SGX Watch List Removed: The "3-Year Loss" Rule You Must Know

The regulatory safety net is gone. Here is the forensic playbook to distinguish the next Avi-Tech from the next delisting disaster.

The Singapore Exchange (SGX) has officially changed the rules of the game. As of October 2025, the Financial Watch List—that badge of shame slapped on companies with three consecutive years of losses and low market caps—is history.

On paper, this move towards a “market-driven regime” sounds modern. It aligns us with global standards where the market, not the regulator, decides who lives and who dies. But for the retail investor, the uncle managing his own CPF, or the retiree hunting for yield, the removal of the Watch List removes a giant, flashing “DANGER” sign.

The risk factors haven’t disappeared—just the label. The “Zombies” are still walking among us, but now they don’t wear a warning tag.

If you are holding small-cap Singaporean equities, you need to become your own regulator. Today, we are going to look at the history of the Watch List to understand who survived, who failed, and how you can spot the difference before your capital evaporates.

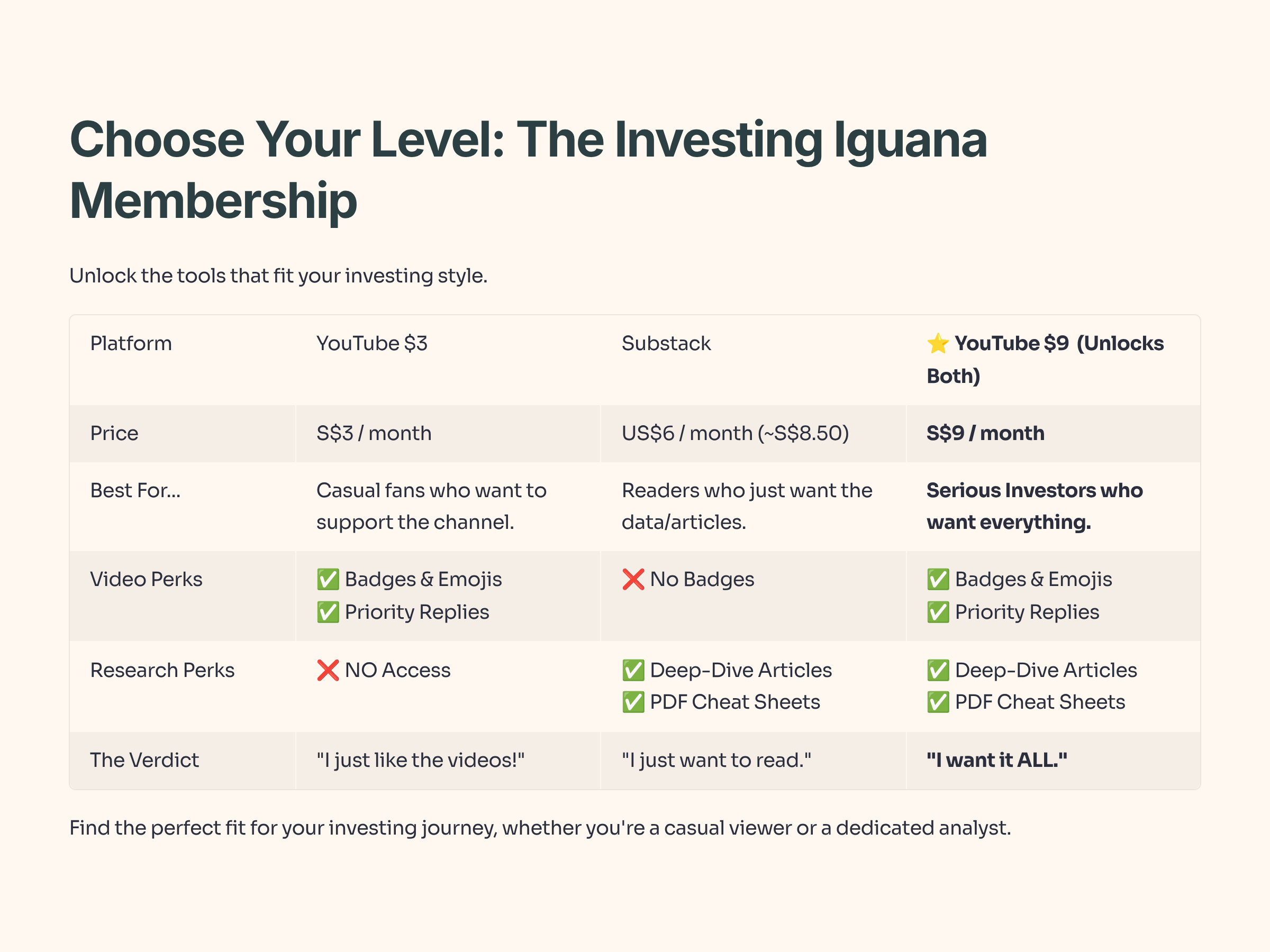

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

The Graveyard and The Graduates

To understand the future, we have to look at the past. Under the old regime, companies were placed on the Watch List if they recorded pre-tax losses for the three most recent completed financial years and had an average daily market cap of less than S$40 million.

They were given a deadline (usually 36 months) to shape up or ship out (delist).

Most failed. Companies like Dragon Group and CNA Group were delisted, leaving shareholders with pennies on the dollar or totally illiquid scrip. But a rare few managed to “graduate” and return to profitability.

The difference between the survivors and the failures wasn’t luck. It was a specific operational behavior.

The “Survival of the Fittest” Data

Iggy’s Insight: The “Growth” Trap

Here is the pattern nobody talks about: The companies that failed (Dragon, CNA) often tried to grow their way out of trouble. They announced new projects, expansions, or “strategic pivots” while their core cash flow was negative.

The companies that survived (Avi-Tech, S i2i) did the opposite. They shrank. They accepted they were smaller companies. They sold assets. They fired people. They acted like Steve Jobs returning to Apple in 1997—slashing 70% of the product line to save the ship. In a turnaround play, boring is bullish.

The New Reality: How to Spot a “Zombie” Without the Label

Now that SGX won’t tell you who is on the Watch List, you have to calculate it yourself. The dynamics that created the list are still present.

1. The “Three Strikes” Rule Still Applies

Just because the rulebook changed doesn’t mean the math did. If a company has posted three consecutive years of losses, they are statistically likely to face a liquidity crunch or a dilutive rights issue.

You must check the Income Statement manually. Do not rely on “Adjusted EBITDA” or “Pro Forma” numbers. Look at Net Profit Attributable to Shareholders. If it’s red for 3 years, stay away unless you see a massive change in management.

2. Cash Preservation vs. Revenue Growth

When analyzing a distressed small-cap, ignore the Revenue line. Look at the Cash Flow from Operations (CFO).

The Survivor Signal: Revenue is dropping, but Cash Flow is turning positive. This means they are cutting unprofitable contracts.

The Zombie Signal: Revenue is flat or rising, but Cash Flow is deeply negative. This means they are “buying revenue” at a loss to keep up appearances.

Iggy’s Take: Governance is the First Indicator

When a company is in trouble, I look at the Board of Directors.

If the company is bleeding cash and the Board is still comprised of the founder’s family and friends who have been there for 10 years, the company will likely die. They are too emotionally attached to cut the cancer.

You want to see “The Butcher.” A new CEO or CFO appointed specifically to restructure. You want to see consolidation signals. If they are announcing a “Grand Expansion into AI” while they can’t pay their current bills, run.

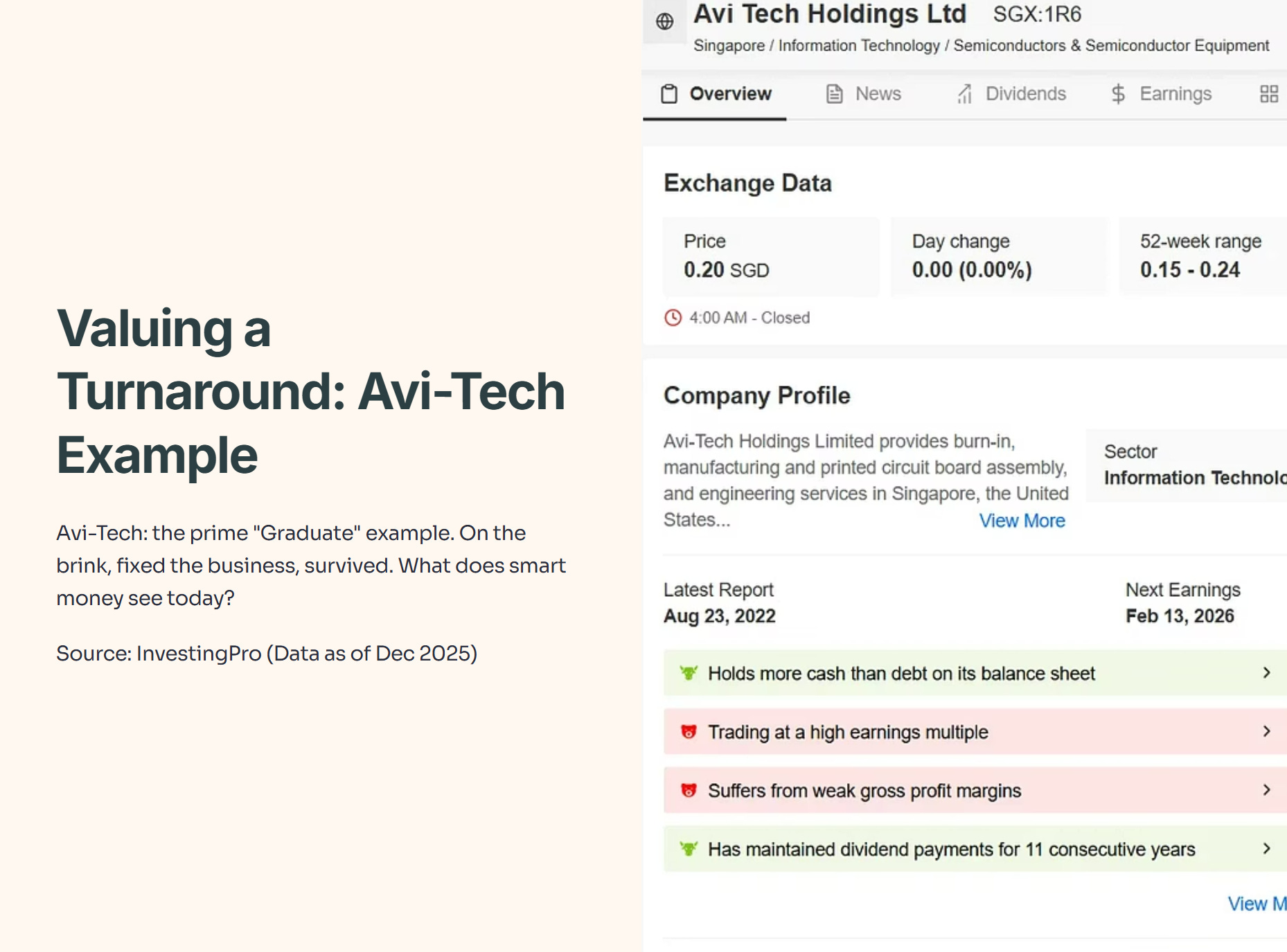

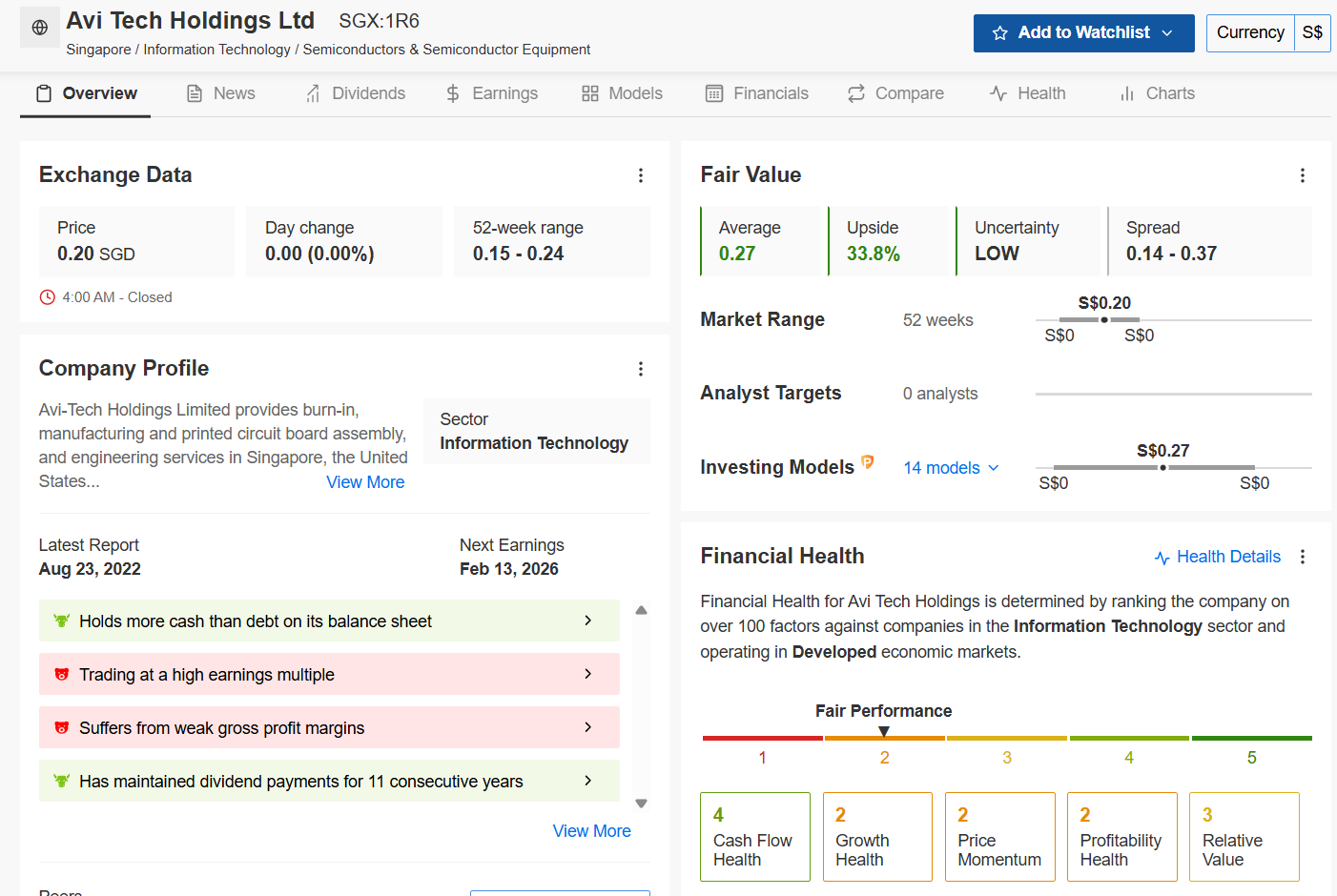

Data Check: Valuing a Turnaround (Avi-Tech Example)

Let’s look at Avi-Tech as the prime example of a “Graduate.” They were on the brink, they fixed the business, and they survived. But what does the smart money see in a “boring” company like this today?

I don’t just guess at valuations. I check the institutional models to see if the recovery is priced in.

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Data Verdict:

Look at that Health Score. It’s an overall 2/5 (”Fair”), which scares off the growth investors. But look closer at the sub-scores: the Cash Flow Health is a 4/5.

This confirms my thesis perfectly. A survivor doesn’t need “Growth Health” (which is a weak 2 here); it needs cash. The model also flags that Avi-Tech “Holds more cash than debt” and has “maintained dividend payments for 11 consecutive years.” That is the definition of a Watch List Graduate.

The institutional models currently calculate a Fair Value of S$0.27, implying a 33.8% Upside from the current S$0.20 level. This isn’t a “to the moon” play; it’s a mispricing of safety.

The Investor’s Playbook: Navigating the Post-Watch List Era

The removal of the Watch List is not a signal to take more risk. It is a signal that you must be more vigilant. Here is your action plan for the week: