The Great Singapore Stock Exodus: Why Companies Are Fleeing Despite Government Rescue Efforts

Singapore’s Market Meltdown: The Real Reasons Listed Firms Can’t Wait to Leave

Editor’s Note: This post has been updated on October 19, 2025, to ensure it is fresh and accurate. It now includes a deeper analysis of the structural drivers (like private capital and regulation) causing the SGX exodus, and features a new comparative analysis of the Singaporean market versus Malaysia’s Bursa.

Singapore’s stock market faces a brutal reality that no amount of government intervention seems able to reverse—companies are abandoning the Singapore Exchange faster than new ones are joining, creating a dangerous downward spiral that threatens the city-state’s reputation as a financial hub.

The numbers tell a stark story that should worry every investor watching Singapore’s markets. Over 20 privatisation offers have emerged in 2025 alone, compared to just nine IPOs and three prospectus filings. This represents a continuation of a troubling trend where delistings have consistently outnumbered new listings for years, shrinking Singapore’s public market from 782 companies in 2013 to just over 600 today.

What makes this exodus particularly concerning is that it’s happening despite the Monetary Authority of Singapore’s aggressive S$5 billion Equity Market Development Programme (EQDP) designed to boost market liquidity and investor participation. The government’s intervention signals just how desperate the situation has become, yet companies continue to flee at an alarming pace.

In This Article:

• The Latest Casualties: AF Global and Spindex Lead the Charge

• The Root Causes: Why Companies Can’t Wait to Leave

• 1. The “Pull”: Private Capital Offers a Better Deal

• 2. The “Push”: Crushing Regulatory Burden Without Benefits

• 3. The Result: A Vicious Cycle of Illiquidity

• The Regional View: Why Malaysia’s Bursa is a Different Beast (And What SG Investors Can Learn)

• Government Response: Too Little, Too Late?

• Programme Benefits and Limitations

• Tax Incentives Fall Short

• The Private Market Alternative: Why It’s Winning

• Valuation Premiums and Certainty

• Operational Flexibility

• What This Means for Singapore Investors

• Immediate Impact on Market Structure

• Long-term Competitiveness Concerns

• Strategic Opportunities

• The Road Ahead: Can Singapore’s Stock Market Recover?

• Critical Success Factors

• Regional Competition Intensifies

• Long-term Structural Reform Needed

• Iggy’s Insights: What Should Singapore Investors Do Next?The Latest Casualties: AF Global and Spindex Lead the Charge

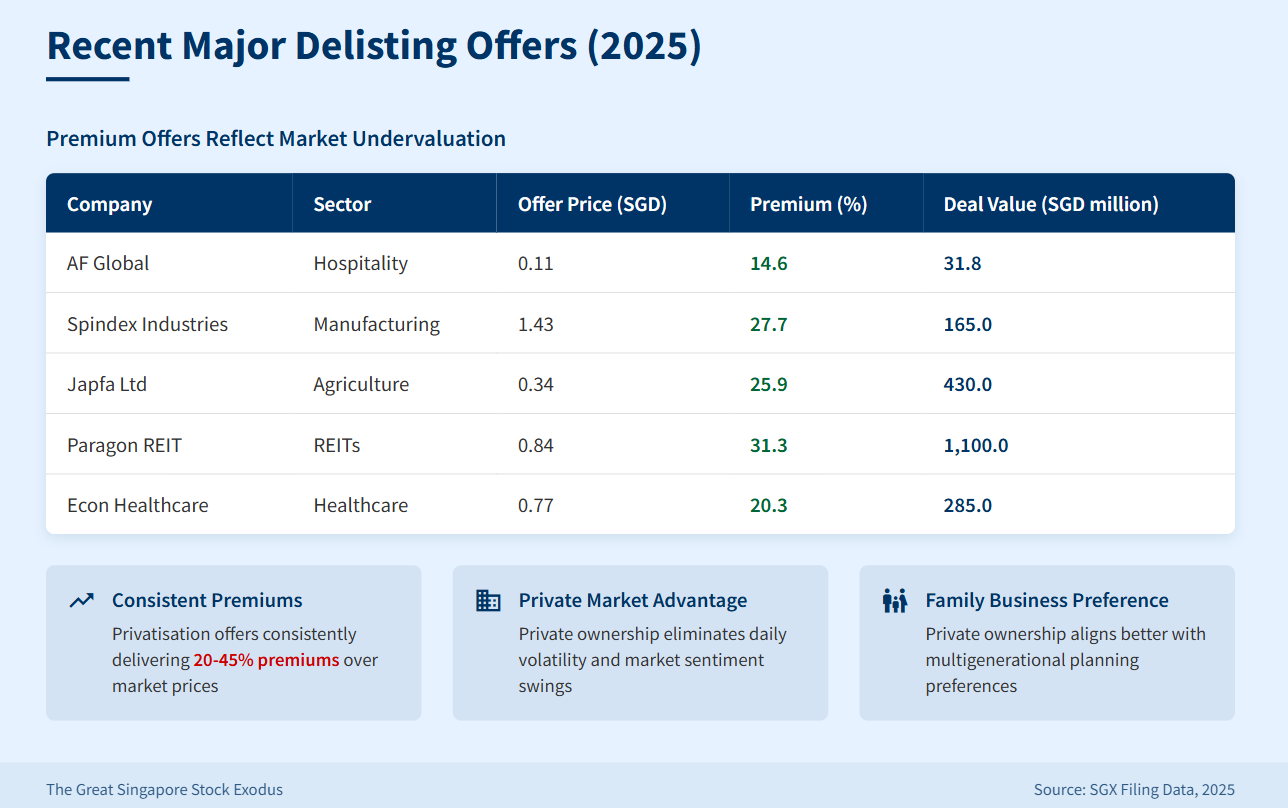

The most recent departures highlight why Singapore’s public markets have lost their appeal. AF Global, the hospitality group, received an 11-cent per share privatisation offer on October 8, 2025, from a consortium led by property tycoon Koh Wee Meng. The S$31.8 million deal values the company’s remaining 27.35% stake at a modest premium, but represents a classic case of controlling shareholders taking advantage of depressed public market valuations.

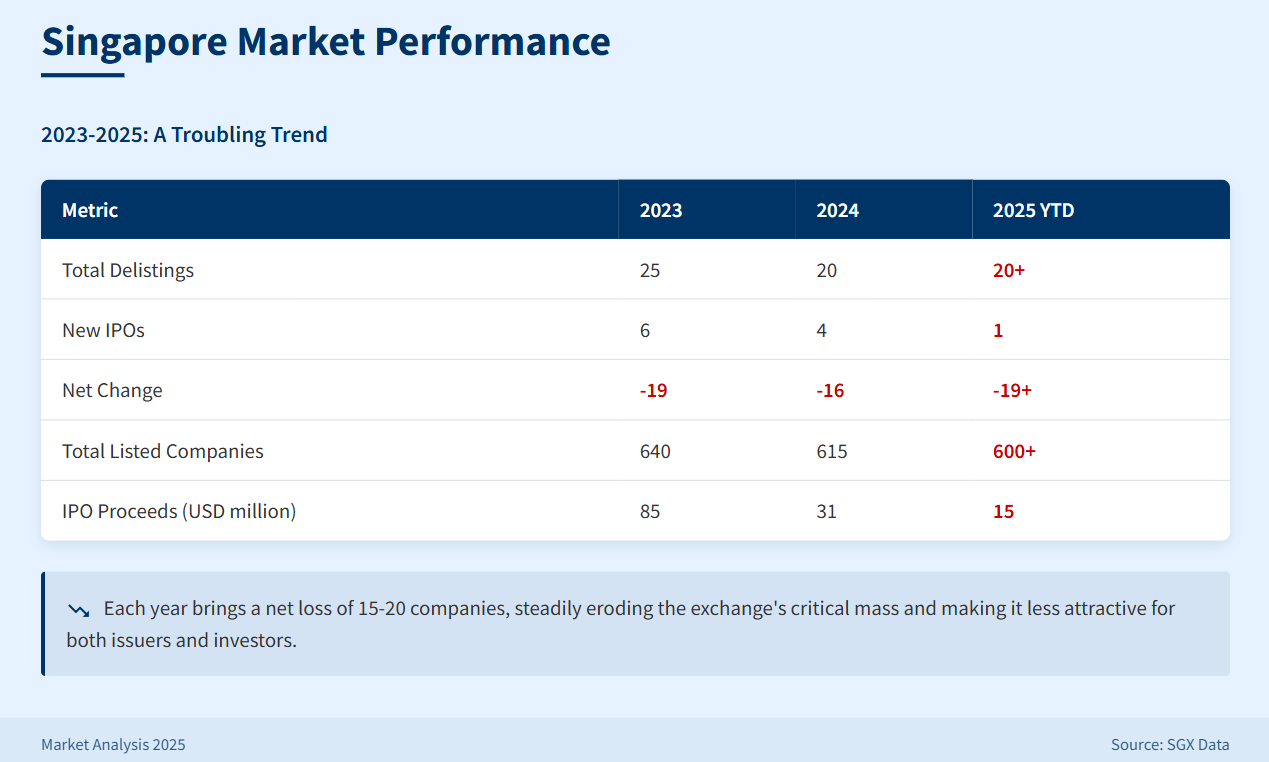

Singapore’s stock market shows a concerning trend with delistings consistently outpacing new IPO listings over the past three years

Similarly, Spindex Industries accepted a S$1.43 per share offer backed by PrimeMovers Equity, representing a 27.7% premium to its last undisturbed trading price. The precision engineering company’s controlling shareholders cited the inability to raise equity capital and limited utility of its listing status as key reasons for going private.

These deals follow a pattern seen across 2024 and 2025, where 20 companies delisted in 2024 alone while only four new companies went public. The contrast with regional peers is stark—Malaysia recorded 55 IPOs raising US$1.5 billion in 2024, while Singapore managed just US$31 million from its four listings.

The table above reveals the devastating math behind Singapore’s market decline. Each year brings a net loss of 15-20 companies, steadily eroding the exchange’s critical mass and making it less attractive for both issuers and investors.

The Root Causes: Why Companies Can’t Wait to Leave

Understanding why companies are fleeing requires looking beyond surface-level explanations. Let’s be clear: this isn’t a mystery. Companies are fleeing because the fundamental cost-benefit analysis of a public listing has completely broken down.

For many firms, especially family-owned or mid-cap ones, the “prestige” of being on the SGX no longer justifies the expense and inflexibility. This breakdown is driven by a powerful “push” away from the public market and an attractive “pull” toward a private alternative.

1. The “Pull”: Private Capital Offers a Better Deal

The rise of private equity and family office capital in Singapore has fundamentally changed the game. Firms like PrimeMovers Equity can offer immediate liquidity at attractive valuations without the ongoing compliance burden of public markets.

With Singapore hosting over 700 family offices managing more than S$100 billion in assets, private capital has become a viable, and often superior, alternative to public funding. Why fight for scraps from public investors when a private fund will write you a check at a 30% premium?

2. The “Push”: Crushing Regulatory Burden Without Benefits

While private options have become more attractive, the public market has become more expensive. Public companies face annual compliance costs ranging from S$500,000 to S$2 million, covering audit fees, regulatory filings, board expenses, and investor relations. For smaller companies generating modest profits, these costs represent a significant drag on shareholder returns.

This burden has only increased. New requirements for sustainability reporting, enhanced corporate governance, and increased disclosure obligations make public listing particularly unattractive for family-controlled businesses that prefer operating flexibility.

3. The Result: A Vicious Cycle of Illiquidity

These two factors—a better private alternative and high public costs—are what cause the most damaging symptom: chronic low liquidity.

This is the pricing death spiral. When companies see no benefit in being public, they don’t engage investors. When better opportunities are private, capital flows there first. This leaves two-thirds of the 600+ listed companies trading at extremely low volumes, many below S$100,000 a day.

This poor liquidity leads to wide bid-ask spreads, which discourages trading, which further reduces liquidity. For the companies trapped in this cycle, their shares trade at persistent discounts to fair value, making it impossible to use equity for acquisitions or employee compensation. When a private equity firm shows up offering a 25-40% premium to that depressed market price, the decision to leave becomes obvious.

The Regional View: Why Malaysia’s Bursa is a Different Beast (And What SG Investors Can Learn)

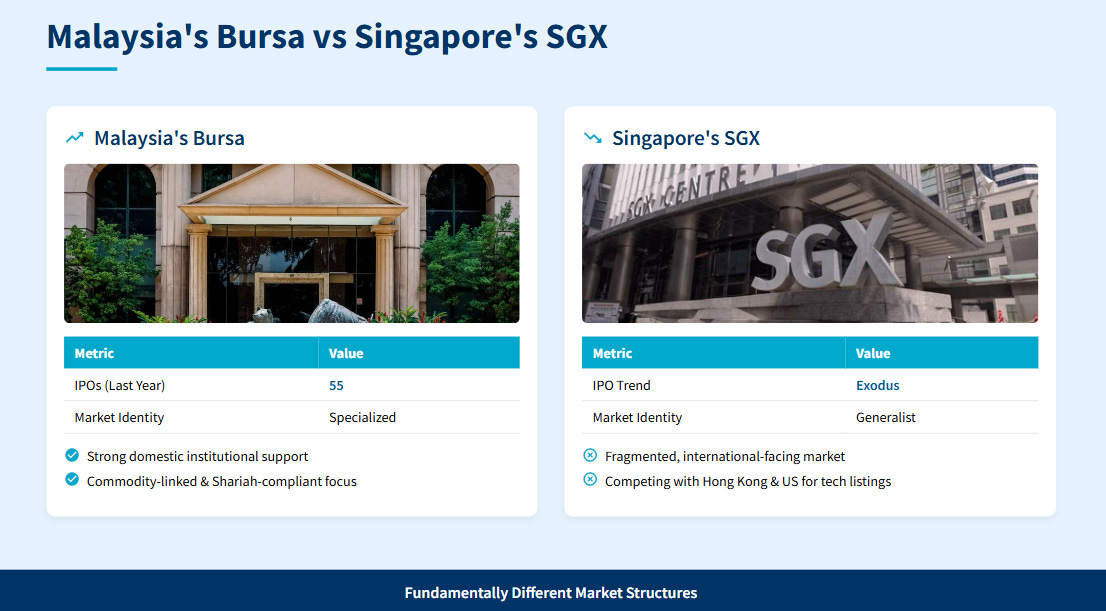

The contrast with Singapore’s northern neighbor couldn’t be starker. As the SGX struggles with an exodus, Malaysia’s Bursa recorded 55 IPOs last year. This isn’t an accident; it’s the result of a fundamentally different market structure that SGX cannot easily replicate.

First, Malaysia boasts powerful domestic institutional support. Giants like the Employees Provident Fund (EPF) and Permodalan Nasional Berhad (PNB) act as cornerstone investors and long-term capital providers. This creates a stable “floor” for liquidity and valuations that Singapore’s more fragmented, international-facing market lacks.

Second, Bursa has a clear, distinct identity. It is a regional powerhouse for commodity-linked industries (like palm oil) and a global leader in Shariah-compliant listings. This specialized focus attracts a dedicated pool of capital looking for that specific exposure, unlike the SGX which often competes (and currently loses) against Hong Kong and the US for high-growth tech listings.

So, why should a Malaysian investor, enjoying a robust IPO market, care about Singapore’s woes?

For one, regional stability. A weakened SGX impacts the entire ASEAN capital market ecosystem, affecting investor sentiment. More directly, many Malaysian investors hold cross-listed stocks or invest in Singaporean S-REITs for dividend income. A liquidity crisis in Singapore can trap their capital or devalue those specific holdings.

For Singaporean investors, the lesson from Malaysia is that a market needs a strong domestic identity and reliable local support to thrive. For Malaysian investors, the takeaway is twofold: appreciate the structural advantages of your home market, but also recognize that the “growth” sectors (like deep tech or global finance) that SGX is failing to retain are now increasingly looking to KL as a viable alternative. The weakness in one hub creates an opportunity in the other.

Government Response: Too Little, Too Late?

The Monetary Authority of Singapore’s S$5 billion EQDP represents the most ambitious attempt to revive the local stock market in decades. The programme allocates government funding to co-invest with asset managers specifically targeting small and mid-cap Singapore stocks, while offering tax incentives for new listings and fund managers.

In July 2025, MAS appointed three fund managers—Avanda, Fullerton, and JP Morgan—to deploy the first S$1.1 billion tranche. The selection of credible, experienced institutions signals serious commitment to the initiative.

Programme Benefits and Limitations

The EQDP addresses some critical pain points. The liquidity injection is substantial in the context of small-cap stocks, which historically account for about one-third of SGX’s daily trades. Enhanced research coverage and investor outreach should help address the visibility problem that plagues many smaller companies.

However, structural challenges remain. The S$5 billion represents only about 1.5% of annual traded value across all SGX stocks. More critically, the programme doesn’t address the fundamental issue of why companies choose to list elsewhere in the first place.

Tax Incentives Fall Short

The new tax measures include a 20% corporate tax rebate for primary listings and a concessionary 5% tax rate for newly listed fund managers. While helpful, these incentives pale in comparison to the liquidity and valuation benefits available in larger markets like Hong Kong or the United States.

The mandatory 30% allocation to Singapore equities required for the concessionary tax rate may actually deter global fund managers who prefer flexibility in portfolio construction.

The Private Market Alternative: Why It’s Winning

The surge in delistings reflects a broader global trend toward private markets, but Singapore’s situation is particularly acute. Private equity firms and family offices can offer several advantages that public markets currently cannot match.

Valuation Premiums and Certainty

Recent privatisation offers have consistently delivered premiums of 20-45% over market prices. AF Global’s 11-cent offer represents a 14.6% premium, while Spindex’s S$1.43 offer came at a 27.7% premium. These premiums reflect the discount at which public markets value Singapore companies.

More importantly, private ownership eliminates the daily volatility and market sentiment swings that can devastate public company valuations during uncertain times.

Operational Flexibility

Private companies enjoy greater flexibility in capital allocation, strategic planning, and operational decisions. They can pursue long-term value creation without quarterly earnings pressure or the need to satisfy diverse shareholder groups with different investment horizons.

For family-controlled businesses, which represent a significant portion of Singapore’s listed companies, private ownership aligns better with their preference for control and multigenerational planning.

What This Means for Singapore Investors

The delisting trend creates both risks and opportunities for Singapore investors. Understanding the implications is crucial for portfolio positioning.

Immediate Impact on Market Structure

The shrinking universe of listed companies concentrates trading activity in fewer stocks, making the market increasingly dominated by large-cap names and REITs. The Straits Times Index constituents now represent an even larger portion of total market activity, potentially creating concentration risk for index investors.

Smaller investors face reduced choice and may find it harder to build diversified Singapore-focused portfolios. The disappearance of mid-cap growth stories particularly hurts investors seeking exposure to Singapore’s economic development.

Long-term Competitiveness Concerns

Singapore’s role as a regional financial hub depends partly on having a vibrant capital market that can facilitate corporate growth and capital formation. The current trend undermines this positioning and may accelerate the flight of financial services activities to competing centres.

However, the government’s intervention through EQDP and other measures shows strong commitment to addressing these issues. If successful, these programmes could create attractive opportunities for investors willing to take positions in undervalued Singapore companies.

Strategic Opportunities

Contrarian investors may find compelling opportunities among Singapore’s unloved small and mid-cap stocks. Companies trading below book value with solid fundamentals could benefit significantly if the EQDP successfully improves market liquidity and sentiment.

The focus on privatisation also creates event-driven opportunities, though investors must be selective and understand the risks of betting on takeover premiums.

The Road Ahead: Can Singapore’s Stock Market Recover?

The success of Singapore’s market revival efforts will depend on addressing structural issues beyond just injecting liquidity. Several factors will determine whether the delisting trend can be reversed.