Alibaba SDR ($HBBD): Is $5.80 the Real Fair Value?

The tech giant finally pays a dividend, but for the conservative SG portfolio, does the 1.3% yield justify the currency risk? Let’s run the numbers.

The Hook: The Allure of “Local” Big Tech

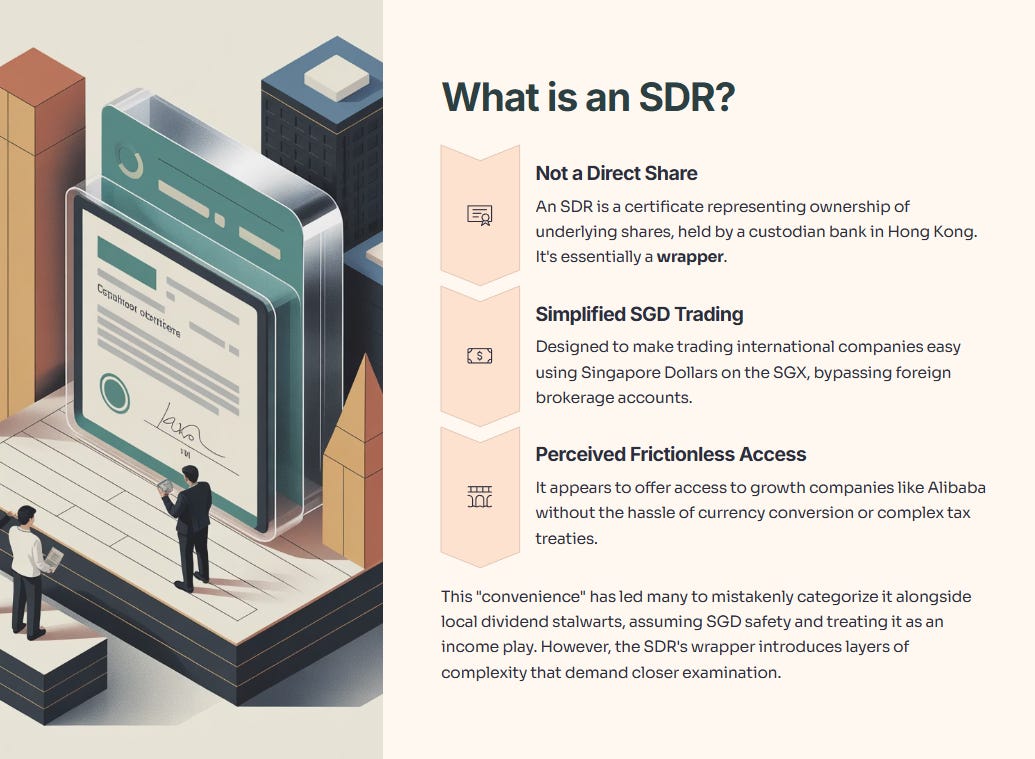

For years, Singaporean investors looked at Alibaba (BABA/9988) with a mix of envy and apprehension. We wanted the growth, but we hated the hassle of US tax treaties or converting SGD to HKD. Enter the Singapore Depository Receipt (SDR) — specifically Alibaba HK SDR 5-to-1 (HBBD.SI).

Suddenly, you can buy Chinese Big Tech with Singapore Dollars—currently trading under $5.00..., keep it in your CDP, and as of mid-2025, actually receive a dividend. It sounds like the perfect solution for the modern portfolio.

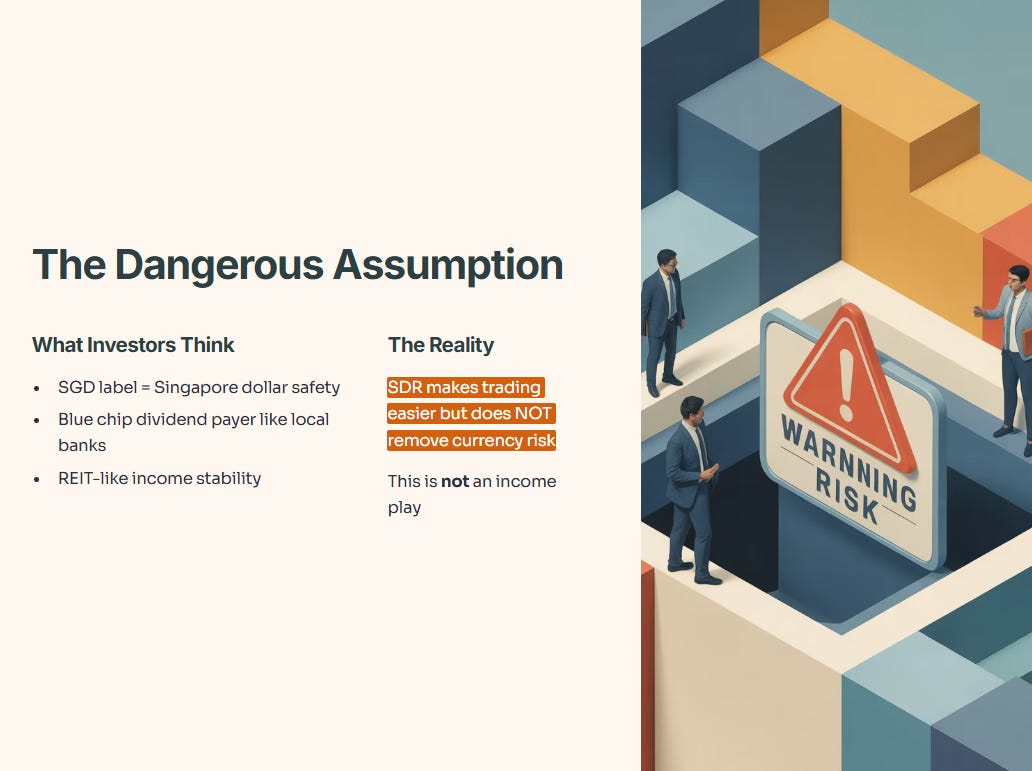

But I am seeing a dangerous trend among my readers. Many of you are treating this SDR like a “Blue Chip” dividend payer, akin to a local bank or a REIT. You see the “SGD” label and assume the safety of the Singapore dollar.

We need to look at the mechanics under the hood. The SDR makes trading easier, but it does not remove the currency risk, and more importantly, the yield mathematics suggests this is not an income play.

In This Article:

• The Hard Numbers: Breaking Down the “Payout”

• Valuation: The “Value Trap” or the Deal of the Decade?

• InvestingPro Reality Check: Is the Upside Real?

• The “SDR” Friction: What You Are Really Paying For

• Financial Health: Can They Keep Paying?

• Iggy’s Playbook: The Investor’s Action Plan

• Iggy's Verdict / Conclusion

The Hard Numbers: Breaking Down the “Payout”

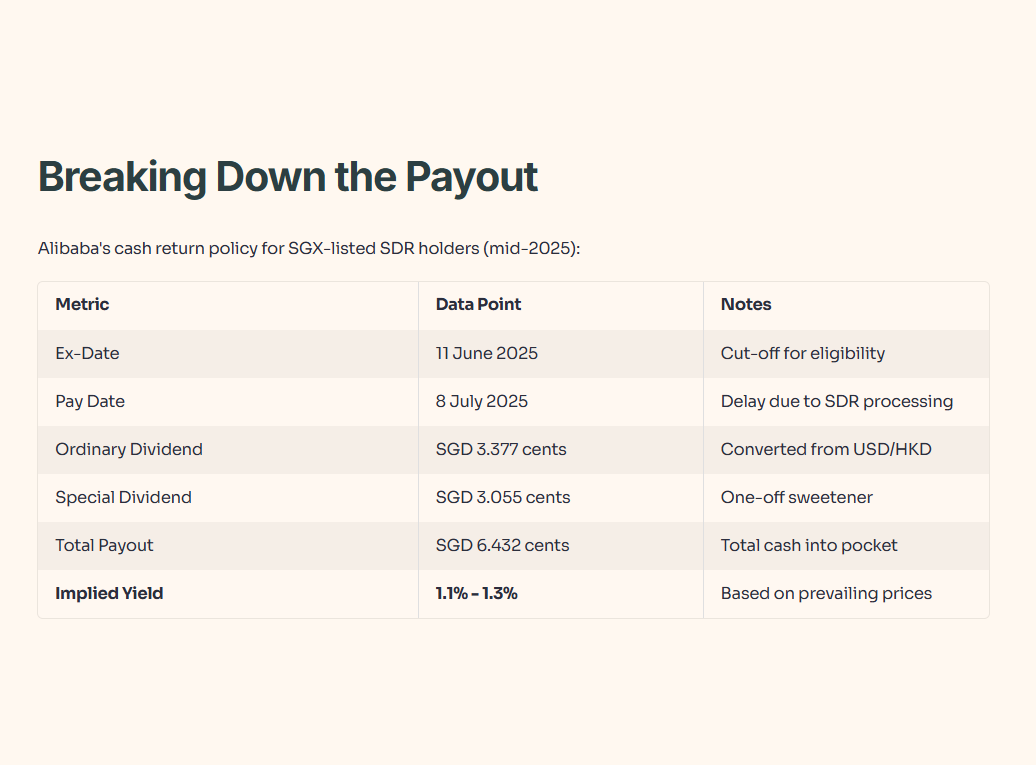

Let’s look at the recent corporate action that got everyone excited. Alibaba initiated a cash return policy. Here is what that looked like for the SGX-listed SDR holder in mid-2025:

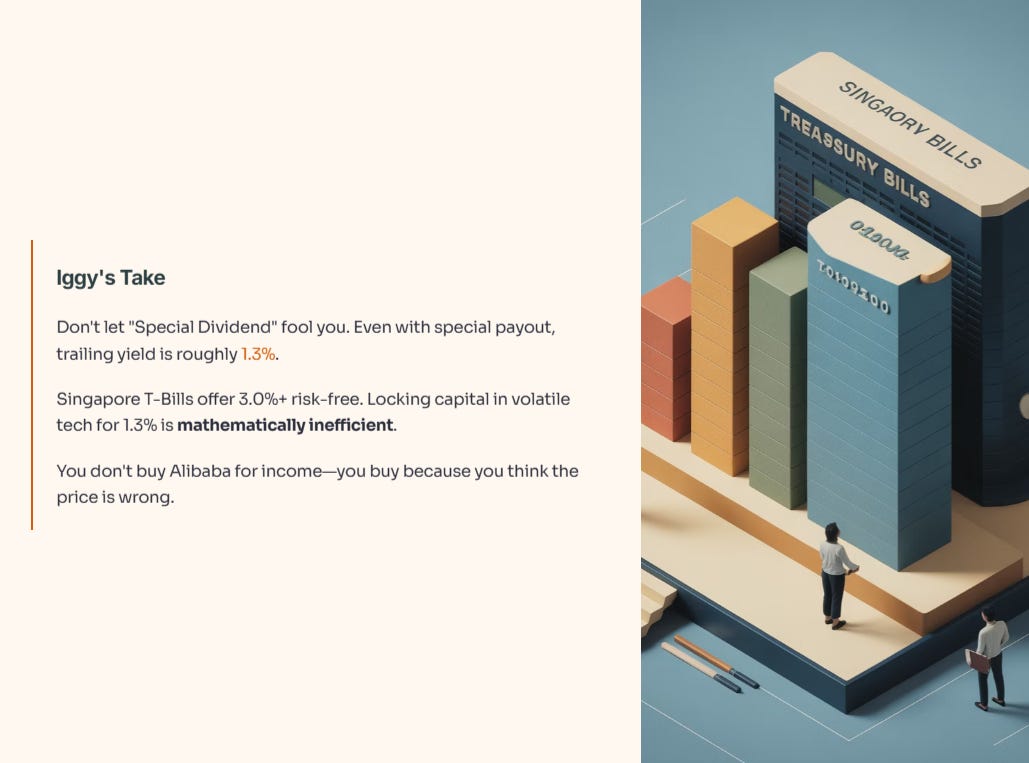

Iggy’s Take:

Do not let the headline “Special Dividend” fool you. Even with the special payout, we are looking at a trailing yield of roughly 1.3%. In a world where Singapore T-Bills are still offering competitive risk-free rates (often 3.0%+), locking up capital in a volatile tech stock for 1.3% income is mathematically inefficient. You do not buy Alibaba for the income; you buy it because you think the price is wrong.

Valuation: The “Value Trap” or the Deal of the Decade?

This is where the argument gets interesting. While the yield is negligible, the valuation metrics for the underlying Alibaba Group are historically compressed.

The consensus among analysts covering the primary listings (HK/US) is broadly positive. They cite recovering cloud momentum and aggressive cost discipline. The stock has been trading at a Price-to-Book (P/B) ratio hovering around 0.35x—levels that usually suggest a company is going bankrupt, not one generating billions in free cash flow.

However, cheap can stay cheap for a long time.

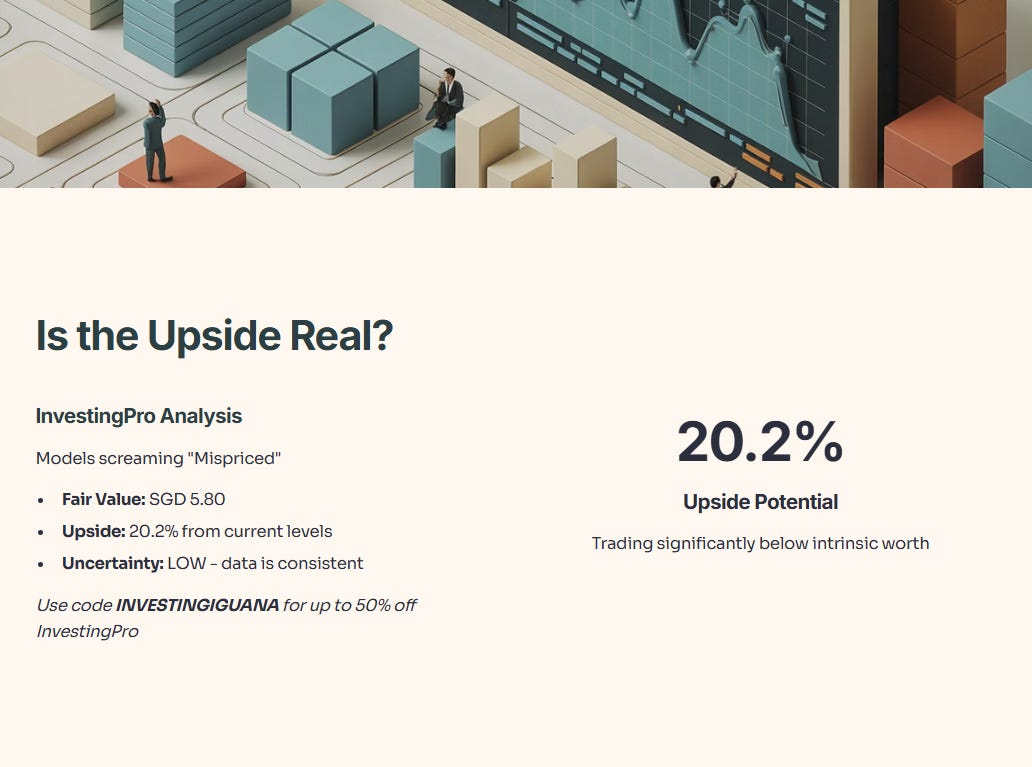

Data Check: Is the Upside Real?

I don’t just guess at valuations based on feelings. I check the institutional models to see if the math supports the narrative.

Source: InvestingPro. Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: The models are screaming “Mispriced.” InvestingPro calculates a Fair Value of SGD 5.80, implying a precise 20.2% Upside from current levels. Even better? The model flags this valuation with “LOW Uncertainty,” meaning the data is consistent. We are looking at a stock trading significantly below its intrinsic worth.

The “SDR” Friction: What You Are Really Paying For

When you buy HBBD.SI, you are buying a wrapper. That wrapper costs money.

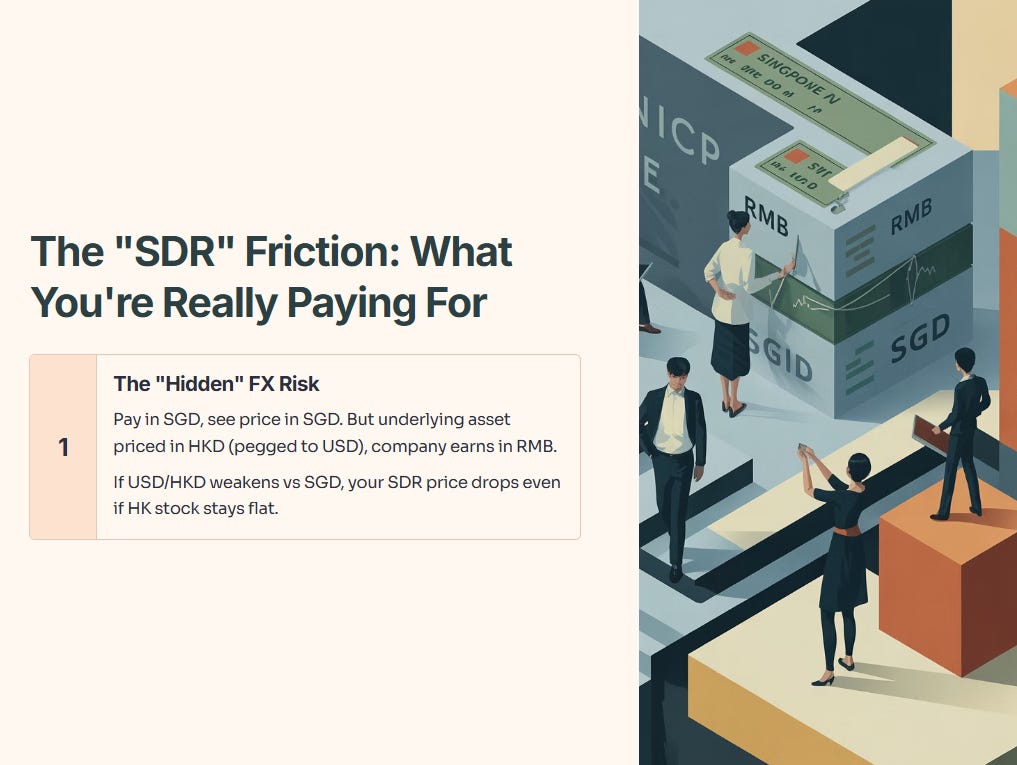

1. The “Hidden” FX Risk

You pay in SGD, and you see the price in SGD. But the underlying asset is priced in HKD (which is pegged to USD), and the company earns in RMB.

If the USD/HKD weakens against the SGD, your SDR price drops even if Alibaba’s stock price in Hong Kong stays flat. You are taking on currency risk without realizing it.

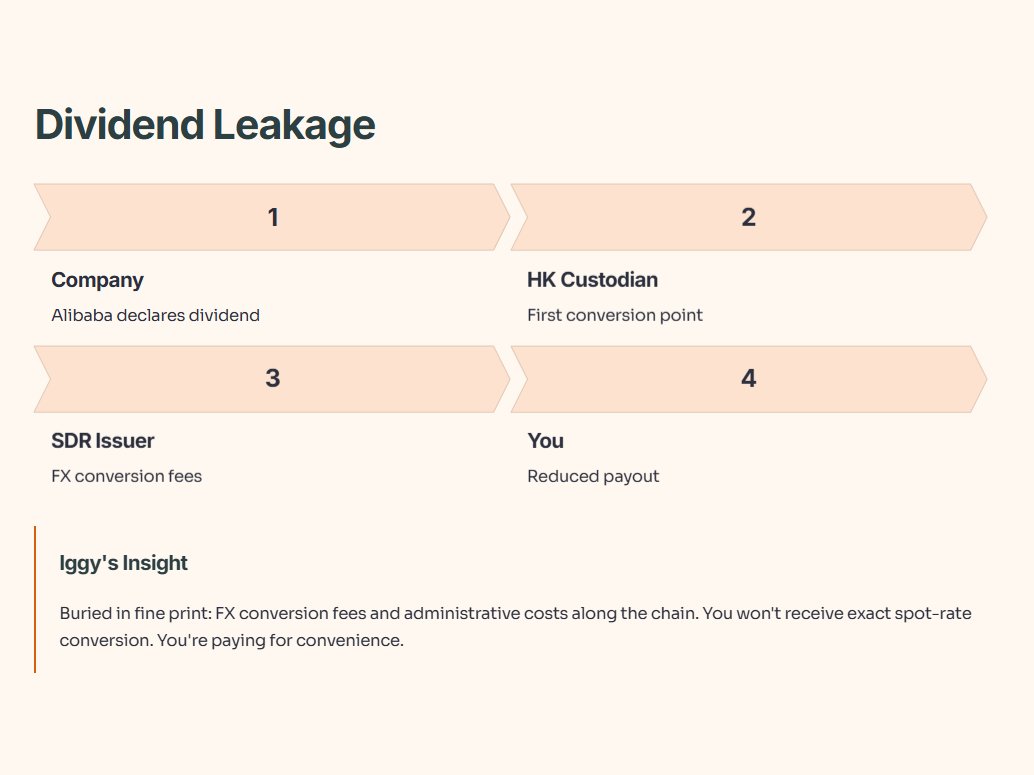

2. The Dividend Leakage

Iggy’s Insight:

This is the part usually buried in the fine print. When Alibaba pays a dividend, it goes from the Company -> HK Custodian -> SDR Issuer -> You.

Along this chain, there are FX conversion fees and potential administrative costs. You will not receive the exact spot-rate conversion of the dividend. You are paying for the convenience of not having to open a Hong Kong brokerage account.

3. The SRS Problem

For my readers planning their retirement buckets: Alibaba SDRs are currently NOT SRS eligible. You must use cash. This is a massive disadvantage compared to buying local banks or REITs where you can deploy tax-advantaged capital.

Financial Health: Can They Keep Paying?

If we are going to treat this as a long-term hold, we need to ensure the balance sheet isn’t a ticking time bomb. The “SDR” doesn’t have debt, but the underlying company does.

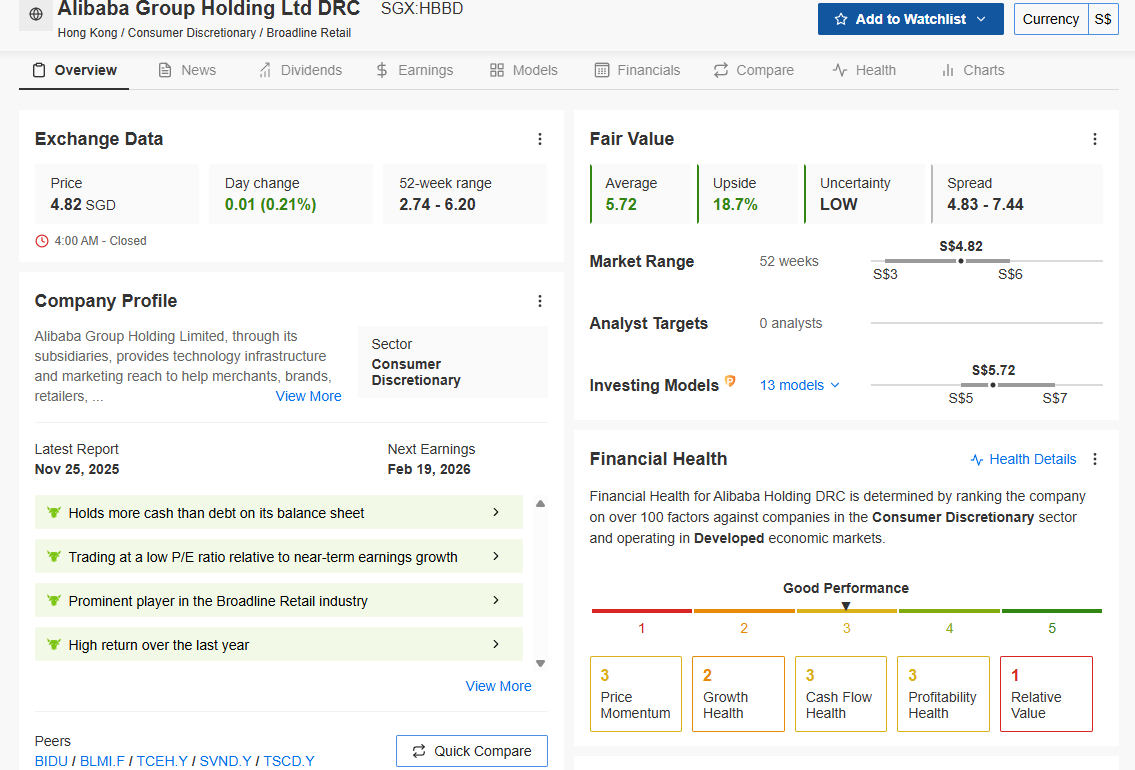

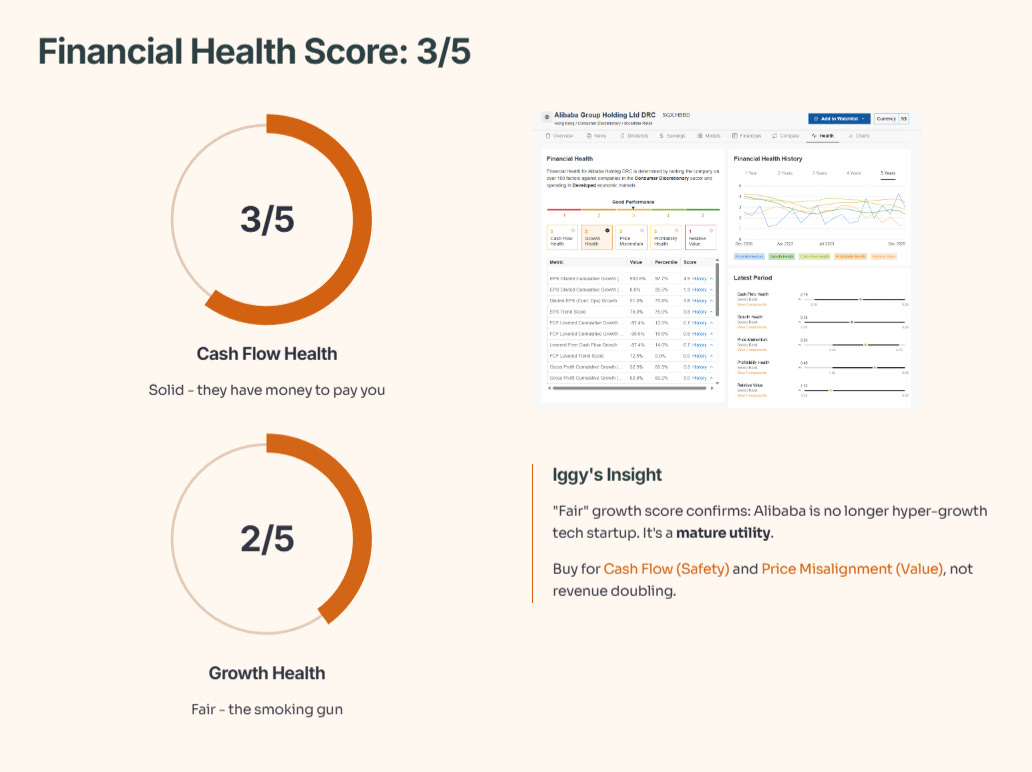

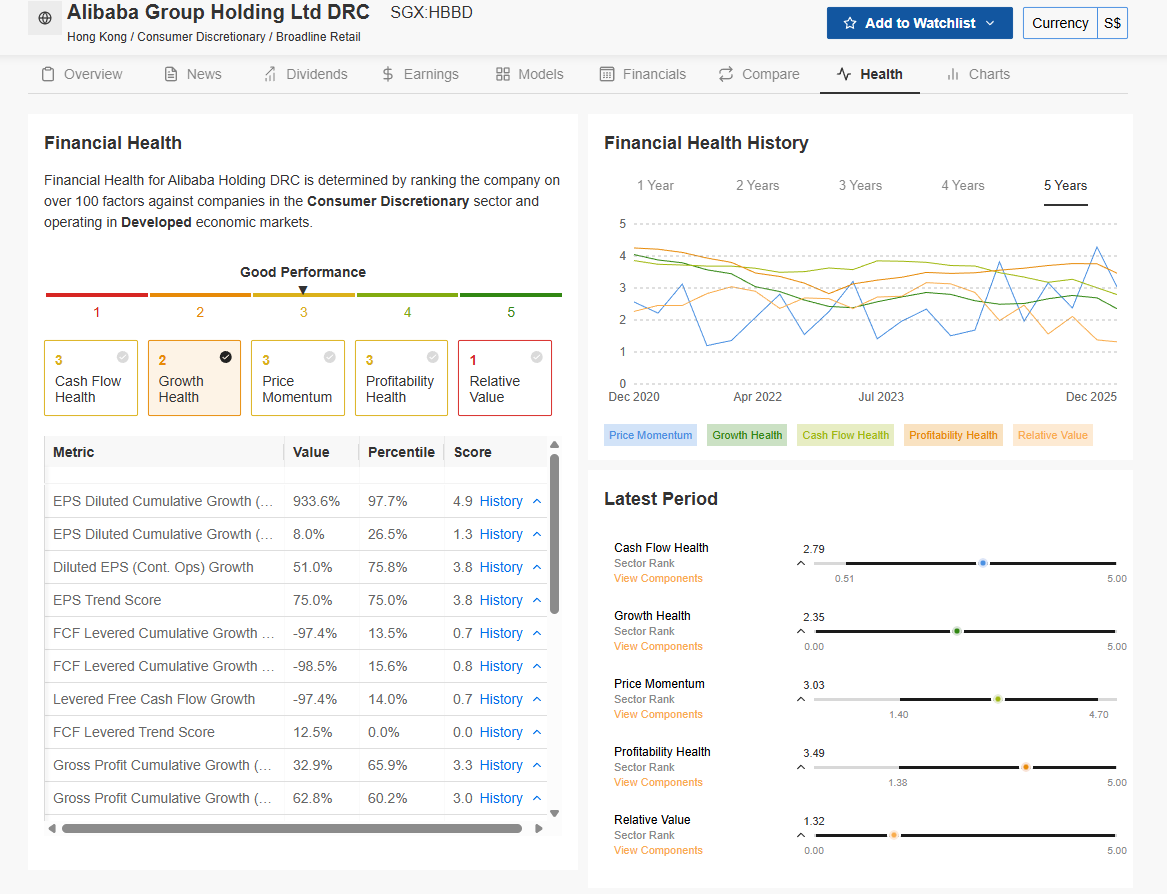

Data Check: Financial Health Score

Is the dividend actually safe? Let’s look at the health score of the underlying business.

The Analysis: InvestingPro gives Alibaba a Financial Health Score of 3/5 (”Good Performance”). But look closer at the breakdown in the chart above.

Cash Flow Health: 3/5 (Solid). They have the money to pay you.

Growth Health: 2/5 (Fair).

Iggy’s Insight: This “Fair” growth score is the smoking gun. It confirms that Alibaba is no longer a hyper-growth tech startup. It is a mature utility. You are buying it for the Cash Flow (Safety) and the Price Misalignment (Value), not because you expect it to double its revenue next year.

Iggy’s Playbook: The Investor’s Action Plan

So, should you buy the Alibaba SDR? It depends entirely on which pocket of money you are using.