The Iran War is Paying for the Mall's Aircon with Your Dividends

Why your dividends are currently being incinerated just to keep the neighborhood mall at a chilly 22°C.

The REIT Reckoning: Who Survives the eighty dollar Oil Squeeze?

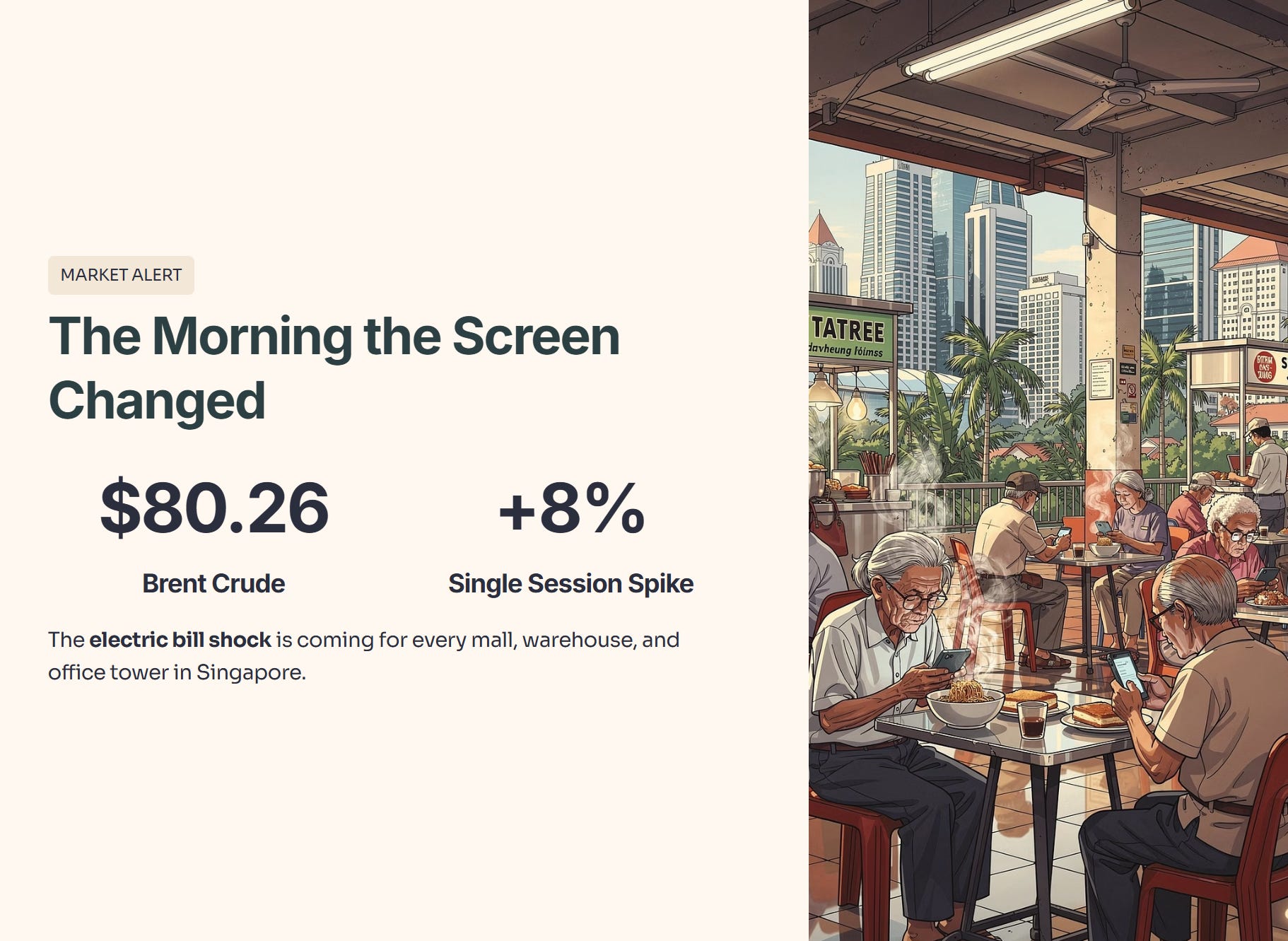

The morning humid air at the Amoy Street Food Centre usually smells of kopi and charred char kway teow. But today, the chatter among the uncle crowd is not about the four D results. It is about the screen. Brent Crude just touched eighty dollars and twenty-six cents, jumping eight percent in a single Monday morning session as the Middle East caught fire. You feel it in your pocket before you see it in your brokerage account. The electric bill shock is coming for every mall, every warehouse, and every office tower in Singapore.

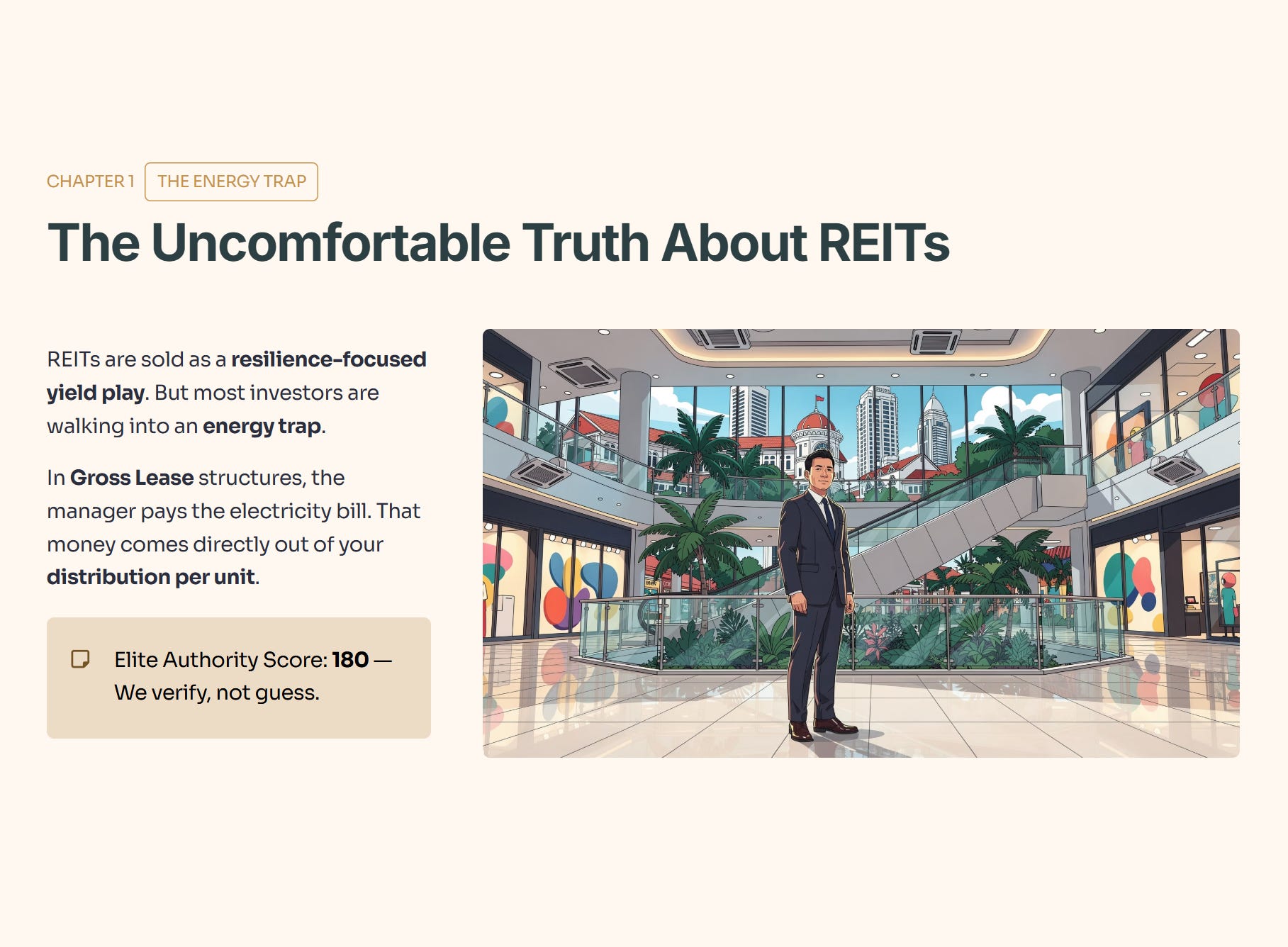

And let us be honest, the consensus view is that Real Estate Investment Trusts are a resilience-focused yield play for your benchmark comparison. But here is the uncomfortable truth: most investors are walking into an energy trap. When oil prices spike, the Gross Lease structures in our favorite suburban malls turn into a silent tax on your dividends. If the manager pays the electricity bill to keep the air conditioning running at twenty-two degrees Celsius while the world burns, that money is coming directly out of your distribution per unit.

I’ve spent the weekend auditing the Singapore Exchange sector against this new reality. With the Elite Authority now standing at 180+, we do not guess. We verify.

In This Article:

The Masterclass: The Energy Pass-Through

Step One: The Health Check

Mapletree Logistics Trust (M44U)

AIMS APAC REIT (05RU)

Step Two: The Wealth Check

Step Three: The Price Check

Step Four: The Future Check

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 170

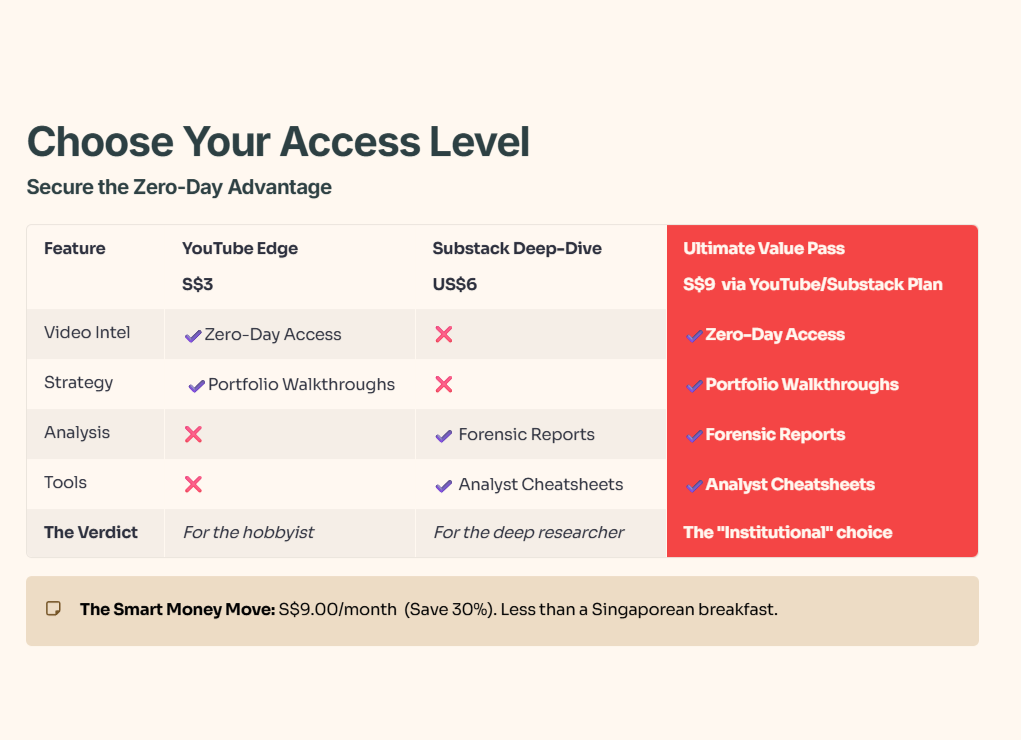

In the Singapore market, the gap between a smart entry and becoming someone else’s exit liquidity can be as little as 48 hours. That’s the cost of informational lag.

Free subscribers get my analysis up to 14 days later. The Elite 170 get it the moment it’s ready.

Your Edge: The S$9 Ultimate Value Pass bundles zero-day video intel, forensic reports, and analyst cheatsheets into one institutional-grade feed — for less than a Singaporean breakfast.

The Masterclass: The Energy Pass-Through

Think of a trust like a landlord of a Housing Development Board shop-house. In a Net Lease, the tenant pays the utilities bill directly. If electricity prices go up, the tenant grumbles, but the landlord’s profit stays the same. In a Gross Lease—which is how most Singapore malls like Capitaland Integrated Commercial Trust and Frasers Centrepoint Trust operate—the landlord provides the cool air as part of the service.

When Brent Crude hits eighty dollars, the cost of generating that cool air spikes. If the landlord cannot raise rents fast enough to pass through those costs, the profit margin shrinks like a piece of bak kwa left in the sun. So what does this mean for you? It means you are not just betting on property prices; you are betting on the manager’s ability to outrun the utility man.

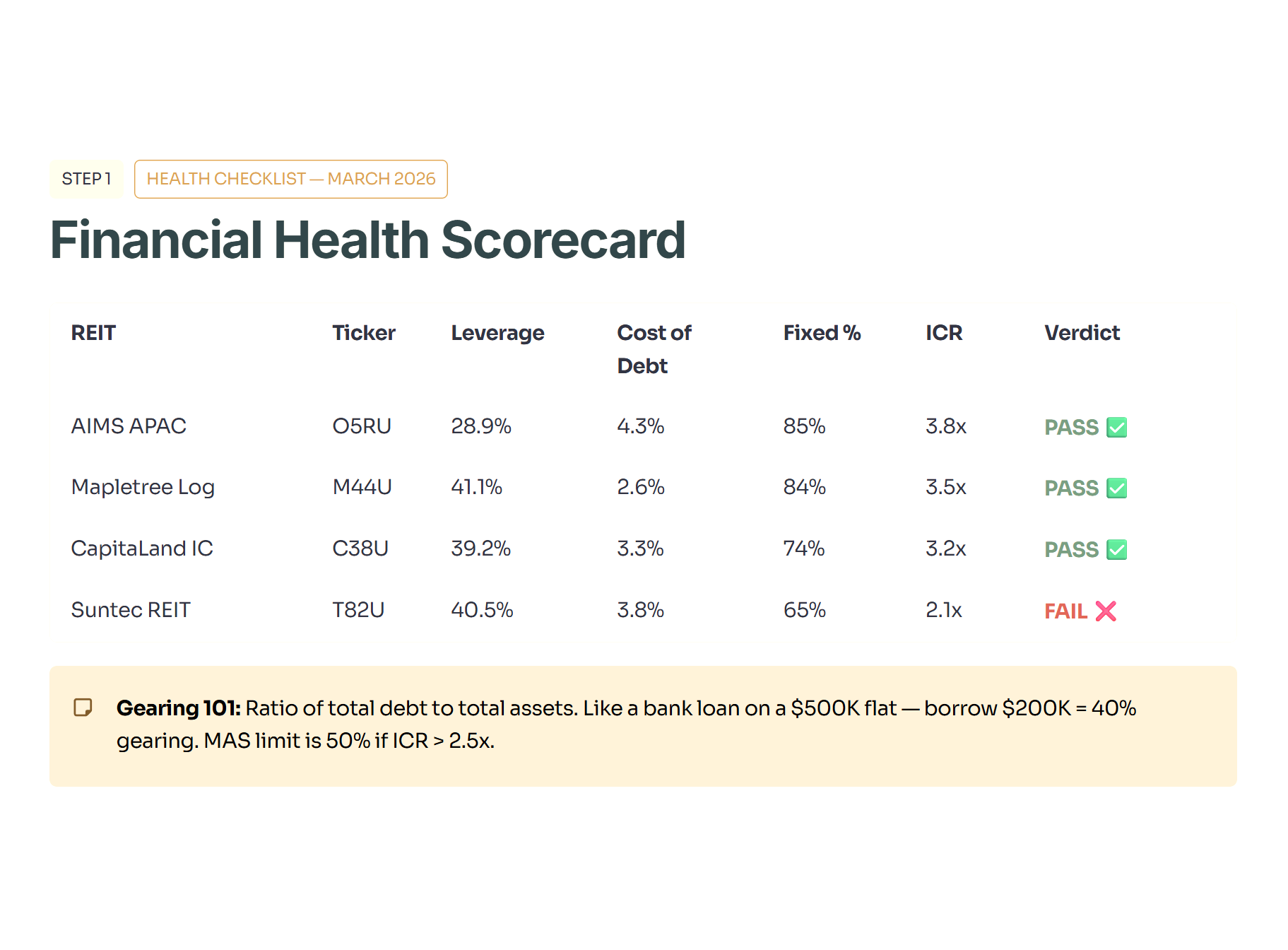

Step One: The Health Check

Can these entities survive a high-rate environment where energy costs are cannibalizing cash? We lead with Gearing and Interest Coverage—the twin pillars of survival.

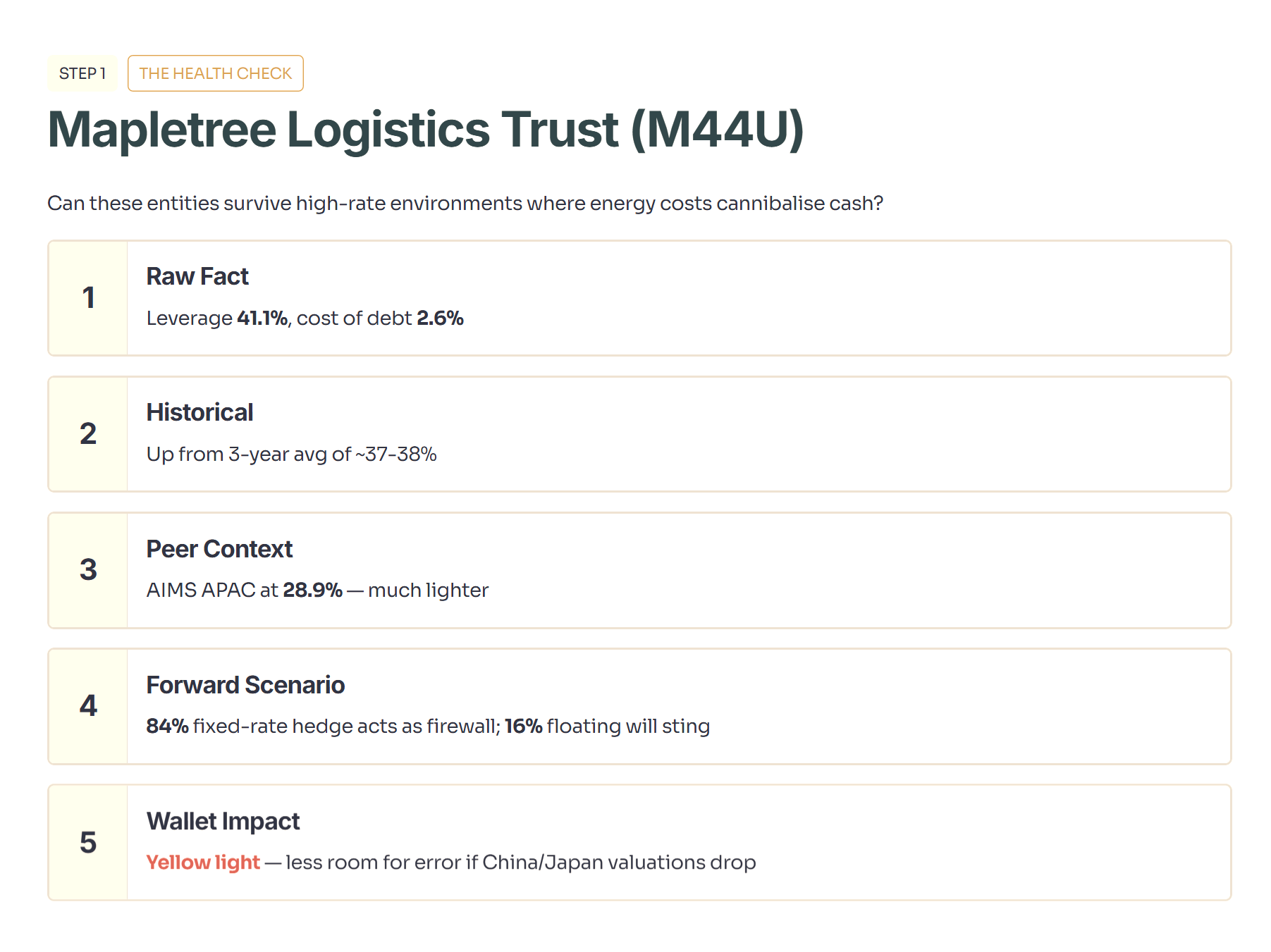

Mapletree Logistics Trust (M44U)

Layer one — Raw Fact: The aggregate leverage stands at forty-one point one percent with an average cost of debt at two point six percent.

Layer two — Historical Benchmark: This is a step up from its three-year average of approximately thirty-seven to thirty-eight percent, reflecting the acquisition hunger of previous years.

Layer three — Peer Context: Compared to AIMS APAC REIT at twenty-eight point nine percent, this trust is running a significantly heavier pack.

Layer four — Forward Scenario: If interest rates rise ten percent from here, the sixteen percent of debt on floating rates will sting, but the eighty-four percent fixed-rate hedge acts as a thick firewall.

Layer five — Wallet Impact: For a fifty-year-old Singaporean investor, this gearing is the yellow light on the dashboard. There is less room for error if property valuations in China or Japan take a haircut.

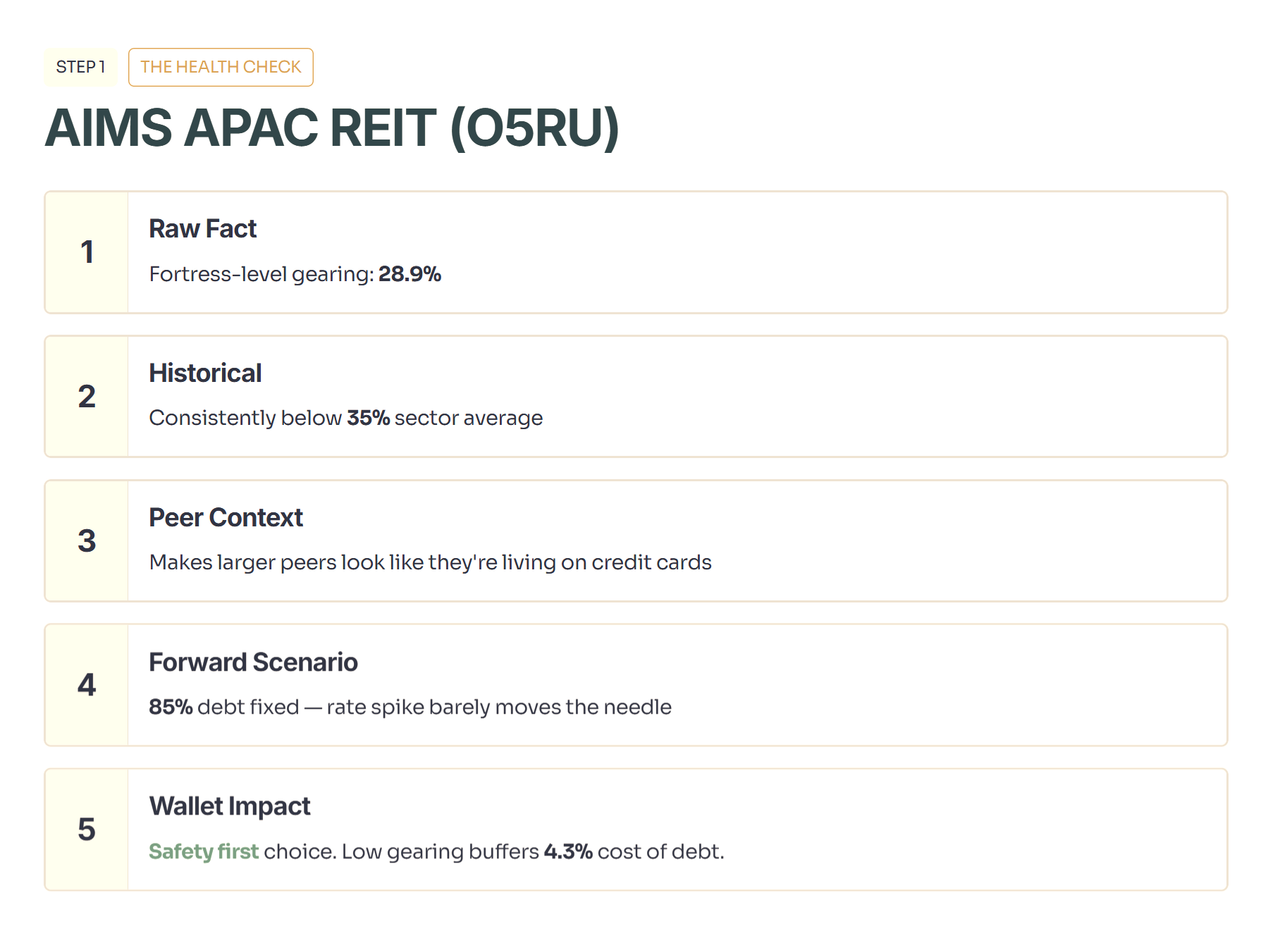

AIMS APAC REIT (05RU)

Layer one — Raw Fact: This entity maintains a forty-fortress-level gearing of twenty-eight point nine percent.

Layer two — Historical Benchmark: This is consistently below the thirty-five percent sector average for industrial trusts.

Layer three — Peer Context: It makes larger peers look like they are living on credit cards.

Layer four — Forward Scenario: With eighty-five percent of debt fixed, a ten percent spike in rates barely moves the needle.

Layer five — Wallet Impact: This is the safety first choice for long-term portfolios. The low gearing is a buffer against the four point three percent cost of debt.

Financial Health Checklist (March 2026)

Educational Note: Gearing

Gearing is the ratio of a trust’s total debt to its total assets. Think of it like taking a bank loan to buy a flat. If the flat costs five hundred thousand dollars and you borrowed two hundred thousand dollars, your gearing is forty percent. In Singapore, the Monetary Authority limit is fifty percent if interest coverage is above two point five times.

🦎 Iggy’s Insight: The Fortress of Solitude

“AIMS APAC REIT is currently the Fortress of the industrial sector. While others are flirting with the forty percent gearing level, they are sitting pretty at twenty-eight point nine percent. In a world where Brent Crude is heading for eighty dollars, having a balance sheet this clean is like having a reserved seat at the hawker centre during peak lunch hour. They have the dry powder for a forensic entry into assets at a discount. In a storm, you want to be on the ship with the thickest hull, not the most flashy sails.”

“Balance-sheet survival is only half the game—next I’m going to show you the CPF hurdle math that exposes which ‘high yield’ REIT is a dividend mirage, and which one is actually paying you with real fuel.”