7 SG Stocks: The "Boring" Strategy with 393% Returns

Why the most compelling growth opportunities are hiding in Singapore’s overlooked corners.

The Paradox of Opportunity

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members.

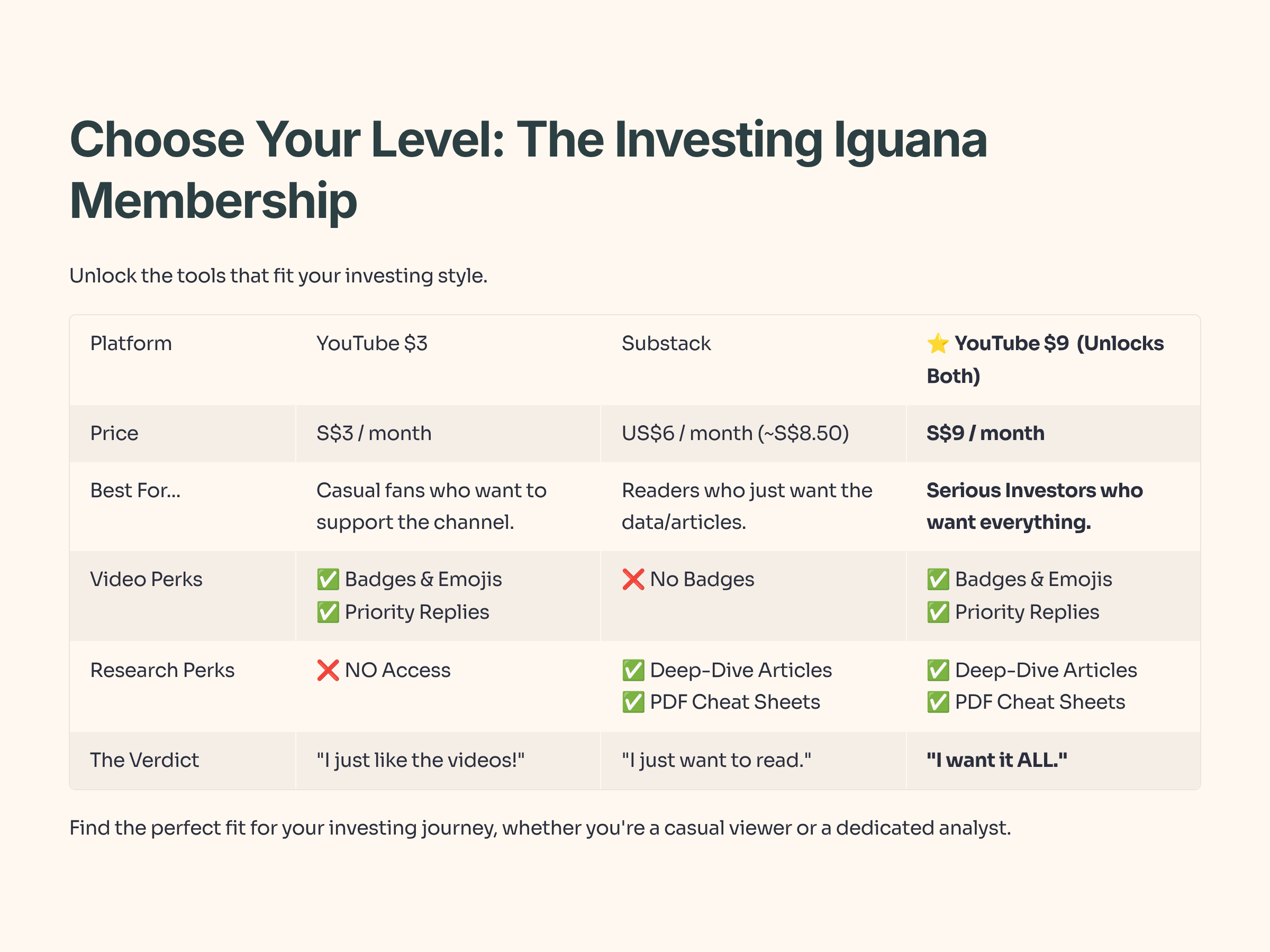

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

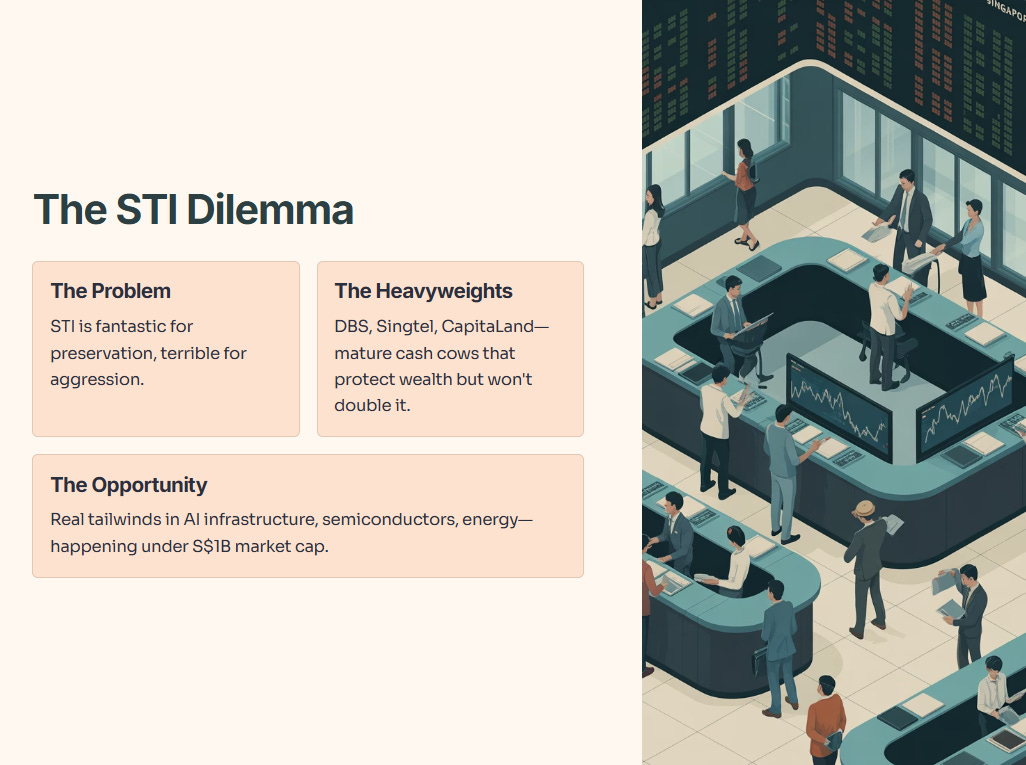

Here is the problem facing the Singaporean investor today: The Straits Times Index (STI) is a fantastic vehicle for preservation, but a terrible one for aggression. The heavyweights—DBS, Singtel, CapitaLand—are mature cash cows. They will protect your wealth, but they are unlikely to double it.

The real tailwinds—AI infrastructure, semiconductor supply chain rebalancing, and energy recovery—are playing out on the SGX right now. But they are not happening in the top 30 components. They are happening in the “under S$1 Billion” market cap space.

Iggy’s Insight:

The lack of analyst coverage in the small-to-mid-cap space is your friend. When big banks don’t cover a stock, pricing inefficiencies occur. That gap between “actual value” and “market price” is where Alpha is generated. We are looking for boring businesses with exciting cash flows.

In This Article:

• The 3 Megatrends Shaping 2026

• UMS Integration & CSE Global

• Frencken Group & InvestingPro Reality Check

• Rest of the 7 lesser known stocks you need to eyeball

• The Playbook: Your Action Plan for 2026

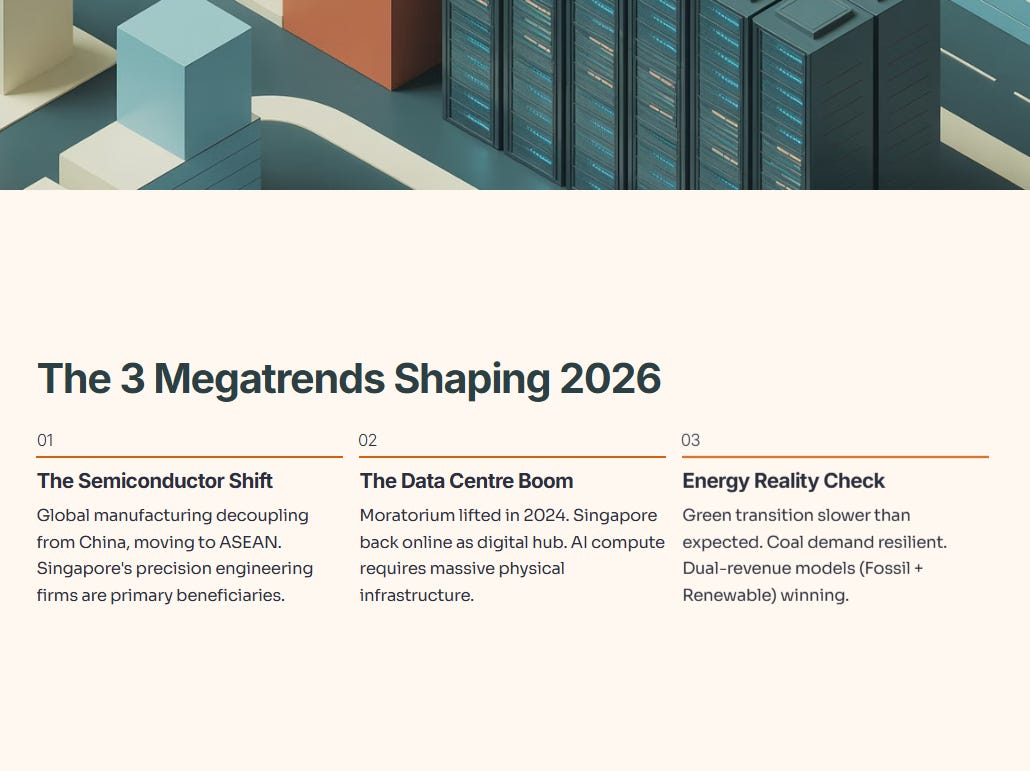

The 3 Megatrends Shaping 2026

Before we look at the tickers, we need to understand the tide lifting these boats.

The Semiconductor Shift: Global manufacturing is decoupling from China and moving toward ASEAN. Singapore’s precision engineering firms are the primary beneficiaries.

The Data Centre Boom: With the moratorium lifted in 2024, Singapore is back online as a digital hub. AI compute requires massive physical infrastructure.

Energy Reality Check: The green transition is slower than expected. Coal demand is resilient, and companies transitioning to dual-revenue models (Fossil + Renewable) are winning.

Let’s dive into the data.

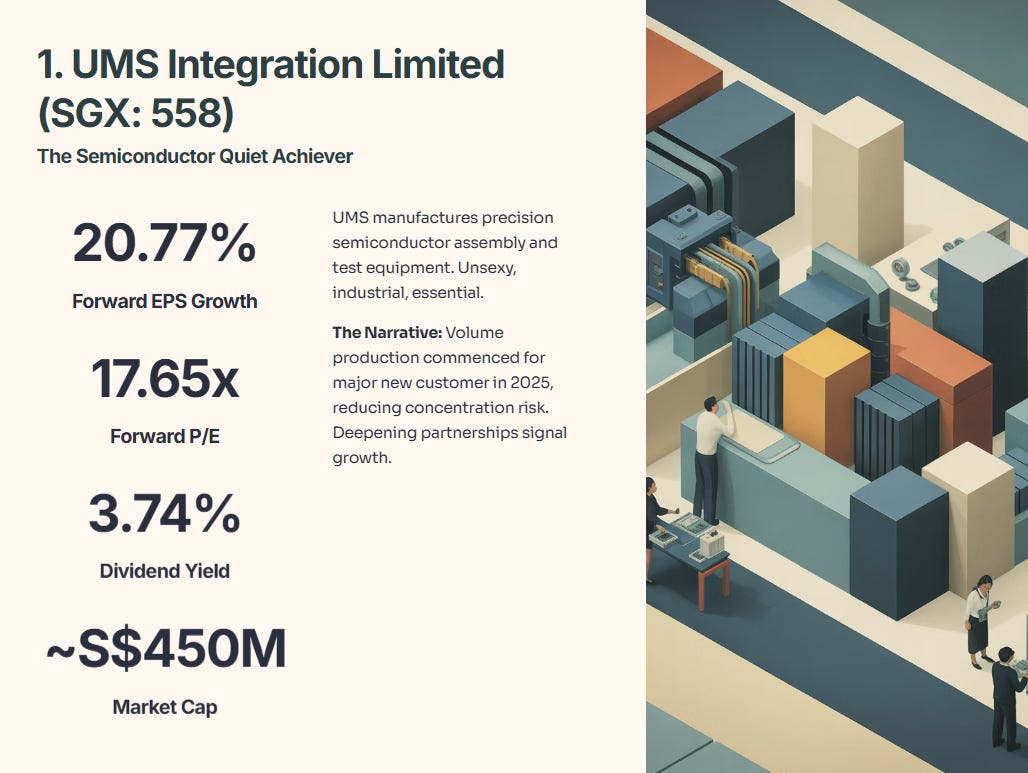

1. UMS Integration Limited (SGX: 558)

The Semiconductor Quiet Achiever

UMS manufactures precision semiconductor assembly and test equipment. It is unsexy, industrial, and essential.

The Narrative: In 2025, UMS commenced volume production for a major new customer. This is critical because it reduces their historical concentration risk on a single key client. Management is now collaborating on new product introductions, signaling a deepening partnership.

Iggy’s Take:

Look at the PEG (Price/Earnings-to-Growth) implied here. Paying 17.65x earnings for a company growing at nearly 21% is a rational trade. Usually, in the tech sector, you pay a premium for growth. Here, you are paying a fair price for a manufacturer that has already secured the contracts.

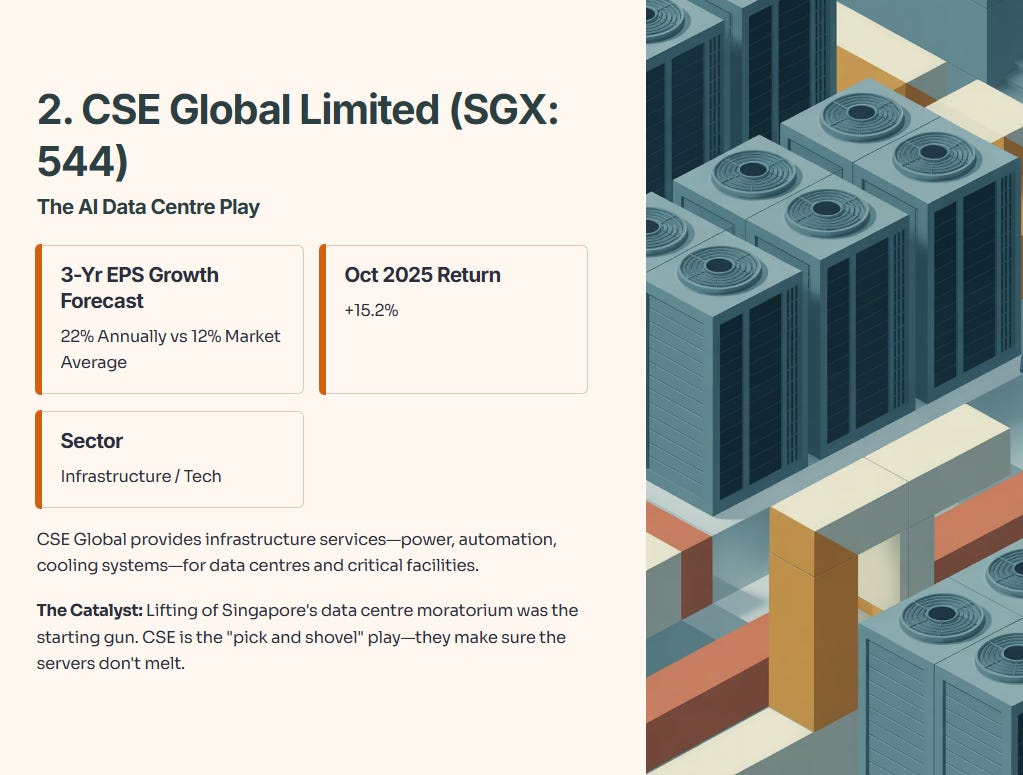

2. CSE Global Limited (SGX: 544)

The AI Data Centre Play

CSE Global provides infrastructure services—think power, automation, and cooling systems—for data centres and critical facilities.

The Catalyst: The lifting of Singapore’s data centre moratorium was the starting gun. Institutional capital is flooding the region to build compute capacity for AI. CSE is the “pick and shovel” play. They don’t own the data; they make sure the servers don’t melt.

Iggy’s Insight:

The market is treating CSE like a standard engineering firm, but it should be valued as a tech-enabler. A 22% annual growth forecast is double the broader market rate. This is a momentum play backed by a tangible order book, not just hype.

🔒 Keep Reading (5 More Stocks + The Action Playbook)

You’ve seen the “hot” AI and Semiconductor plays. But the real wealth in Singapore is often found in the boring, overlooked corners that the institutions are quietly accumulating.

Subscribe now to unlock the remaining 5 stocks, including:

Stock #3 (The Safety Play): A manufacturing giant with 20 years of consecutive dividends and a rare “Double Validation” signal (where both Algorithms and Analysts agree it’s ~23% undervalued).

Stock #5 (The Contrarian Play): The energy stock where analysts see 50% upside, creating a massive divergence from the market pricing. Includes exclusive InvestingPro data breakdown.

Stock #6 & #7: The “Hidden” ESG transition play and the construction stock with an 18% ROE.

The 2026 Playbook: My exact strategy on how to position, size, and execute these trades for a CPF/SRS portfolio.

Join 60+ Premium Members today to get the full Deep Dive.