Why The "Strong SGD" is Crushing Wilmar (Translation Lag)

Why the SGD’s 11-Year High Creates a “Death Zone” for Exporters and a “FOMO Trap” in Wilmar.

1. The Currency Trap & The “Sucker’s Rally”

The headlines are celebrating. On January 26, the Singapore Dollar smashed through an 11-year ceiling, trading at 1.2678 against the Greenback. The Straits Times Index (STI) is flirting with the psychological 5,000-point barrier.

To me, it looks like a trap.

We are seeing a violent bifurcation in the market. While domestic powerhouses feast on cheaper imports, global exporters are seeing their margins evaporated by FX translation losses. But here is the twist: The market is ignoring the math.

Take Wilmar International. It just surged 4.5% to a 52-week high of S$3.50, driven by pure adrenaline. The retail crowd sees a green candle and chases it. I see an RSI flashing “Overbought” and a price that has detached from reality.

Today, we strip away the euphoria and audit three blue chips—Genting Singapore, Wilmar International, and Singapore Airlines. One is a fortress, one is a death trap, and one is a “take profit” candidate for the disciplined investor.

In This Article:

Concept Deep Dive: The “Translation Lag”

The Iggy Audit: The Diagnosis

The Forensic Evidence: Following the Cash

The Future Multiverse

InvestingPro Reality Check

Iggy's Verdict🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

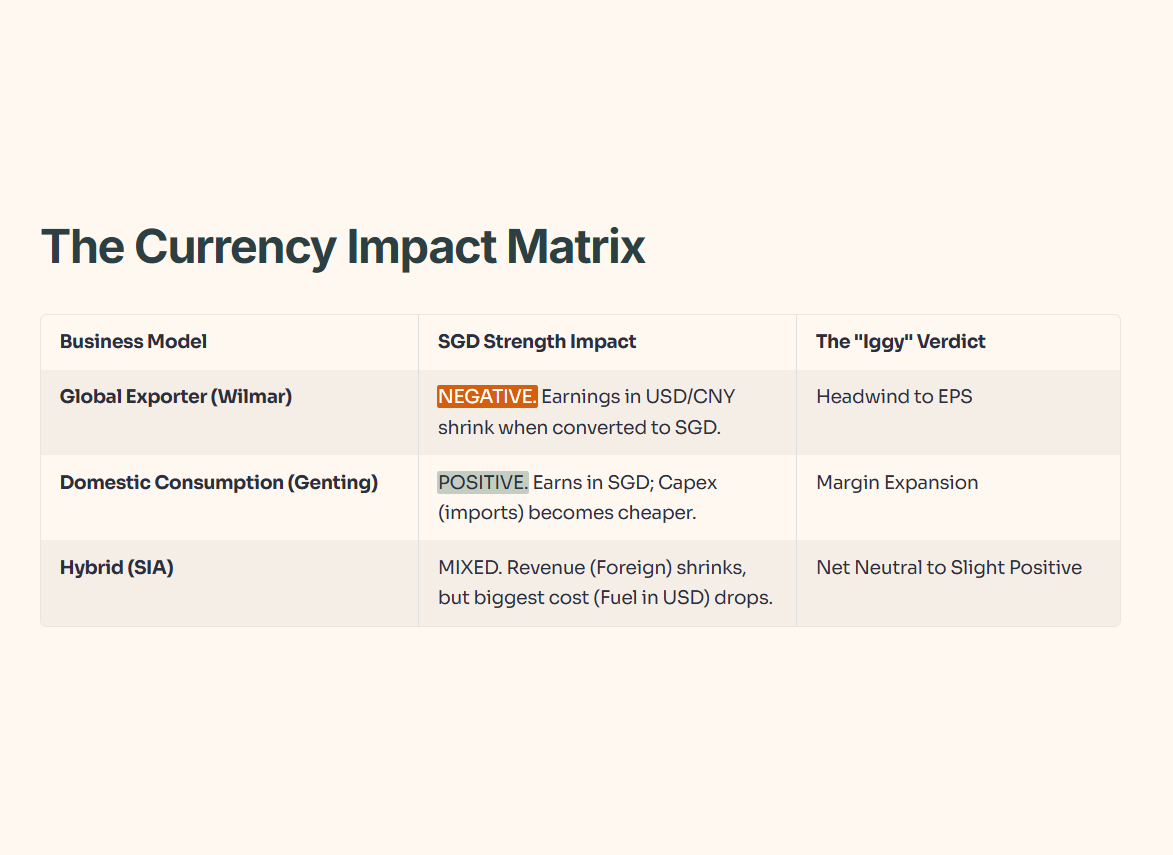

3. Concept Deep Dive: The “Translation Lag”

Before we touch a single stock, you need to understand the mechanism that is currently distorting earnings. When the SGD strengthens by 6% (as it has YTD), it creates the “Exporter’s Mismatch.”

If a company sells palm oil in USD but pays dividends in SGD, a 6% currency swing effectively wipes out 6% of their top-line revenue before they’ve sold a single extra tonne of product. Conversely, companies with heavy USD-denominated expenses (like jet fuel or construction materials) get a “discount.”

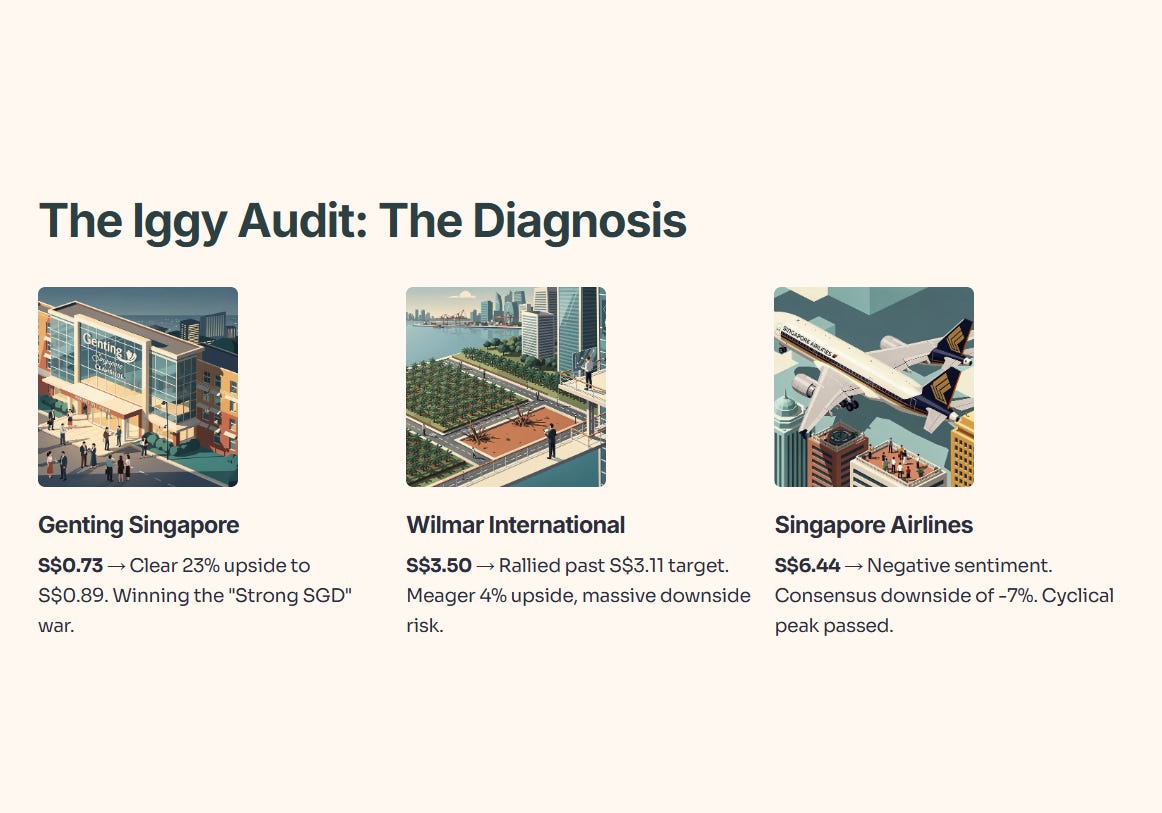

4. The Iggy Audit: The Diagnosis

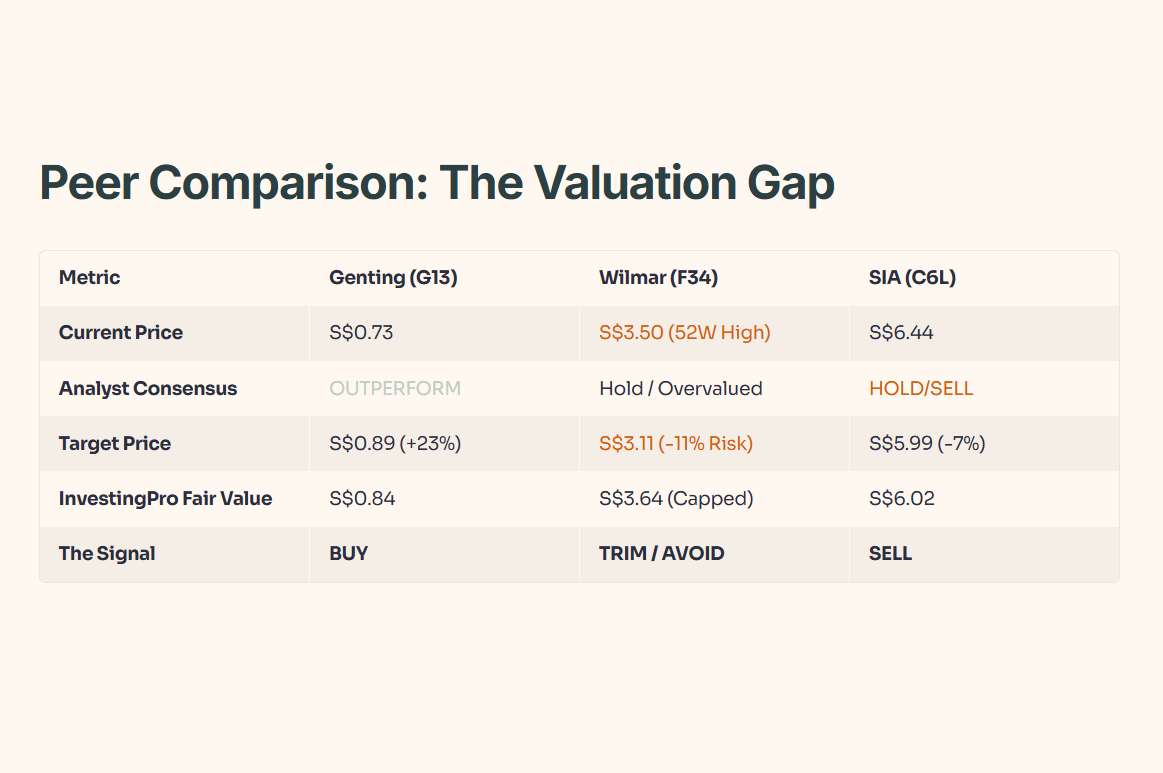

Let’s look at the battlefield. We have three giants, but their valuations tell three very different stories.

Genting Singapore is the only one making sense. Trading at S$0.73, it offers a clear 23% upside to the S$0.89 consensus target. It is winning the “Strong SGD” war because its costs (construction materials for RWS 2.0) are getting cheaper while its revenue is in SGD.

Wilmar International is where the danger lies. It has rallied to S$3.50, blowing past the average analyst target of S$3.11. The “InvestingPro Fair Value” is S$3.64, leaving you a meager 4% upside against massive downside risk. You are picking up pennies in front of a steamroller.

Singapore Airlines remains the sick man of the group. With negative sentiment and a consensus downside of -7%, it is priced for a cyclical peak that has already passed.

The Synthesis:

Winner: Genting Singapore. It is the only stock where price appreciation (+23% potential) aligns with yield.

Loser: Wilmar. Why buy at S$3.50 when the smartest analysts in the room think it’s worth S$3.11? The “Value” window has closed.

5. The Forensic Evidence: Following the Cash

Now, we open the books. This is where the narrative of “high yield” often falls apart.

The Wilmar “Health Warning”

The latest data paints a concerning picture for Wilmar. While the price is hitting highs, the engine room is sputtering.

Weak Margins: The dashboard explicitly flags that Wilmar “Suffers from weak gross profit margins.” In an inflationary world, 1.7% margins leave zero room for error.

The RSI Signal: The RSI is currently flashing “Overbought”. Statistically, when a low-margin cyclical stock hits an RSI peak at a 52-week high, a pullback is imminent.

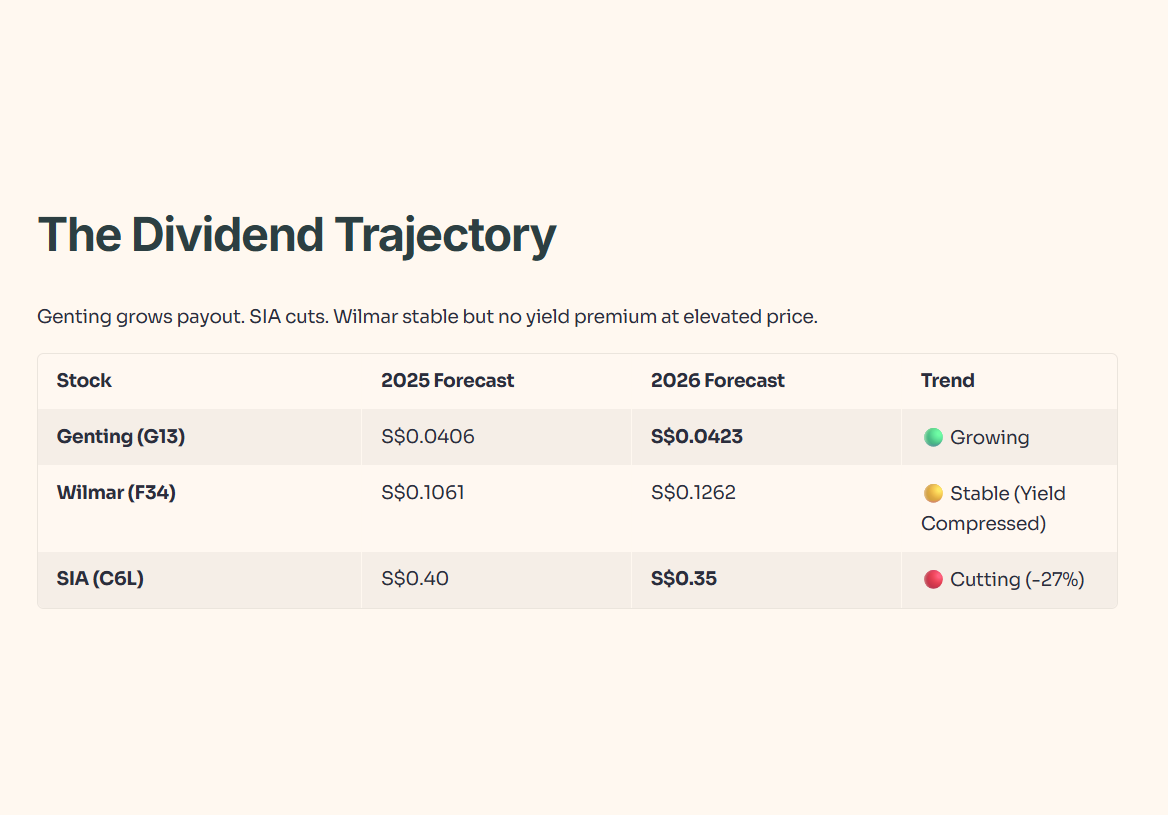

The Dividend Argument

Genting is actively growing its payout. SIA is cutting theirs. Wilmar is stable but offers no yield premium at this elevated price.

The Financial Health Checklist: The “FOMO” Warning

If you look beneath the hood, the divergence in financial health is startling. Genting Singapore is operating with a robust 22.88% profit margin, a fortress-like buffer that allows it to fund its expansion while maintaining a healthy fair value upside. Contrast that with Wilmar International, where the current rally masks a critical weakness: razor-thin margins of just 1.71%. When a company with such negligible room for error hits an “Overbought” technical status and trades with less than 4.0% upside to its fair value cap, it stops being an investment and becomes a “FOMO Trap.” Meanwhile, Singapore Airlines remains in the “Cautious” zone, with depressed margins and an overvalued profile that simply cannot justify chasing the yield. In short: Genting has the cash flow to survive a downturn; Wilmar is priced for perfection it cannot afford; and SIA is running on fumes.