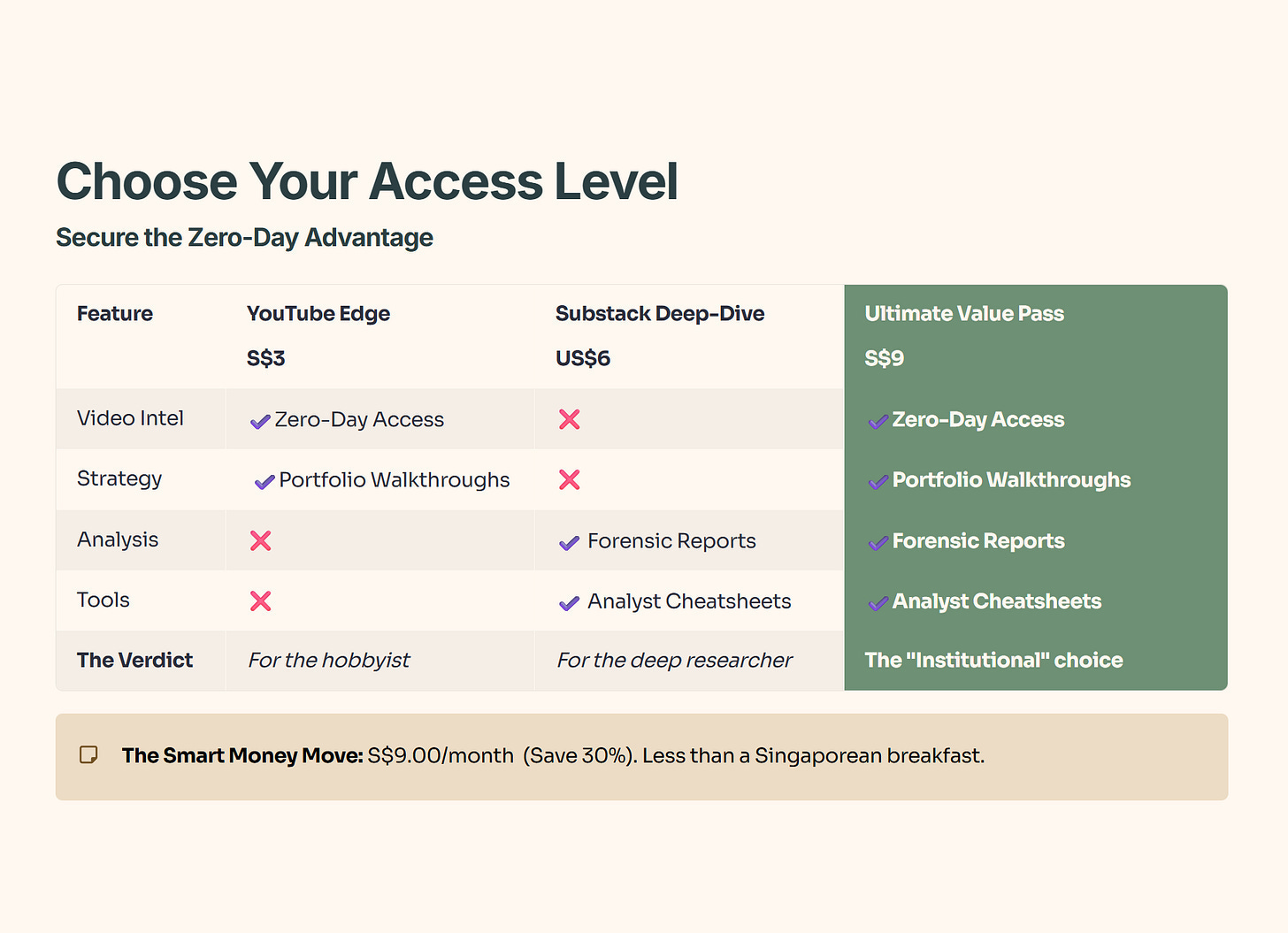

The S$9 Ultimate Value Pass bundles zero-day video intel, forensic reports, and analyst cheatsheets into one institutional-grade feed — for less than a Singaporean breakfast.

The Slide-by-Slide Audit: Finding the Fortress

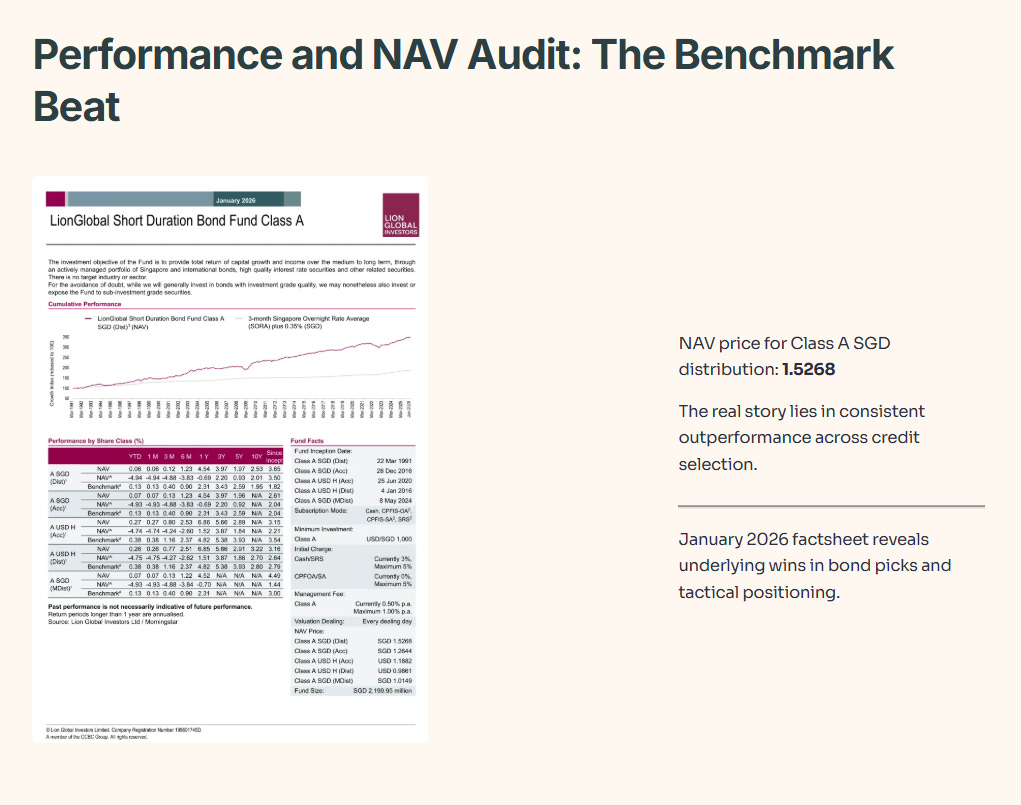

When we look closely at the January 2026 factsheet, the wins start to appear in the underlying credit selection.

Performance and NAV Audit: The Benchmark Beat

The net asset value price for the Class A Singapore dollar distribution share class stands at 1.5268, but the real story is the consistency of the outperformance.

Educational Note: Benchmark Outperformance

Let’s pause on that term. Beating a benchmark is like being the only stall in the wet market that manages to keep prices stable when a supply chain disruption hits. Your benchmark is what everyone else is doing; your outperformance is the extra value you provide through better sourcing. So what does this mean for you? It means the fund manager is actually adding value through their bond picks rather than just riding a market wave.

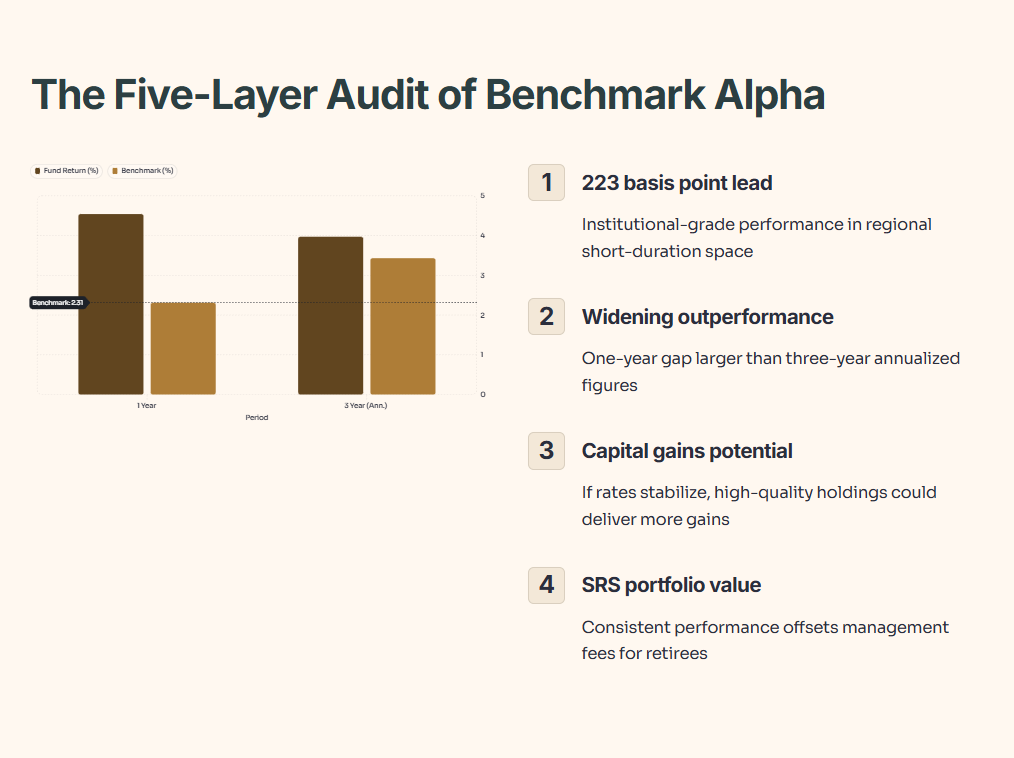

The Five-Layer Audit of Benchmark Alpha

The fund delivered a 4.54 percent return versus the 2.31 percent benchmark over one year. This outperformance has widened compared to the three-year annualised figures, where the fund returned 3.97 percent against a 3.43 percent benchmark. In the regional short-duration space, a 223 basis point lead over the benchmark is institutional-grade performance.

If interest rates enter a more stable phase, these high-quality holdings could lead to more capital gains. For a retiree managing a Supplementary Retirement Scheme portfolio, this consistent performance helps offset the management fee, making the real return more palatable.

“Next, I’ll show you the exact ‘quality pivot’ inside the portfolio—what they’re buying, why it lowers blow-up risk, and the one holding-type that quietly makes this fund behave like a fortress.”