The 7.5% Yield Paradox: Is CapitaLand Ascendas REIT an Industrial Sanctuary or a High-Gearing Watchlist Trigger?

Like buying premium brand abalone with a dented tin. The content is Grade A, but the "gearing" makes shoppers nervous.

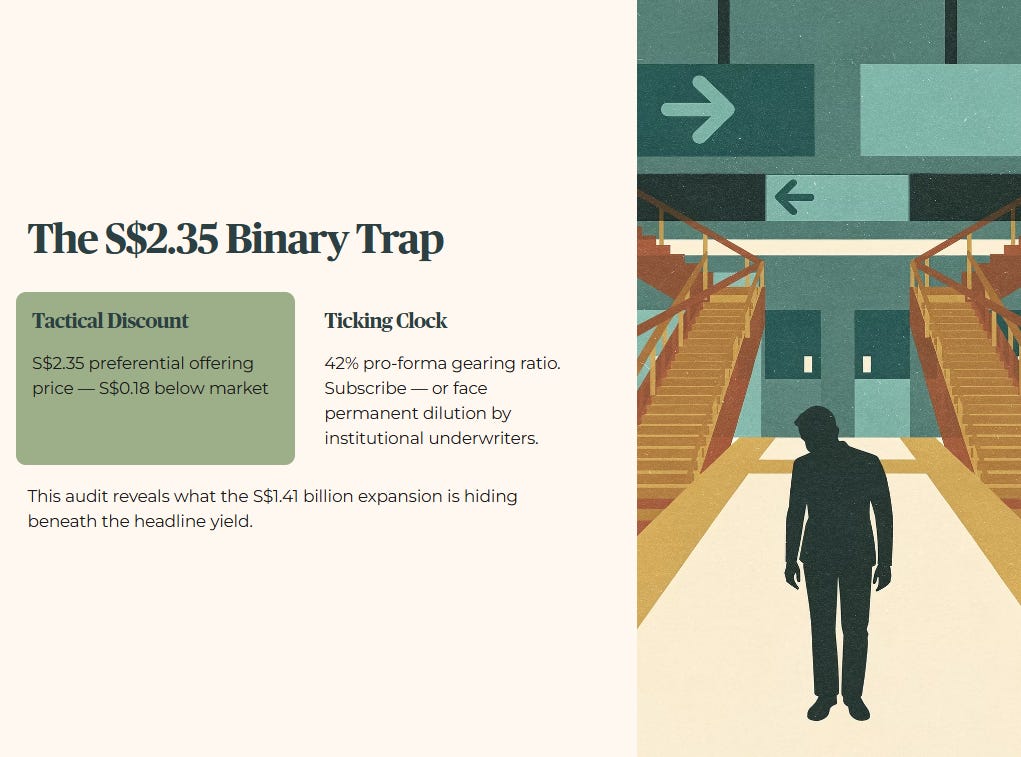

The S$2.35 Binary Trap: Why Your CPF/SRS Portfolio Cannot Afford to Ignore the CLAR Preferential Offering

The S$2.35 preferential offering price and the 42% pro-forma gearing ratio. One of these numbers is a tactical discount. The other is a ticking clock on the balance sheet.

If you are holding this REIT for long-term retirement income, you currently stand in a binary trap: subscribe to the new units, or watch your existing equity be permanently diluted by institutional underwriters. This audit reveals exactly what the management’s S$1.41 billion expansion is hiding beneath the headline yield.

In This Article:

The Five Layer Analytical Floor

Step 1 The Health Check Solvency

Step 2 The Wealth Check Yield and Distribution Trajectory

Step 3 The Price Check Valuation

Step 4 The Anatomy of the S141 Billion Pivot

Step 5 The Bottom Line Forensic Stance

Iggys Forensic Compliance Standards Standard Disclaimer

About Iggy & the Elite Investors

The Crash Wasn’t a Surprise. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided before the opening bell — not after the damage is done. The red flags are always there. The question is whether you had the forensic framework to read them in time.

Iggy’s Elite Investors didn’t chase the headline yield. They had the full forensic breakdown — the gearing ratios, the occupancy gaps, the debt overhang — before the market opened and before the price moved. Zero-day reports, the complete “Red Zone” watchlist, and institutional-grade cheatsheets that flag the landmines disguised as opportunities.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

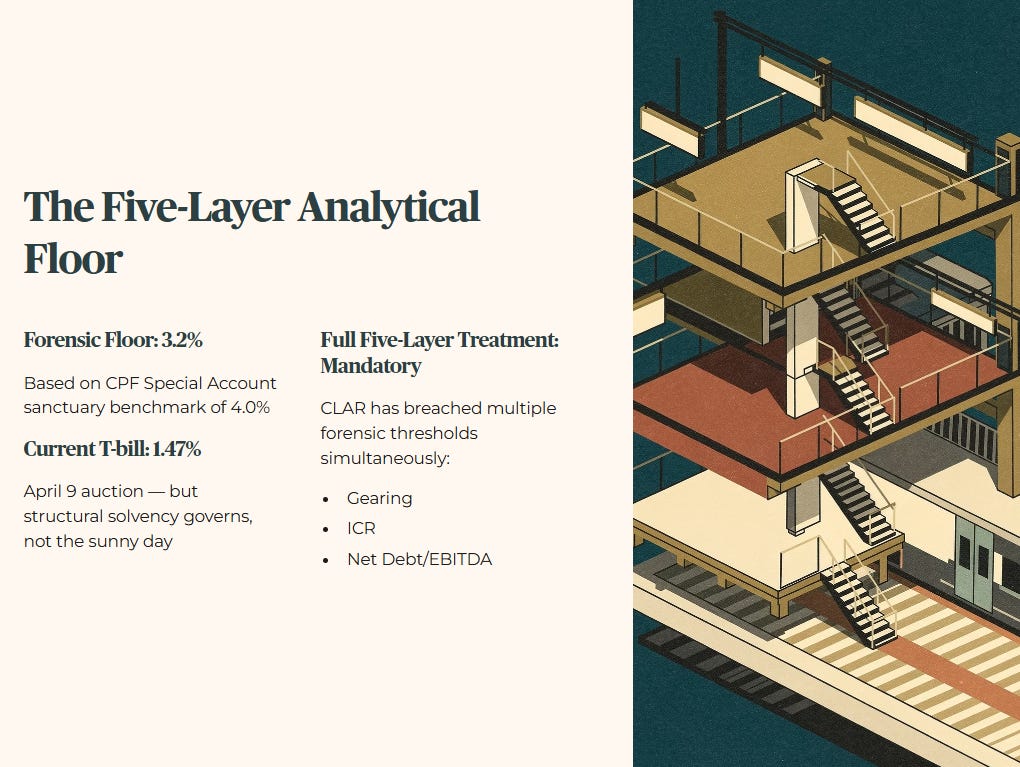

THE FIVE-LAYER ANALYTICAL FLOOR

The starting point for any serious tracking of Singapore-listed real estate is a forensic floor that accounts for the opportunity cost of capital. I maintain a static forensic floor of 3.2% based on personal tracking of the risk-free rate and the CPF Special Account sanctuary benchmark of 4.0%.

For a titan like CLAR, we audit for the storm, not the sunny day. While the current 6-month Singapore T-bill reached a cut-off yield of 1.47% in the April 9 auction, structural solvency is the governing question. Because CLAR has breached multiple forensic thresholds — specifically gearing, ICR, and Net Debt/EBITDA — the Full Five-Layer treatment is mandatory.

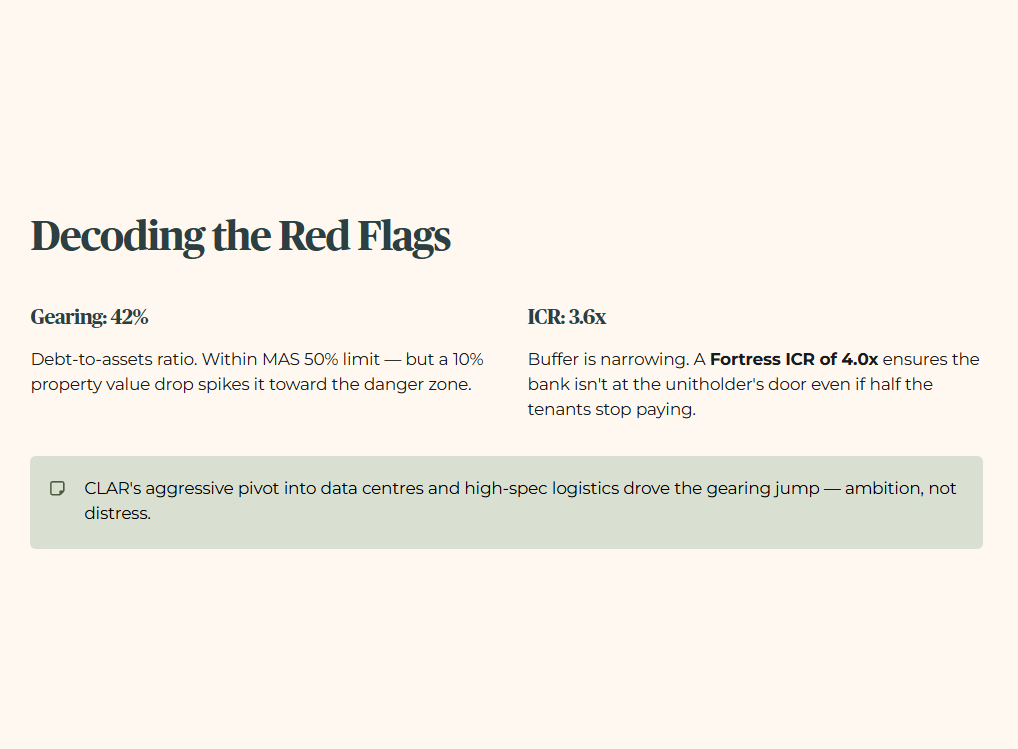

Layer 1 — Raw Fact CapitaLand Ascendas REIT’s pro-forma aggregate leverage is projected to rise to 42.0% following the integration of the S$1.41 billion acquisition cluster.

Layer 2 — Benchmark This figure severely breaches the Iggy Forensic Ceiling of 35% and sits significantly above the trust’s reported 31 December 2025 gearing of 39.0%.

Layer 3 — Peer Context Mapletree Industrial Trust (MIT) currently maintains an aggregate leverage of 37.2%, which also fails the absolute 35% sanctuary threshold but offers a more robust buffer than CLAR’s pro-forma position.

Layer 4 — Forward Scenario In a bearish macro trigger where global interest rates remain elevated through 2027 and CLAR faces a 10% spike in refinancing costs for its upcoming debt wall, the current Interest Coverage Ratio (ICR) could compress from 3.6x to below the 3.25x credit-rating floor. This would trigger a DPU contraction of approximately 0.6 to 0.9 cents as interest expenses eat into distributable income.

Layer 5 — Wallet Impact For a 62-year-old in Toa Payoh managing an SRS drawdown, a 42% gearing level represents a Watchlist Trigger. If the management fails to maintain double-digit rental reversions, this investor faces a potential 5% to 8% reduction in their annual cash distribution, turning a “safe” income stream into a capital risk play.

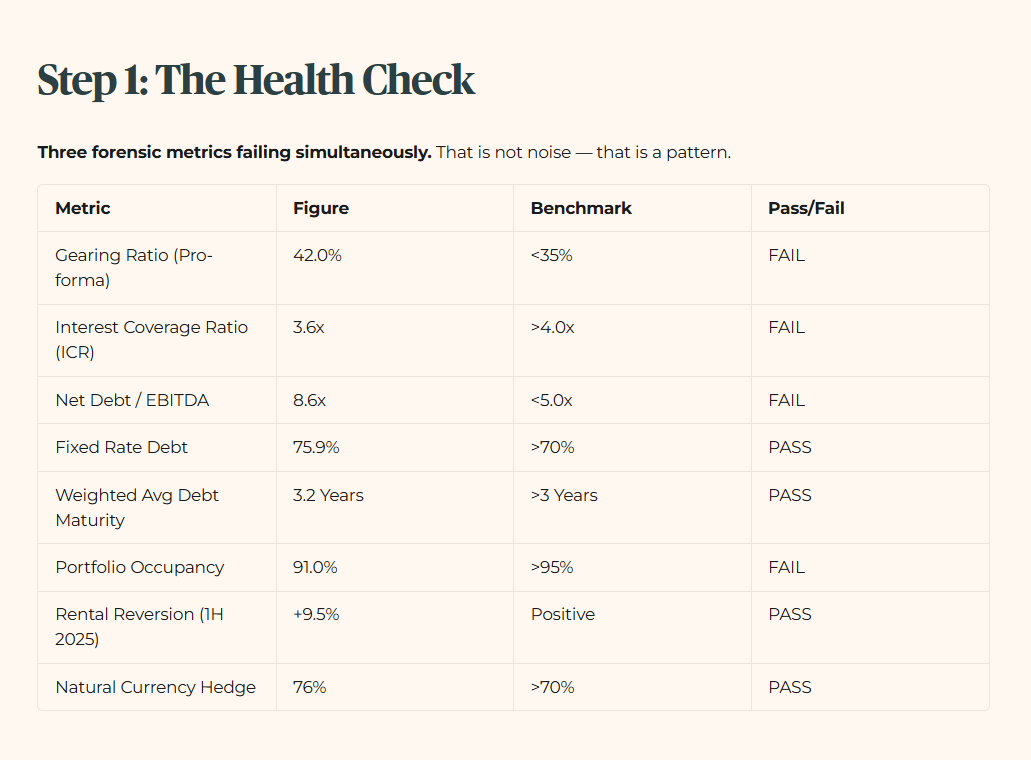

Step 1: The Health Check (Solvency)

Three forensic metrics are failing simultaneously. That is not noise — that is a pattern. This is where the dividend math breaks if the manager loses pricing power.

Gearing is simply the ratio of a REIT’s total debt to its total assets. It tells us how much of the “house” is owned by the bank. CLAR’s pro-forma jump to 42% is a consequence of its aggressive pivot into New Economy assets like data centres and high-spec logistics. While it remains within the MAS regulatory limit of 50%, it leaves very little headroom for asset devaluations. If property values drop by just 10% in a global slowdown, that gearing ratio would spike toward the danger zone.

The Interest Coverage Ratio measures how many times the REIT can pay its interest expenses using its operating profit. A ratio of 3.6x means the buffer is narrowing. In forensic terms, a Fortress ICR of 4.0x or higher ensures that even if half the tenants stop paying rent, the bank is not coming to the unitholder’s door.

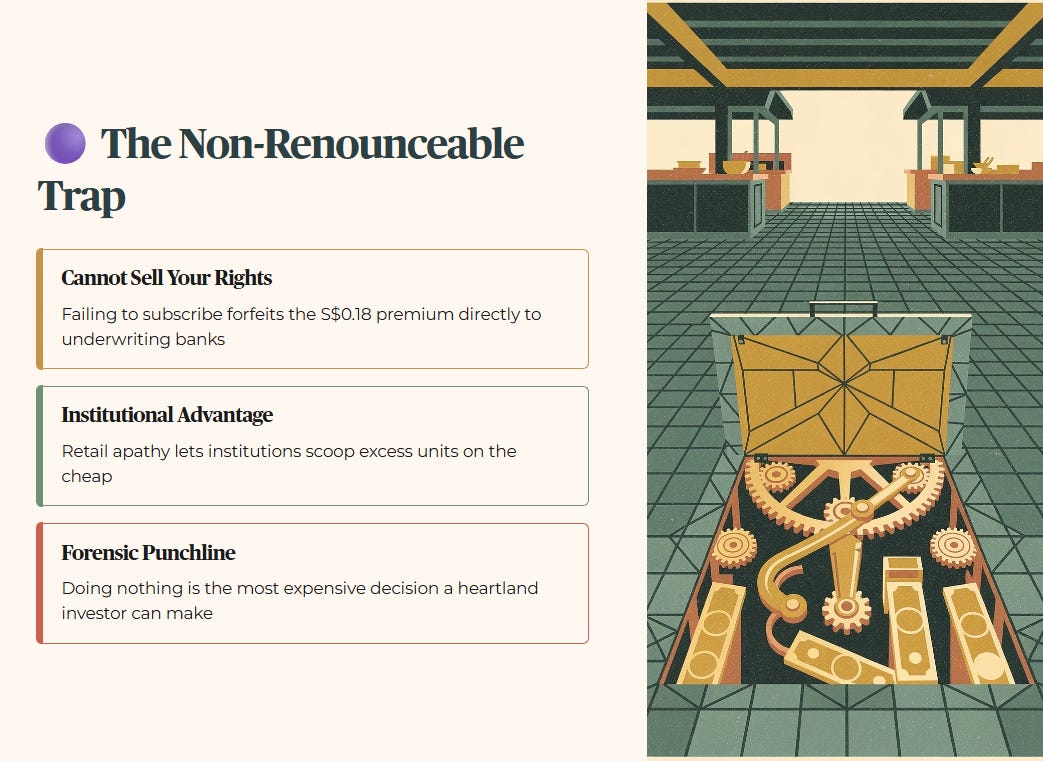

🟣 Iggy’s Insight: The Non-Renounceable Trap

A non-renounceable preferential offering is fundamentally coercive. Because you cannot sell your rights on the open market, failing to subscribe means you forfeit the S$0.18 premium between the S$2.35 issue price and the current S$2.53 market price directly to the underwriting banks. This is not merely an investment choice. It is a defensive necessity to prevent the absolute dilution of your equity base. Institutional players rely on retail apathy during these corporate actions to scoop up excess units on the cheap. Leaving your allotment on the table is a permanent, unforced surrender of capital.

Forensic Punchline: In a non-renounceable rights issue, doing nothing is the most expensive decision a heartland investor can make.

Step 2: The Wealth Check (Yield and Distribution Trajectory)

The yield picture for CLAR requires two separate readings: what the trailing record shows, and what the post-acquisition projection claims. Conflating the two is how retail investors get caught in the wrong calculation.

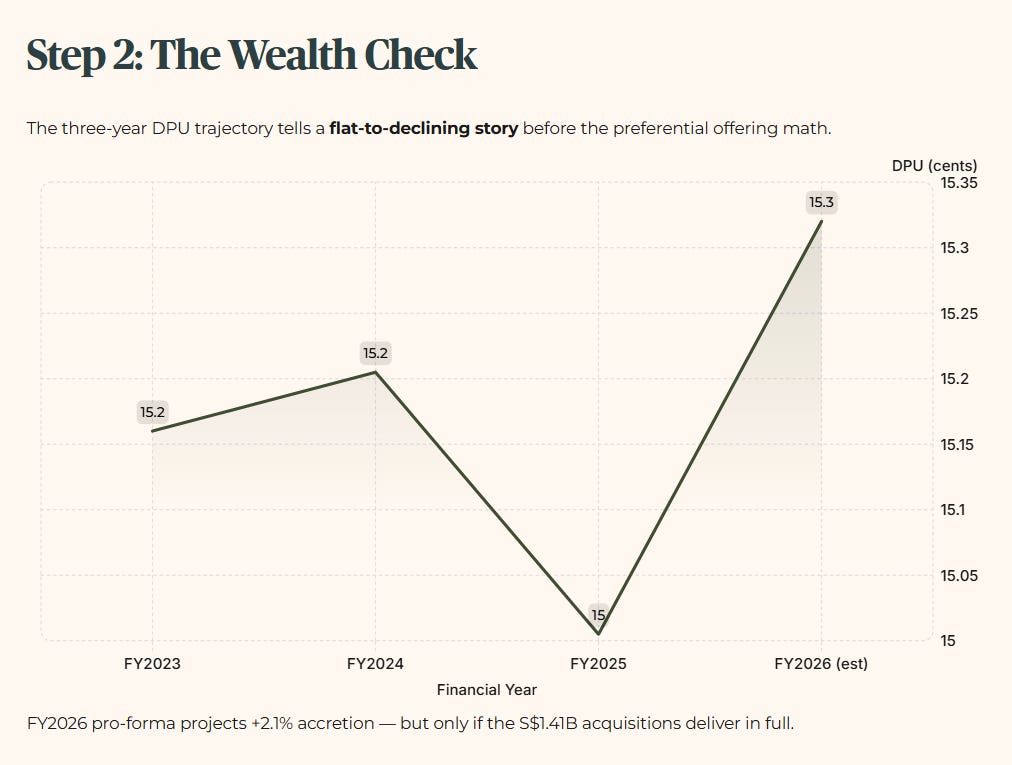

The three-year DPU trajectory tells a flat-to-declining story before we even get to the preferential offering math.

The FY2025 decline from 15.205 cents to 15.005 cents is not a business failure. Distributable income itself rose 1.4% year-on-year. The DPU slippage is a unit base dilution effect from the May 2025 equity fundraise. At the current price of S$2.51, the FY2025 trailing yield is approximately 5.98%. The 7.5% figure cited in this audit is a forward pro-forma estimate that only materialises if the S$1.41 billion acquisitions deliver the projected 2.1% DPU accretion in full.

A note on the advanced distribution: The 3.750-cent distribution with an ex-date of 31 March 2026 is a one-off advanced distribution covering the period 1 January 2026 to 1 April 2026, declared specifically in connection with this equity fundraise. It is not a regular semi-annual payment. Unitholders subscribing to new units under the preferential offering do not qualify for this distribution. If you are buying at S$2.35, your effective Year 1 yield calculation must exclude this 3.750 cents entirely.

The Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. While the T-bill sits at 1.47% from the April 9 auction, I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7%: that is the 3.2% floor plus 150 basis points of mandatory risk premium.

At the forward pro-forma yield of 7.5%, CLAR clears that hurdle. But the clearing depends entirely on the Osaka data centre and Loyang logistics cluster delivering organic NPI growth, not sponsor top-ups. CLAR’s ability to command rental reversions of +9.5% to +12% is the MRT Door Paradox in action: even as the crowd pushes to get out, the demand to get into prime industrial space remains strong enough that the manager keeps raising the ticket price. The moment that reversion trend weakens, the 7.5% forward estimate becomes the first number to be revised downward.

The yield gap is already explained — but the 42% gearing and the 2026 debt wall only make sense once you test whether the Osaka and Loyang assets can actually de-risk the balance sheet.