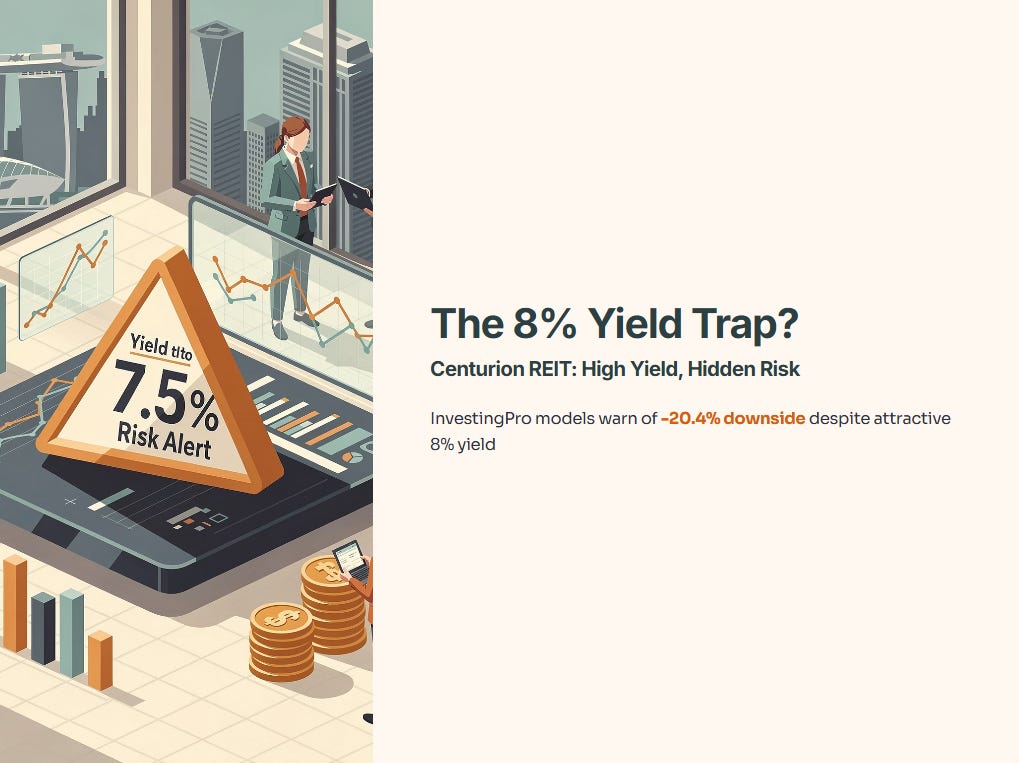

Smart Money Move or Retail FOMO? Navigating Centurion REIT’s 2027 Expansion Pipeline

The yield looks safe at the surface, but the InvestingPro models are shouting a -20.4% downside warning that most retail investors are blindly ignoring.

About Iggy the Investing Iguana channel

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 5,300 subscribers and an “Inner Circle” of 100+ paid members across YouTube and Substack.

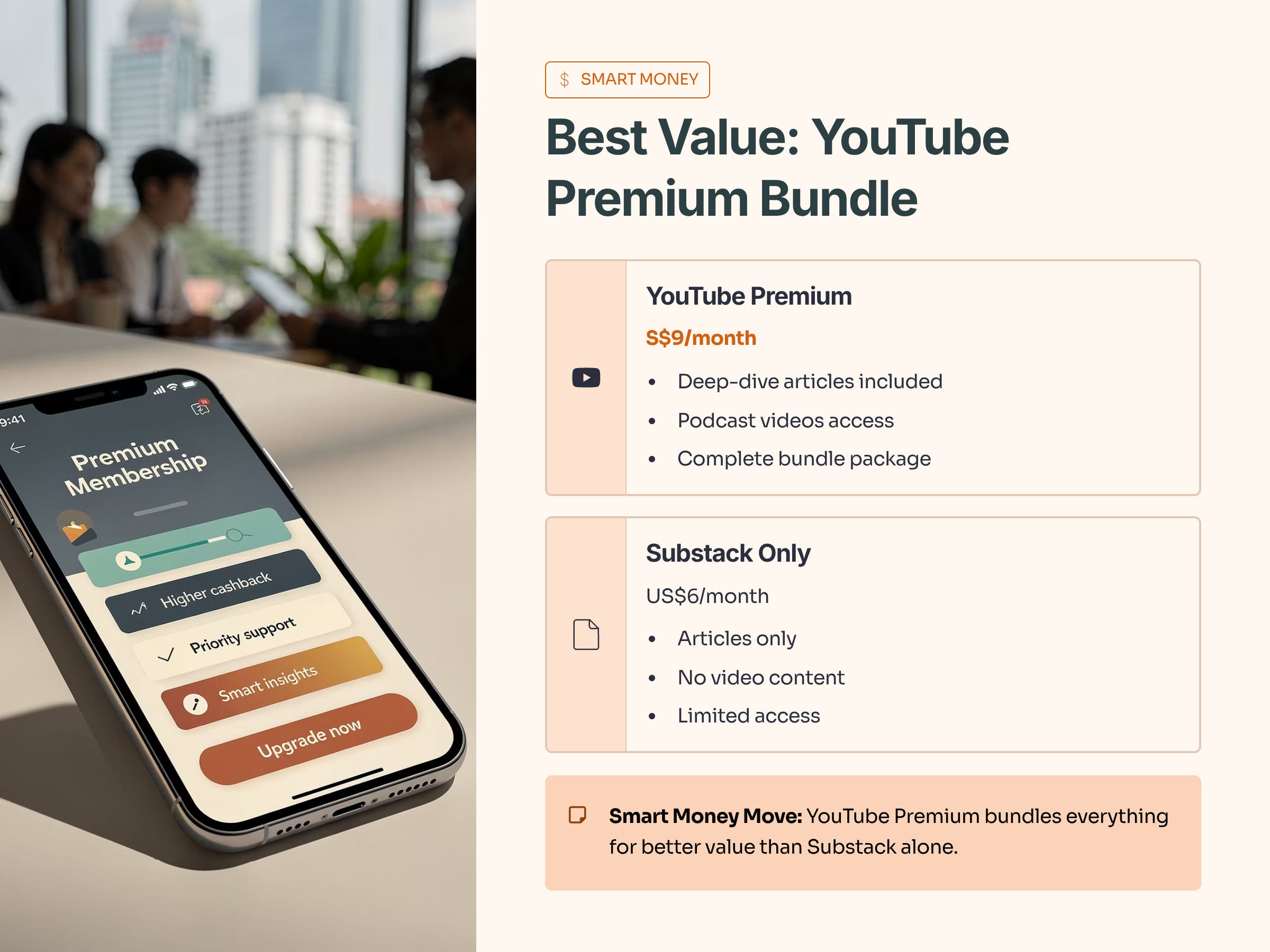

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

In This Article:

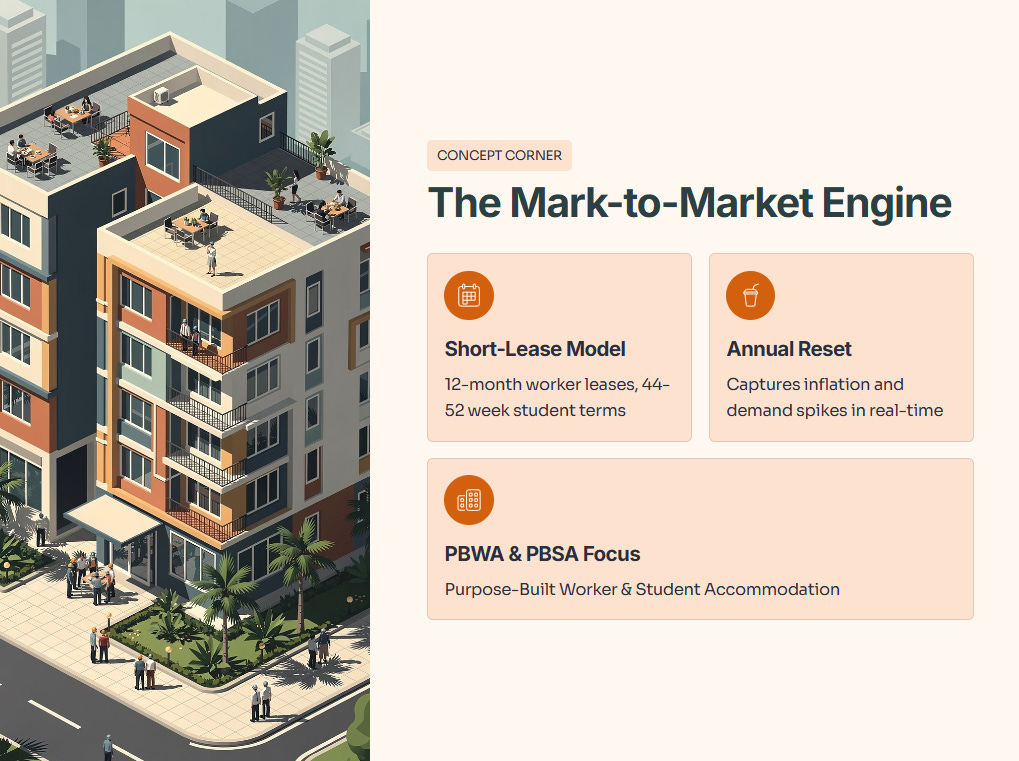

Concept Corner: The Mark-to-Market Engine

The Iggy Audit: The Narrative

The Data Fortress: The Evidence

The Scenario Matrix: The Forecast

InvestingPro Reality Check

The Verdict

Concept Corner: The Mark-to-Market Engine

Most S-REITs are handcuffed by fixed 3-to-5-year industrial or commercial leases. Centurion Accommodation REIT (8C8U) operates on a “Short-Lease Mark-to-Market” model. In Purpose-Built Worker Accommodation (PBWA) and Student Accommodation (PBSA), leases reset every 12 months for workers or 44–52 weeks for students.

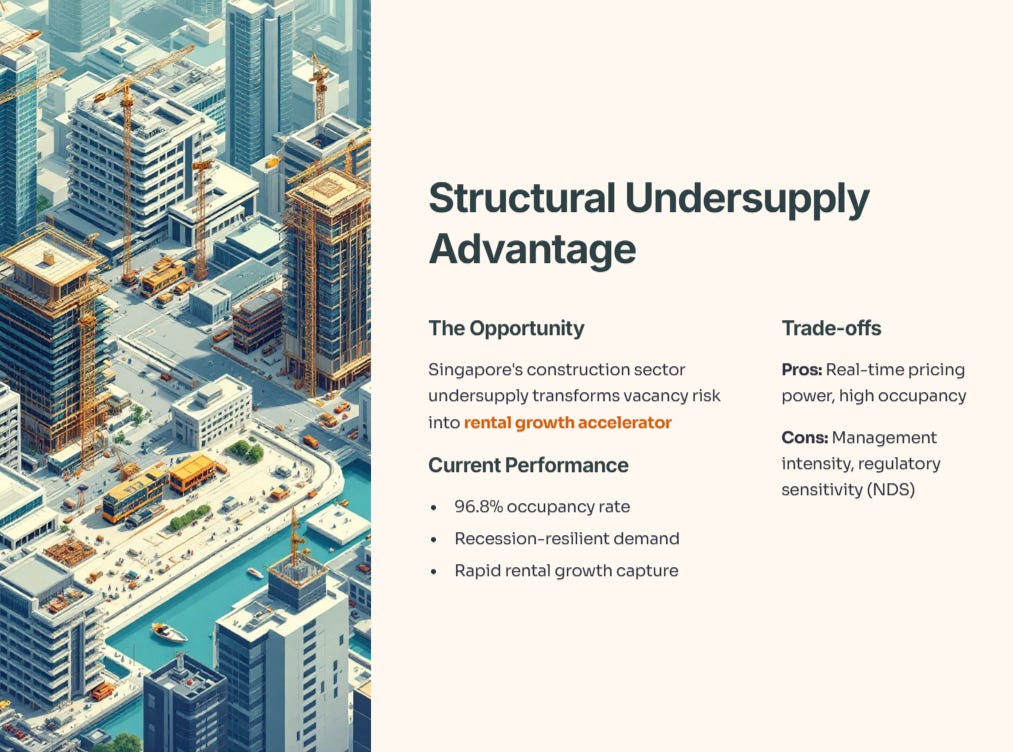

When a market is structurally undersupplied—like Singapore’s construction sector—this isn’t a vacancy risk; it’s a rental growth accelerator. It allows the REIT to capture inflation and demand spikes in real-time.

Pros: Rapid capture of rental growth; high occupancy (currently 96.8%); recession-resilient demand.

Cons: Higher management intensity; sensitivity to rapid regulatory changes like New Dormitory Standards (NDS).

The Iggy Audit: The Narrative

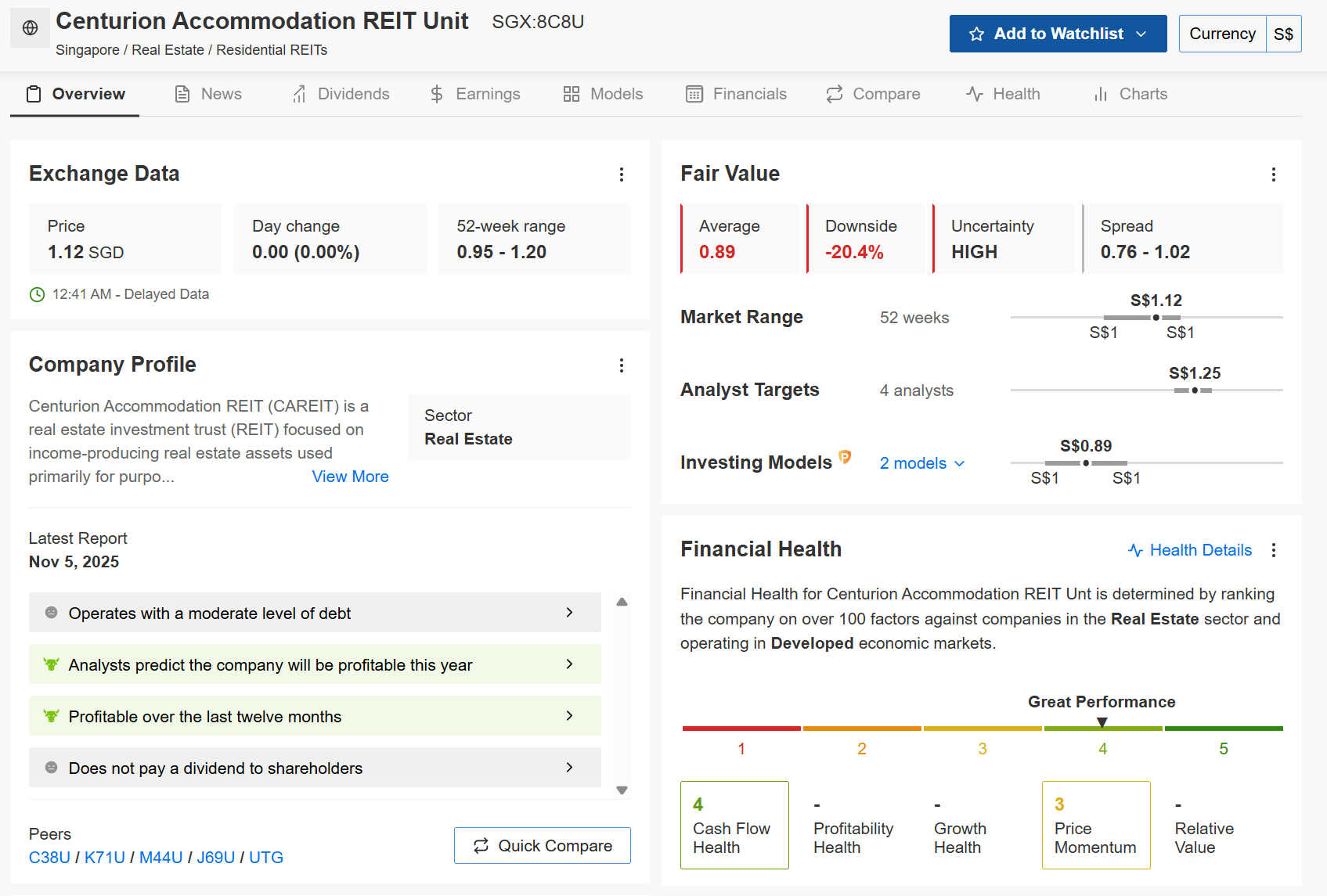

Investors are calling this a “safe yield play.” However, InvestingPro data reveals the stock is currently trading at S$1.12, while their consolidated fair value model sits at S$0.89—representing a potential -20.4% downside risk. While analysts like DBS remain bullish with a S$1.30 target, the gap between market price and intrinsic value is widening.

The “Smart Money” knows that the worker-to-bed ratio in Singapore is roughly 4.0x. With the Building and Construction Authority projecting demand up to S$53 billion in 2025, those beds aren’t going empty, but you might be overpaying for the privilege of owning them.

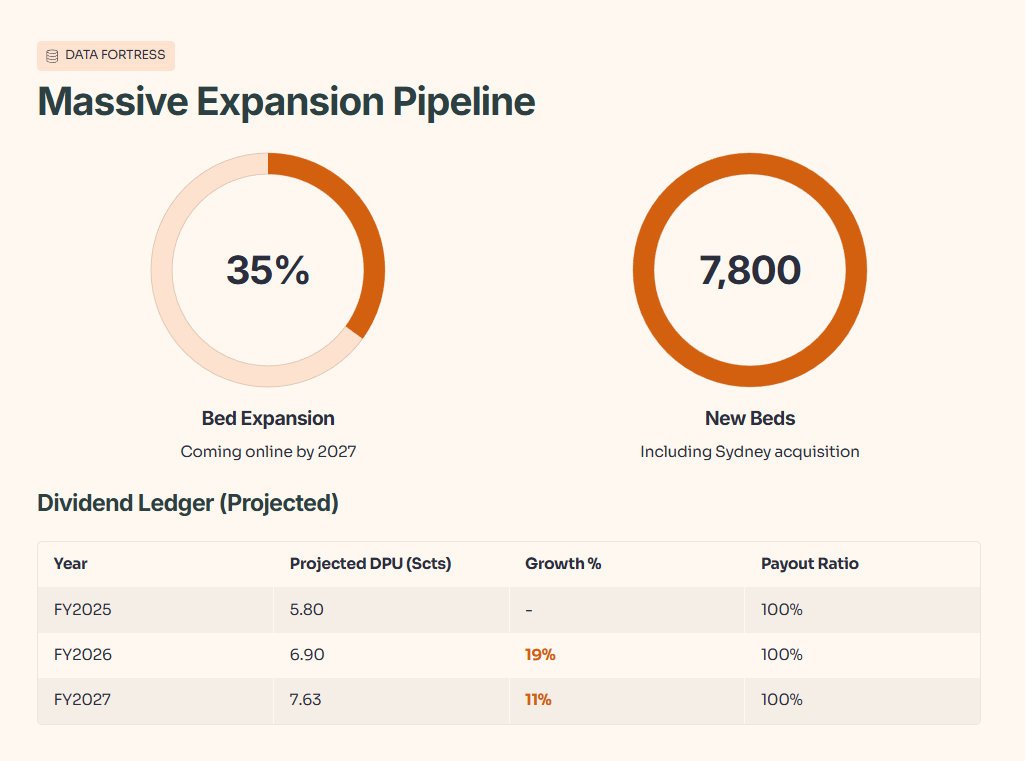

The Data Fortress: The Evidence

The bull case rests on a massive 35% bed expansion coming online by 2027, totaling over 7,800 new beds including the newly acquired Epiisod Macquarie Park in Sydney.

The strength of Centurion REIT’s “Data Fortress” isn’t just in current occupancy, but in a mathematically locked-in growth runway. The REIT is orchestrating a massive 35% bed expansion by 2027, adding over 7,800 new beds to its portfolio. This isn’t speculative growth; it is anchored by physical assets like the newly acquired Epiisod Macquarie Park in Sydney and key Singapore expansions at Westlite Toh Guan and Mandai. This capacity surge is the direct engine behind the projected 19% DPU jump in FY2026, fueling a distribution trajectory that rewards patient “Smart Money” with a high-conviction 100% payout ratio.

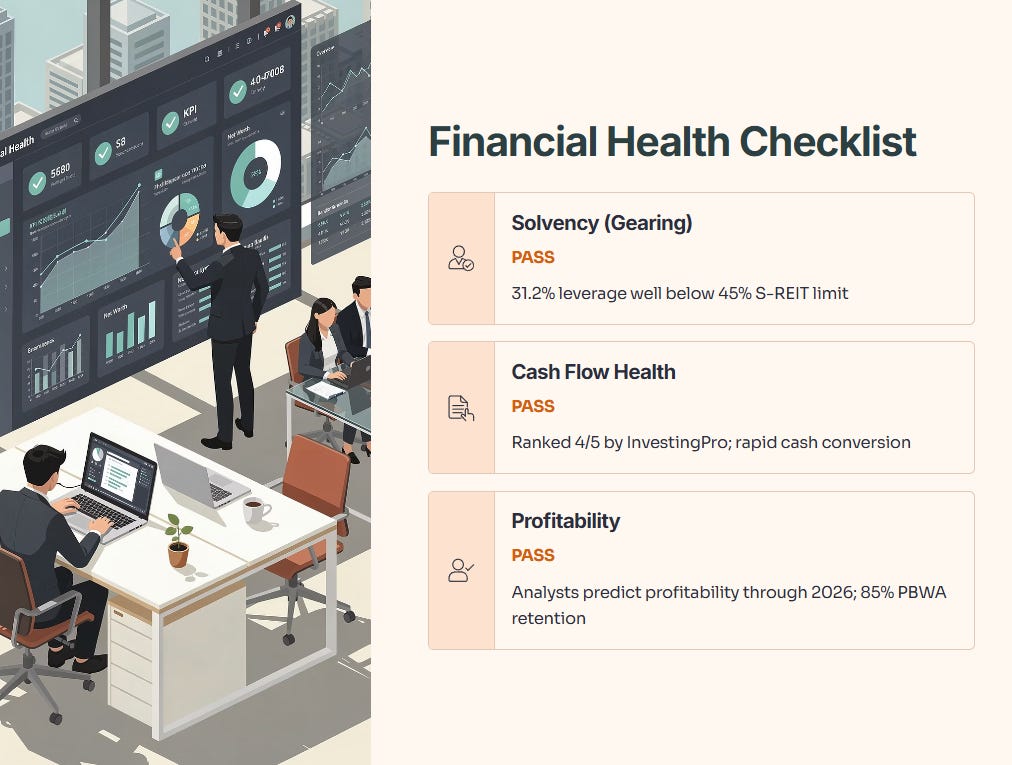

From a balance sheet perspective, the fortress is equally resilient. With a conservative 31.2% gearing, the REIT maintains significant debt headroom well below the regulatory 45% limit, insulating it against sudden interest rate shocks. InvestingPro gives it a high 4/5 Cash Flow Health score, a testament to how the “Short-Lease” model ensures that rising rents are converted into actual distributable cash almost immediately. When you combine these metrics with a ~85% tenant retention rate in the Singapore worker segment, you aren’t just looking at a high-yield stock—you’re looking at a structurally sound income machine designed to weather market volatility while compounding your capital.

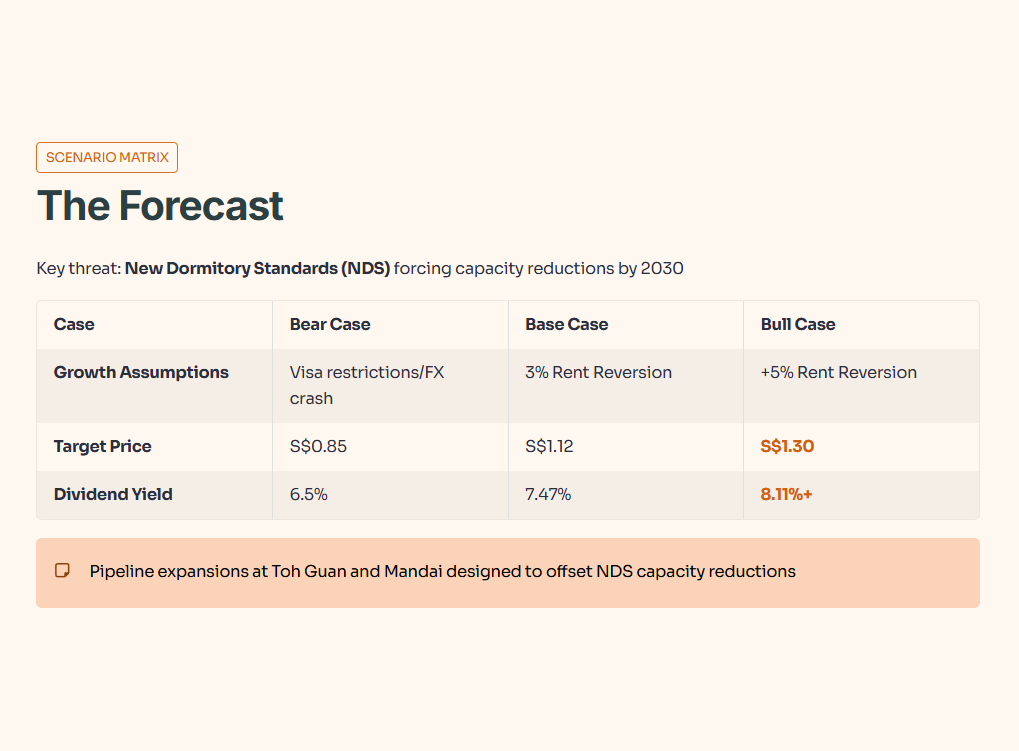

The Scenario Matrix: The Forecast

The biggest long-term threat is the New Dormitory Standards (NDS) forcing capacity reductions by 2030, though current pipeline expansions at Toh Guan and Mandai are designed to offset this.

InvestingPro Authority:

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

The Verdict: The Action Plan