The November Shockwave: Why SIA Crashed, UOB “Kitchen Sinked,” and The 350-Basis Point Opportunity

Every Singapore investor is asking the same questions this week: “Why did SIA stumble just as Genting skyrocketed? Is the 72% profit drop at UOB a disaster? And where do I hide my cash for 2026?”

Let’s be honest: November’s earnings season was a wake-up call. The rising tide that lifted all boats in early 2024 has receded, exposing the rocks beneath.

We saw Singapore Airlines (SIA) report a stunning 67.8% plunge in net profit. We saw Genting Singapore post a 19% profit jump despite a shaky global economy. We saw UOB take massive provisions that scared the daylights out of retail traders. And quietly, ST Engineering just proved why boring is beautiful.

If you’re confused, you’re paying attention. But chaos creates opportunity—if you understand the story behind the numbers.

Here is the deep-dive analysis you won’t get on the evening news.

In This Article:

• Part 1: The Bank Divergence—Why “Net Profit” Is A Lie

• Part 2: The “Re-Opening” Trap—SIA vs. Genting

• Part 3: The Industrial Shield—ST Engineering

• Part 4: The “Fat Pitch”—REITs vs. The 10-Year Bond

• The Investing Iguana Playbook (2026 Edition)

Part 1: The Bank Divergence—Why “Net Profit” Is A Lie

The headline news was terrifying: UOB reported a Q3 net profit of just S$443 million—a roughly 72% drop year-on-year. If you only read the headlines, you would have panic-sold. But if you looked closer, you would see that the “disaster” was actually a strategic masterstroke.

UOB isn’t losing money because borrowers are defaulting today; they are stockpiling cash because they think borrowers might default tomorrow. They took a massive S$1.36 billion allowance for credit losses—a move we call “Kitchen Sinking.” They effectively took all the potential bad news at once to clear the decks for 2026.

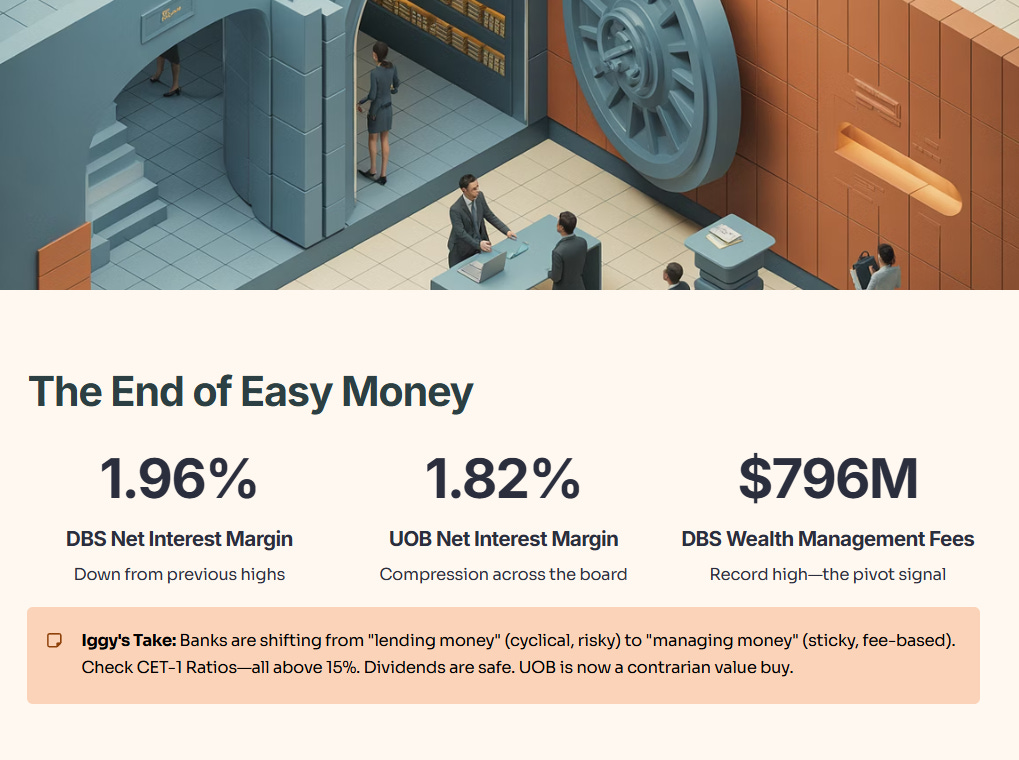

While DBS and OCBC remained steady ships, the real story across all three banks is the end of the easy money era. We are seeing Net Interest Margin (NIM) Compression across the board, with DBS dropping to 1.96% and UOB to 1.82%. The “Free Cash Flow” party driven by high interest rates is over.

Iggy’s Take: Don’t fear the drop; follow the pivot. Banks are aggressively shifting from “lending money” (which is cyclical and risky) to “managing money” (which is sticky and fee-based). DBS hitting a record S$796 million in wealth management fees is the signal. If you hold banks in your SRS account, ignore the headline profit drop. Check the CET-1 Ratios (all above 15%)—the dividends are safe. UOB is now a contrarian value buy for long-term holders who understand that the “loss” was an accounting cushion, not a cash burn.

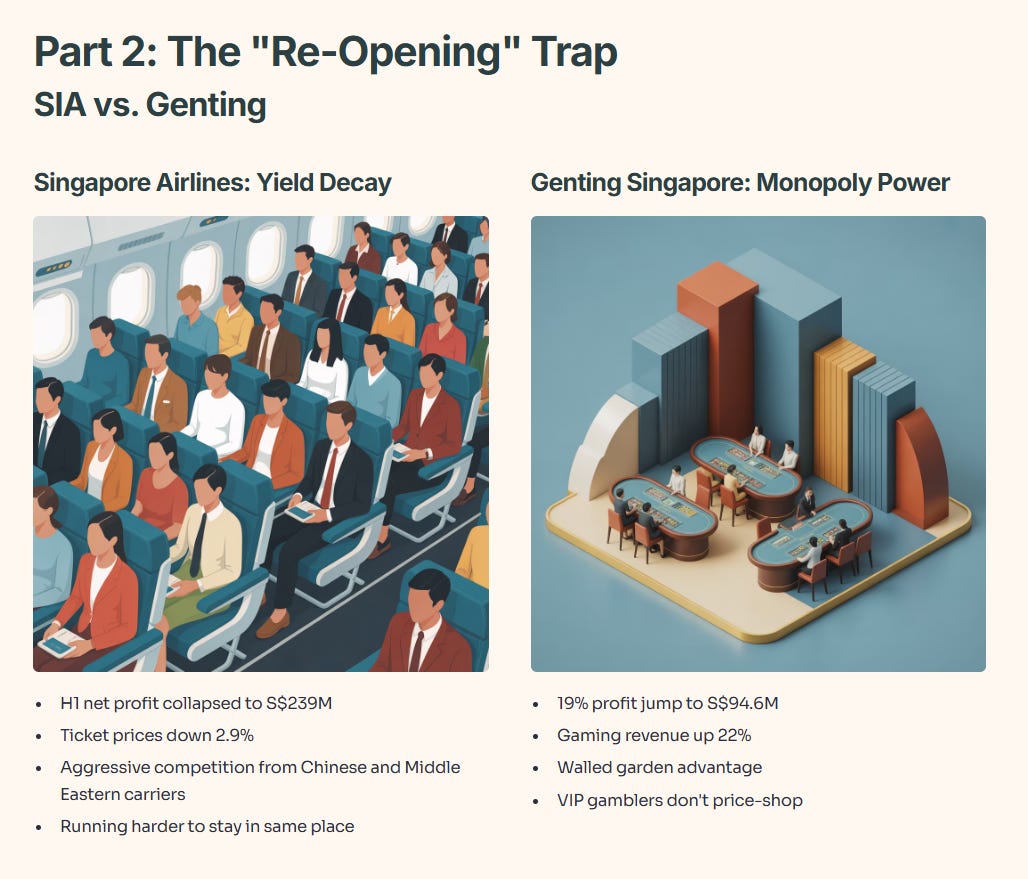

Part 2: The “Re-Opening” Trap—SIA vs. Genting

This month offered the most critical lesson of the year on pricing power. Both SIA and Genting rely on tourism, yet one crashed while the other soared. The difference lies in who controls the price.

SIA is suffering from Yield Decay. Despite revenue hitting a record high, their H1 net profit collapsed to S$239 million. The culprit isn’t demand—planes are fuller than ever. The culprit is competition. Aggressive capacity increases from Chinese and Middle Eastern carriers have forced ticket prices down by 2.9%, while costs for fuel and staff have risen. SIA is effectively running harder just to stay in the same place.

Genting Singapore, conversely, is enjoying Monopoly Power. Their 19% profit jump to S$94.6 million wasn’t an accident. Resorts World Sentosa operates in a “walled garden.” Unlike economy passengers who price-shop flights on Skyscanner, VIP gamblers don’t price-shop casinos. Genting was able to raise its “win rate” and gaming revenue by 22% because they cater to a captive, luxury audience.

Iggy’s Take: In 2026, you must avoid businesses fighting price wars. SIA is locked in a brutal dogfight for every passenger. Genting owns the arena. The broad “Re-Opening Trade” is dead; the “Luxury Pricing Trade” is the only one left alive.

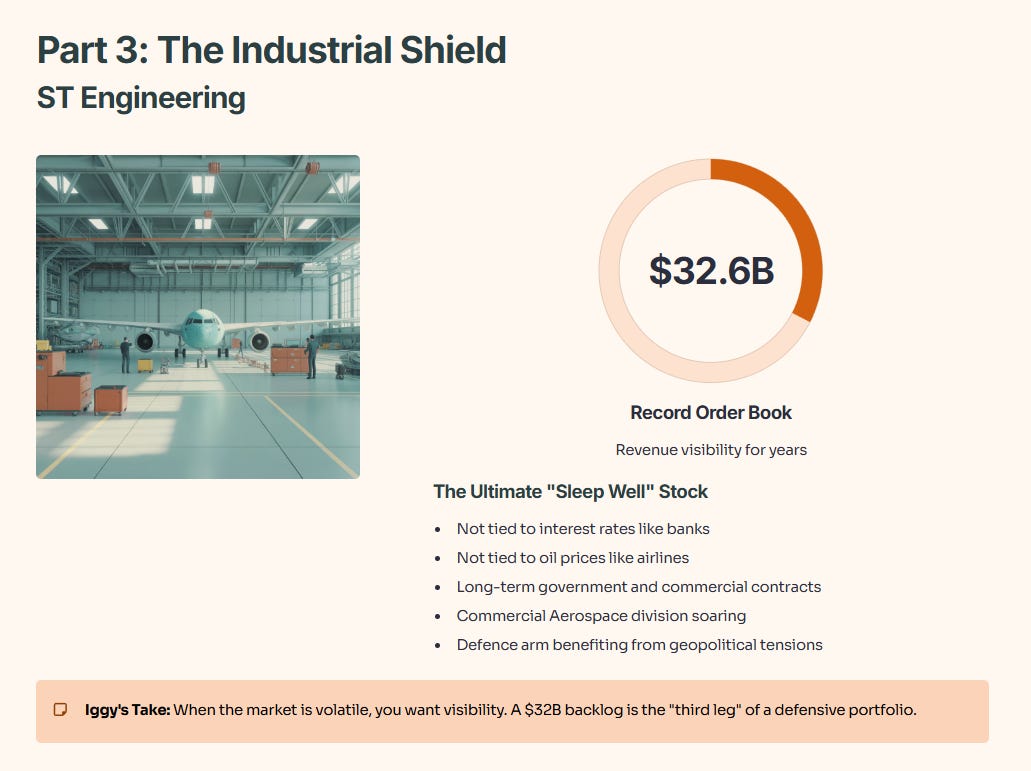

Part 3: The Industrial Shield—ST Engineering

While the market obsessed over the volatility in banks and airlines, ST Engineering quietly delivered the kind of boring, robust news that defensive investors dream of. They just reported a record order book standing at a staggering S$32.6 billion.

This is the ultimate “Sleep Well” stock. Unlike banks that are tied to interest rates, or airlines tied to oil prices, ST Engineering is anchored by long-term government and commercial contracts. Their Commercial Aerospace division is soaring as airlines (like SIA) are forced to spend heavily on maintenance to keep older planes flying, and their Defence arm is benefiting from rising geopolitical tensions.

Iggy’s Take: When the market is volatile, you want visibility. A $32 billion backlog gives you revenue visibility for years, not just quarters. This is the “third leg” of a defensive portfolio—balancing out the financial and tourism risks with pure industrial stability.

Part 4: The “Fat Pitch”—REITs vs. The 10-Year Bond

For the last two years, REITs were “dead money.” It made no sense to take the risk of owning a mall when you could get a risk-free 4% yield from a 6-month T-bill. But in the last few weeks, that math has flipped violently.

As of mid-November 2025, the 10-year Singapore Government Bond yield has crashed to ~1.95%.

This has created a massive opportunity. High-quality REITs are still yielding between 5.5% and 6.0%. That means the “yield spread”—the extra cash you get for taking on risk—is now hovering around 355 basis points. Historically, whenever the spread widens past 300bps, REITs tend to significantly outperform the market over the next 12 months.

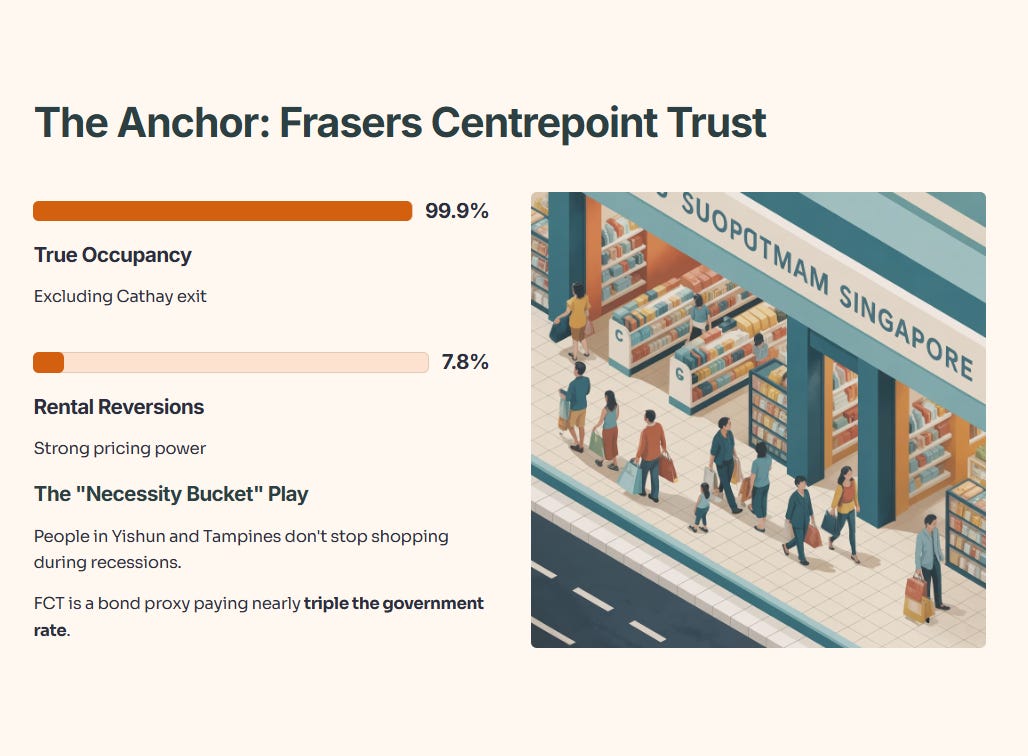

The Anchor: Frasers Centrepoint Trust (FCT) FCT recently posted a retail committed occupancy of 98.1%, but that figure is misleading. It includes the exit of Cathay Cineplexes. Excluding that single tenant, their occupancy is a rock-solid 99.9%. With rental reversions at +7.8%, this is a “necessity bucket” play. People in Yishun and Tampines don’t stop shopping because of a recession. With the 10-year yield below 2%, FCT is effectively a bond proxy paying you nearly triple the government rate.

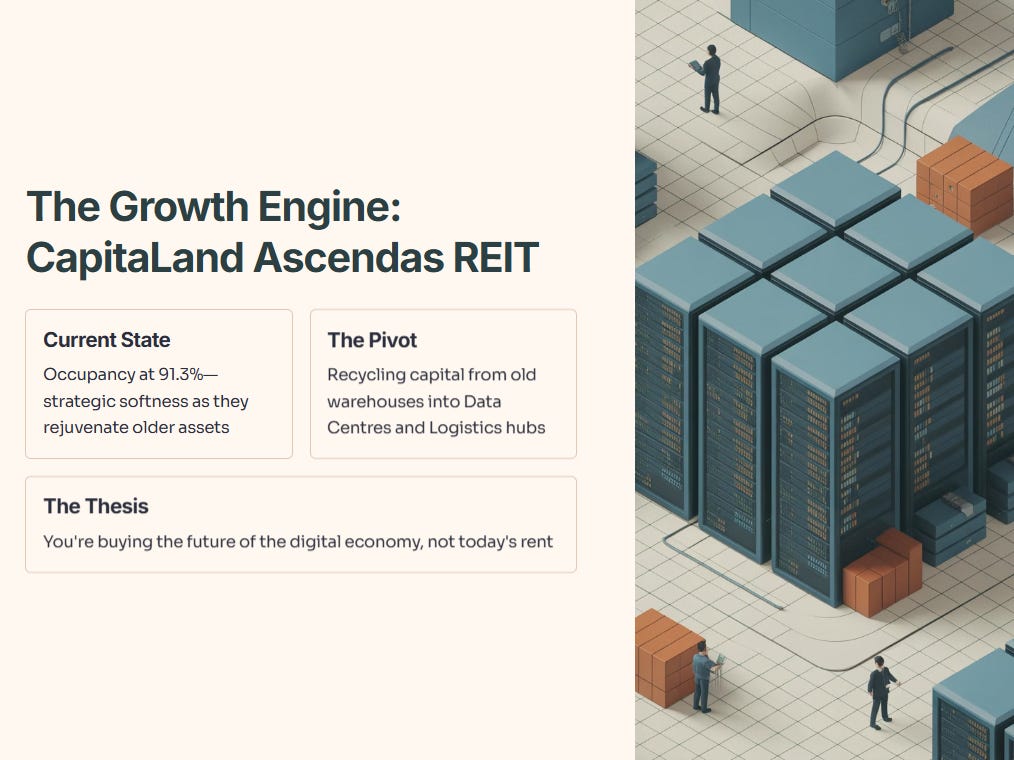

The Growth Engine: CapitaLand Ascendas REIT (CLAR) CLAR’s occupancy dipped slightly to 91.3%, but this is a strategic “softness” as they rejuvenate older assets. You aren’t buying CLAR for today’s rent; you are buying it for the pivot to the digital economy. As they recycle capital from old warehouses into Data Centres and Logistics hubs, they are future-proofing the portfolio.

The Investing Iguana Playbook (2026 Edition)

We are moving from a “Growth” cycle to a “Quality” cycle. Here is how I am positioning the portfolio: