The 4% “Hack” Singapore’s Government Just Closed Forever

On January 19, 2025, roughly 1.4 million Singaporeans woke up to find their CPF Special Account (SA) permanently closed. If you’re wondering why this matters—this deep dive is for you.

On January 19, 2025, roughly 1.4 million Singaporeans woke up to find their CPF Special Account (SA) permanently closed. If you’re wondering why this matters—or worse, if you don’t even know what you just lost—this deep dive is for you.

The CPF SA closure ended one of Singapore’s best-kept financial secrets: SA Shielding. For years, savvy investors used this tactic to squeeze thousands of extra dollars from their CPF accounts. Now that door is shut. But before we talk about what comes next, let’s understand what we just lost.

In This Article:

• What Was CPF Shielding?

• The Transfer Mechanics: Why Order Matters

• How the “Hack” Actually Worked

• Step 1: Understand the Rules

• Step 2: Choose Low-Risk Investments

• Step 3: Execute Before Your 55th Birthday

• Step 4: Let Your Birthday Pass

• Step 5: Liquidate and Return to SA

• Why People Bothered With This Strategy

• The End: Budget 2024 and the SA Closure

• The New Problem for 2025 and Beyond

• The New Reality: Trade-offs You Must Accept

• Iggy’s Take:What Was CPF Shielding?

CPF Shielding was a strategy to maximize your CPF interest earnings. The goal was simple: keep as much money as possible earning 4% interest instead of 2.5%.

Here’s the problem it solved. When you turn 55, CPF creates a new Retirement Account (RA) for you. This RA needs to be filled up to the Full Retirement Sum (FRS), which is $213,000 for 2025. CPF automatically transfers money from your accounts to fill this RA. The transfer happens in a specific order: Special Account funds first, then Ordinary Account funds.

Why does this order matter? Your SA earns 4% interest. Your OA earns just 2.5%. If CPF uses your high-interest SA money to fill your RA, you’re left with more low-interest OA money sitting around. That’s leaving free money on the table.

CPF Shielding flipped this process. By temporarily moving SA money into investments before turning 55, you “hid” it from the automatic transfer. CPF would then use your OA money to fill the RA instead. After your birthday, you’d sell the investments and return the money to your SA. Now you had more money earning 4% instead of 2.5%.

The Transfer Mechanics: Why Order Matters

Let me show you exactly how the old automatic transfer worked.

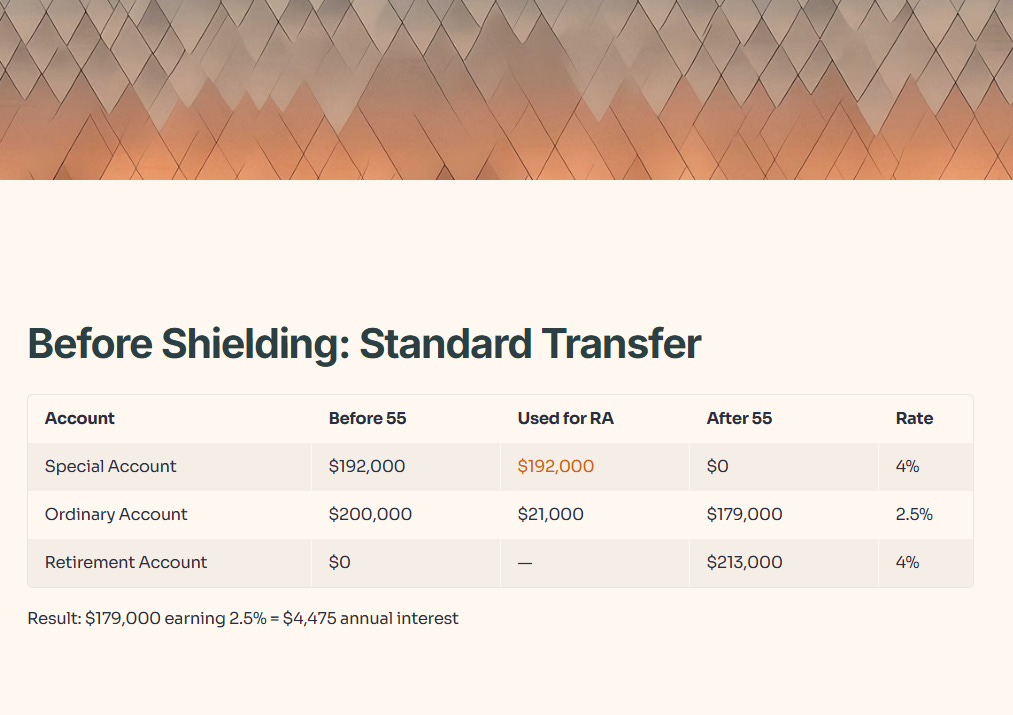

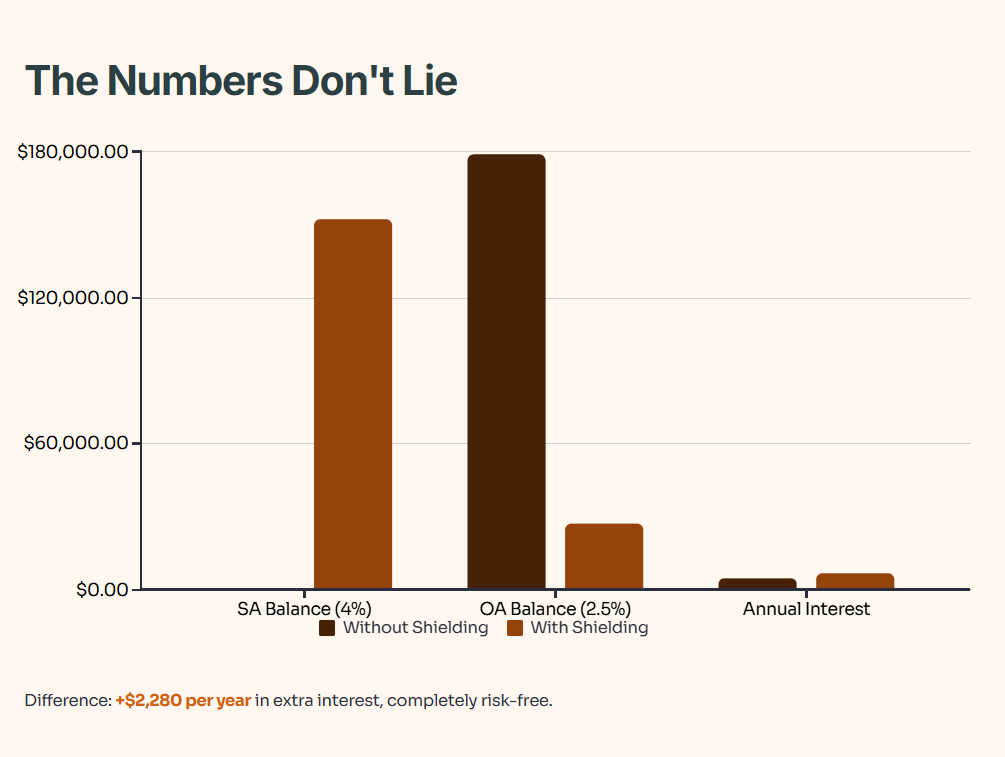

Before CPF Shielding: Standard Transfer Process

In this example, CPF drained your entire SA first. You’re left with $179,000 in your OA earning a measly 2.5%. That’s $4,475 in interest each year.

But what if you could force CPF to use your OA money instead?

With CPF Shielding: Optimized Transfer

Now you have $152,000 earning 4% in your SA and $213,000 earning 4% in your RA. That’s $365,000 at 4% instead of $213,000. The extra interest? $6,080 per year instead of $4,475. That’s an extra $1,605 annually, risk-free.

The difference compounds over 10 years to roughly $17,000 in extra interest. Over 20 years? Nearly $38,000. All without taking a single dollar of investment risk.

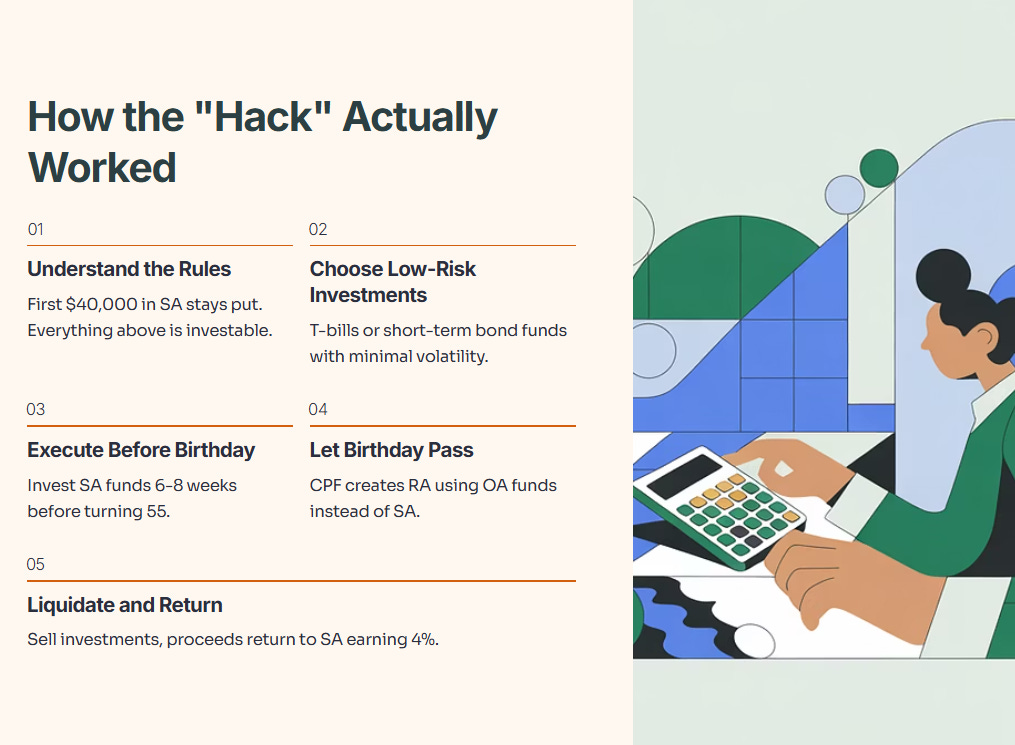

How the “Hack” Actually Worked

CPF Shielding required precision timing and understanding of the CPF Investment Scheme (CPFIS). Here’s how people executed it.

Step 1: Understand the Rules

You can’t invest the first $40,000 in your SA. That money stays put. Everything above $40,000 is fair game for CPFIS-SA investments.

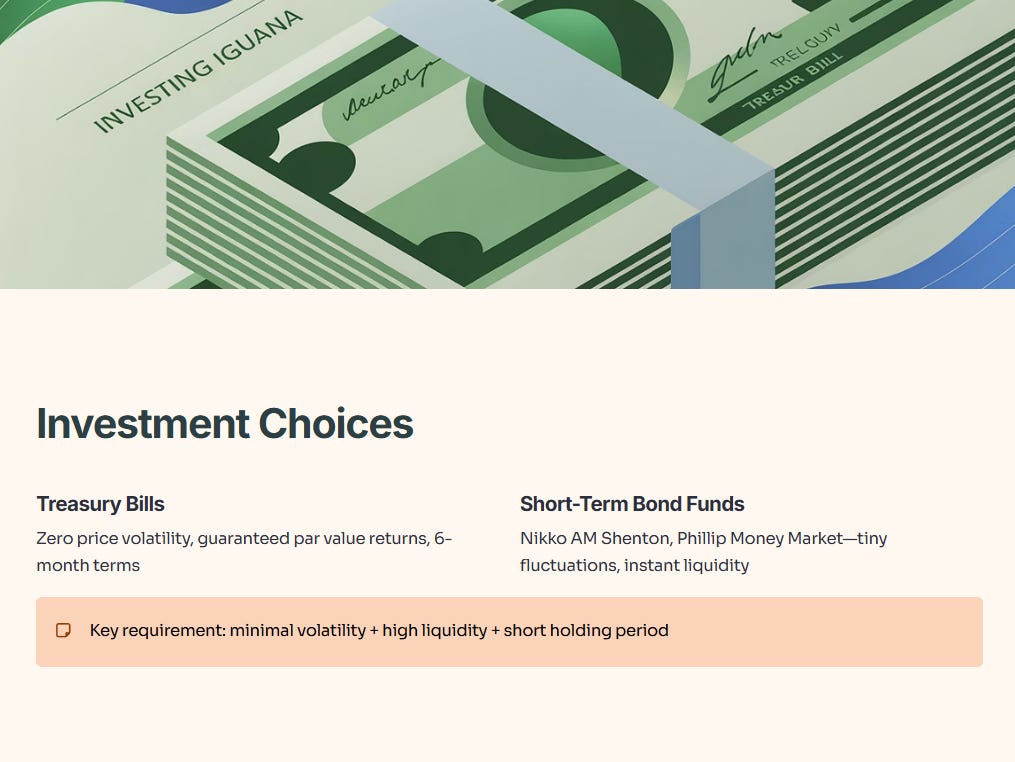

Step 2: Choose Low-Risk Investments

Most people used either Treasury Bills (T-bills) or short-term bond unit trusts. Why? You needed something with minimal volatility, high liquidity, and a short holding period. Popular choices included the Nikko AM Shenton Short Term Bond Fund, Phillip Money Market Fund, or 6-month Singapore T-bills.

T-bills were ideal because they had zero price volatility and guaranteed returns at par value. Short-term bond funds had tiny fluctuations but offered instant liquidity.

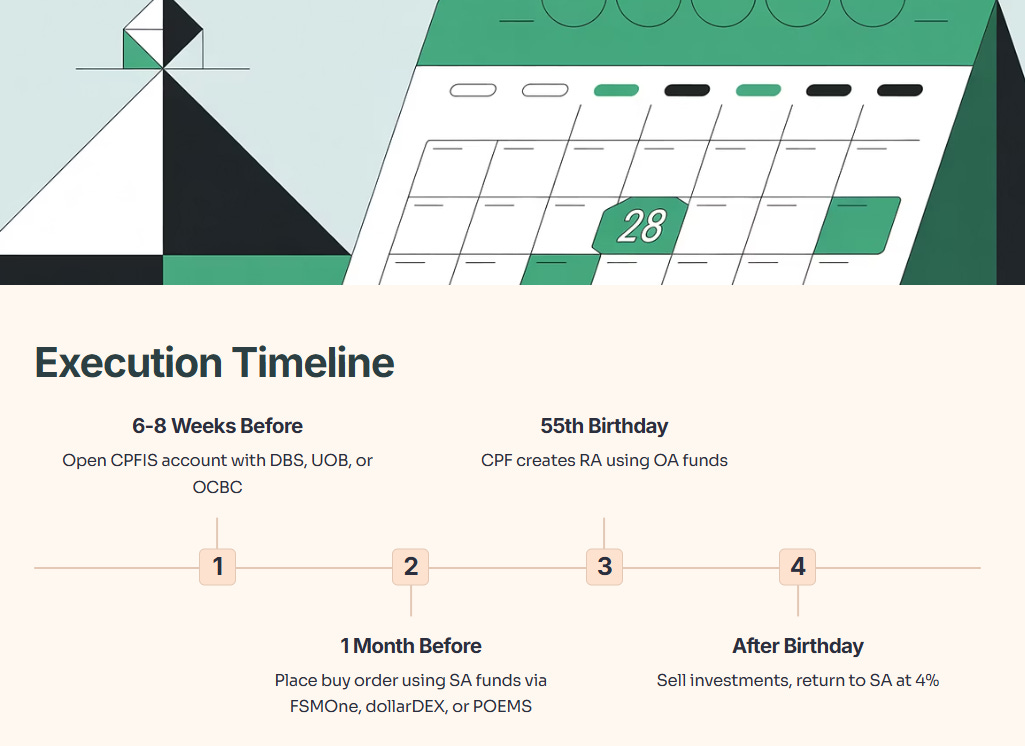

Step 3: Execute Before Your 55th Birthday

Timing was critical. You needed to invest your SA funds (minus the $40,000 minimum) at least one month before turning 55. Most people aimed for 6-8 weeks to avoid missing the cutoff.

You’d open a CPFIS account with a bank (DBS, UOB, or OCBC), open an online trading account (FSMOne, dollarDEX, or POEMS), and place a buy order using your SA funds as payment.

Step 4: Let Your Birthday Pass

On your 55th birthday, CPF created your RA. Since your SA only had $40,000 left, CPF took the rest from your OA to reach the FRS of $213,000.

Step 5: Liquidate and Return to SA

After your RA was formed, you’d sell your investments. The proceeds returned to your SA. This was the magic moment: this money was now both fully withdrawable as cash and earning a risk-free 4% interest, a combination no bank could offer.

Key Benefit of CPF Shielding

The shielded amount created your own high-interest savings account earning 4%, fully withdrawable, completely risk-free.

Why People Bothered With This Strategy

You might wonder: why go through all this trouble for a few thousand dollars a year? The answer lies in liquidity, flexibility, and compounding.

Your RA money is locked until you start CPF LIFE payouts at 65. Even then, you can’t withdraw lump sums. It pays out monthly for life. If you need cash before 65, too bad. Your RA is untouchable.

But your SA was different. After meeting your FRS, any SA balance became withdrawable cash while still earning 4%. This created a unique situation: a government-guaranteed, risk-free account paying 4% that you could access anytime. No bank in Singapore offers this.

CPF Account Comparison: Liquidity vs Returns

The SA gave you both high returns and flexibility. That’s why shielding made sense. You maximized your 4% earnings while keeping the money accessible.

The math was even better for larger balances. If you had $400,000 in combined CPF savings, shielding could create an extra $120,000 earning 4% instead of 2.5%. That’s $1,800 in extra annual interest, compounding over decades.

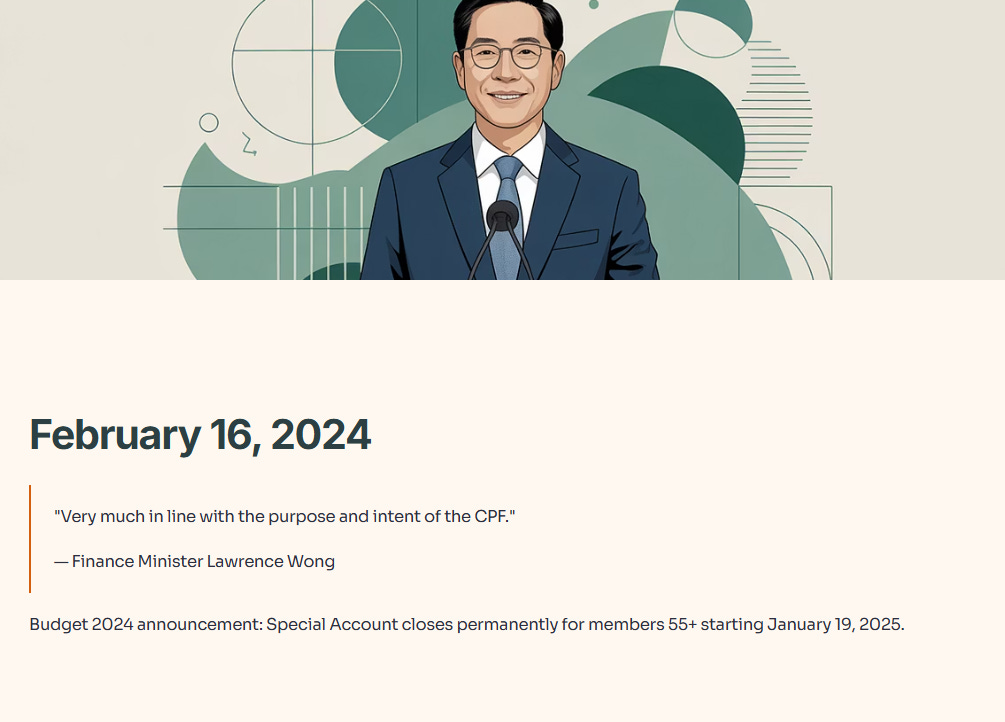

The End: Budget 2024 and the SA Closure

On February 16, 2024, Deputy Prime Minister Lawrence Wong announced the death of CPF Shielding. Starting January 19, 2025, the Special Account would close permanently for all CPF members aged 55 and above.

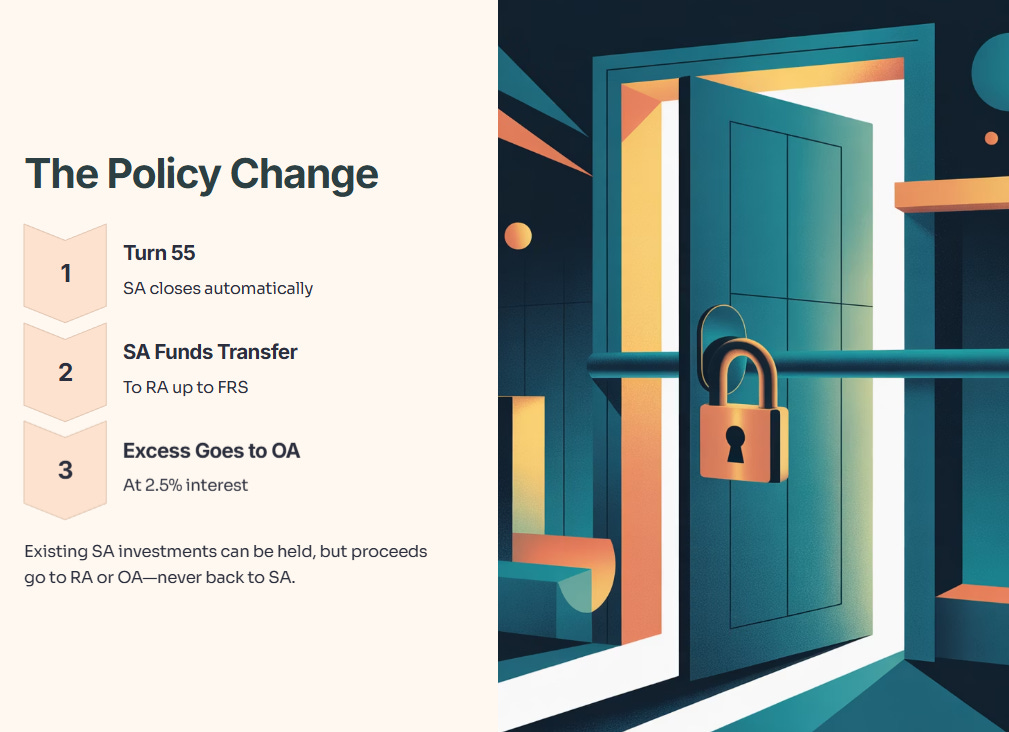

The policy change was straightforward. When you turn 55, your SA closes automatically. All SA funds transfer to your RA up to the FRS. Any excess goes to your OA. There’s no more SA to shield. The account simply disappears.

What happens to existing SA investments made before the closure? You can keep holding them. But when you sell or they mature, the proceeds go to your RA (up to the FRS) or your OA if your RA is full. They don’t return to a non-existent SA.

Post-Closure Money Flow

The government’s reasoning was simple: align interest rates with the nature of savings. Only long-term retirement funds locked in the RA should earn 4%. Money sitting in accessible accounts should earn the lower OA rate.

Finance Minister Lawrence Wong defended the move as “very much in line with the purpose and intent of the CPF.” The SA was designed for retirement savings, not as a high-interest savings hack.

The New Problem for 2025 and Beyond

The SA closure killed the shielding strategy. But the underlying goal remains: maximize your risk-free, high-interest CPF returns while maintaining flexibility.