The Chicken Rice Audit: Is a Business Class Seat Worth 450 Plates of Chicken Rice?

"Uncle, one plate S$5 already!" Why let the bank take 450 plates from your pocket for a "free" flight?

The tension in a Singaporean heartland usually begins at the stomach. Specifically, it begins at the hawker centre where the price of a standard plate of chicken rice has quietly crept from S$3.50 to S$5.00 in what feels like a blink. This is a physical tension every resident understands. It is the steady, silent erosion of purchasing power. When we talk about “8 miles per dollar” (8 mpd) from the HSBC Everyday Global Account (EGA), we aren’t just talking about a bank promotion. We are talking about a mathematical trade-off. We are asking if a seat at the pointy end of the plane is worth the literal sacrifice of 450 plates of chicken rice per year.

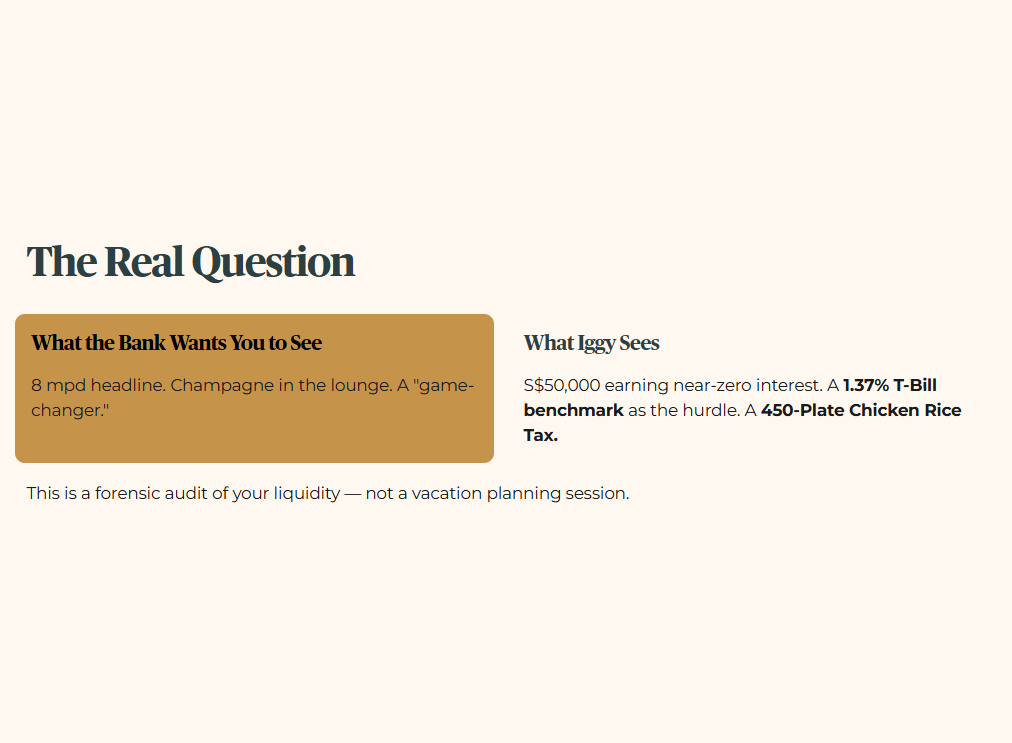

As of March 2026, our community of Iggy’s Elite Investors has grown increasingly skeptical of “engineered” travel yields. The banks want you to see the 8 mpd; they want you to visualize the champagne in the lounge. My job is to make you look at the S$50,000 sitting in an account earning almost zero interest while the current 1.37% Iggy T-Bill benchmark stands as the hurdle. This isn’t a “game-changer”—it is a 450-Plate Chicken Rice Tax. We are conducting a forensic audit of your liquidity, not a vacation planning session.

🦎 Iggy’s Insight

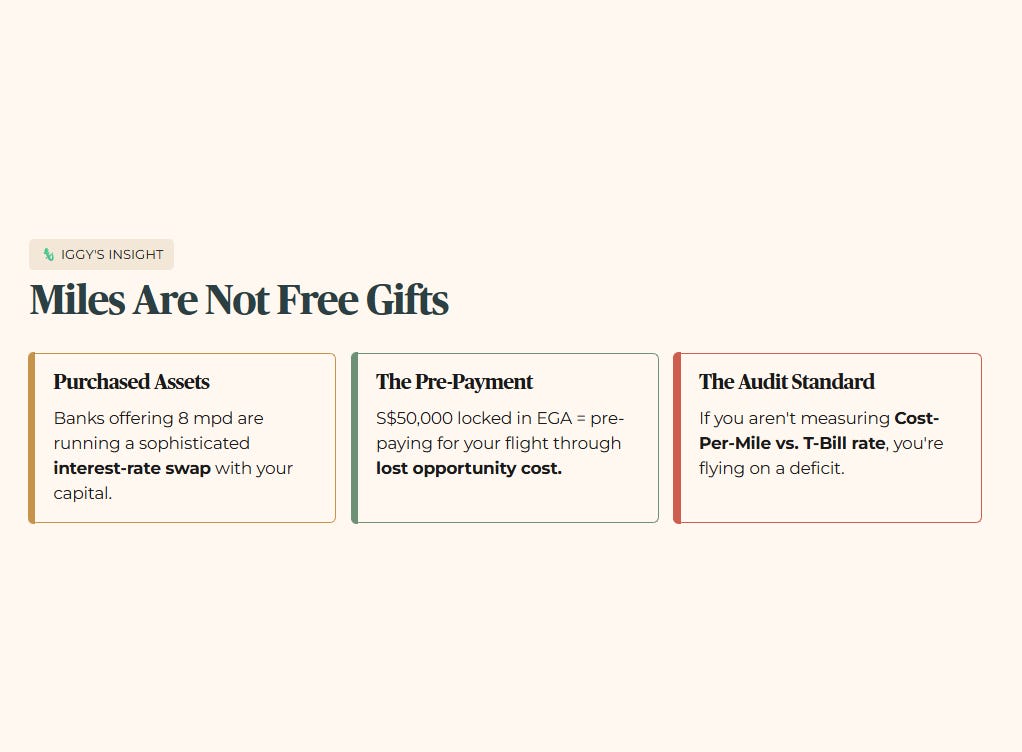

Most Singaporean residents leave thousands of dollars on the table because they treat credit card miles as “free gifts” rather than “purchased assets.” When a bank offers you an outsized earn rate like 8 mpd, they aren’t being generous; they are conducting a sophisticated interest-rate swap with your capital.

By locking up S$50,000 in an Everyday Global Account (EGA) to unlock that tier, you are essentially pre-paying for your flight through lost opportunity costs. If you aren’t auditing the “Cost-Per-Mile” against the risk-free rate of a T-Bill, you are flying on a deficit. This is the difference between a retail “player” and a forensic investor.

In This Article:

The Fixed-Cost Audit

Fixed-Cost Arbitrage Table

Interpretation

The Changi Advantage

The Elite Take

Note on the Stress-Test Buffer

The Heartland Verdict

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite Investors

A Quick Note Before the Verdict. You aren’t here for the kopi tips or the hype. You’re here because you want the forensic truth before you commit a single dollar of your capital. That tells me something about the kind of investor you are.

But here’s the uncomfortable truth about how independent publishing works. The algorithm doesn’t know you read every word. It doesn’t know you checked the gearing ratio twice. It only sees one signal — whether you’ve hit that subscribe button. Every forensic investor who reads without subscribing is invisible to the machine.

If this analysis has ever helped you identify a risk or calculate a margin of safety — subscribe for free now and share this with one person who needs to hear it. Not for me. To tell the algorithm that data-driven SGX analysis deserves a seat at the table alongside the noise.

The Fixed-Cost Audit (The Hard Math)

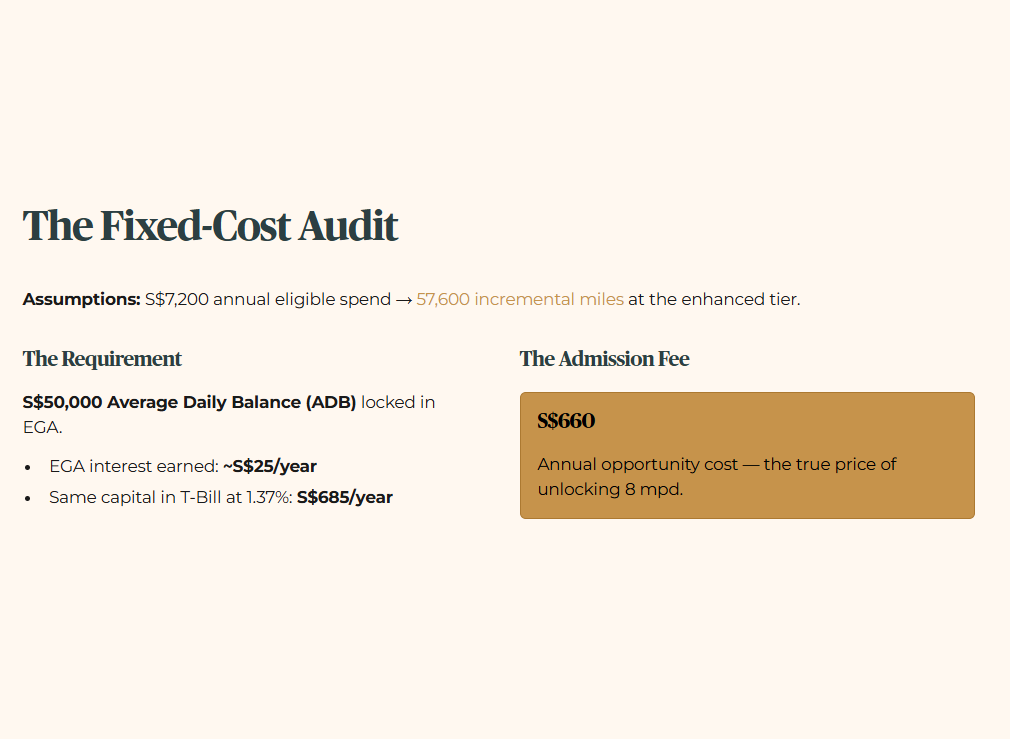

This analysis assumes S$7,200 in annual eligible spend (S$600/month), which yields 57,600 incremental miles at the enhanced tier.

To understand the HSBC EGA “Enhanced” 8-MPD Tier, we must look past the marketing fluff and apply the Double-Entry Rule: every mile earned has a cost. For the 50+ demographic in Singapore, capital preservation and yield are the “Fortress” pillars.

The requirement for this 8-mpd tier is a S$50,000 Average Daily Balance (ADB). If that money sits in the EGA, it earns a nominal interest rate that is functionally zero—roughly S$25 per year. However, if that same S$50,000 were placed in the latest MAS T-Bill auction at 1.37%, it would generate S$685 per year. The difference—S$660—is what I call the Admission Fee (the opportunity cost of locking up liquidity).

Fixed-Cost Arbitrage Table

Interpretation

By choosing the EGA tier, you are effectively buying 57,600 incremental miles for S$660, which results in a Cost-Per-Mile (CPM) of 1.14 cents.

In my framework, the 1.5 CPM Floor is the absolute limit. If the cost to “manufacture” a mile exceeds 1.5 cents, the strategy is a Yield Trap and you should pivot to cashback. While 1.14 cents is technically below the floor, it leaves a razor-thin margin for error.

If Singapore Airlines devalues the KrisFlyer program by 15%—which they have done historically—your 1.14 cent cost suddenly balloons, and you are left holding an asset that has depreciated before you even step onto the tarmac.

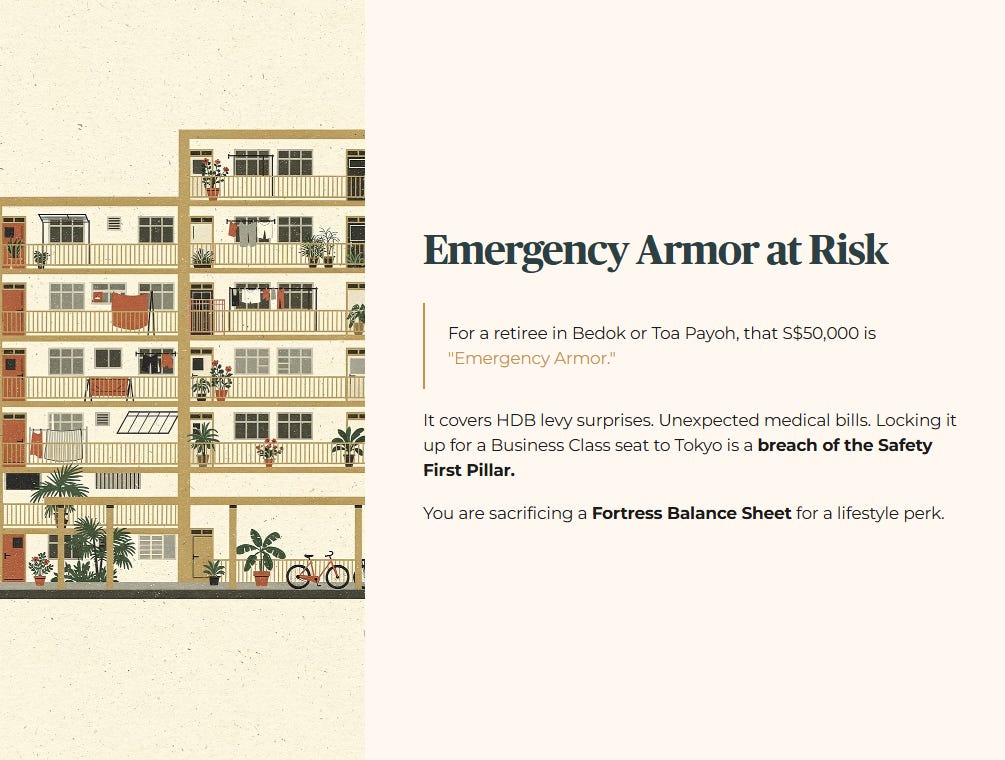

And let’s be honest, the banks want you to think this card is a gem. But here is the uncomfortable truth: for a retiree living in Bedok or Toa Payoh, that S$50,000 is “Emergency Armor.” It is the money that covers a sudden HDB lift upgrade levy or an unexpected medical bill. Locking it into a low-yield environment for the sake of a Business Class seat to Tokyo is a breach of the “Safety First” Pillar. You are sacrificing a Fortress Balance Sheet for a lifestyle perk.

Cliffhanger (one sentence): While the 8 mpd headline wins on paper, the “Changi Advantage” audit exposes the single friction point that quietly turns this into a retiree-unfriendly miles trap—and it starts before you even reach T3.