The Great 2026 Rotation: 7 Themes That Will Define Your Portfolio

The era of “easy cash” is over. As the Fed pivots, the smart money is moving from Fixed Deposits to forgotten yield plays. Here is the roadmap.

Happy New Year. It is January 1, 2026.

For the last two years, you didn’t have to be a genius to make money. You just had to put your cash in a Fixed Deposit or T-Bill and collect 3.5% to 4% risk-free. But the wind has changed direction. The headlines on my terminal this morning are clear: The game has changed.

While the crowd is celebrating the “soft landing,” I am looking at the cracks in the foundation—specifically in Hong Kong commercial real estate and how it threatens one of our local banking giants.

Iggy’s Insight:

The most dangerous phrase in investing right now is “set and forget.” The strategy that worked in 2024 and 2025—hoarding cash and buying banks—is likely the wrong playbook for 2026. We are entering a cycle of yield compression. If you wait for the headlines to confirm it, you have already missed the move.

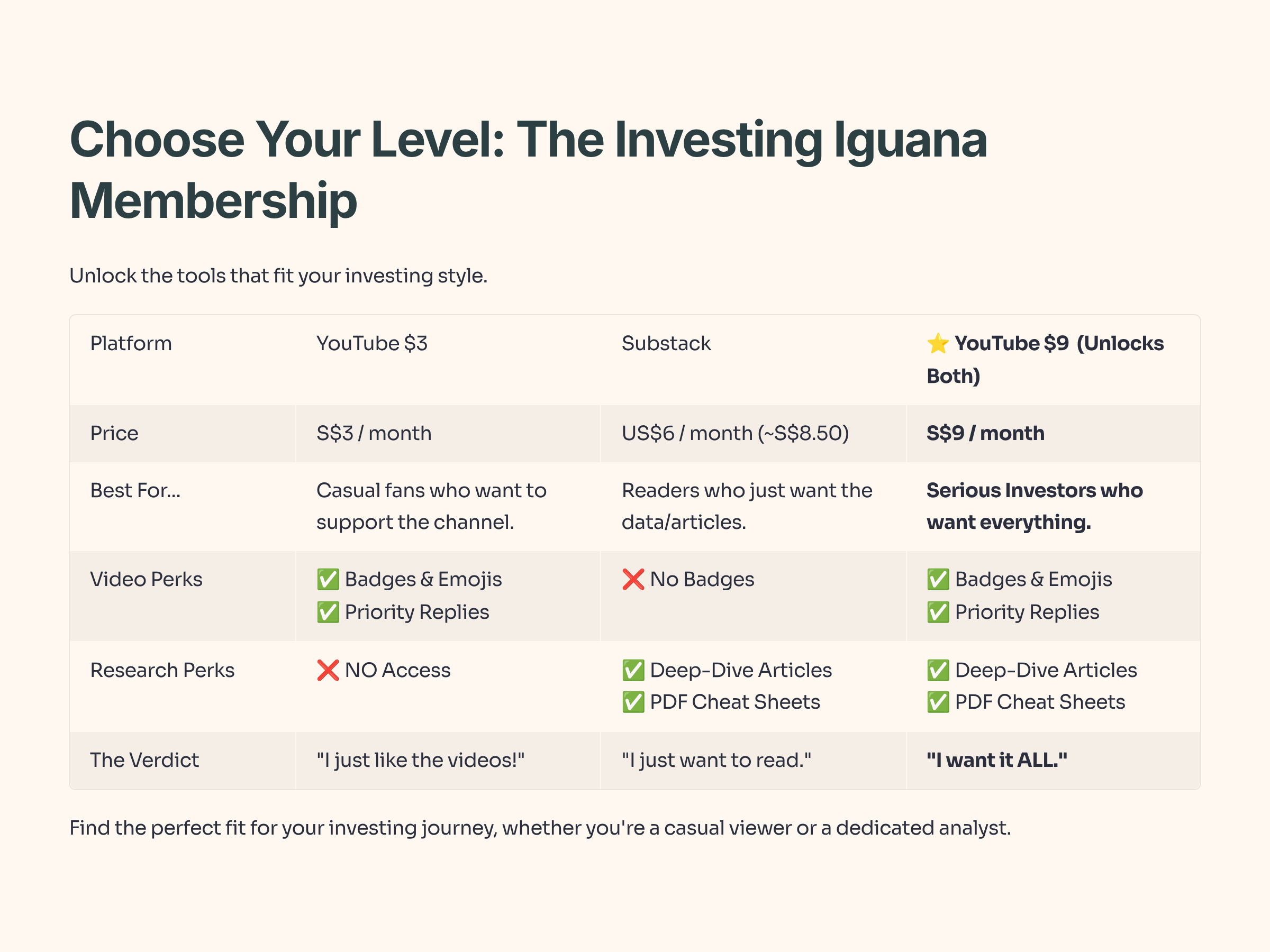

If you’re new here, welcome. I’m Iggy, your Singapore-based Private Investor and Market Researcher. Since October 2025, we’ve built a community of over 5,300 investors and produced over 1,300 videos and 400 articles. We are home to a growing ‘Inner Circle’ of over 100 paid members across YouTube and Substack.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

In This Article:

• Theme 1: The Macro Pivot (Fed Blinked)

• Theme 2: The Lion City Roars (GDP Upgrade)

• Theme 3: The REIT Renaissance

• Theme 4: The Banking Divergence (Dividends vs. Growth)

• Theme 5: The “Green” Alpha (Sembcorp)

• Theme 6: The New Engine (Manufacturing & AI)

• Theme 7: The “Elephants in the Room” (Risks & Portfolio Triage)

• The Investor’s Action Plan: Q1 2026

• InvestingPro Reality Check

• Iggy's Verdict / Conclusion

Theme 1: The Macro Pivot (Fed Blinked)

The data is definitive. After a prolonged battle with inflation, the Federal Reserve is shifting gears. Economist Mark Zandi sees the Fed surprising markets with three rate cuts in the first half of 2026 alone.

Why does this matter for your CPF and SRS portfolio? Because Singapore imports its interest rate policy. As US rates fall, the SORA (Singapore Overnight Rate Average) will collapse. The 3.8% yield you enjoyed on your idle cash is about to evaporate. Analysts expect the 2-year US Treasury yield to trade in the 3.45%–3.65% range in 1H 2026, forcing a downward re-pricing of risk-free assets.

Iggy’s Insight:

Don’t be fooled by the current T-Bill rates; they are a lagging indicator. The forward markets are already pricing in a drop. If you are sitting on cash waiting for “one last hike,” you are fighting the Fed. The smart play is to lock in yields on longer-duration assets (like REITs or bonds) before the SORA crash hits your bank account.

Theme 2: The Lion City Roars (GDP Upgrade)

Simultaneously, the Ministry of Trade and Industry (MTI) has upgraded Singapore’s 2025 growth to roughly 4.0% and forecasts a steady 1.0% to 3.0% for 2026. This is being dubbed “Singapore’s $133B Manufacturing Miracle,” driven by a massive surge in electronics and biomedical manufacturing.

This isn’t just a number on a spreadsheet; it represents a fundamental shift. We are moving from a “slow growth, high inflation” environment to a “moderate growth, falling inflation” environment—the “Goldilocks” scenario for equities.

Iggy’s Insight:

Note where the growth is coming from. It’s not retail sales; it’s high-value manufacturing and electronics (up 6.1% in Q3 2025). This tells me the “trade recovery” plays (like logistics and industrial stocks) will see earnings upgrades first. Avoid generic “Singapore Inc” ETFs and target the sectors actually driving this GDP beat.

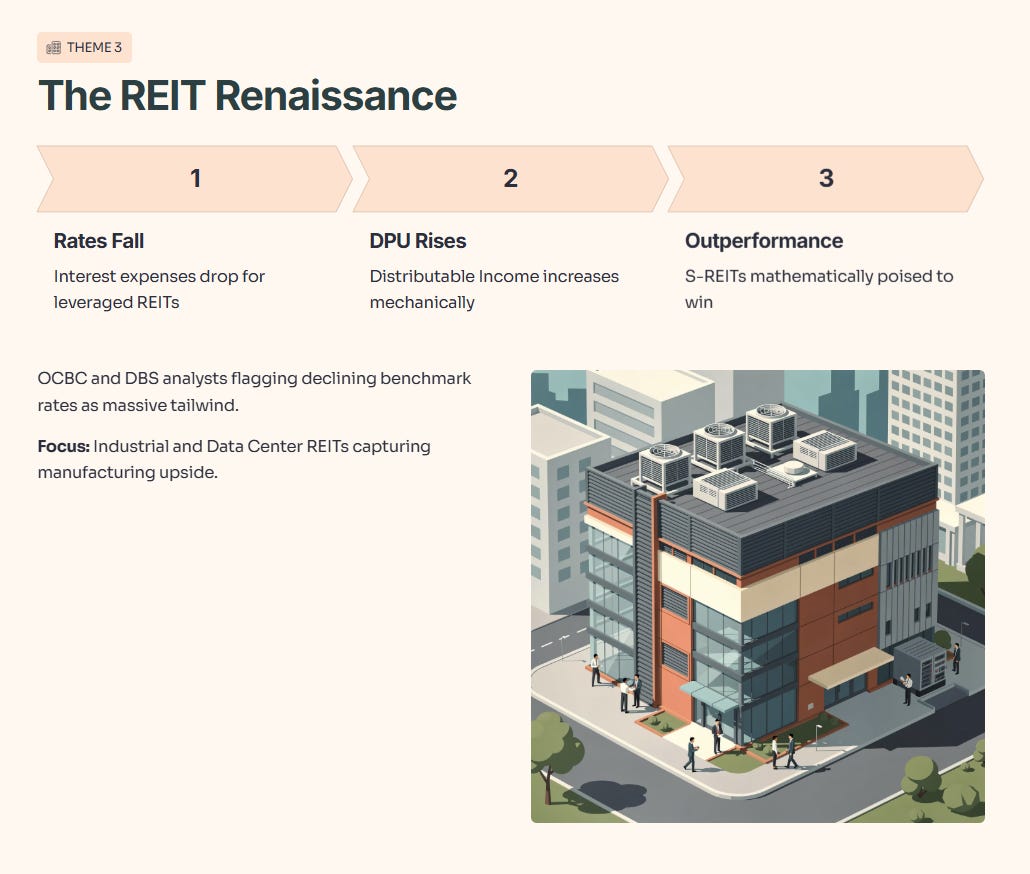

Theme 3: The REIT Renaissance

If rates fall and GDP rises, S-REITs are mathematically poised to outperform.

The logic is mechanical: REITs are leveraged vehicles. Their biggest expense is the cost of debt. As interest rates fall in 2026, their interest expenses drop, and their Distributable Income (DPU) rises.

Analysts from OCBC and DBS are already flagging this, noting that declining benchmark rates act as a massive tailwind for the sector. We are looking specifically at Industrial and Data Center REITs that can capture the manufacturing upside.

Iggy’s Insight:

The market is inefficient. It is currently pricing REITs based on yesterday’s interest rates. The InvestingPro Fair Value models suggest a 15-20% upside for blue-chip REITs. The time to buy these is before the first Fed cut is officially announced, not after.

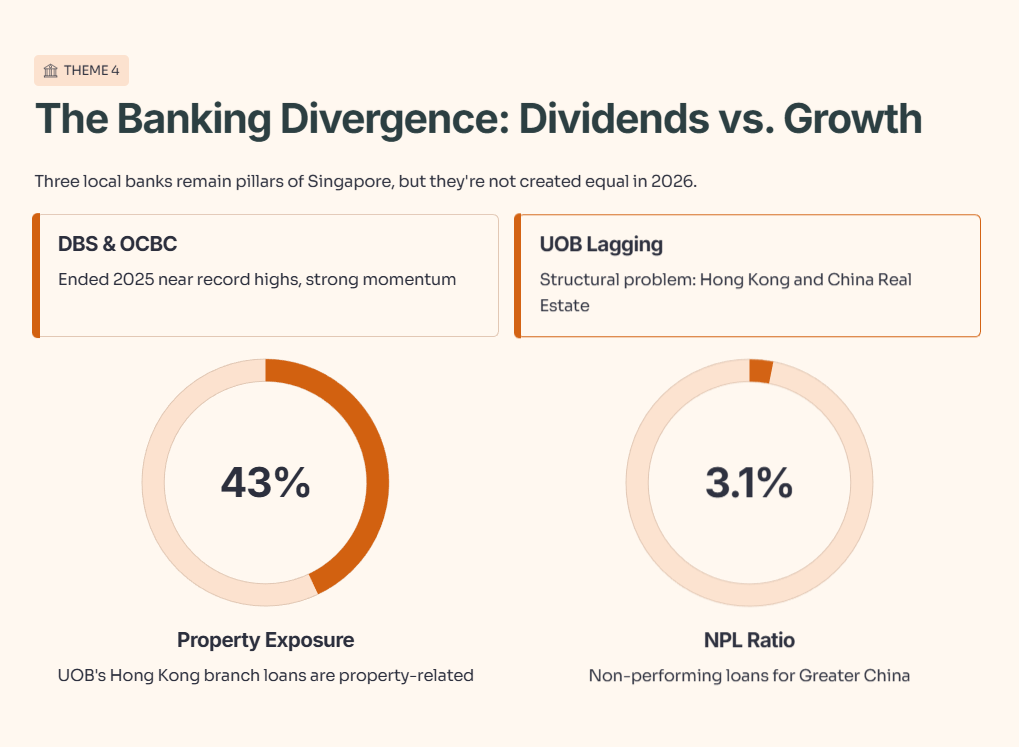

Theme 4: The Banking Divergence (Dividends vs. Growth)

For years, I have told you that the three local banks are the pillars of Singapore. That remains true, but they are not created equal in 2026.

While DBS and OCBC ended 2025 near record highs, UOB is lagging significantly. The structural problem is Hong Kong and China Real Estate.

The “Kitchen Sink”: UOB booked massive provisions for commercial real estate risks in late 2025.

The Exposure: A staggering 43% of UOB’s Hong Kong branch loans are property-related, with a non-performing loan (NPL) ratio for Greater China hitting 3.1%.

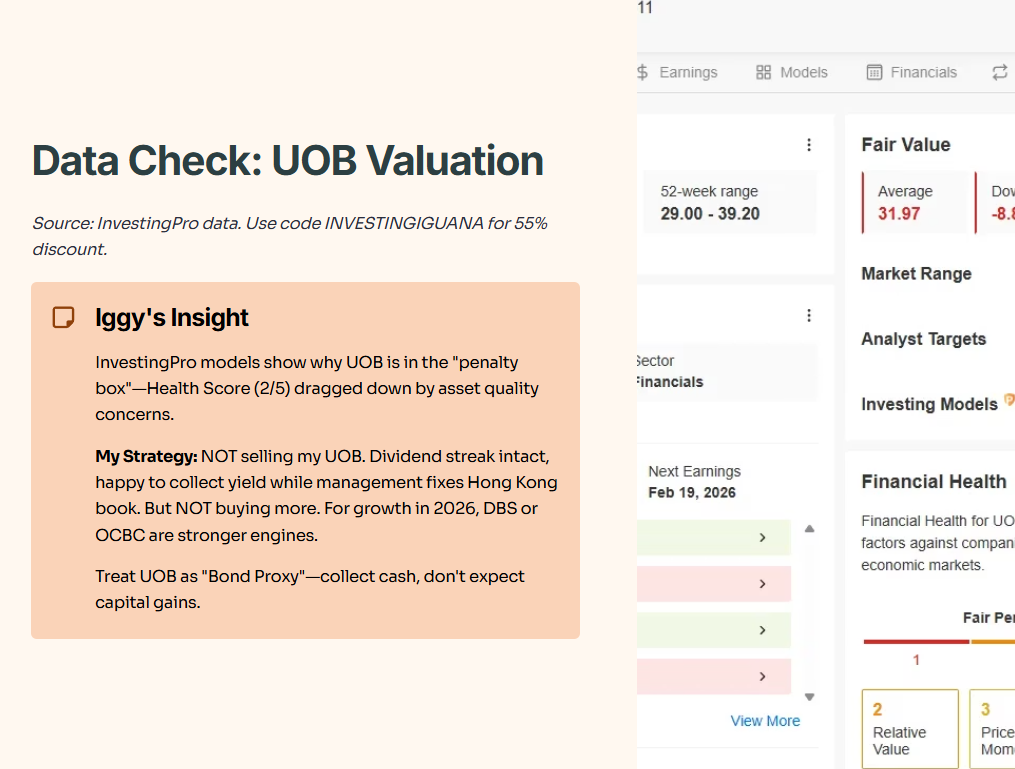

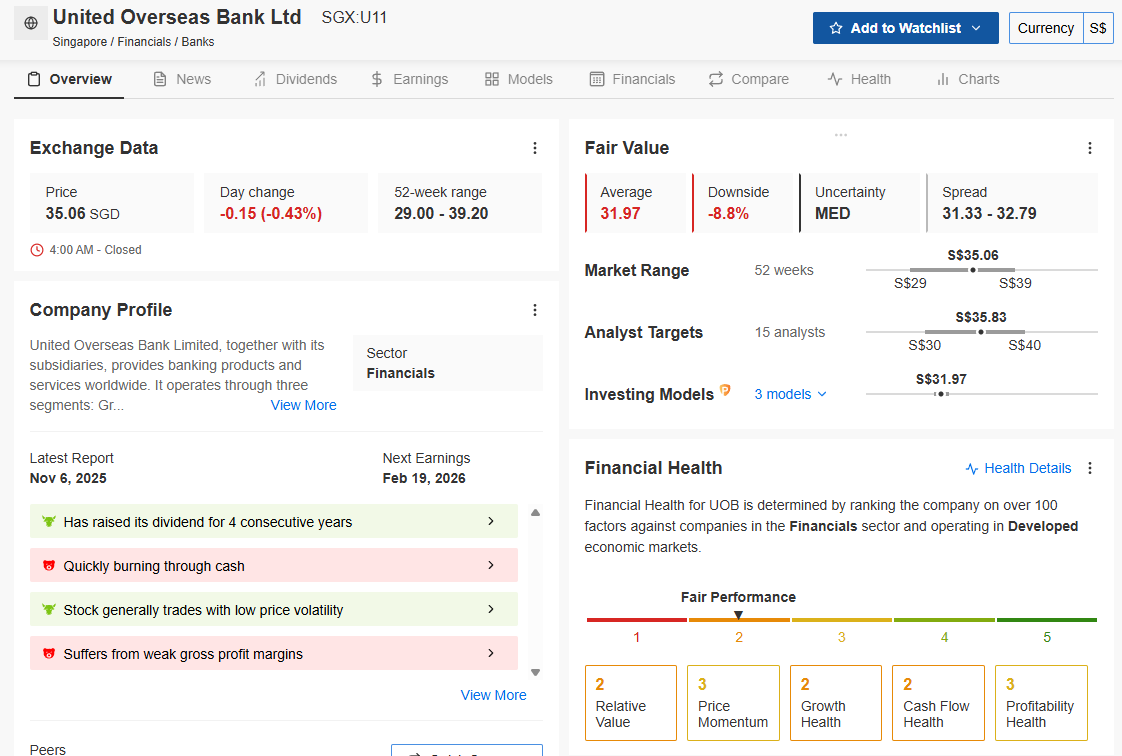

Data Check: UOB Valuation I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Iggy’s Insight: The InvestingPro models clearly show why UOB is in the “penalty box” right now. The “Health Score” (2/5) is being dragged down by these asset quality concerns.

However, let me be clear on my strategy: I am NOT selling my UOB. The dividend streak is intact, and I am happy to collect the yield while management fixes the Hong Kong book. But I am also not buying more at these levels. If you are looking for growth in 2026, the data suggests DBS or OCBC are the stronger engines. Treat UOB as a “Bond Proxy” for now—collect the cash, but don’t expect capital gains.