SGX Alert: Stop Treating The Assembly Place Like The Next Coliwoo

Why a S$6.2M profit figure hides a massive gap between this Catalist debut and the Coliwoo Mainboard listing.

If you’re new here, welcome. I’m Iggy, your Singapore-based Private Investor and Market Researcher. Since October 2025, we’ve built a community of over 5,300 investors and produced over 1,300 videos and 400 articles. We are home to a growing “Inner Circle” of over 100 paid members across YouTube and Substack.

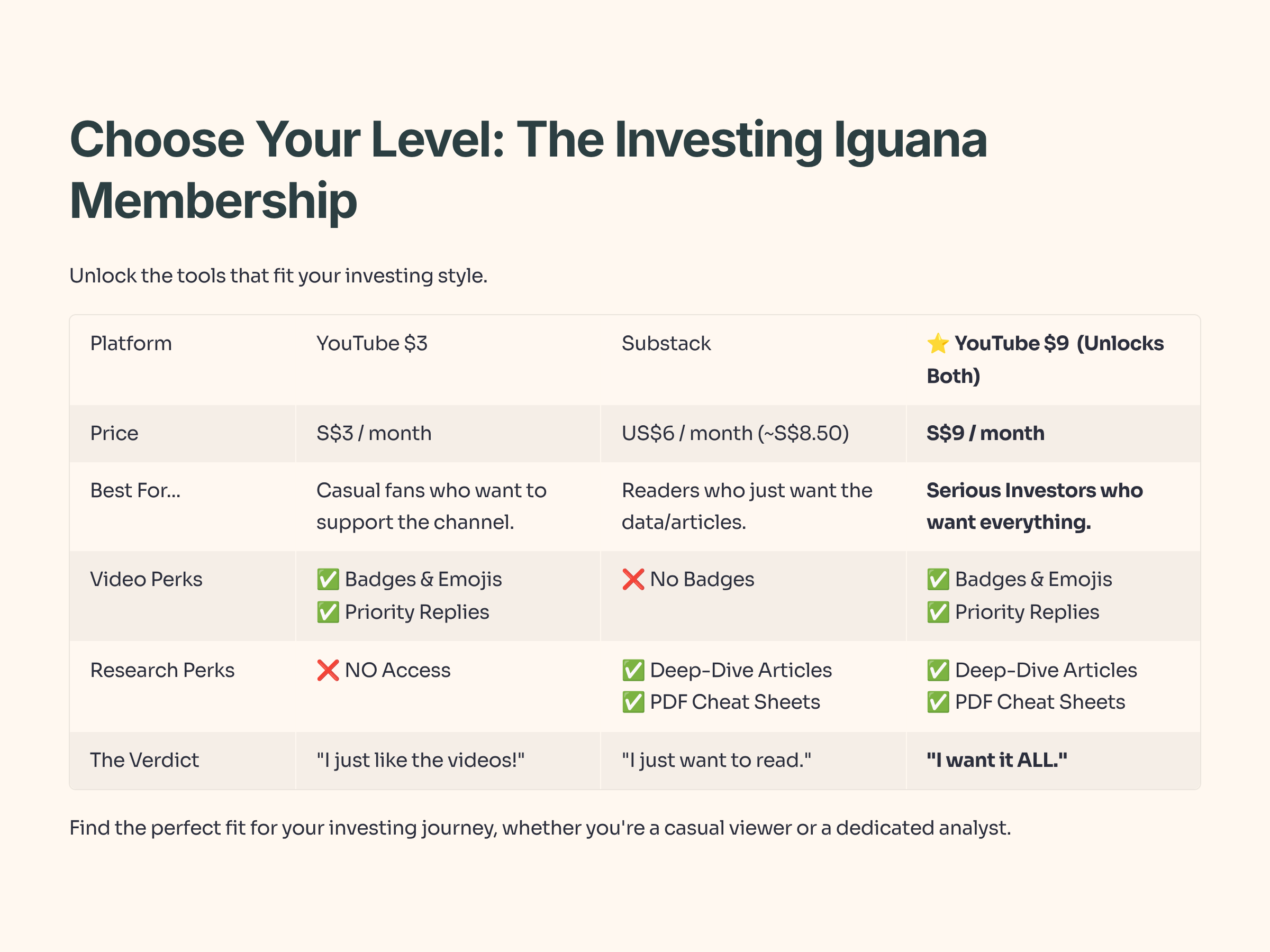

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

Table of Contents

The Big Flaw: Why TAP isn't the "next Coliwoo"

Head-to-Head: TAP vs. Coliwoo data comparison

Asset-Light vs. Asset-Heavy: The profit vs. cash disconnect

The Dividend Ghost: Why growth takes priority over payouts

Valuation Check: Using LHN models as a reality check

Action Plan: Strategy for retirees and growth hunters

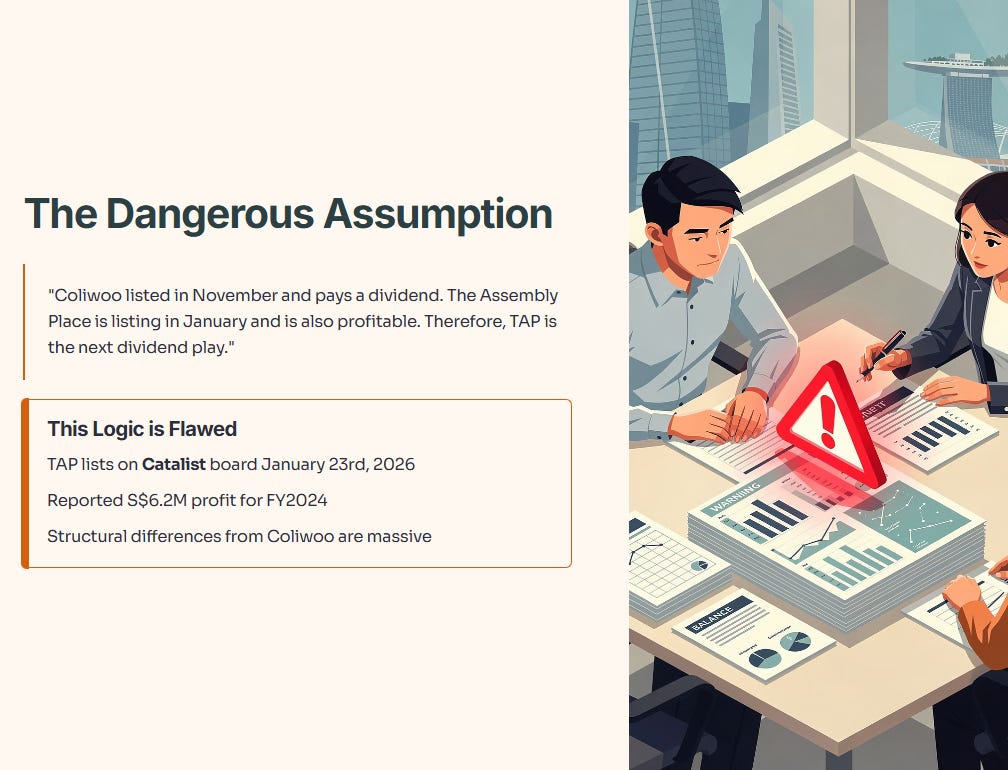

There is a dangerous assumption floating around the SGX forums right now. It goes like this: “Coliwoo listed in November and pays a dividend. The Assembly Place (TAP) is listing in January and is also profitable. Therefore, TAP is the next dividend play.”

This logic is flawed.

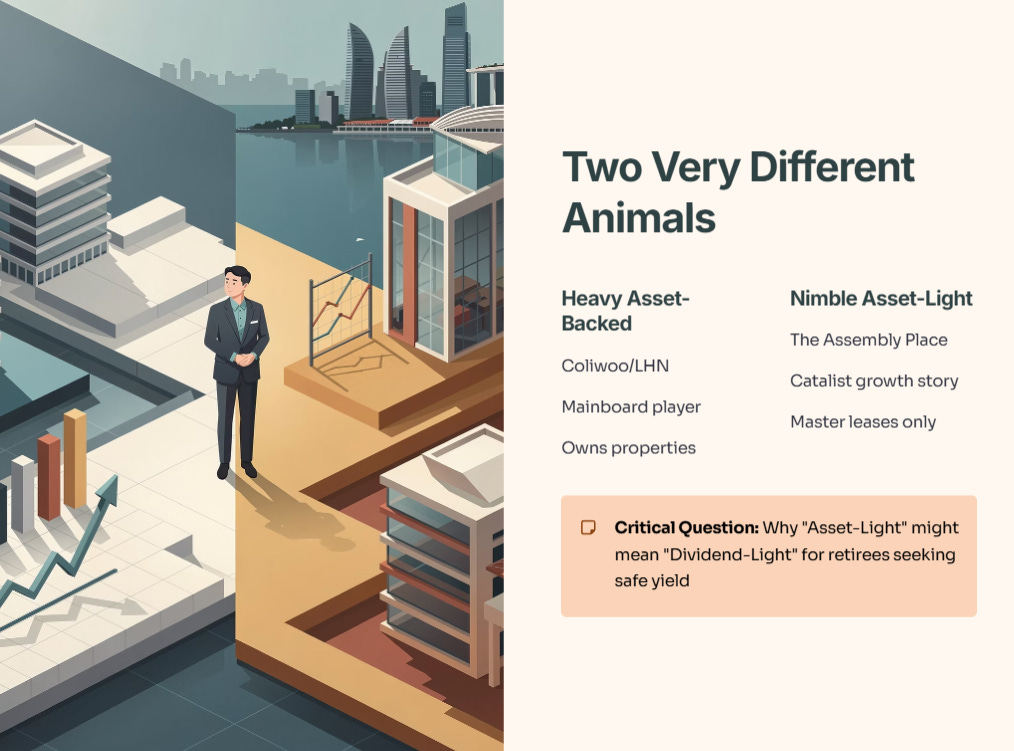

The Assembly Place is listing on the Catalist board this January 23rd, 2026. While the headline numbers look attractive—specifically a reported S$6.2 million profit for FY2024—the structural differences between TAP and Coliwoo are massive.

As a researcher focused on capital preservation, I see a clear divergence here. We are looking at two very different animals: one is a heavy, asset-backed Mainboard player (Coliwoo/LHN), and the other is a nimble, asset-light Catalist growth story (TAP). If you are a retiree looking for safe yield, you need to understand why “Asset-Light” might mean “Dividend-Light.”

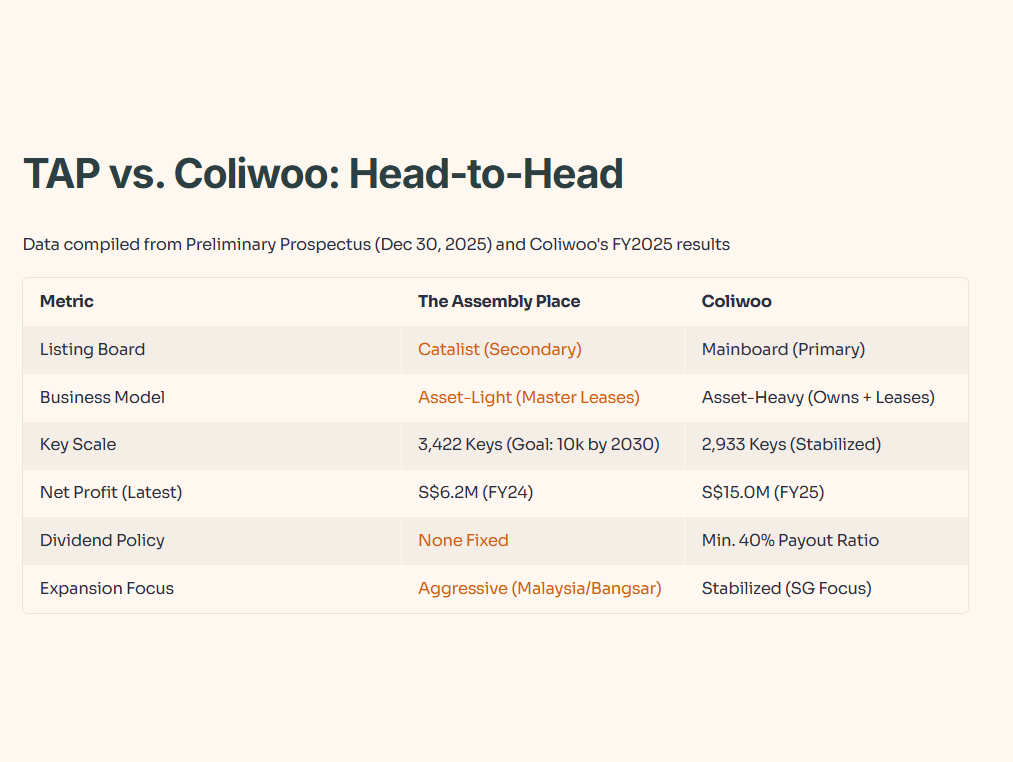

The Data: TAP vs. Coliwoo Head-to-Head

Let’s look at the raw comparison. I’ve compiled this data from the Preliminary Prospectus lodged on Dec 30, 2025, and Coliwoo’s recent FY2025 results.

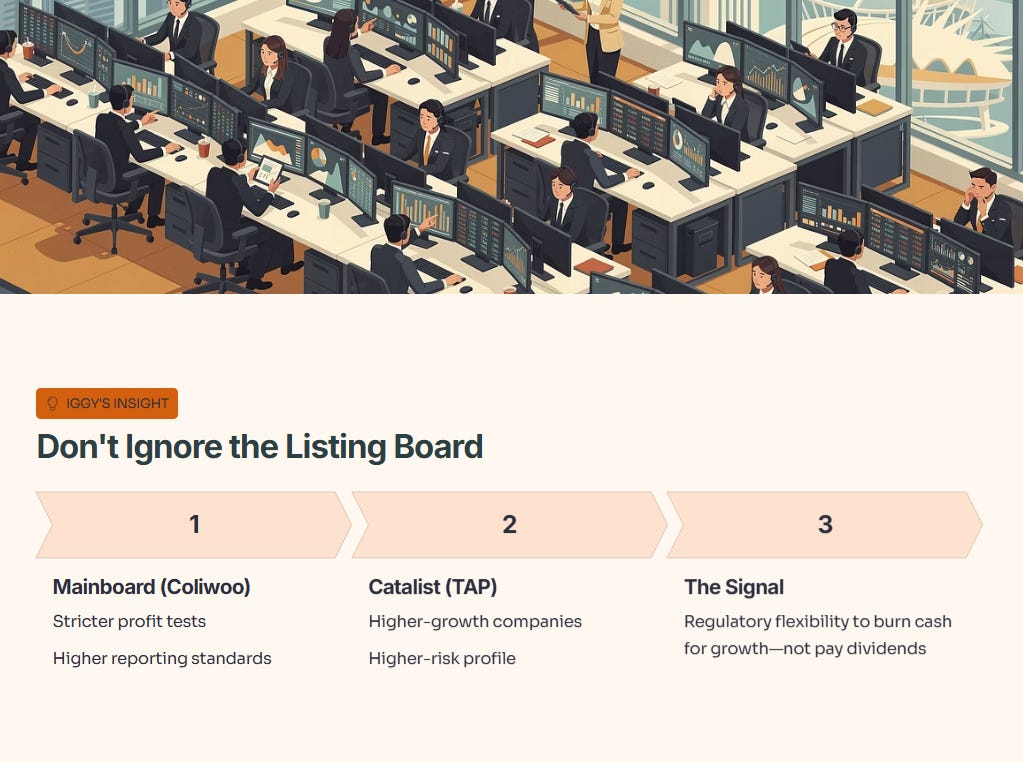

Iggy’s Insight:

Do not ignore the listing board. Mainboard listings (Coliwoo) require stricter profit tests and reporting standards. Catalist listings (TAP) are designed for higher-growth, higher-risk companies. When a company chooses Catalist despite having S$6.2M in profit, it usually signals they want regulatory flexibility to burn cash for growth—not to pay you dividends.

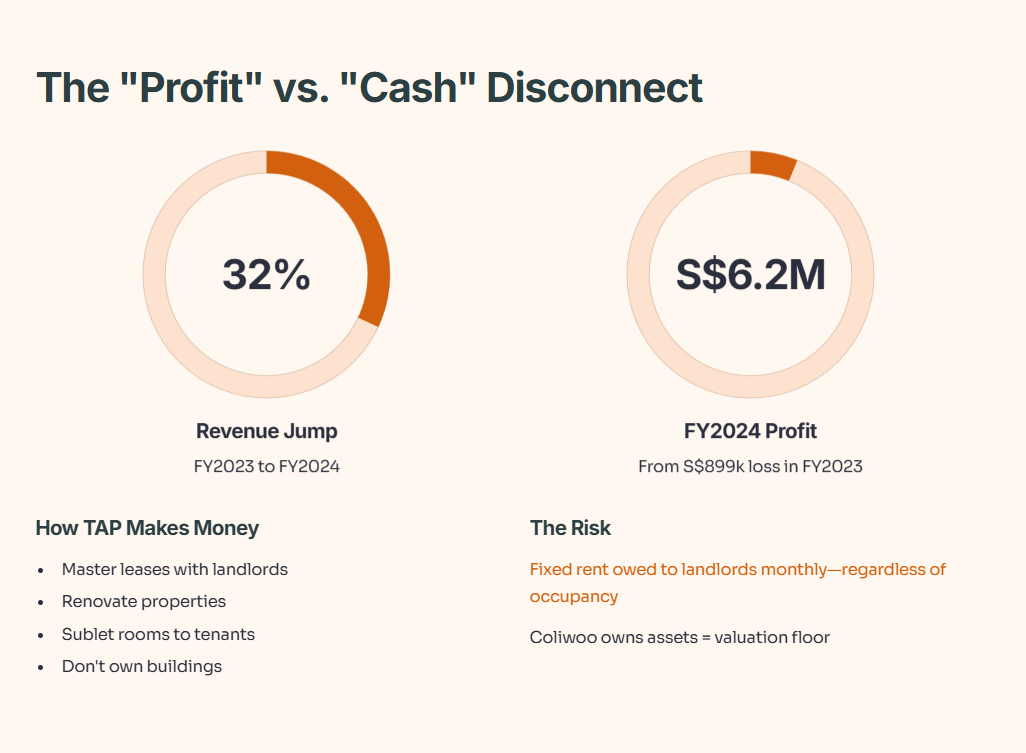

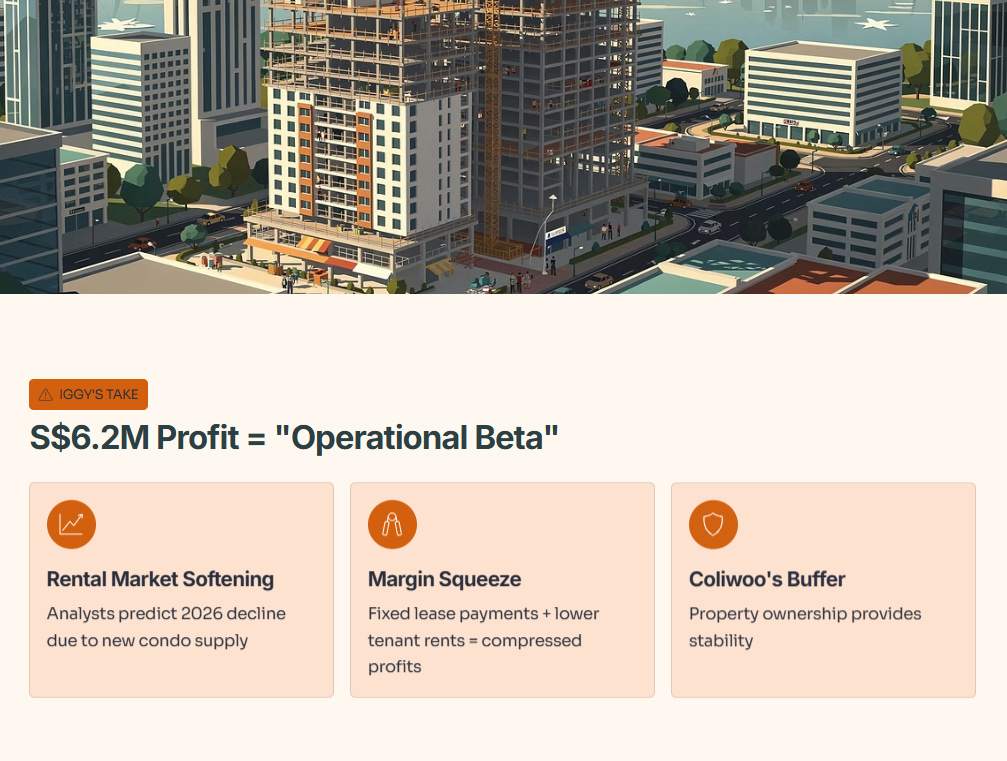

1. The “Profit” vs. “Cash” Disconnect

The headline story for TAP is the turnaround. They went from a loss of S$899,000 in FY2023 to a profit of **S$6.2 million in FY2024**. That is an impressive 32% revenue jump.

However, you must look at how they make money. TAP operates an “Asset-Light” model. They don’t own most of the buildings; they sign master leases with landlords (like Centurion or individual owners), renovate them, and sublet the rooms.

This is excellent for Return on Equity (ROE) when times are good because you don’t have heavy capital tied up in land. But it is terrible for cash flow stability when occupancy drops. You still owe the landlord rent every month, regardless of whether you have tenants.

Coliwoo, by contrast, owns a significant portion of its assets (via the LHN ecosystem). This provides a floor to their valuation—the physical brick and mortar.

Iggy’s Take:

I view TAP’s S$6.2M profit as “Operational Beta.” It’s highly sensitive to rental rates. If Singapore’s rental market softens in 2026 (which analysts are predicting due to new condo supply), TAP’s margins get squeezed from both sides: fixed lease payments to landlords and lower rents from tenants. Coliwoo has the buffer of property ownership.

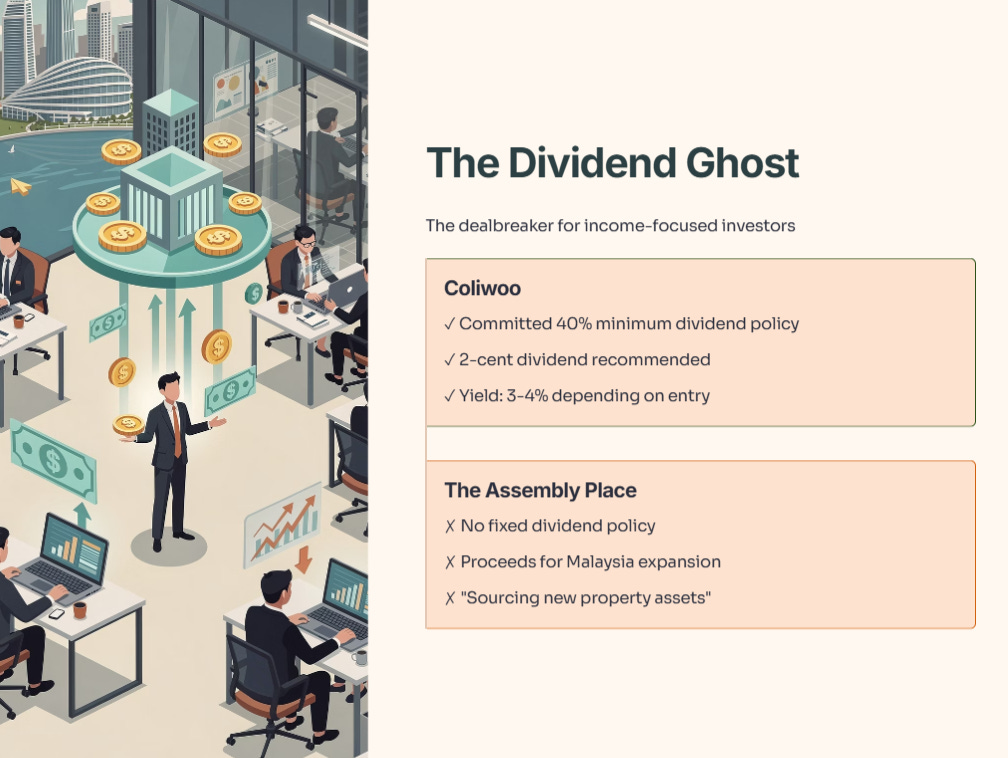

2. The Dividend Ghost

This is the dealbreaker for my income-focused readers.

Coliwoo explicitly committed to a dividend policy of at least 40% of profit. They just recommended a 2-cent dividend, translating to a yield of roughly 3-4% depending on your entry.

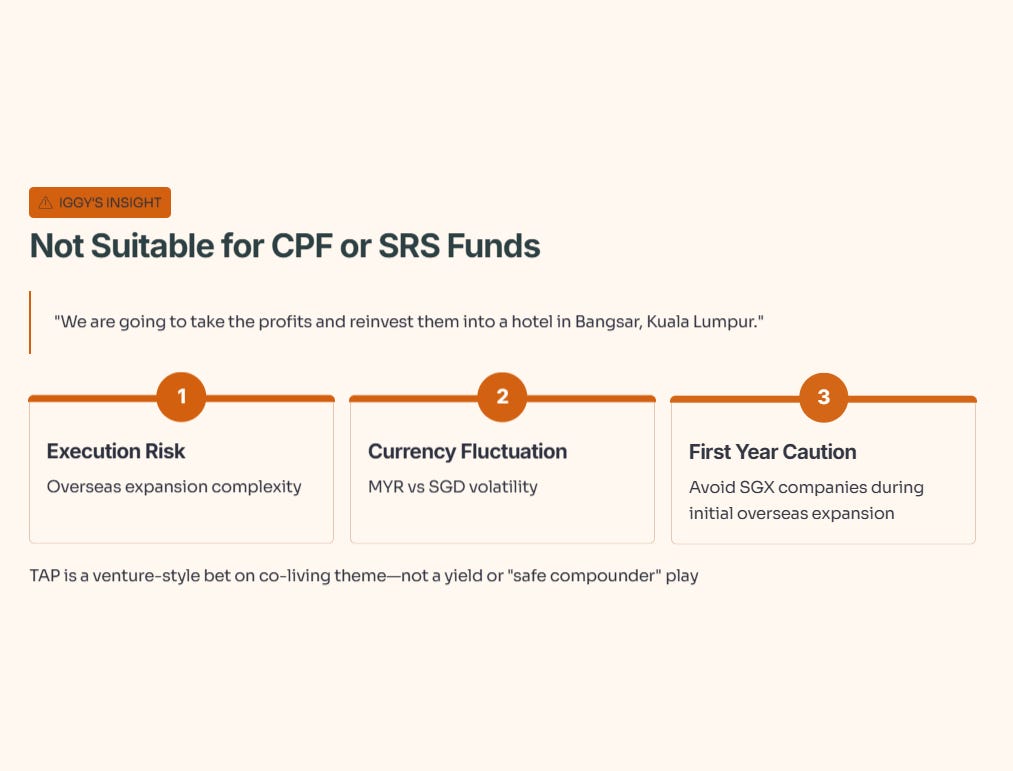

The Assembly Place, in its preliminary prospectus, stated it does not have a fixed dividend policy.

They intend to use proceeds for “expansion into Malaysia” and “sourcing new property assets.” This is classic growth-stage behavior. They are telling you upfront: “We are going to take the profits and reinvest them into a hotel in Bangsar, Kuala Lumpur.”

Iggy’s Insight:

If you are using CPF or SRS funds, you generally want yield or “safe compounders.” TAP is neither right now. It is a venture-style bet on the co-living theme. Investing in a company expanding into Malaysian hospitality carries execution risk—currency fluctuation (MYR vs SGD) and operational complexity. I generally avoid SGX companies during their first year of overseas expansion.

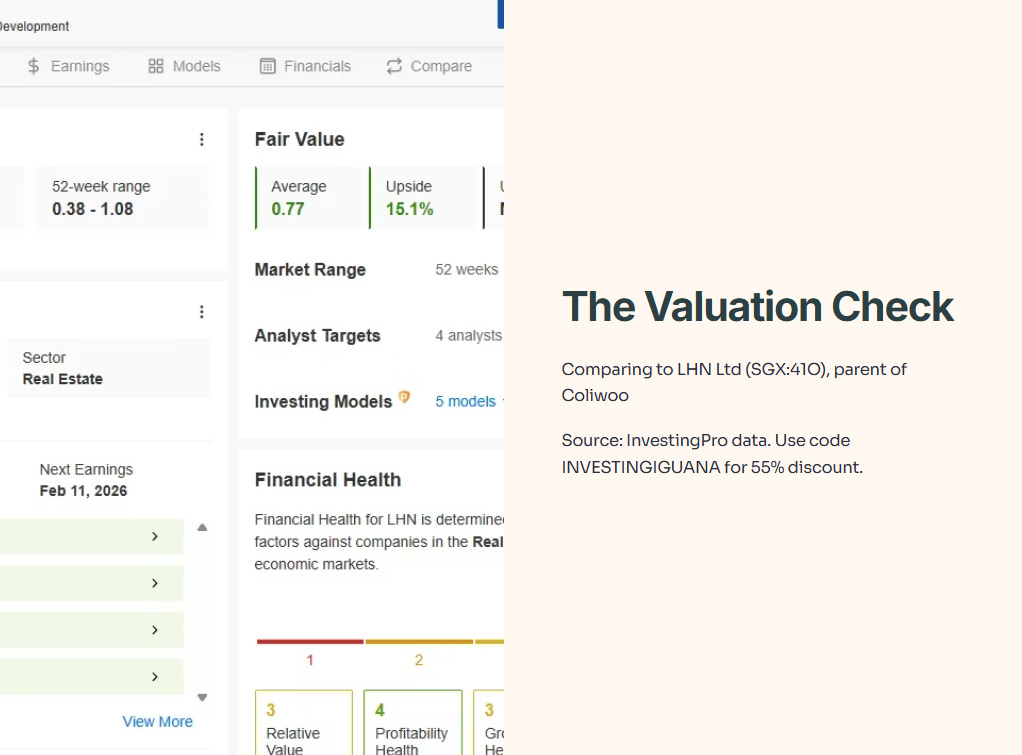

3. The Valuation Check

How much should you pay for this?

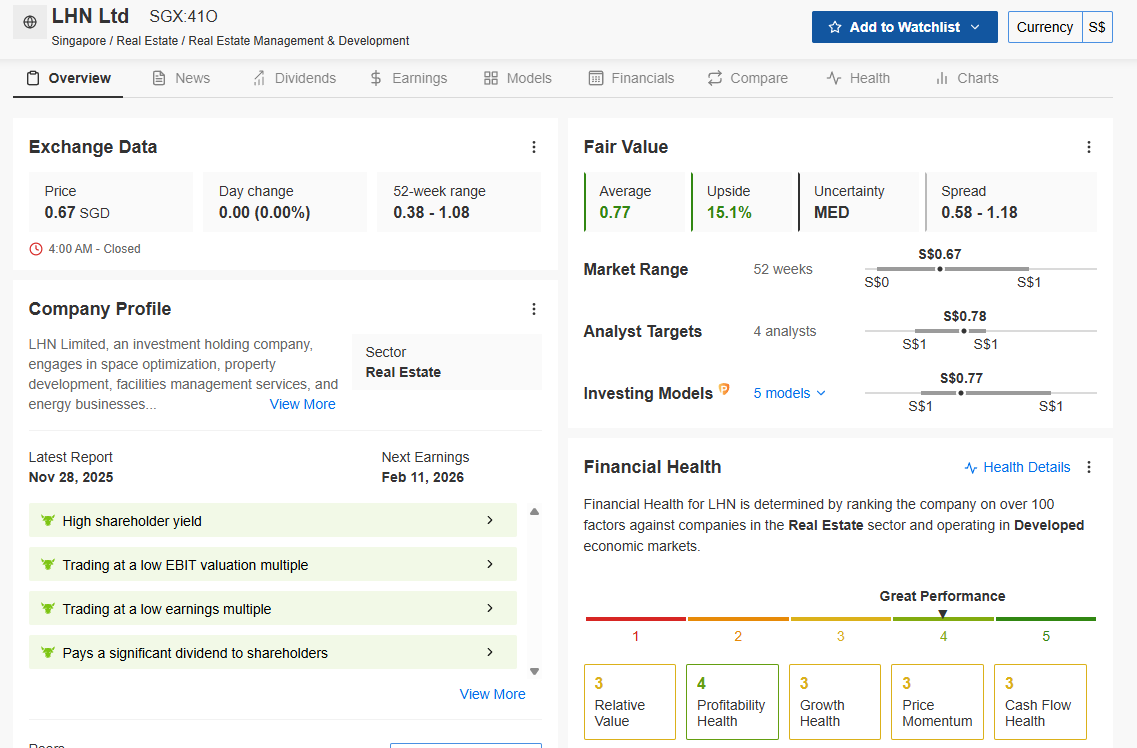

I don’t just guess at valuations. I check the institutional models. Let’s look at LHN Ltd (SGX:41O), the parent of Coliwoo, to see what a “healthy” co-living business looks like right now.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Look at the hard numbers for LHN (the benchmark) above:

Valuation Gap: LHN is trading at S$0.67, but the institutional models peg the Fair Value at S$0.77. That is a 15.1% Upside buffer.

Quality Check: Notice the Financial Health Score of 4 out of 5 (Great Performance). This score is driven by high profitability health and cash flow.

The Income Reality: Look at the green “ProTips” on the left. It explicitly highlights: “Pays a significant dividend to shareholders.”

Iggy’s Insight:

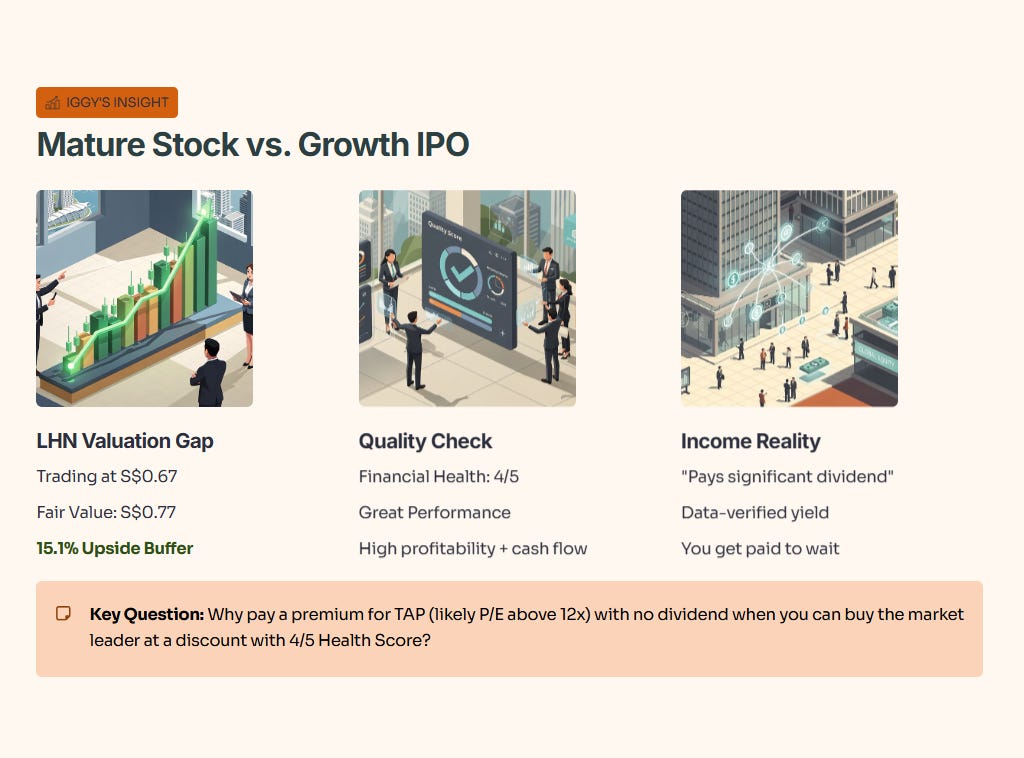

This is the difference between a “Mature” stock and a “Growth” IPO.

With LHN (Coliwoo), the models confirm you are buying an undervalued asset (trading below S$0.77) that pays you to wait. With TAP, you will likely be paying a premium for future growth that hasn’t happened yet.

If TAP lists with a P/E above 12x, ask yourself: Why pay a premium for a company with no dividend policy when you can buy the market leader at a discount with a 4/5 Health Score?

The Investor’s Action Plan

So, what do we do with the Assembly Place IPO?