The $3,500 Deductible: Why I’m Downgrading My Shield Plan

The MOH just closed the loophole in your insurance rider. Here’s what changes April 1, 2026—and why “downgrading” might be the smartest trade of the decade.

The End of the “Free Lunch”

If you’ve been following the Singaporean market for the last decade, you know there was a beautiful arbitrage opportunity in the private health insurance world. You could buy a rider—a fancy insurance add-on—that covered everything. Your deductible? Paid. Your co-payment? Paid. You could walk into Mount Elizabeth, order the lobster bisque, and feel bulletproof.

In This Article:

• The Deep Data: What Just Died?

• The Math: What This Actually Costs You

• The “InvestingPro” Reality Check: The Healthcare Sector

• The “Self-Insure” Strategy: The Calculation That Actually Works

• The Actionable Conclusion: Your Playbook

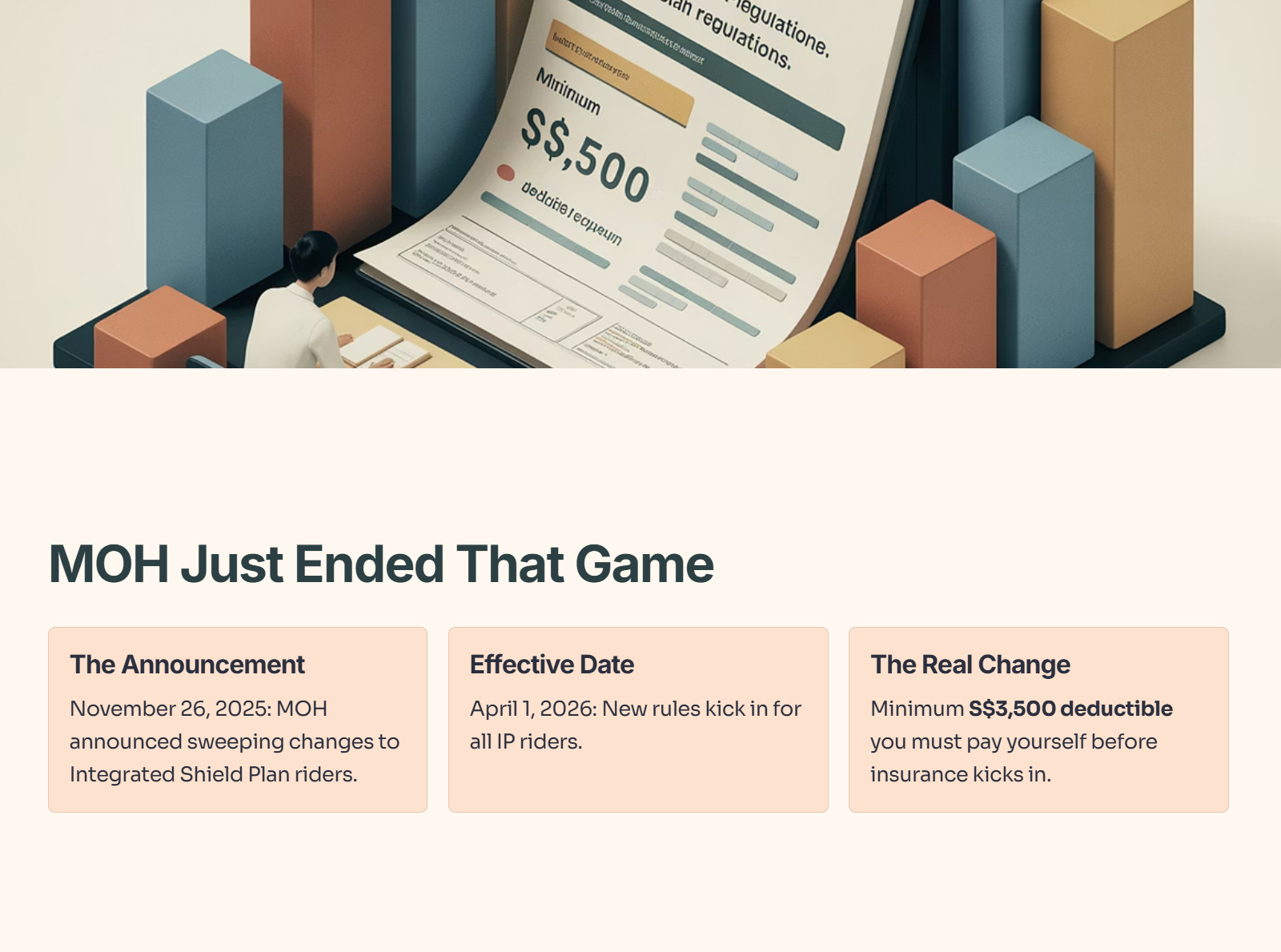

The Ministry of Health (MOH) just ended that game.

On November 26, 2025, the MOH announced sweeping changes to Integrated Shield Plan (IP) riders, effective April 1, 2026. The headlines are screaming that riders will be “30% cheaper.” That is technically true, but it is a surface-level analysis.

What they actually did was force investors back into having “skin in the game”—specifically, a minimum S$3,500 deductible you have to swallow yourself before the insurance kicks in.

Iggy’s Insight:

This isn’t just a policy tweak; it’s a regime change. For years, we paid premiums for “peace of mind.” Now, that peace of mind has a literal price tag: S$3,500 per admission. But here is the contrarian view: This is actually a massive opportunity to optimize your cash flow. Most of you are over-insured and under-invested. This forces a correction.

Let me break down the new rules, show you the math, and walk you through a “Self-Insurance” strategy that could save you thousands over the next decade.

The Deep Data: What Just Died?

Starting April 1, 2026, IP riders are not allowed to cover the minimum MOH deductible. That is the pivot point.

The Old Regime vs. The New Regime

Why did MOH do this? They are killing the “Buffet Syndrome.” When insurance covers the first dollar, patients don’t ask about costs. The data confirms this: patients with full riders claimed 1.4x more often and had bills 1.4x larger than those without.

Iggy’s Take:

The system was eating itself. Premiums were spiraling because there was zero friction between the patient and the bill. By introducing a S$3,500 barrier to entry, MOH is introducing a “price signal.” Markets only work when price signals exist. This restores the feedback loop.

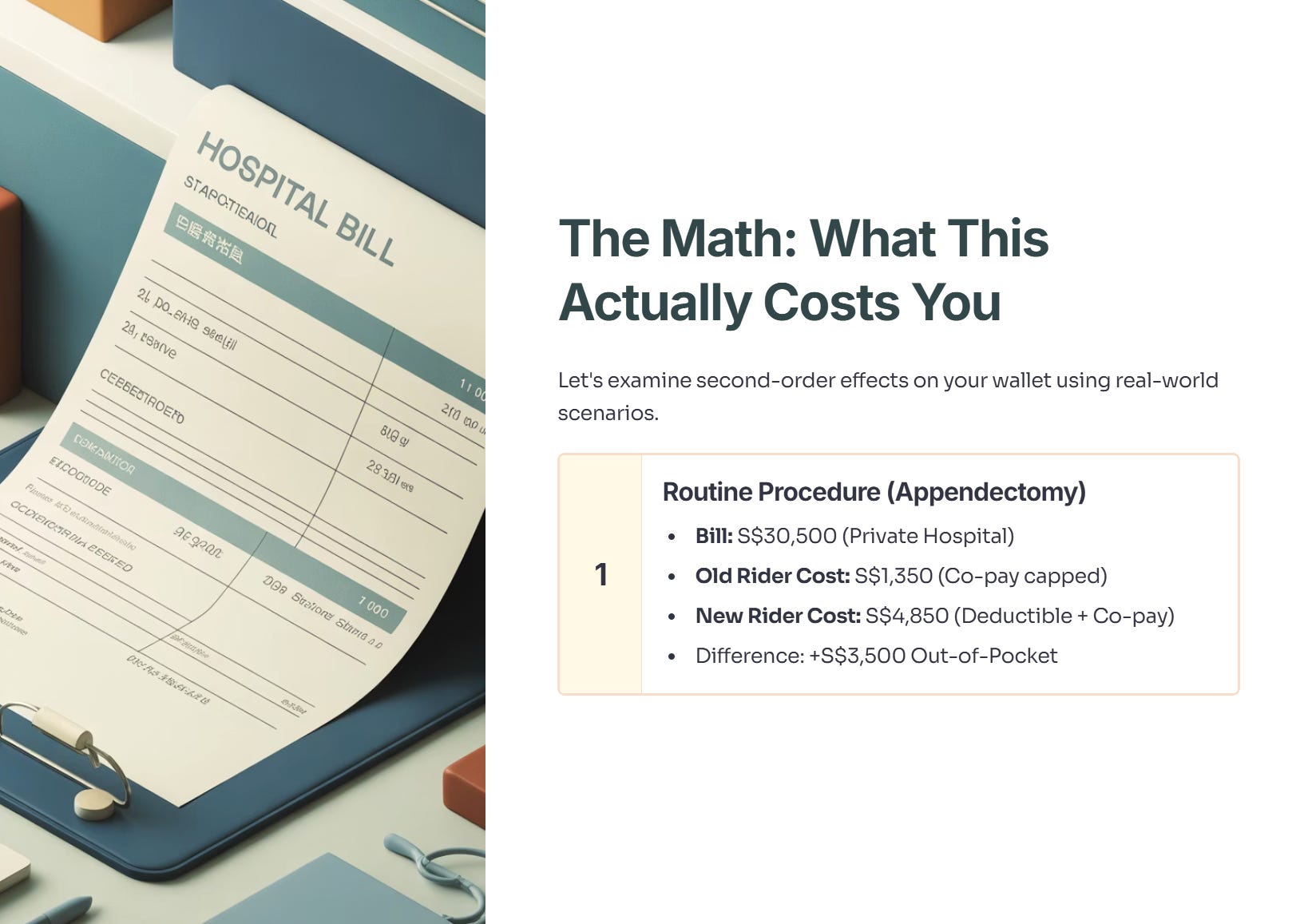

The Math: What This Actually Costs You

Let’s look at the “Second-Order Effects” on your wallet using real-world scenarios.

Scenario 1: The Routine Procedure (e.g., Appendectomy)

Old Rider Cost: S$1,525

New Rider Cost: S$4,850

Difference: +S$3,325 (approx. S$3.3k)

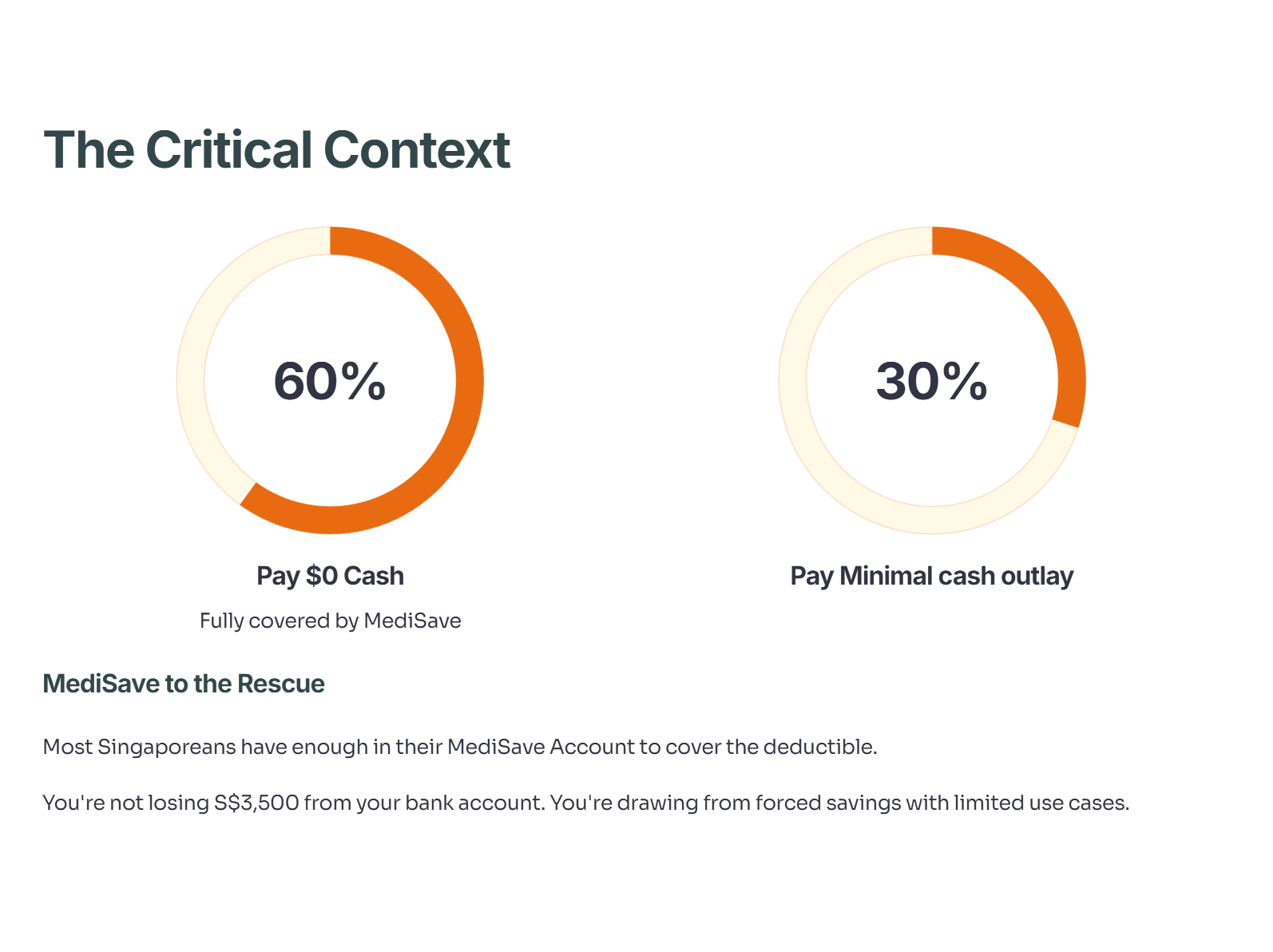

The Critical Context:

While a S$3,500 jump sounds scary, remember MediSave. Most Singaporean investors have enough in their MediSave Account (MA) to cover the deductible.

60% of claimants will pay $0 cash (fully covered by MediSave).

30% of claimants will pay <S$1,000 cash.

You are not losing S$3,500 from your bank account; you are drawing it from a forced savings account (CPF) that has limited use cases anyway.

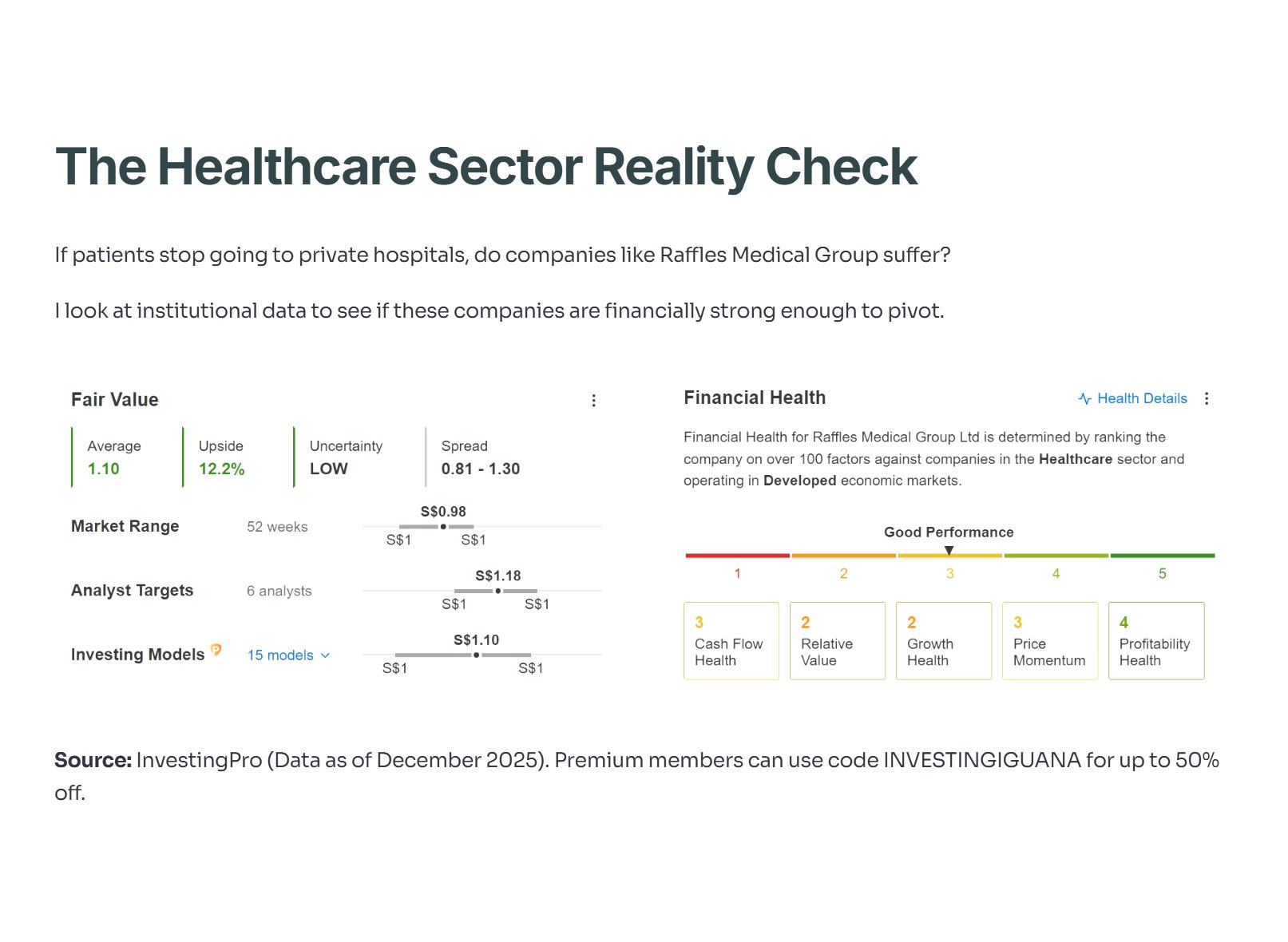

The “InvestingPro” Reality Check: The Healthcare Sector

We know this policy helps the system, but what about the providers? If patients stop going to private hospitals because of the deductible, do companies like Raffles Medical Group or the insurers themselves suffer?

We know this policy hurts your wallet in the short term. But does it hurt the hospitals? If patients stop going to private hospitals because of the S$3,500 barrier, stocks like Raffles Medical Group could crash.

I checked the data to see if this is a ‘Sell’ signal.

Source: InvestingPro by Investing.com (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Analysis:

The InvestingPro Health Score likely indicates that top-tier healthcare providers maintain strong balance sheets (often a score of 3 or 4 out of 5) despite regulatory headwinds. While the “buffet” is over, the demand for quality healthcare is inelastic. If the Fair Value indicates upside, the market may have overreacted to the fear of dropped patient numbers, creating a buying opportunity for the stock while you save money on your insurance.