The April–May 2026 Yield Trap — Why a 12% Dividend Can Destroy Your Capital

Before you collect that April dividend, check whether the company can actually afford to pay it.

A forensic audit of every SGX dividend name going ex in April and May — ranked by structural integrity.

A technology hardware manufacturer is bleeding S$92.6 million in dividends against only S$38.4 million in operating cash flow, producing a mathematically disastrous 240.6% payout ratio.

If you are deploying your CPF SA capital into this counter assuming the 4.57% yield is structurally safe, you are actively funding the destruction of your own principal. Today, you will walk away knowing exactly which April and May dividend names possess the fortress balance sheets to protect your retirement, and which ones are engineered illusions.

In This Article:

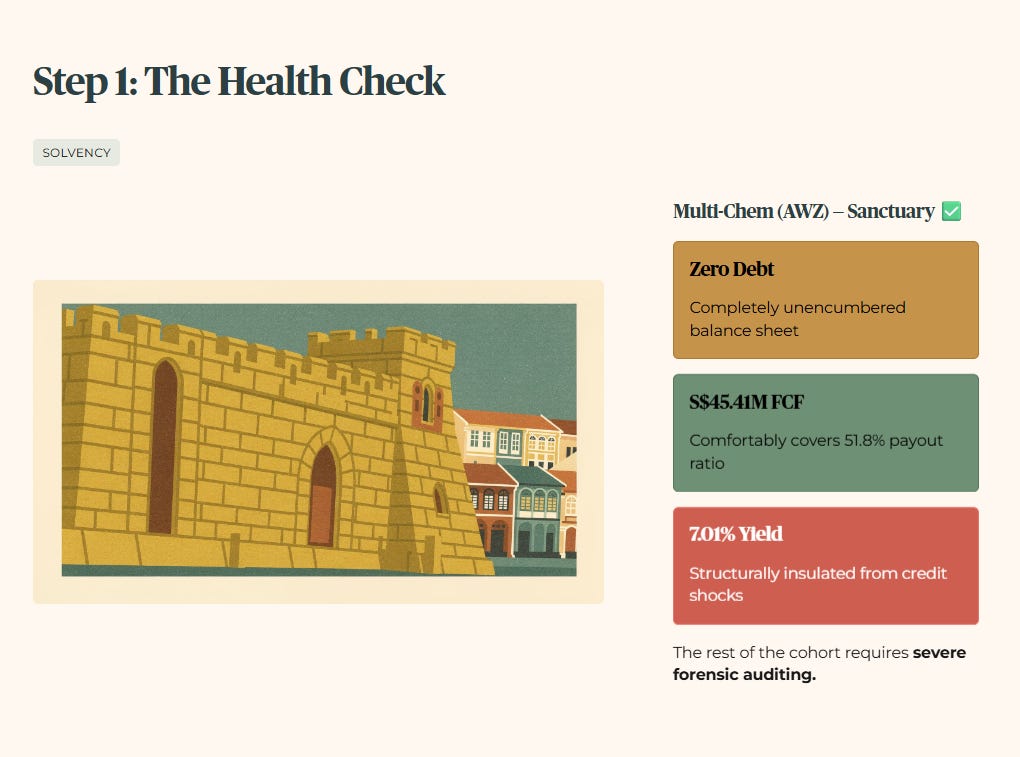

Step 1 The Health Check Solvency

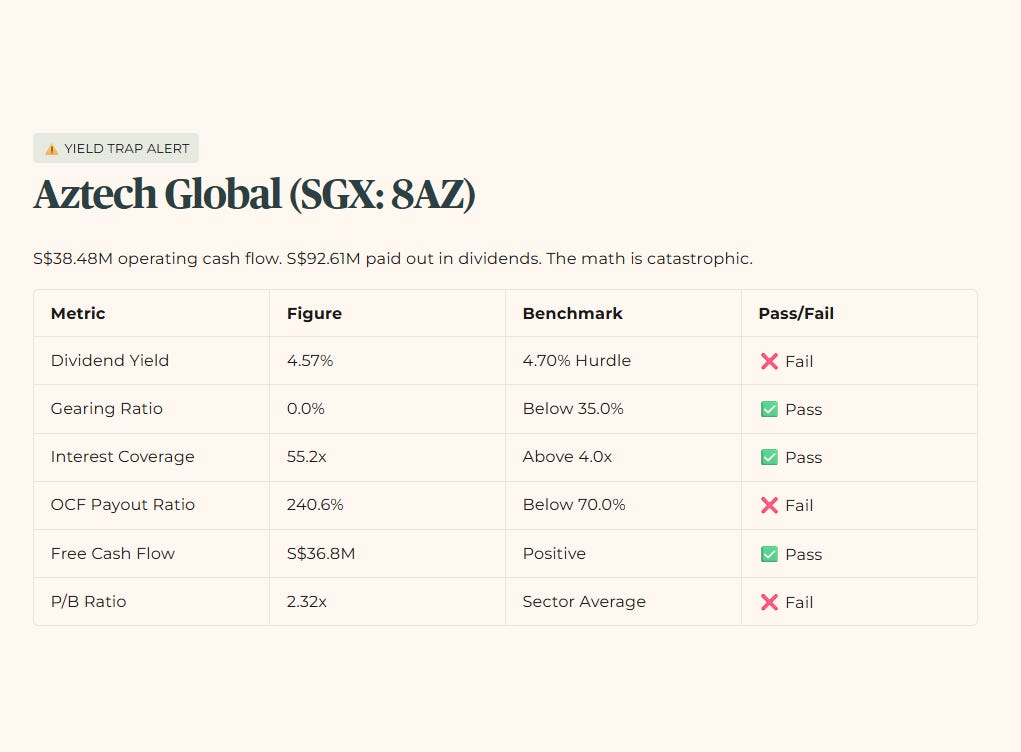

Yield Trap Alert Aztech Global SGX 8AZ

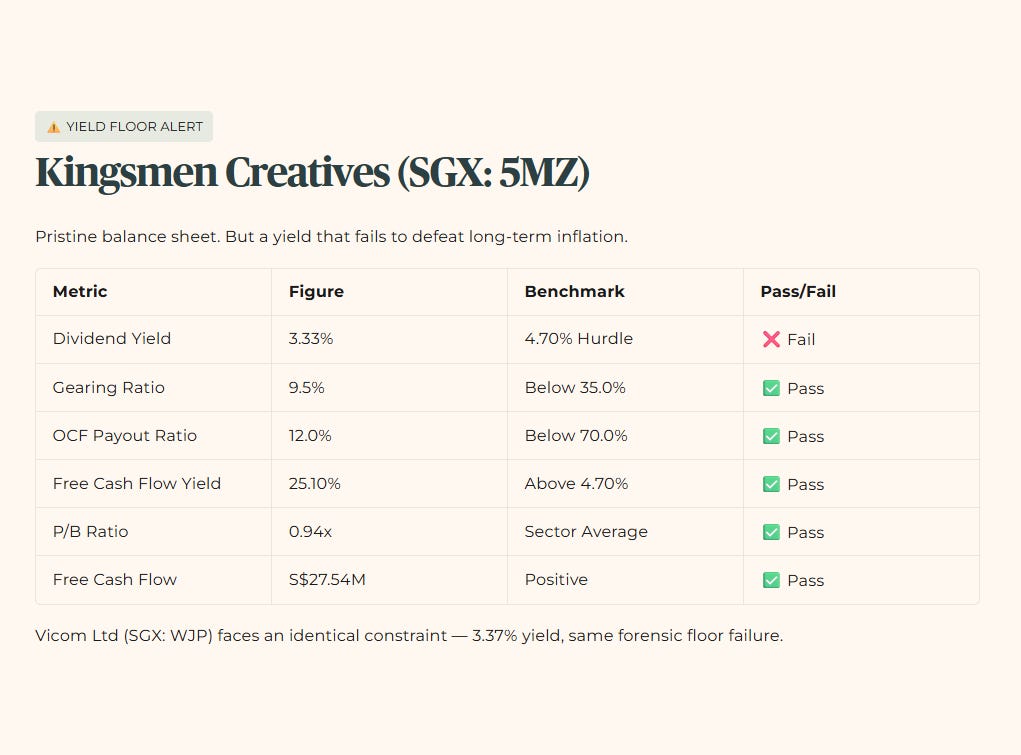

Yield Floor Alert Kingsmen Creatives SGX 5MZ

Step 2 The Wealth Check Yield and Cash Flow

Iggys Insight The Cash Flow Trap Most Retail Investors Miss

Step 3 The Price Check Valuation

Iggys Insight What the Vicom Fair Value Gap Is Actually Telling You

Step 4 The Bottom Line Forensic Stance

Iggys Forensic Compliance Standards Standard Disclaimer

Step 1. The Health Check (Solvency)

We subject every active thesis to the Triage Rule. Multi-Chem (SGX: AWZ) clears the threshold completely, operating a zero-debt balance sheet that generates S$45.41 million in free cash flow to comfortably cover its highly disciplined 51.8% payout ratio. For a 58-year-old in Toa Payoh managing an SRS drawdown, this acts as a Sanctuary asset, providing an unencumbered 7.01% yield structurally insulated from credit shocks.

The rest of the cohort requires severe forensic auditing.

YIELD TRAP ALERT — AZTECH GLOBAL (SGX: 8AZ)

This is where the dividend math breaks.

Aztech Global generated S$38.48 million in operating cash flow but is paying out an astonishing S$92.61 million in dividends. The current 240.6% OCF Payout violently exceeds Iggy’s 70% threshold and sits massively above the company’s own historical three-year average.

Venture Corporation (SGX: V03) currently sits at a 4.68% yield, maintaining strict capital discipline rather than artificially inflating its distributions to appease the market. However, the forensic stress-test produces an uncomfortable modelled scenario: if a macro demand contraction in technology hardware exports reduces revenue by 10%, the distribution could become mathematically unsustainable under that modelled condition, requiring a dividend rebase in the vicinity of 77.5% to bring the payout ratio back under the 70% structural safety ceiling. For a 62-year-old in Toa Payoh managing an SRS drawdown, this constitutes a material Watchlist risk that warrants close monitoring before any capital commitment.

YIELD FLOOR ALERT — KINGSMEN CREATIVES (SGX: 5MZ)

The pristine balance sheet cannot compensate for a yield that fails to defeat long-term inflation.

Kingsmen Creatives generated S$33.5 million in operating cash flow to comfortably fund a highly conservative S$4 million dividend. However, the 3.33% yield falls critically below Iggy’s 4.7% minimum hurdle, despite the 12.0% payout ratio sitting vastly superior to the company’s three-year historical average. Vicom Ltd (SGX: WJP) faces an identical structural constraint, currently posting a 3.37% yield that similarly fails the mandatory forensic floor.

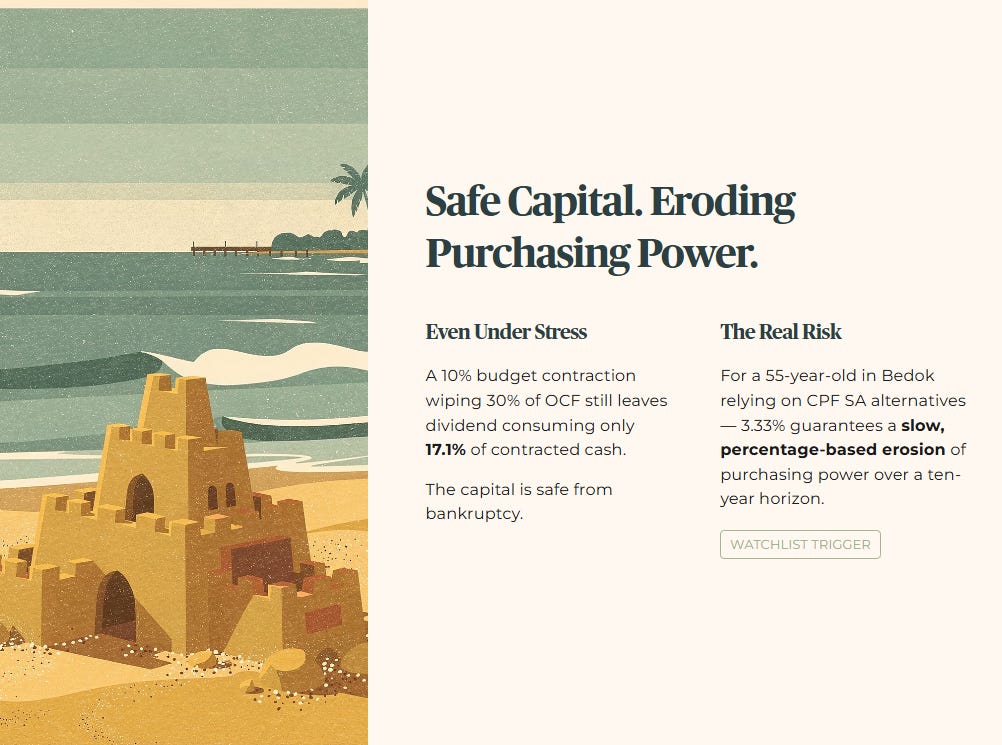

If corporate exhibition budgets contract by 10%, wiping out 30% of operating cash flow, the dividend still only consumes 17.1% of the newly contracted cash, leaving the distribution mathematically secure but inflation-exposed. For a 55-year-old in Bedok relying on CPF SA alternatives, this is a Watchlist Trigger. The capital is perfectly safe from bankruptcy, but the 3.33% return guarantees a slow, percentage-based erosion of your purchasing power over a ten-year horizon.

Step 2. The Wealth Check (Yield and Cash Flow)

We do not evaluate yield in a vacuum. The structural baseline of all Singaporean capital allocation is the prevailing risk-free rate. The calculation to determine if you are adequately compensated for holding equity risk is non-negotiable: Asset Yield (%) minus the current T-Bill rate equals your Risk Premium. With the current T-Bill verified at 1.47%, the math becomes the ultimate arbiter of truth.

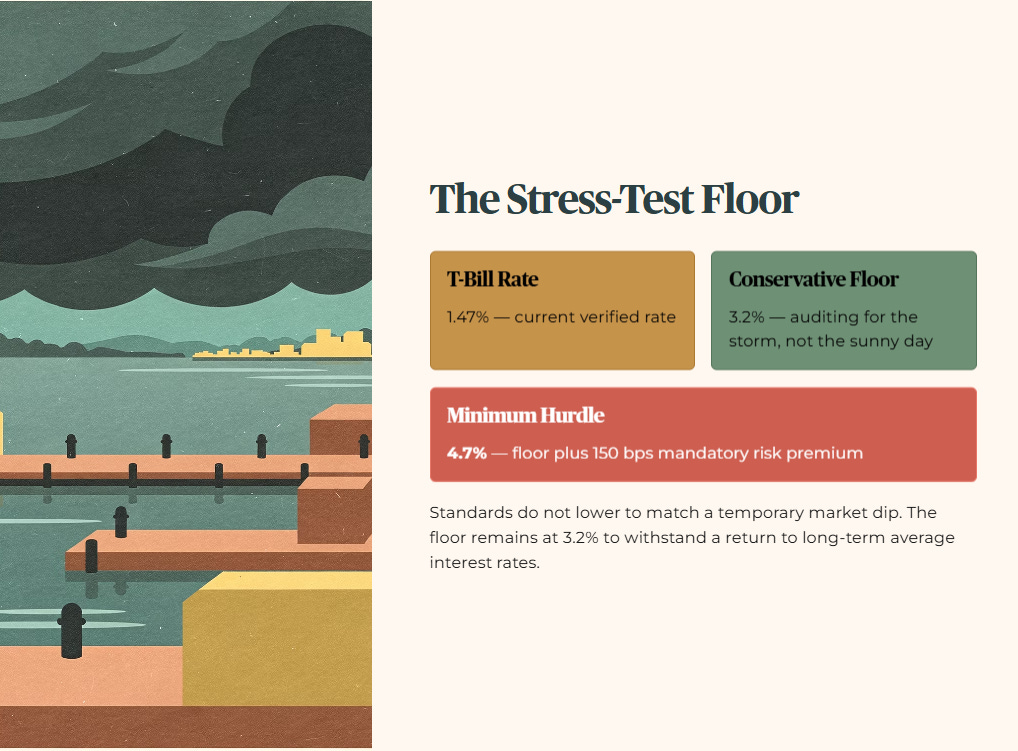

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. While the T-Bill sits at 1.47%, I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

Now that the 4.7% hurdle is hard-coded, the next step is to run Multi-Chem, Aztech, Kingsmen, and Vicom through a yield‑minus‑T‑Bill screen — and one of the “income” counters you have just read about mathematically fails the sanctuary test the moment this calculation is applied.