Is the $1,500 Budget 2026 Top-Up Enough for Your Retirement? (Data Review)

Decoding the Budget 2026 “Liquidity Lock,” the Means-Testing Trap, and the Forensic Math of a 4% Yield vs. Zero Cash-Flow.

The headlines are buzzing with festive energy: “Singaporeans to receive up to $1,500 in CPF top-ups!” On the surface, it’s a classic Budget 2026 win for the “sandwich generation” and seniors. But for the Elite 170, we don’t read the headlines; we audit the plumbing.

When you peel back the layers of this “gift,” you find a highly surgical policy designed not for the masses, but for a very specific subset of the population. If you’ve spent your life building your Iron Bastion and hitting your Full Retirement Sum (FRS), this article is your reality check. The government isn’t just giving away money—it’s buying a long-dated, zero-liquidity liability.

In This Article:

Part 1: The Health Check – The “Invisible” Exclusion List

Part 2: The Wealth Check – The Liquidity vs. Yield Trade-Off

Part 3: The Strategic Pivot – Budget 2026 vs. The 2028 Vision

Iggy's Verdict

About Iggy & the Elite 170

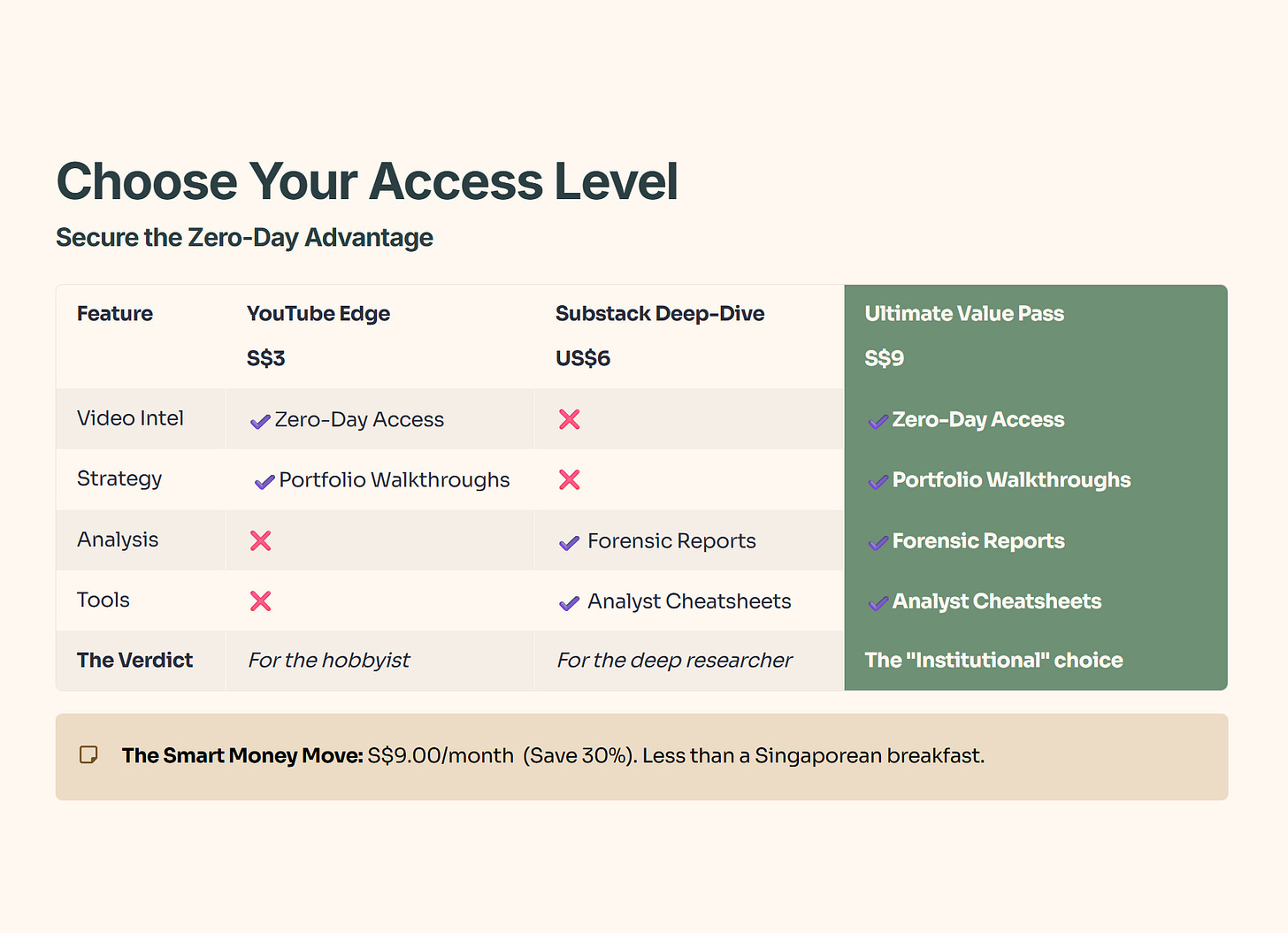

🦎 Join the Inner Circle: Optimize Your Informational Latency: In the Singapore market, the gap between a calculated entry and becoming a liquidity provider for others is often just 48 hours. While 5,800+ readers wait two weeks for the “Old News” version, my Inner Circle observes the data while the market structure is still evolving.

🚨 Mitigate Informational Lag: Free subscribers wait 14 days to see my analysis. In this jungle, informational asymmetry is a primary driver of portfolio variance. Access the data while the market dynamics are still being priced in.

Choose Your Edge:

⚡ Zero-Day Access: Observe every deep-dive video the second it’s rendered. No delays, no missed data points.

📂 The Forensic Vault: Access the full forensic reports and portfolio walkthroughs where I strip away the corporate hype to reveal the hard math behind every Singapore blue chip.

💎 The “Smart Money” Bundle: Secure the full S$9/mo Pass (YouTube + Substack).

It’s a nominal overhead—less than the cost of two coffees at Toast Box—to analyze the market with the same datasets as institutional participants.

Get the data while it’s fresh. 👉 Join the Inner Circle Here

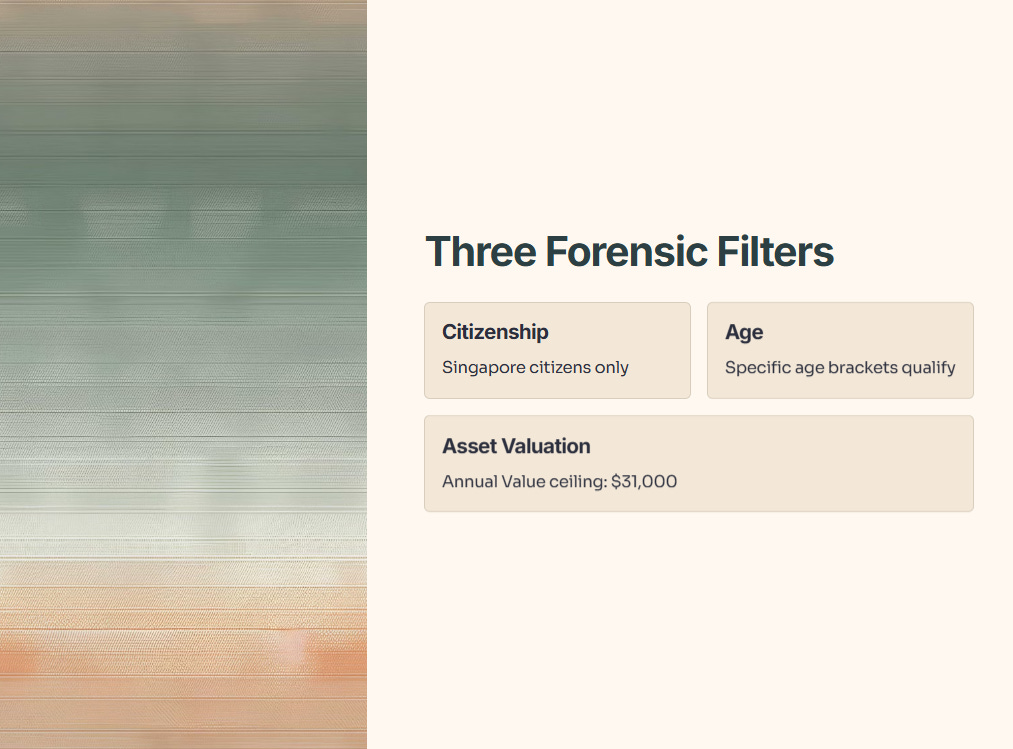

🛡️ Part 1: The Health Check – The “Invisible” Exclusion List

Before we look at the compounding math, we must look at the gatekeepers. The Budget 2026 top-up is governed by three primary “Forensic Filters”: Citizenship, Age, and Asset Valuation.

The most brutal filter is the Annual Value (AV) of your home. Set at a ceiling of $31,000, this metric is designed to decouple “asset-rich” Singaporeans from state support. While almost every HDB dweller in Woodlands or Jurong will pass the $21,000 baseline, those who have “upgraded” to modest private properties—think a city-fringe studio or an older terrace house—may find themselves forensically disqualified despite having identical cash-flow struggles.

🎓 Educational Note: The AV Filter

The Annual Value (AV) is the estimated yearly rent your property could fetch. It is the state’s primary proxy for wealth. In 2026, an AV of $31,000 is the “Hard Border.” If your roof is worth more than this on the rental market, the government assumes you have the means to fund your own retirement.

💰 Part 2: The Wealth Check – The Liquidity vs. Yield Trade-Off

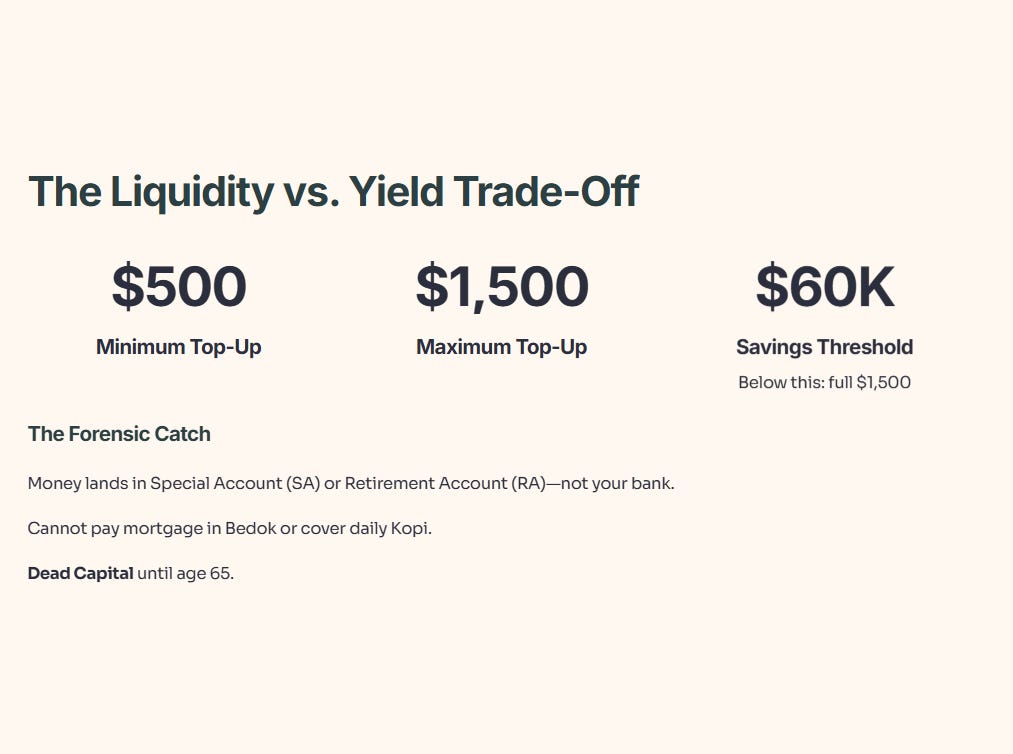

Let’s talk about the money itself. The top-up is tiered, ranging from $500 to $1,500. For those with less than $60,000 in retirement savings, the full $1,500 is a significant 2.5% boost to their floor. But here is the forensic catch: The money lands in your Special Account (SA) or Retirement Account (RA).

By funneling this “bonus” into the 4% interest accounts rather than your Ordinary Account (OA) or your bank account, the state is performing a Liquidity Lock. You cannot use this money to pay down your mortgage in Bedok or to cover your daily Kopi. It is “Dead Capital” that only resurrects as a monthly payout when you turn 65.

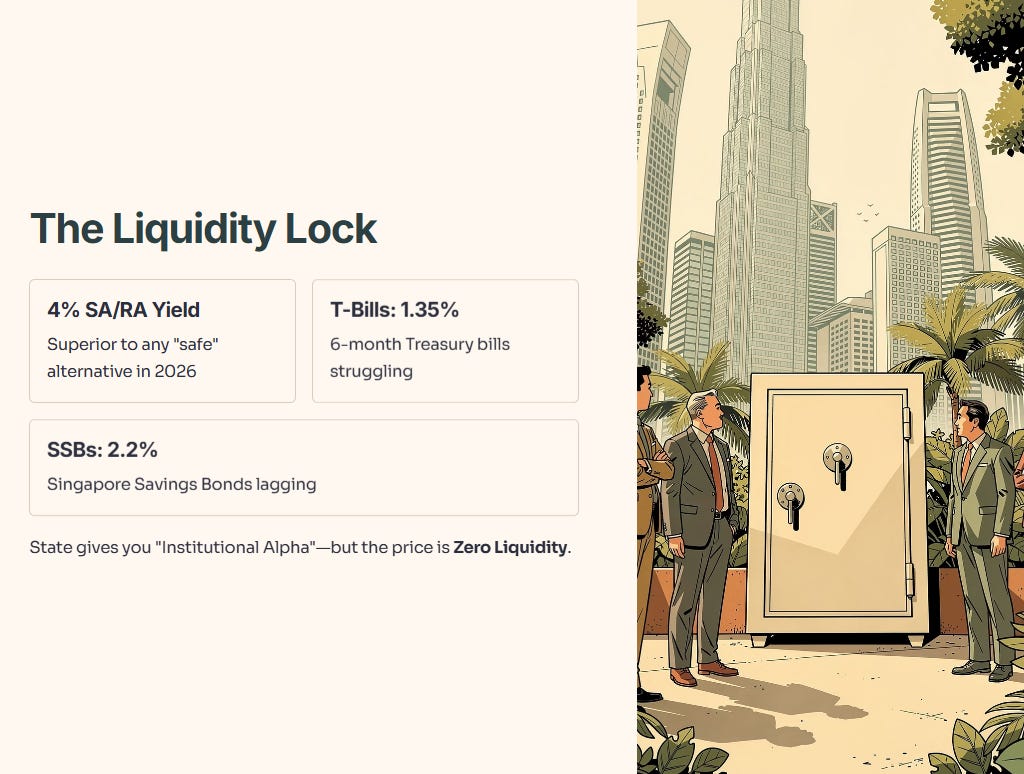

Mathematically, the 4% yield is superior to any “safe” alternative in 2026. With 6-month T-bills yielding a measly 1.35% and SSBs struggling at 2.2%, the state is essentially giving you “Institutional Alpha.” But the price of that Alpha is Zero Liquidity.

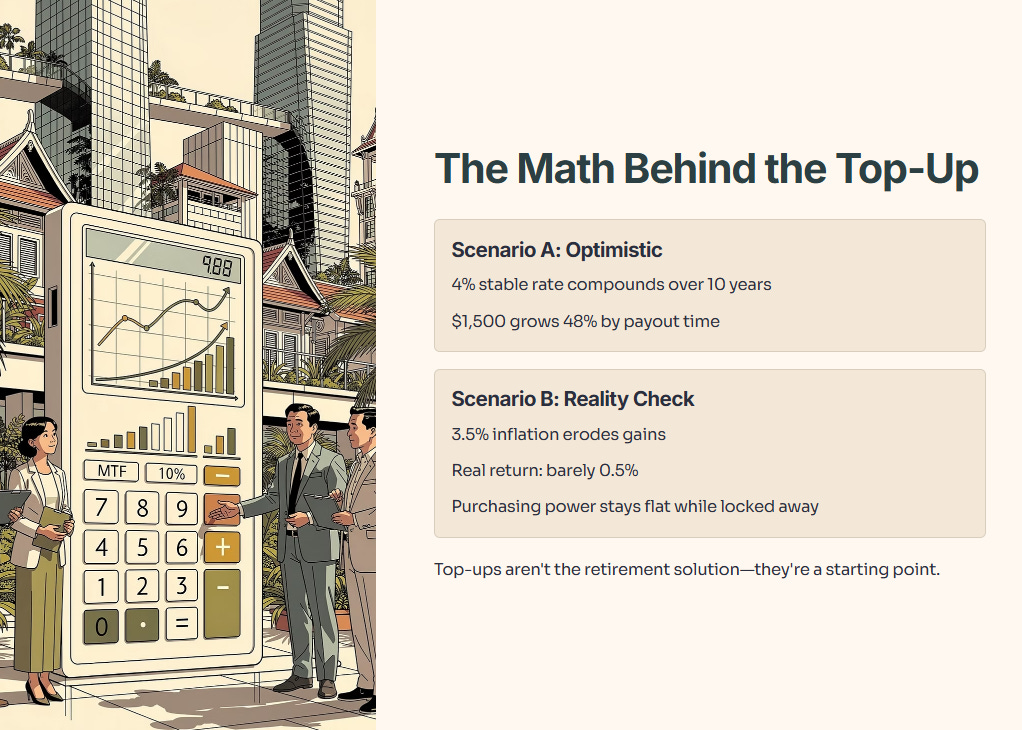

So what does that actually mean in cold hard numbers? Let's run the forensic math.

Let’s run the forensic math. Two scenarios.

Scenario A (The Bull Case): The 4% interest rate holds steady for the next ten years. If you are 55 today, that $1,500 compounds to roughly $2,220 by the time your payouts kick in — a 48% gain on paper. Sounds good, right?

Scenario B (The Inflation Trap): Inflation stays sticky at 3.5%. Your real return collapses to a measly 0.5%. Your purchasing power has gone nowhere — except your money was locked in a vault you couldn’t touch for a decade.

This is the part the headlines skip. The 4% yield is the nominal headline number. The real return — the one that actually buys your Kopi and covers your medical bills — is razor-thin the moment inflation shows up. Before we celebrate this top-up as a retirement solution, the Elite 170 needs to audit the real number, not the marketing number.

Next, I’ll show you the exact forensic checklist I use to separate “headline yield” from “real compounding” — and the specific metrics that decide whether a bank stock or REIT is a fortress or a liability.