The Hype Around STI 10,000: What DBS Isn’t Telling You.

Their 15-year prediction has a fatal flaw that's buried in the math. We dug it up.

Your neighbors are buzzing about a bold forecast. DBS Group Research just claimed Singapore’s Straits Times Index could hit 10,000 points by 2040. That’s triple where it sits today.

You might feel confused. The STI sat stuck for 17 years before finally breaking 4,000 points in July 2025. Now DBS says it could more than double again in just 15 years. What changed? And more importantly, should you bet your retirement savings on this prediction?

This analysis cuts through the hype. We explore the real drivers behind DBS’s forecast, calculate what returns you actually need, and identify the hidden risks that could derail this journey. By the end, you’ll know if this prediction holds water or if it’s just another optimistic bank projection.

In This Article:

• The 17-Year Stalemate Finally Broke

• DBS’s Bold Vision: Singapore’s Economy Could Double

• The Currency Play: Singapore Dollar Hits Parity

• The Math Behind 10,000: What Returns Do You Need?

• Three Forces That Could Drive the Rally

• Passive Funds and Large-Cap Stocks

• Government Support for Small and Mid-Cap Stocks

• Deposit Reallocation as Interest Rates Fall

• The STI’s Built-In Handbrake: Why 9% Is a Tough Ask

• The STI’s Concentration Risk: A Bet on Three Banks

• The Conservative Culture Problem

• Technology Companies Are Missing

• The Macro Headwinds: Beyond the Index Itself

• Safe Haven Status Has Limits

• Productivity Challenges Ahead

• Interest Rate Sensitivity Creates Risk

• The 2040 Timeline Matters

• Comparing to Other Markets

• What Could Actually Go Right

• The Bottom Line for Singapore Investors

• Your Strategic DecisionThe 17-Year Stalemate Finally Broke

Singapore’s benchmark stock index hit a wall in 2007. The STI peaked at 3,830 points and then spent nearly two decades going nowhere.

That painful period ended in July 2025. The index broke through 4,000 points and kept climbing. By October 2025, it pushed past 4,400 points, marking a genuine shift in market momentum.

Timothy Wong, head of DBS Group Research, calls this a “medium-term bullish shift.” He points to several factors: fading US exceptionalism, Singapore’s safe-haven appeal, attractive valuations, low domestic interest rates, and support from the Monetary Authority of Singapore.

The STI has gained more than 15% since the start of 2025. That performance stands out, especially when you compare it to the previous 17 years of stagnation.

DBS’s Bold Vision: Singapore’s Economy Could Double

DBS doesn’t just see a strong stock market ahead. The bank predicts Singapore’s entire economy will more than double by 2040.

The numbers look ambitious. Singapore’s GDP stood at US$547 billion in 2024. DBS forecasts it will reach between US$1.2 trillion and US$1.4 trillion by 2040. That growth would be driven by three main engines: capital accumulation, human capital development, and productivity gains.

Real GDP growth would average 2.3% annually from 2025 through 2040. That pace might sound modest, but it outpaces other developed economies. For a mature, high-income nation like Singapore, maintaining 2.3% annual growth represents solid performance.

The services sector plays a starring role in this story. DBS expects services to contribute nearly 74% of Singapore’s nominal gross value-added by 2040. Within services, wholesale trade, transport, and storage would account for 29% of GVA. Financial services could rise to 15% of GVA, while information and communication might reach 6.3%, powered by cloud computing, data analytics, and artificial intelligence.

Here’s what DBS projects for Singapore’s economic structure by 2040:

Singapore’s Economic Composition: 2040 Projection

The projection assumes Singapore maintains its edge as a global financial hub, strengthens its position in digital IT services, and expands its care economy to serve an aging population.

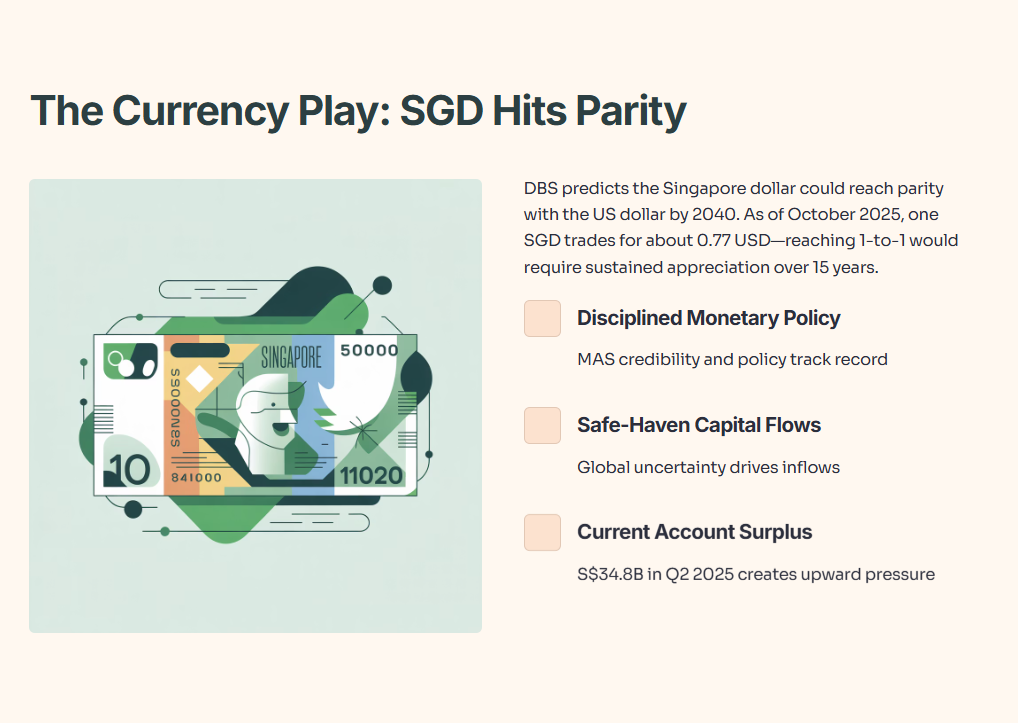

The Currency Play: Singapore Dollar Hits Parity

DBS makes another striking prediction. The Singapore dollar could reach parity with the US dollar by 2040.

That would be a massive shift. As of October 2025, one Singapore dollar trades for about 0.77 US dollars. Reaching 1-to-1 parity would require sustained appreciation over 15 years.

Four factors could drive this currency strength. First, disciplined monetary policy from MAS has built credibility. Second, Singapore continues to attract safe-haven capital flows as global uncertainty persists. Third, productivity improvements support fundamental economic strength. Fourth, Singapore runs a persistent current account surplus, which creates natural upward pressure on the currency.

Singapore’s current account surplus hit S$34.8 billion in the second quarter of 2025. That surplus reflects the country’s position as a net exporter of goods and services. When a country consistently exports more than it imports, foreign demand for its currency increases, pushing the exchange rate higher.

The US dollar may also weaken during this period. The dollar experienced significant declines in the first half of 2025 as markets questioned US exceptionalism. If that trend continues, it would make Singapore dollar parity more achievable.

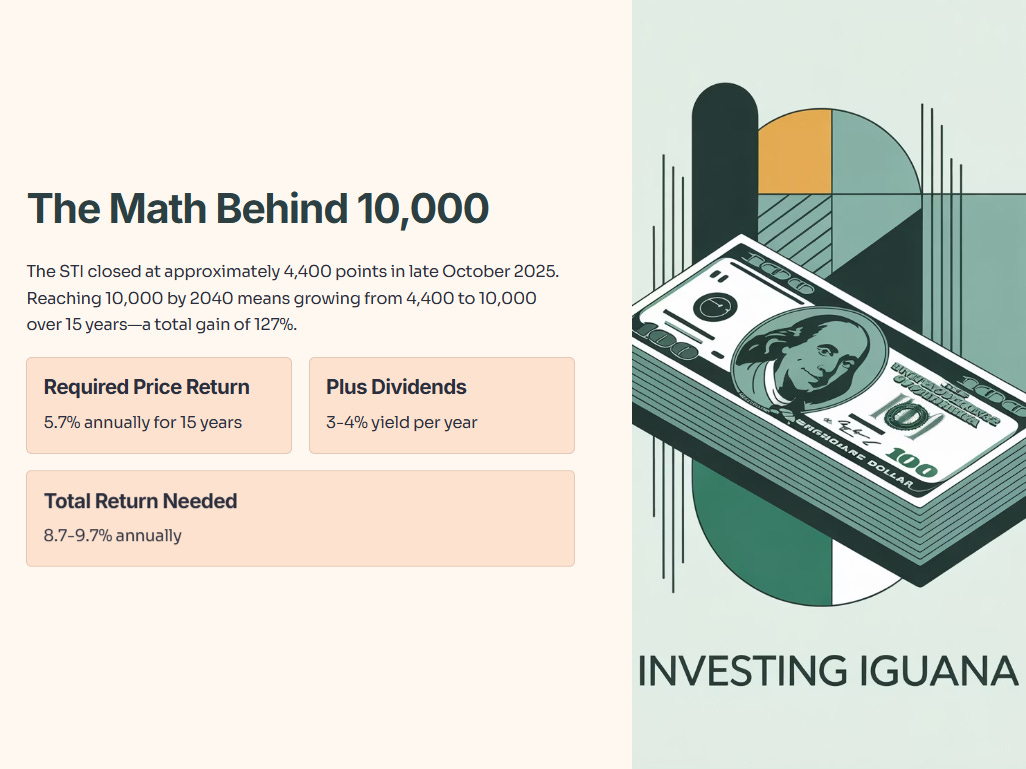

The Math Behind 10,000: What Returns Do You Need?

Let’s calculate what the STI needs to deliver for DBS’s prediction to come true.

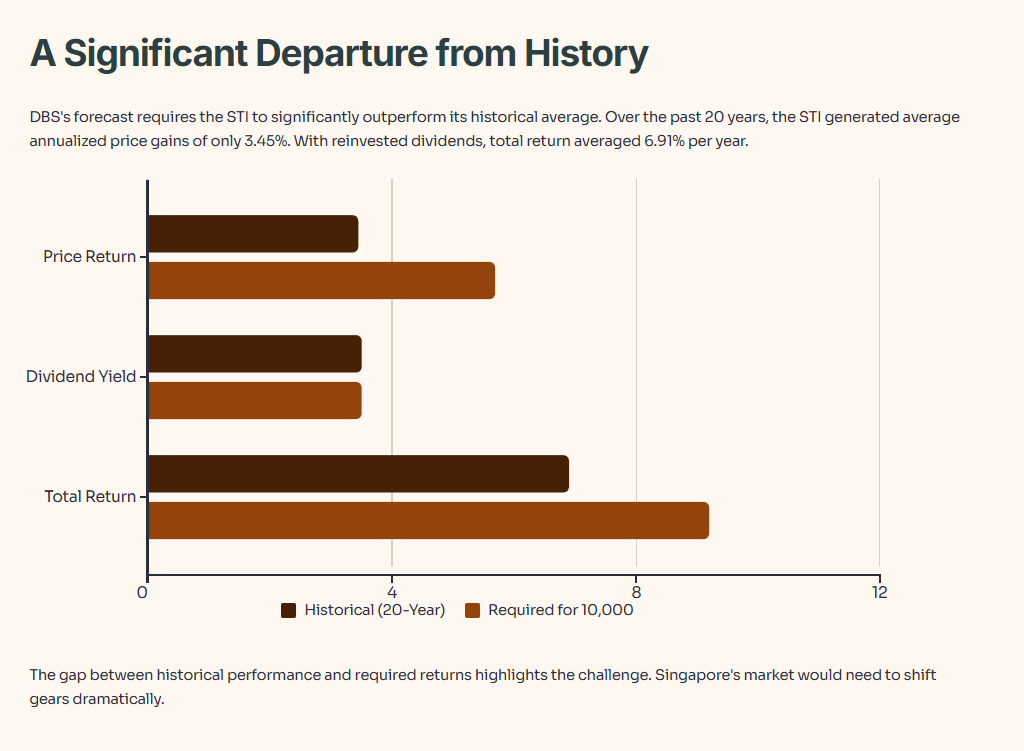

The STI closed at approximately 4,400 points in late October 2025. Reaching 10,000 points by 2040 means the index must grow from 4,400 to 10,000 over 15 years. That represents a total gain of 127%.

Using compound annual growth rate calculations, the STI would need to deliver approximately 5.7% annual price returns. Add in dividends of roughly 3% to 4% per year, and you’re looking at total returns of 8.7% to 9.7% annually.

Those numbers might seem reasonable at first glance. But Singapore’s stock market has a patchy track record.

Over the past 20 years, the STI generated average annualized price gains of only 3.45%. When you include reinvested dividends, the total return averaged 6.91% per year. Over the last 10 years, STI ETF returns averaged just 4.29% annually.

So DBS’s forecast requires the STI to significantly outperform its historical average. Instead of the 7% total returns Singapore investors got used to, you would need 9% or more every single year for 15 years.

Required Returns: STI Path to 10,000

The gap between historical performance and required returns highlights the challenge. Singapore’s market would need to shift gears dramatically.

Three Forces That Could Drive the Rally

DBS identifies three funding sources that could push Singapore equities higher over the next 15 years.

Passive Funds and Large-Cap Stocks

Passive funds should drive growth in large-cap stocks. Safe-haven inflows from US and European passive funds could more than offset outflows from active funds. As global investors seek stability amid tariff wars and geopolitical tensions, Singapore’s reputation as a safe jurisdiction becomes more valuable.

Government Support for Small and Mid-Cap Stocks

The Equity Market Development Programme launched by MAS injects S$5 billion into Singapore equities. The programme focuses specifically on improving liquidity and broadening participation in small and mid-cap stocks.

MAS appointed the first three asset managers in July 2025: Avanda Investment Management, Fullerton Fund Management, and JP Morgan Asset Management. These managers received an initial combined allocation of S$1.1 billion, with more appointments coming later in 2025.

The impact is already visible. The FTSE ST Mid and Small Cap Index rose 9% in the third quarter of fiscal 2025, outpacing the blue-chip STI’s 7% gain during the same period. Institutional inflows into small and mid-cap stocks hit S$382 million in Q3 2025, with nearly half flowing into eight technology stocks.

Deposit Reallocation as Interest Rates Fall

As interest rates decline, depositors will redeploy funds from money market accounts, fixed deposits, and high-yield savings accounts into stocks. This rotation favors income and staples stocks across all market capitalizations.

Singapore’s three major banks—DBS, OCBC, and UOB—currently offer dividend yields between 4.5% and 5%. REITs provide even higher yields, with the average Singapore REIT offering 6.9% as of February 2025. These yield levels become more attractive as deposit rates fall.

The STI’s Built-In Handbrake: Why 9% Is a Tough Ask

The STI’s Concentration Risk: A Bet on Three Banks

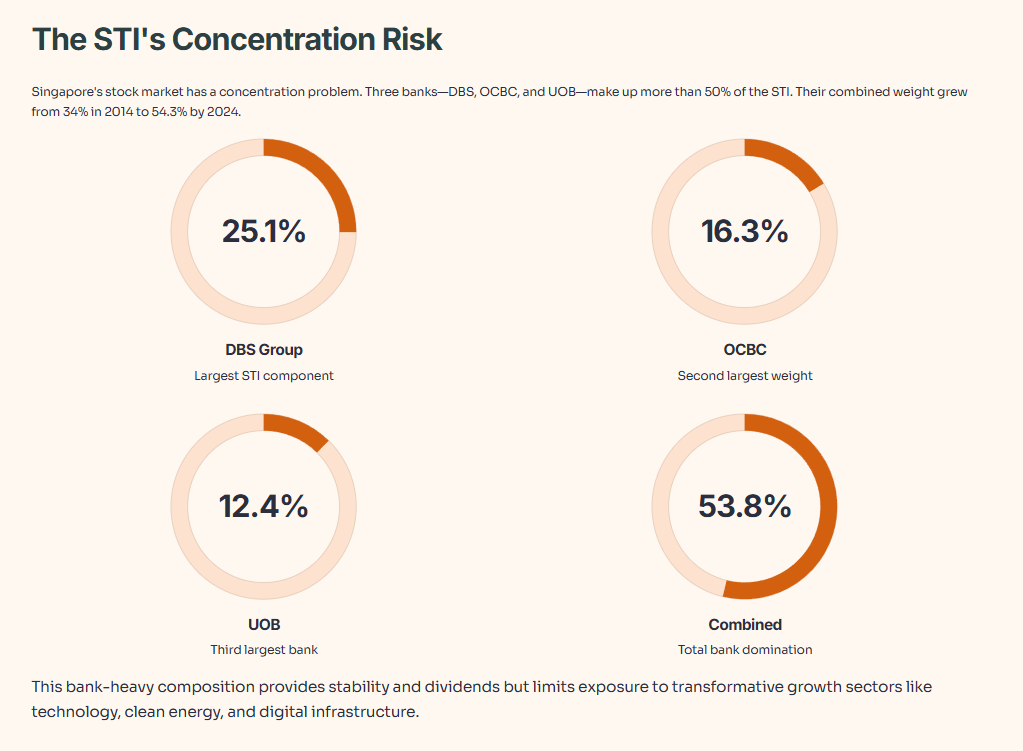

Singapore’s stock market has a concentration problem. Three banks—DBS, OCBC, and UOB—make up more than 50% of the STI.

Their combined weight has grown substantially. In 2014, the three banks accounted for about 34% of the index. By 2024, that figure reached 54.3%. As of late 2025, their weight stood above 52%.

This bank-heavy composition provides stability and steady dividend income. But it also limits exposure to transformative growth sectors like technology, clean energy, and digital infrastructure.

The lack of diversity creates risk. When interest rates shift or credit conditions change, the entire index moves with the banks. You’re not getting broad exposure to Singapore’s economy. You’re mostly betting on three financial institutions.

STI Composition: Bank Domination

The banks delivered strong returns in recent years. DBS posted a 166% five-year total return, OCBC gained 96%, and UOB returned 82%. But those gains came during a period of rising interest rates. As rates normalize, bank profitability faces pressure.

The Conservative Culture Problem

Singapore’s investment culture leans heavily toward safety and yield. That conservative approach has served investors well in many ways. But it also creates obstacles for the market’s growth.

Investors here prefer steady dividends over capital growth. A 2024 survey found that 42% of Singapore investors favored a conservative approach, with only 24% willing to be aggressive. By contrast, investors elsewhere in Asia and the Middle East showed more appetite for risk, with 34% adopting aggressive strategies.

This preference shows up in portfolio construction. Retail and institutional investors overweight REITs, dividend-paying stocks, and real estate. They underweight high-growth technology companies and emerging sectors.

DBS acknowledges this challenge directly. The bank states that Singapore’s “traditionally conservative investment culture must evolve to accommodate higher-growth, higher-valuation stocks that reflect the new economy’s dynamics.”

Without this cultural shift, the STI will struggle to attract and retain high-growth technology companies. These firms will continue listing on larger international exchanges like Nasdaq or Hong Kong instead of Singapore.

Technology Companies Are Missing

Walk through the STI’s 30 components and you’ll notice something odd. The index barely includes any pure technology companies.

Singapore Exchange data shows the STI is dominated by financials (over 56%), real estate and REITs (about 15%), and then smaller allocations to industrials, consumer services, and telecommunications. Technology plays a minor role.

This stands in sharp contrast to indices like the S&P 500, where technology companies represent the largest sector. The lack of tech exposure limits the STI’s growth potential.

Small and mid-cap technology stocks exist in Singapore. Companies like iFast, Frencken, Venture, UMS, and Valuetronics have performed well. But they remain outside the main index.

The government’s Equity Market Development Programme specifically targets this gap. By improving liquidity in small and mid-cap stocks, MAS hopes to nurture these companies until they grow large enough to enter the STI.

Success requires more than just funding. Singapore must convince high-growth tech firms to list locally rather than seeking foreign exchanges. That means improving the regulatory environment, deepening capital markets, and attracting more international investors.

The Macro Headwinds: Beyond the Index Itself