Why a Record Order Book Can Lose You Money (Visibility Fallacy)

Why billions in net cash beats a $32B 'order book' for your SRS and CPF protection.

The order book is at a record high, but the share price is hitting a ceiling. It’s the ultimate “Value Trap” for the retail investor who thinks a big backlog automatically equals a big payday. In the engineering world, a massive order book isn’t a trophy; it’s a liability if you can’t manage costs while trading at an all-time high valuation. If you aren’t looking at the margin expansion trajectory against current fair value, you’re just betting on a company’s ability to stay busy, not its ability to make you rich.

In This Article:

Concept Corner: The Revenue Visibility Fallacy

The Iggy Audit: Engineering a 2026 Turnaround

The Data Fortress: Evidence of Strength

The Scenario Matrix: 2026 Forecast

InvestingPro Reality Check

The Verdict: The Strategy for 2026

About Iggy the Investing Iguana channel

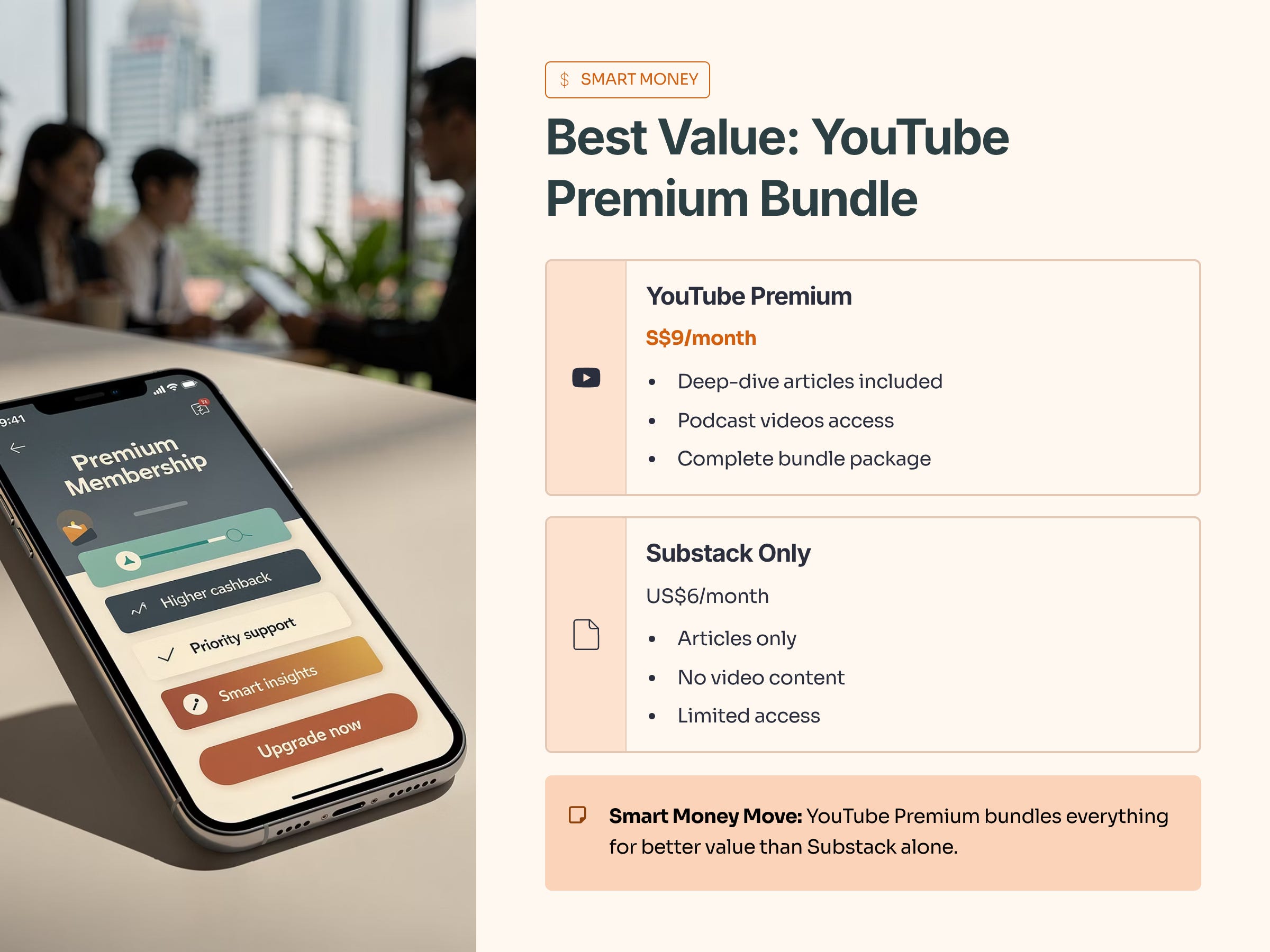

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 5,300 subscribers and an ‘Inner Circle’ of 100+ paid members across YouTube and Substack.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

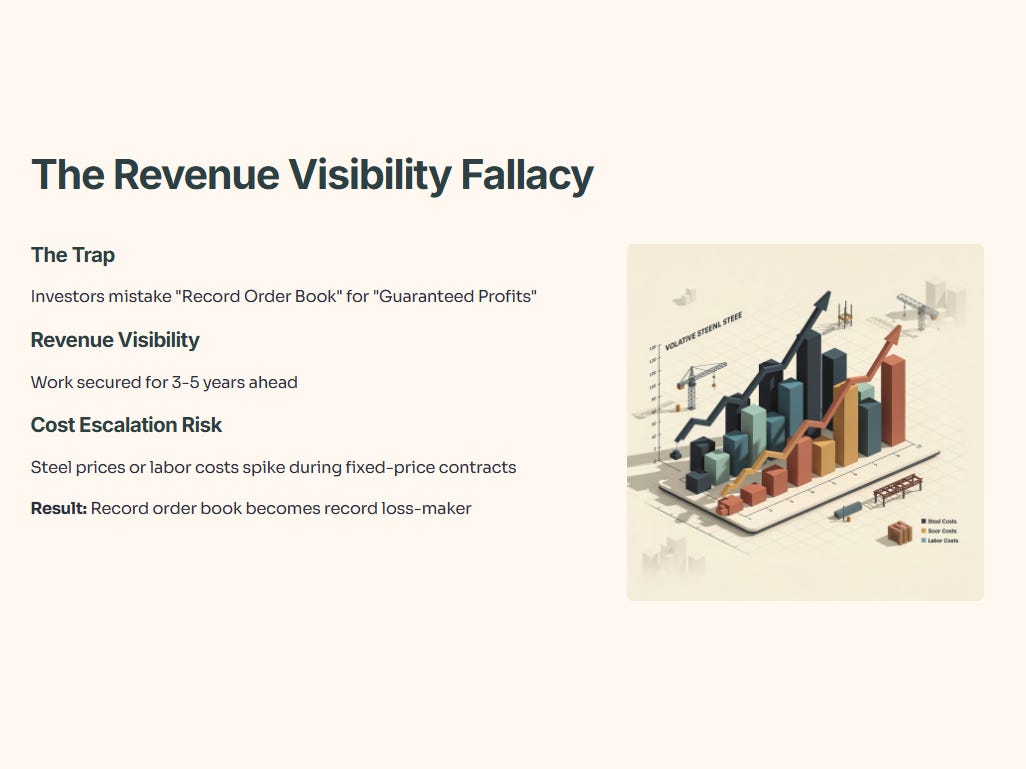

Concept Corner: The Revenue Visibility Fallacy

Investors often mistake a “Record Order Book” for “Guaranteed Profits.” In heavy engineering, this is known as Revenue Visibility. While it tells you the company has work for the next 3-5 years, it doesn’t account for Cost Escalation Risk. If steel prices or labor costs spike while a company is locked into a fixed-price 5-year contract, that “record order book” becomes a record loss-maker.

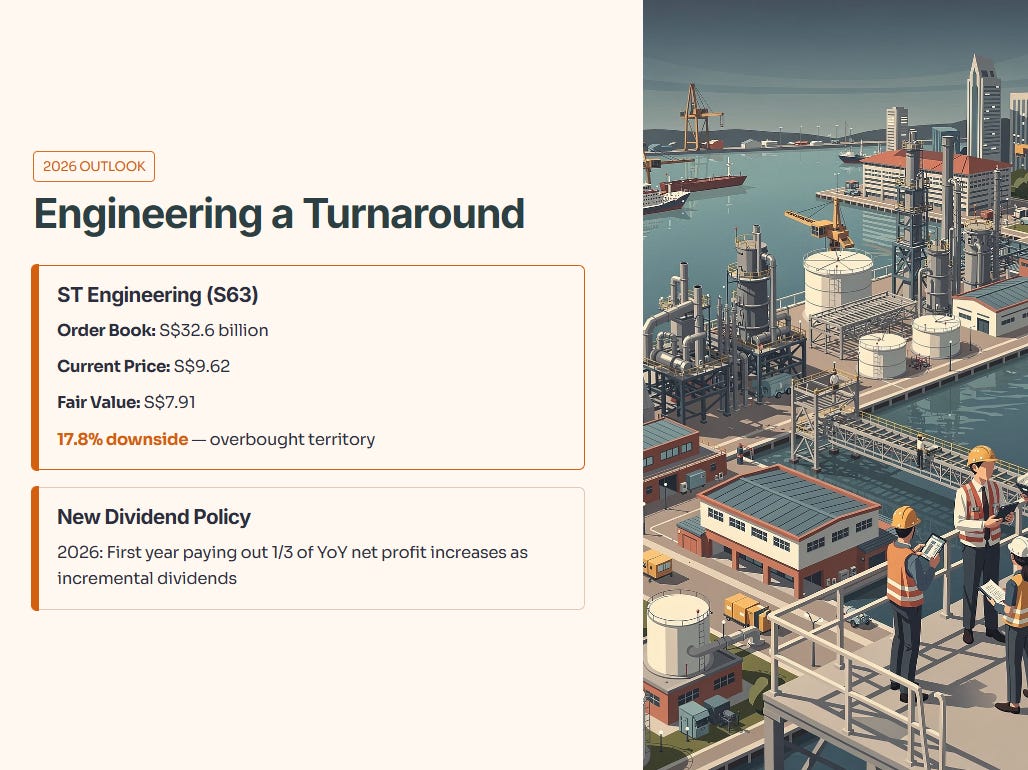

The Iggy Audit: Engineering a 2026 Turnaround

The “Smart Money” is quietly rotating into Singapore’s engineering giants, but they are being selective.

ST Engineering (SGX: S63) is hitting resistance. While its S$32.6 billion order book is impressive, the stock is currently in overbought territory. Its InvestingPro Fair Value sits at S$7.91, suggesting a 17.8% downside from the current price of S$9.62. 2026 will be the first year of its new dividend policy—paying out a third of year-on-year net profit increases as incremental dividends.

Yangzijiang Shipbuilding (SGX: BS6) is the real value play right now. Trading at S$3.50, it has an **18.4% upside** to its InvestingPro Fair Value of **S$4.14**. With shipbuilding margins reaching a record 35% in 1H2025 and a net cash position of RMB 18.3 billion, it is fundamentally stronger than its peers.

Peer Comparison Table (2026 Estimates)

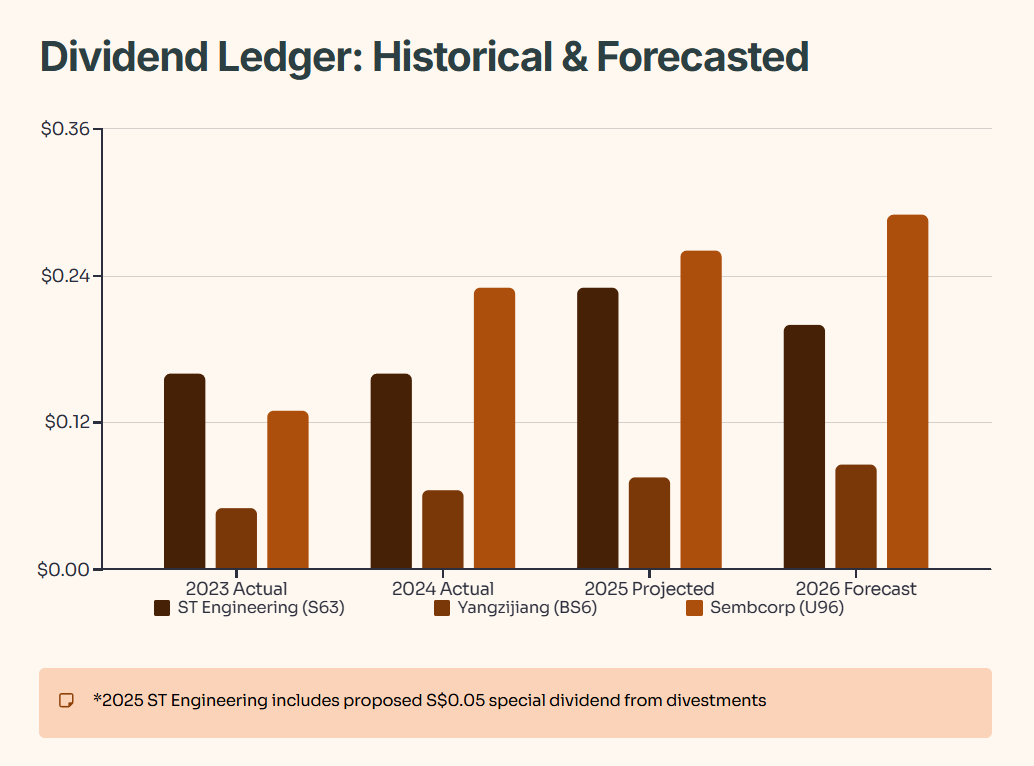

The Data Fortress: Evidence of Strength

Engineering stocks are only as good as their ability to pay you while you wait for projects to convert to cash.

Dividend Ledger (Historical & Forecasted)

*Includes proposed S$0.05 special dividend from divestments.

Financial Health Checklist (Pass/Fail)

The Scenario Matrix: 2026 Forecast