The Ah Pek Audit: Explaining SGX Bank Dividends Without Using Financial Jargon

Using DBS's Own Numbers to Show What the Headline Yield Won't Tell You

DBS just posted a headline dividend yield of 4.70 percent. Strip out the temporary capital return payment sitting inside that number, and the durable yield falls to 3.96 percent, below both the CPF Special Account rate and my own minimum yield hurdle. That gap between what the headline says and what the bank can actually sustain is exactly what this audit is built to catch.

Every bank on the exchange will tell you its dividend is dependable, but almost none of them will tell you which part of that dividend is guaranteed and which part is a decision that could stop after the next earnings call. One investor sees a 4.70 percent headline yield and buys on the spot. Another investor checks where that number actually comes from before committing a single dollar of CPF or SRS money. This audit is built for the second investor, using DBS as the live example so you can run the same four steps yourself on any bank you hold.

Working through financial statements can feel overwhelming when your primary goal is securing stable distributions for your capital. Over years of tracking the Singapore market, I have found that the core health of a banking entity boils down to a few basic variables that anyone can read. We do not need Wall Street formulas to protect our hard-earned retirement capital. Let us break down the exact mechanism of how local financial giants generate and distribute cash.

From Our Sponsor

Step 1: The Health Filter (Solvency Audit)

Iggy’s Insight Block 1

Step 2: The Valuation Reality

Step 3: The Income Stress Test

Step 4: The Peer Comparison, and the Live Case Study

Iggy’s Insight Block 2

Iggy’s Bottom Line

From Our Sponsor

Before we start the audit, a quick note on execution cost, because the best forensic analysis in the world does not help you if fees eat your entry position. In the world of dividend investing, we spend a lot of time talking about the yield spread, the difference between what a stock pays you and the risk-free rate. But there is a hidden leak that most retail investors completely ignore, transaction friction. If you are deploying ten thousand Singapore dollars into a Singapore REIT, and your broker eats a chunk of that in minimum commissions or platform fees, you are starting your investment in the red before you have even bought a single share.

Data is only useful if you have the tools to act on it without getting eaten alive by those fees. That is why I use Longbridge. They are currently the only platform in Singapore offering lifetime zero commission^ for US, Hong Kong, and Singapore stocks. Their data visualisation is also some of the fastest I have used, which is critical when you are timing an entry in a volatile market.

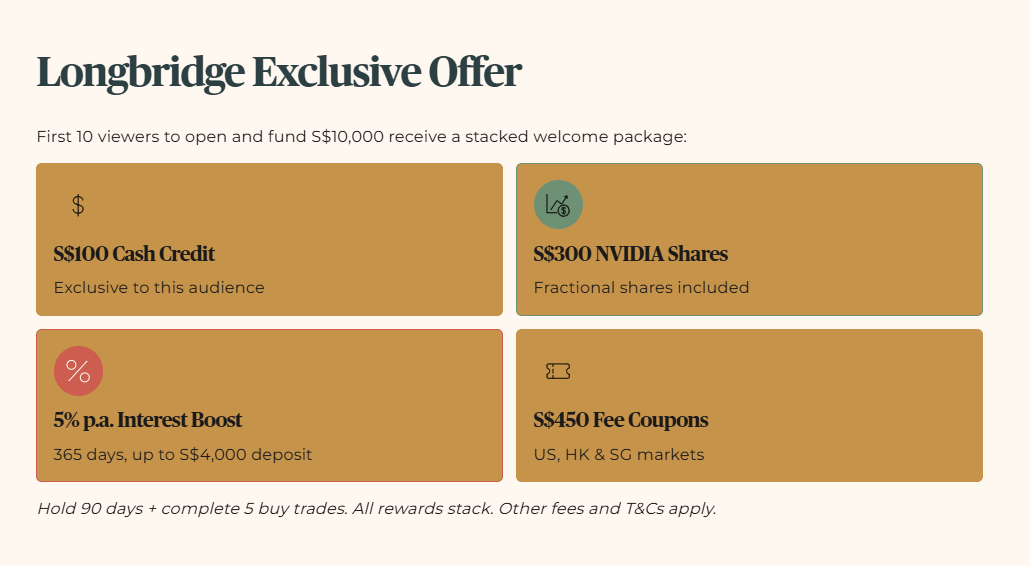

To help you plug that leak, I have partnered with Longbridge on an exclusive arrangement for my viewers. For the first ten viewers who open and fund an account with a minimum of ten thousand Singapore dollars, Longbridge is offering a direct one hundred Singapore dollar* cash credit on top of their already generous June welcome rewards.

Here is what the full package looks like if you deposit ten thousand dollars, hold it for ninety days, and complete five buy trades. You receive the exclusive one hundred dollar cash credit. You receive three hundred Singapore dollars worth of NVIDIA fractional shares. You receive a five percent per annum interest boost coupon# valid for three hundred and sixty-five days on deposits up to four thousand dollars, worth up to two hundred Singapore dollars over the year. And you receive platform fee coupons worth up to four hundred and fifty Singapore dollars across US, Hong Kong, and Singapore markets. All of these stack together. You do not have to choose between them.

Why does this math matter to a forensic investor? Because one hundred dollars on a ten thousand dollar deposit is an immediate one percent Day One Yield Boost, before you have executed a single trade. Combined with the interest boost coupon and platform fee savings, the total welcome package meaningfully neutralises transaction friction and protects your margin of safety from the moment you fund the account.

This is strictly limited to the first ten spots. The link and full terms are in the description. Other fees and terms and conditions apply, so read those carefully before you proceed. But for a forensic investor who cares about entry cost and yield from day one, this is worth five minutes of your time.

Now, back to the forensic framework, because knowing where to buy affordably is only half of the equation. The other half is knowing what you are actually buying.

Step 1: The Health Filter (Solvency Audit)

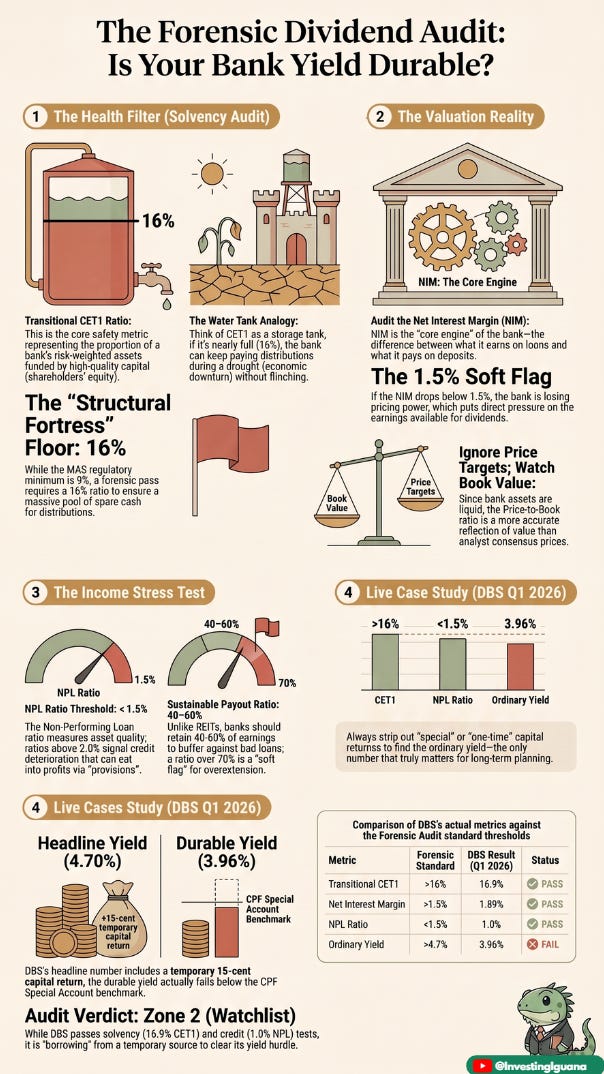

The absolute first step in auditing any banking entity is evaluating its ultimate safety net. In standard stock or REIT analysis, you look at gearing ratios to see how much debt a company holds relative to its equity. For banking institutions, standard gearing metrics and interest coverage ratios are entirely useless because banks are highly leveraged by design. Your deposits are treated as their liabilities, which they use to fund loans. Therefore, we must substitute standard gearing with a specific banking capital metric.

That metric is Transitional CET1 (Common Equity Tier 1 ratio). To define this in plain language, Transitional CET1 is the proportion of a bank’s risk-weighted assets funded by the highest-quality capital, primarily ordinary shareholders’ equity. The Monetary Authority of Singapore requires Singapore-incorporated banks to maintain a minimum transitional CET1 of 9 percent.

When you review financial reports or media releases, you will notice two figures, transitional and fully phased-in. Always focus on the transitional figure. MAS regulatory capital requirements are set and published on a transitional basis. The phased-in figure is an accounting construct that can understate the capital buffer regulators actually require banks to maintain. For a retail investor audience assessing whether a bank’s capital position is safe, the transitional figure is the one that corresponds to the regulatory floor.

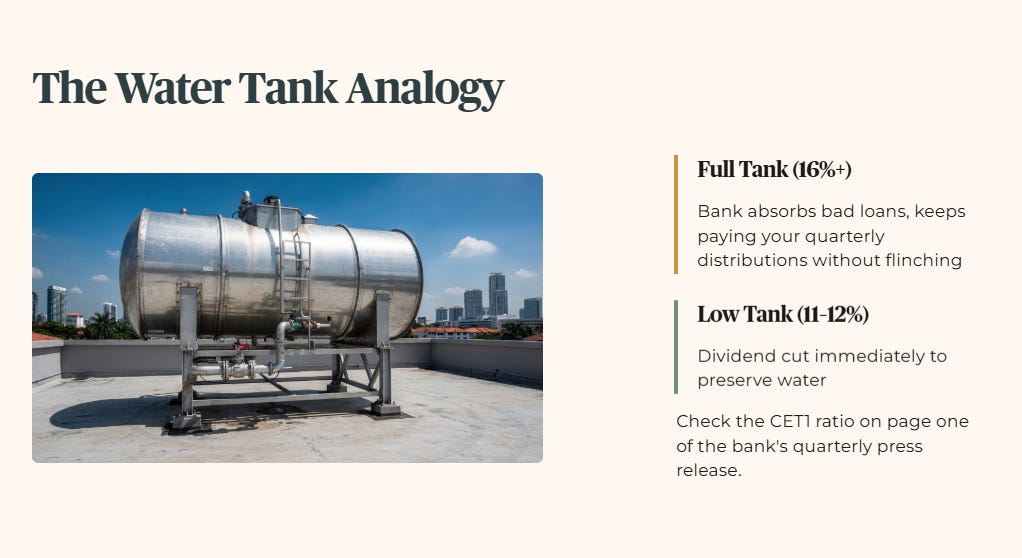

I apply a strict forensic filter to this capital ratio. While the regulator says 9 percent is safe, my personal standard for a structural fortress is a floor of 16 percent. This sets a significantly higher bar to ensure a meaningful buffer above the regulatory minimum. If a bank maintains a capital ratio comfortably above 16 percent, it means they have an enormous pool of spare cash protecting them from bad loans. This excess capital is the exact pool from which special distributions and capital management programmes are built. If this ratio drops below 14 percent, the bank enters a cautionary zone where fresh dividend growth slows down as management retains cash to rebuild their buffers.

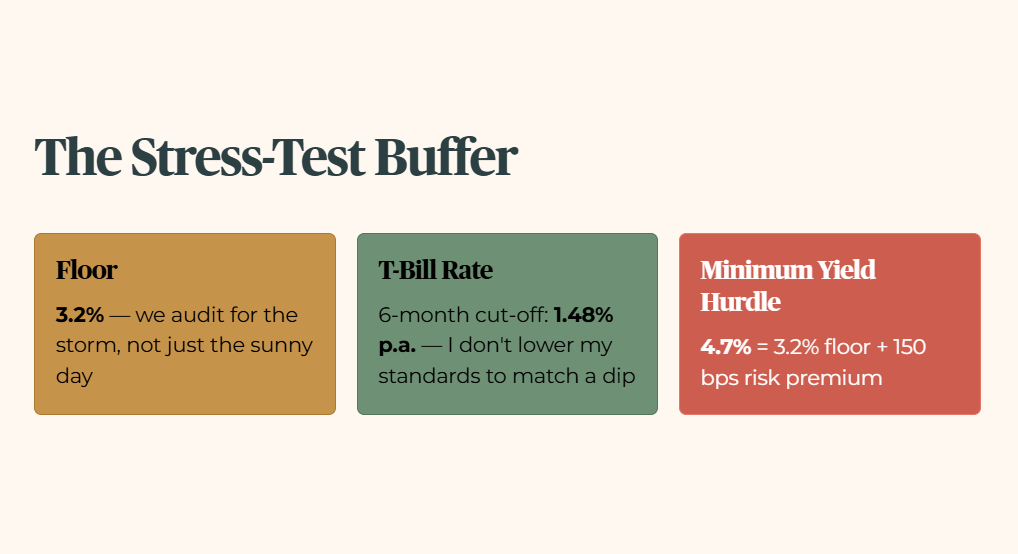

A note on the stress-test buffer. For this audit, I apply a conservative floor of 3.2 percent. We audit for the storm, not just the sunny day. While the six-month T-bill cut-off yield sits at 1.48 percent per annum, I do not lower my standards to match a temporary market dip. My floor remains at 3.2 percent to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7 percent, that is the 3.2 percent floor plus 150 basis points of mandatory risk premium.

Think of the transitional capital ratio like the water level in a household storage tank. If the regulatory minimum is a tiny pool at the bottom, my 16 percent threshold ensures the tank is nearly full. When an economic drought hits and borrowers struggle to pay their loans, the bank has to draw down on this water. A bank starting with a full tank can keep paying your quarterly distributions without flinching. A bank skimped at 11 or 12 percent will immediately cut the dividend to preserve water.

To execute this step, look at the first page of the bank’s quarterly financial highlights or press release. Management will always highlight the CET1 ratio under their capital adequacy section. If the number sits above 16 percent, the health filter is a clear pass.

🦎 Iggy’s Insight Block 1

The single step in this framework that most retail investors skip is verifying the underlying capital adequacy metric against the regulatory floor. Most people look exclusively at historical dividend tables, assuming past payouts guarantee future safety. Skipping the capital buffer check is the most expensive mistake in SGX income investing because banks are highly leveraged regulatory entities. When economic conditions worsen, the regulator forces capital preservation over retail investor satisfaction. If you do not audit the capital base first, you are essentially picking up pennies in front of a financial steamroller.

Step 2: The Valuation Reality

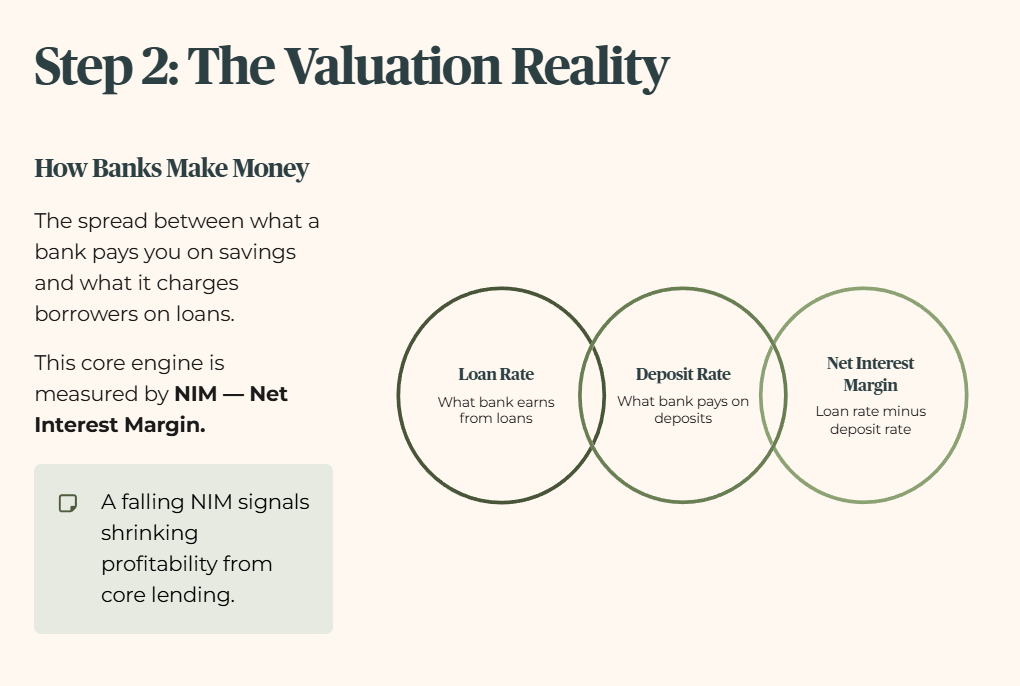

Once we establish that the bank is financially sound, we must audit how it actually generates its core profits. The primary driver of a commercial bank’s earnings is the spread between what it pays you for your savings accounts and what it charges corporations and home buyers for their loans.

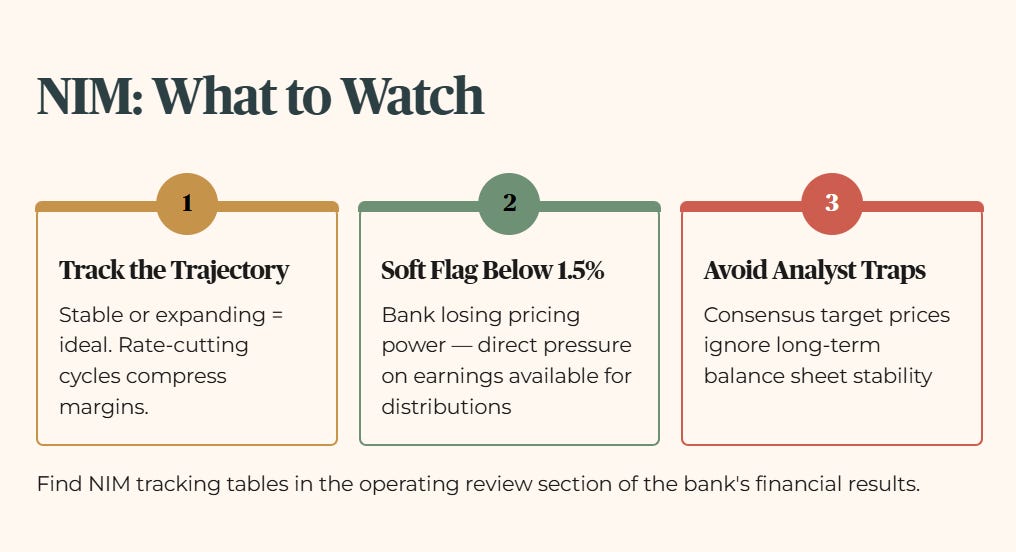

This core engine is measured by NIM, Net Interest Margin. To define this in plain language, NIM is the difference between what a bank earns on loans and what it pays on deposits, expressed as a percentage of interest-earning assets. A falling NIM signals shrinking profitability from core lending.

When interest rates are high globally, banks enjoy wide interest margins because loan rates rise much faster than deposit rates. However, when central banks cut rates, interest margins naturally face compression. As a forensic investor, you must track the trajectory of this margin over consecutive quarters. A stable or expanding margin is ideal, but during rate-cutting cycles, you want to see how efficiently management defends this spread. If the margin drops below 1.5 percent, it triggers a soft flag. A margin compressing below this level means the bank is losing its pricing power, which puts direct pressure on the total earnings available for distributions.

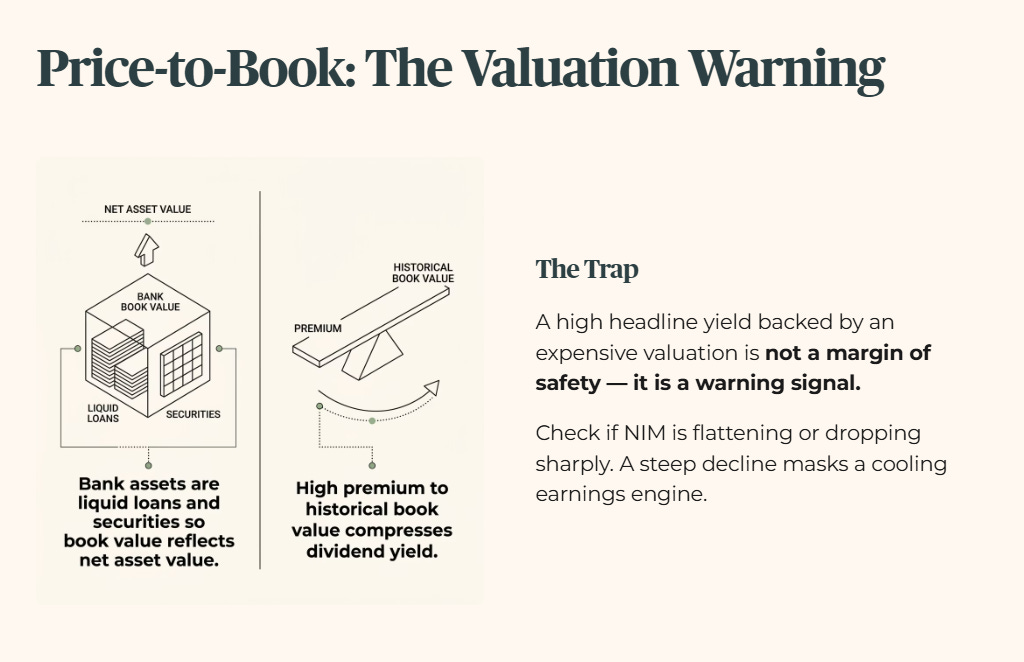

We must compare this operational reality against market valuations. Retail investors often fall into the trap of looking at analyst consensus target prices. Analysts frequently base their valuations on short-term earnings momentum, ignoring long-term balance sheet stability. A forensic audit requires calculating whether the current market premium is justified by the underlying assets.

Look at the price-to-book ratio of the banking sector. Since bank assets are highly liquid loans and securities, book value is a reasonably accurate reflection of net asset value. When a bank trades at a significant premium to its historical book value, the dividend yield drops compressively. A high headline yield backed by an expensive valuation is not a margin of safety, it is a warning signal.

You can find the net interest margin tracking tables inside the operating review section of the bank’s financial results. Management usually provides a historical breakdown comparing the current quarter against the preceding four quarters. Your job is to check if the line is flattening or dropping severely. If the decline is sharp, the headline dividend narrative is likely masking a cooling earnings engine.

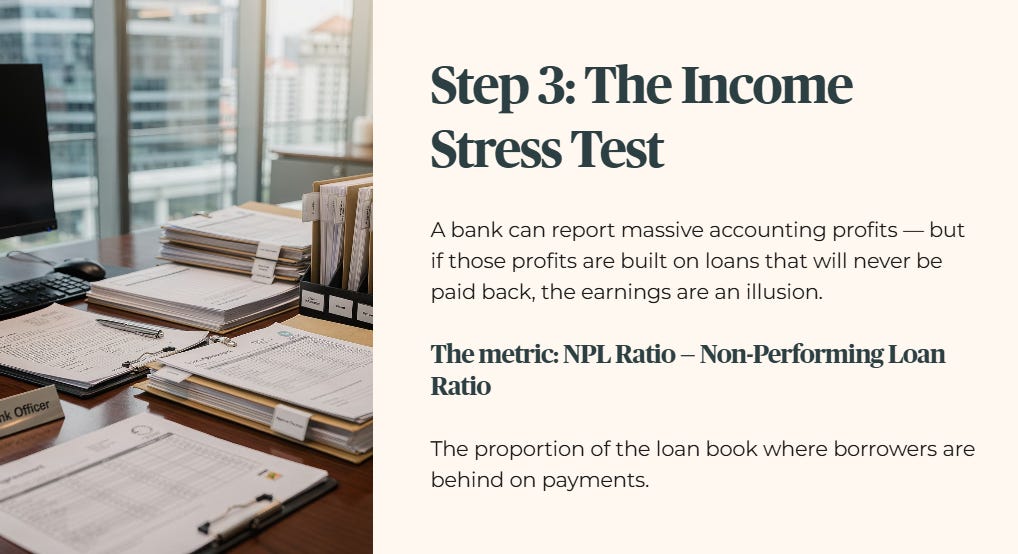

Step 3: The Income Stress Test

Step three moves from how much a bank earns to how clean those earnings truly are. A bank can report massive accounting profits on paper, but if those profits are built on loans that will never be paid back, the earnings are an illusion.

To audit asset quality, we use the NPL ratio, Non-Performing Loan ratio. To define this in plain language, the NPL ratio is the proportion of the loan book where borrowers are behind on payments. Rising NPLs signal credit quality deterioration and potential write-offs ahead.

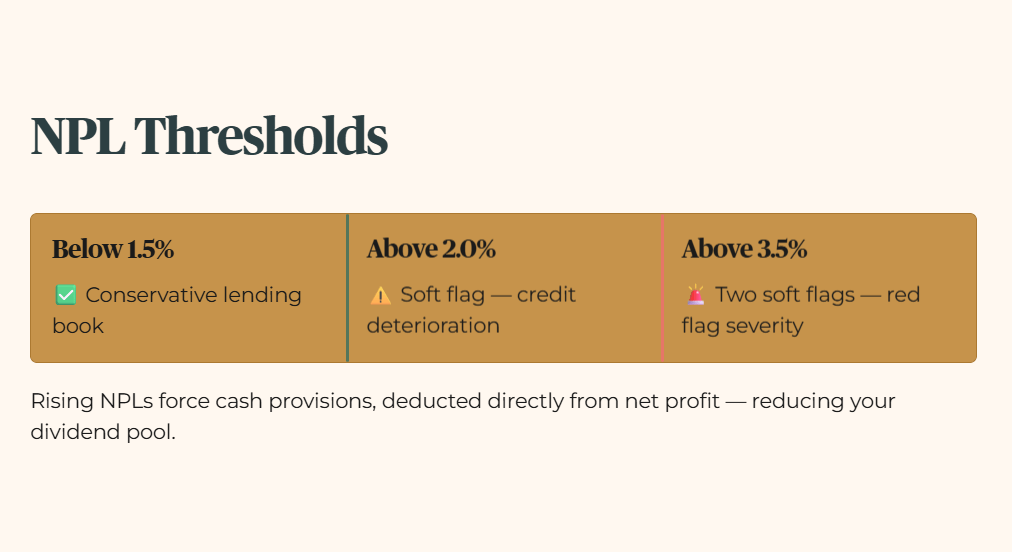

My forensic threshold for bank credit quality is strict. An NPL ratio below 1.5 percent represents a highly conservative lending book. If the ratio climbs above 2.0 percent, it triggers a soft flag for credit deterioration. If it breaches 3.5 percent, it counts as two soft flags directly, representing a red flag severity level. When borrowers default, the bank must set aside cash provisions to cover the losses. These provisions are deducted directly from net profit, which reduces the pool of funds available for your dividends.

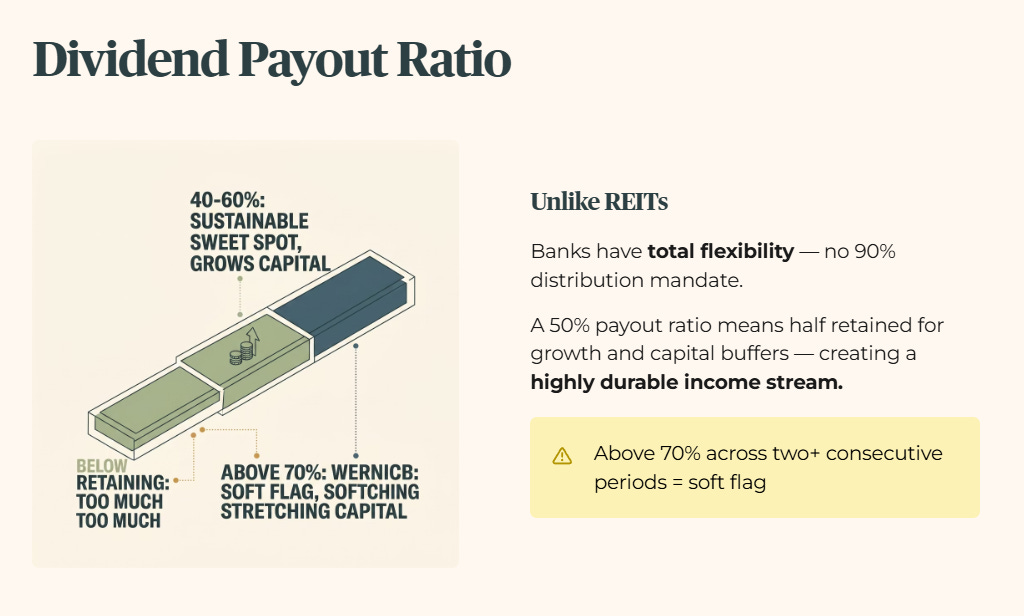

Next, we look at distribution sustainability by auditing the dividend payout ratio. For commercial banks, this is the percentage of net profit paid out as dividends to shareholders. Unlike REITs, which are legally mandated to distribute 90 percent of their taxable income, banks have total flexibility. They must balance rewarding shareholders with retaining capital for business growth and regulatory compliance.

A sustainable banking payout ratio should sit between 40 and 60 percent of net profit. If a bank maintains guidance around a 50 percent payout ratio, it means they keep half of their earnings to grow the business and reinforce their capital buffers. This creates a highly durable income stream.

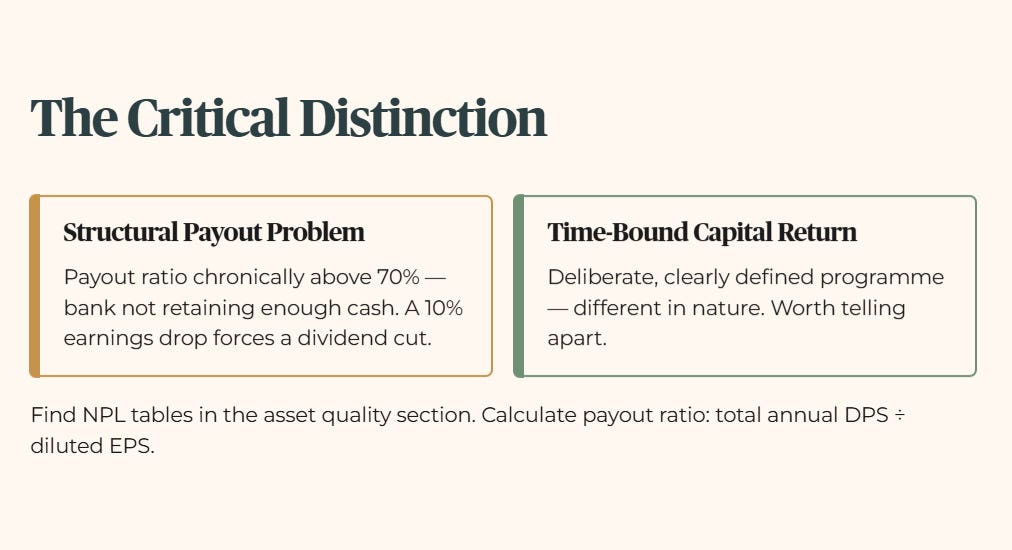

A note on distribution sustainability. If the dividend payout ratio climbs above 70 percent, sustained across two or more consecutive reporting periods, it triggers a soft flag. A bank paying out more than 70 percent of its earnings is stretching its capital. It means the bank is not retaining enough cash to buffer against future bad loans or to fund loan growth. If earnings drop by just 10 percent, a bank with an overextended payout ratio will be forced to cut its absolute dividend per share to protect its capital adequacy ratios. A temporary, clearly time-bound capital return programme is a different thing entirely, and worth telling apart from a structural payout problem, which is exactly what our live case study below shows.

You can find the asset quality metrics and NPL tables in the asset quality or credit risk section of the financial report. The payout ratio can be calculated easily by dividing the total annual dividend per share by the diluted earnings per share found on the income statement.

Step 4: The Peer Comparison, and the Live Case Study

The final step of the framework involves benchmarking, and there is no better way to learn it than watching it run on a real bank. Let us apply all four steps to DBS Group Holdings, using its own first-quarter 2026 results.

Step 1, the health filter. DBS reported a transitional CET1 ratio of 16.9 percent, comfortably clearing the structural fortress floor of 16 percent. This capital buffer sits well above the MAS regulatory minimum, giving the bank meaningful room to absorb shocks without touching its dividend.

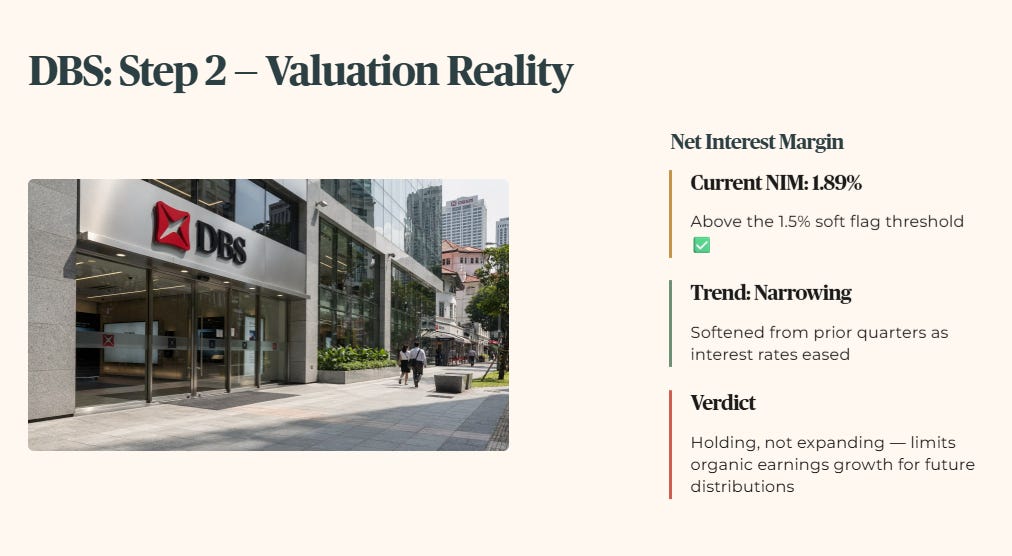

Step 2, the valuation reality. Net interest margin came in at 1.89 percent, above the 1.5 percent soft flag threshold, though it has narrowed from prior quarters as interest rates softened. The margin is holding, not expanding, which matters for how much organic earnings growth is actually available to fund future distributions.

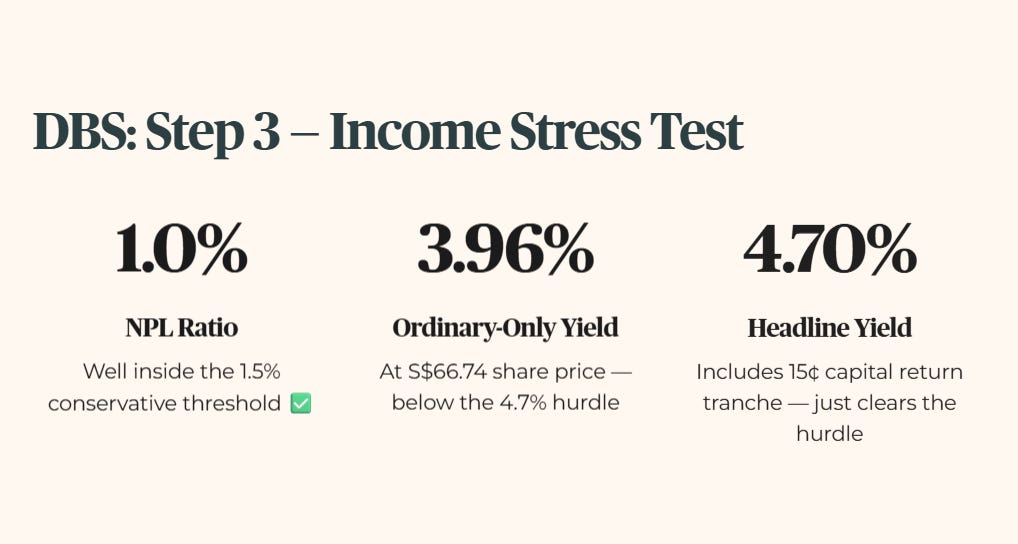

Step 3, the income stress test. Non-performing loans held stable at 1.0 percent, well inside the conservative 1.5 percent threshold. Asset quality here is not the concern. The concern sits somewhere else entirely, in how the dividend itself is built.

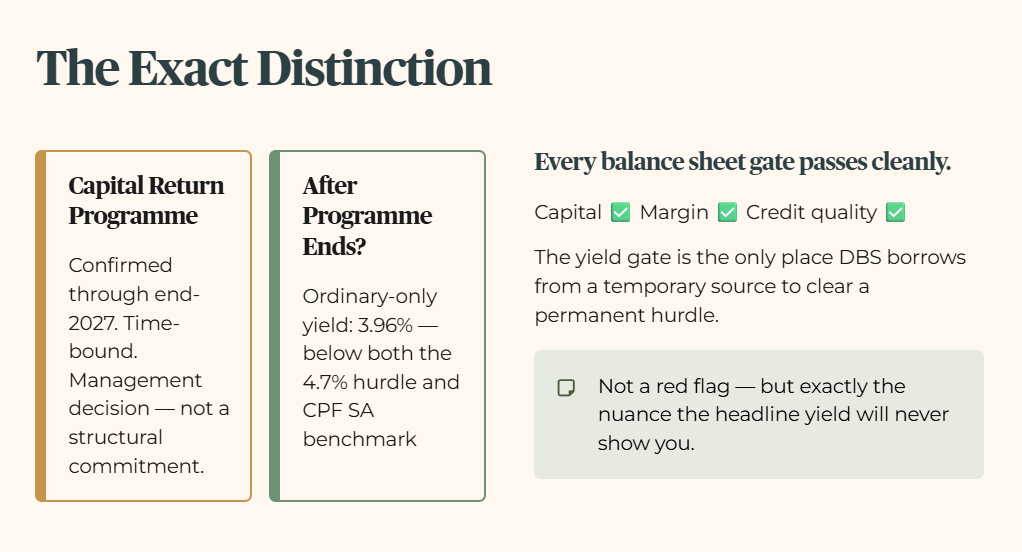

At a share price of S$66.74, DBS pays a quarterly dividend of 66 cents ordinary, plus 15 cents from a separate capital return programme. Annualise the ordinary tranche alone and you get an ordinary-only yield of approximately 3.96 percent, below both the 4.7 percent minimum yield hurdle and the 4.0 percent CPF SA benchmark. Add the capital return tranche and the headline yield reaches 4.70 percent, just clearing the hurdle.

This is the exact distinction Step 3 warned you about. The capital return programme is confirmed to run through end-2027, a deliberate, time-bound distribution decision by management, not a structural payout commitment. It is doing real work to get DBS across the yield hurdle today. But a forensic investor plans for what happens after the programme ends, not just for what the headline says now.

Every balance sheet gate here passes cleanly, capital, margin, and credit quality all sit inside Zone 1 territory on their own. The yield gate is the only place DBS is borrowing from a temporary source to clear a permanent hurdle. That is not a red flag. It is exactly the kind of nuance the headline yield number will never show you, and exactly why the audit exists.

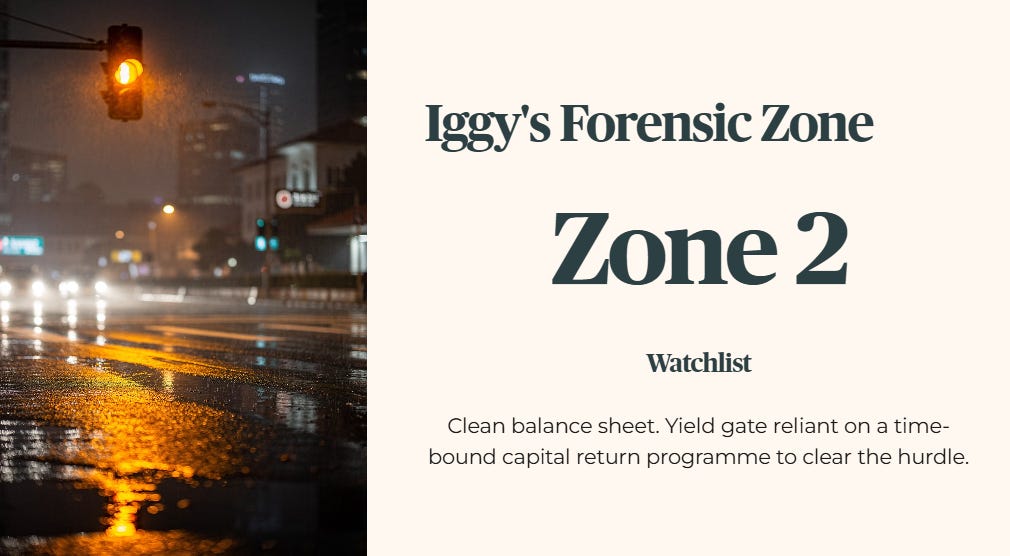

Iggy’s Forensic Zone: Zone 2, Watchlist.

🦎 Iggy’s Insight Block 2

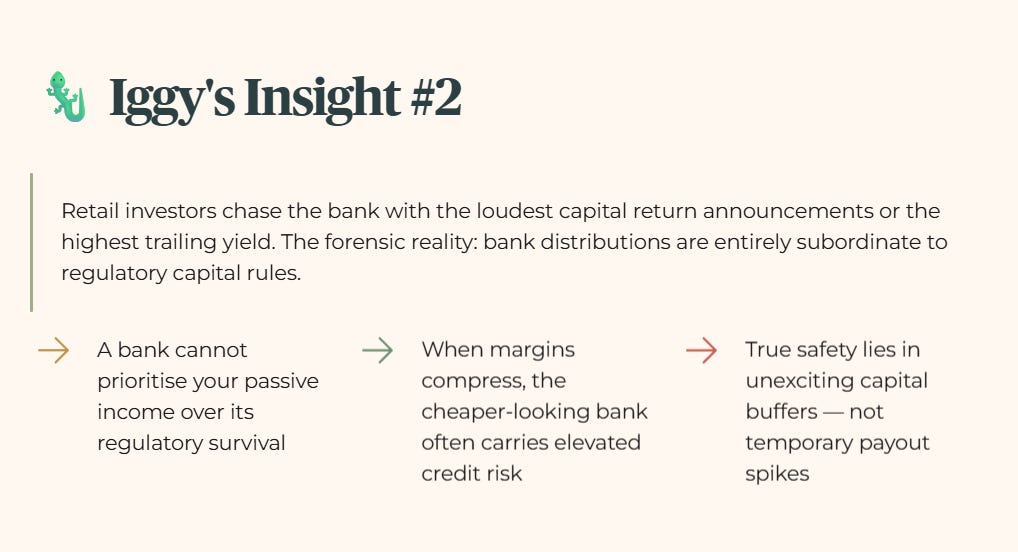

What a systemic banking audit reveals is the deep gap between the headline dividend narrative and the underlying balance sheet reality. Retail investors chase the bank with the loudest capital return announcements or the highest trailing yield. The forensic reality is that bank distributions are entirely subordinate to regulatory capital rules. A bank cannot prioritize your passive income over its regulatory survival. When interest margins compress globally, the bank that looks cheaper on paper is often the one carrying elevated credit risks or tighter capital adequacy margins. True safety lies in the unexciting capital buffers, not the temporary payout spikes.

Iggy’s Bottom Line

You can now independently audit any commercial banking financial statement by substituting irrelevant gearing metrics with regulatory capital ratios, and stress-testing the underlying credit quality.

Strategic consideration one. Audit your existing banking allocations immediately by locating the Transitional CET1 ratio in their latest quarterly filing, ensuring the figure clears a conservative 14 percent defensive threshold to protect against sudden capital conservation measures.

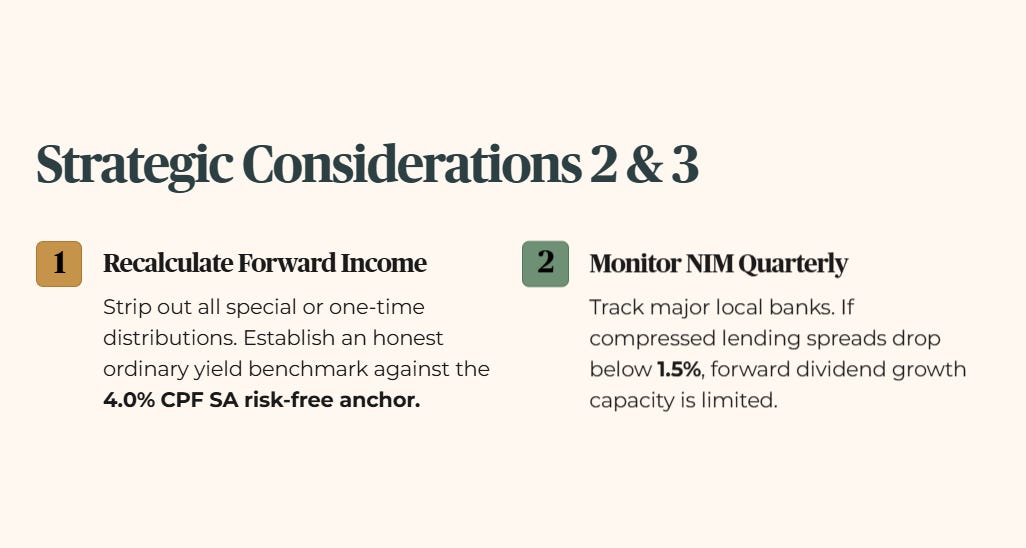

Strategic consideration two. Recalculate your portfolio’s forward income by stripping out all special or one-time distributions from your bank yield calculations, establishing an honest operational ordinary yield benchmark against the 4.0 percent CPF SA risk-free anchor.

Strategic consideration three. Monitor quarterly net interest margin trends across the major local banking institutions, noting if compressed lending spreads drop below the 1.5 percent soft flag threshold, which limits forward dividend growth capacity.

If the tides of the global interest rate cycle turn next month, does your bank hold enough excess capital to defend your retirement lifestyle, or are you holding an unhedged bet on a corporate lending book?

YOUR FORENSIC VERDICT, ONE PAGE.

The full audit is above. This is the Iggy Forensic Audit distilled to one A4 page — every number that matters, every flag that triggered, one clear verdict. Save it, print it, pull it out when this stock crosses your radar again, or when you need to refer to these data points for your retirement planning.

Iggy’s Forensic Disclaimer

This video is a paid partnership with Longbridge Singapore. It is intended for general awareness and does not constitute investment advice or a recommendation to buy, sell, or otherwise engage with any investment products or financial services. The author is not a licensed financial adviser and is not offering financial advice. All views expressed are solely those of the author and do not necessarily reflect the views of Longbridge Singapore. All investments carry risks, may not be suitable for everyone, and you may lose your investment principal. Past performance is not indicative of future results. You should seek independent financial advice if you are unsure about any investment decisions. This advertisement has not been reviewed by the Monetary Authority of Singapore.