The "Old Keppel" is Dead: The 72% Signal You Missed

The market still prices Keppel like a rig builder. Here is why the shift to Asset Management makes it a prime candidate for your CPF portfolio.

Most Singaporean investors have a “mental legacy” problem with Keppel Ltd (SGX: BN4).

When you hear the name, you likely think of oil rigs, lumpy contracts, and corruption scandals in Brazil. You think of a conglomerate that moves with the price of crude oil.

If that is your mental model, you are looking at a ghost. That company doesn’t exist anymore.

While the retail market was distracted by bank yields and REIT consolidations, Keppel executed a surgical pivot. They didn’t just sell off their offshore marine business; they fundamentally changed how they make money.

The result? A boring, predictable, fee-earning machine that is trading at a valuation that hasn’t caught up to reality yet.

In This Article:

• The Mechanics: The “Capital Recycling” Flywheel

• The Three Engines: It’s Not Just Property

• 1. Infrastructure: Boring is Beautiful

• 2. Connectivity: The AI Play

• 3. Real Estate: The “Aermont” Factor

• The “Uncle” Test: Addressing the Dividend (3.3%)

• The Valuation Disconnect

• Conclusion: The “Sleep Well” Growth Stock?

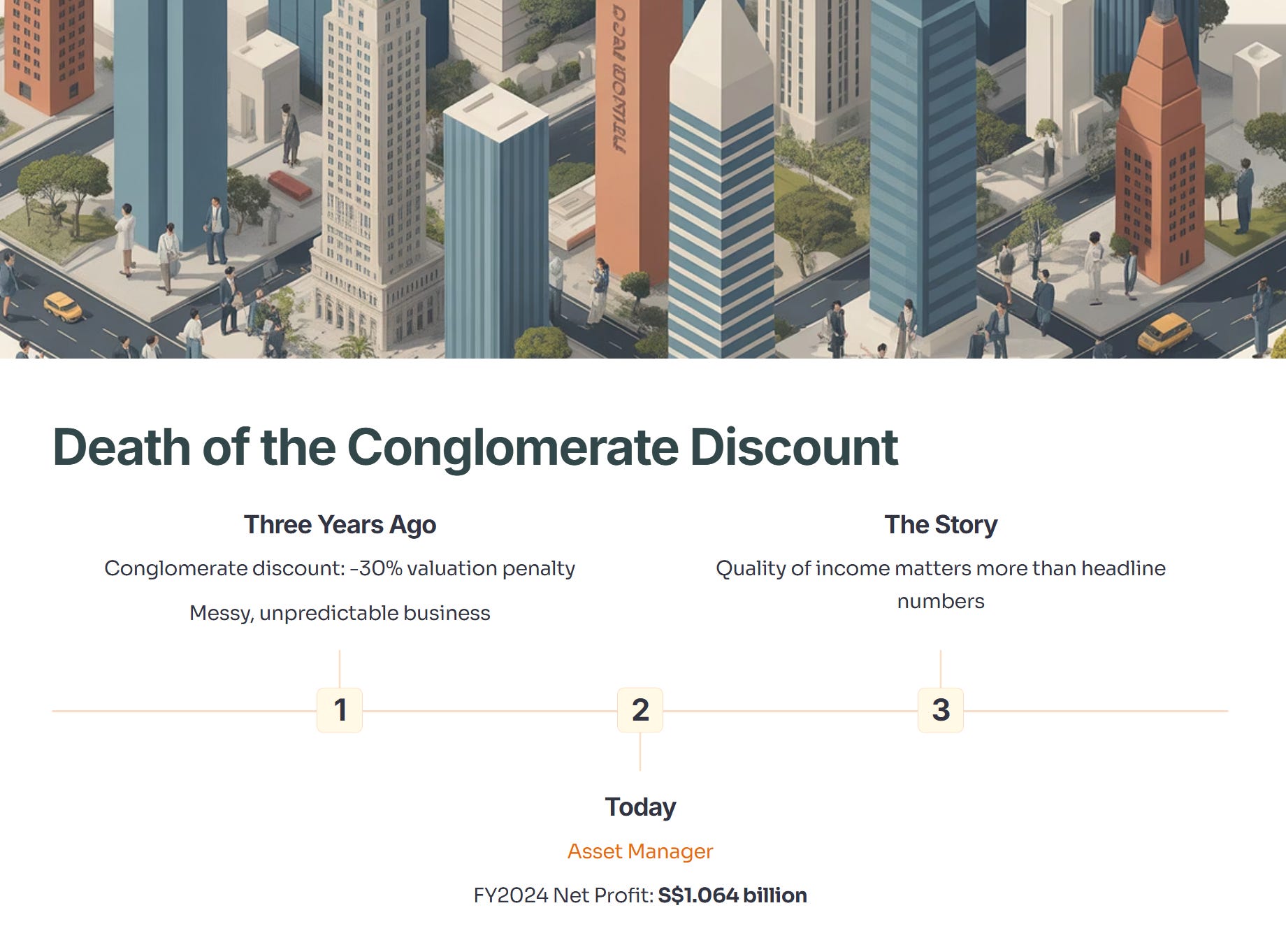

The Death of the Conglomerate Discount

Three years ago, Keppel suffered from the “Conglomerate Discount.” Investors took the sum of its parts and subtracted 30% because the business was messy and unpredictable.

Today, the “New Keppel” is an asset manager.

By the end of FY2024, Keppel reported Net Profit from continuing operations of S$1.064 billion. But the headline number isn’t the story. The quality of that income is the story.

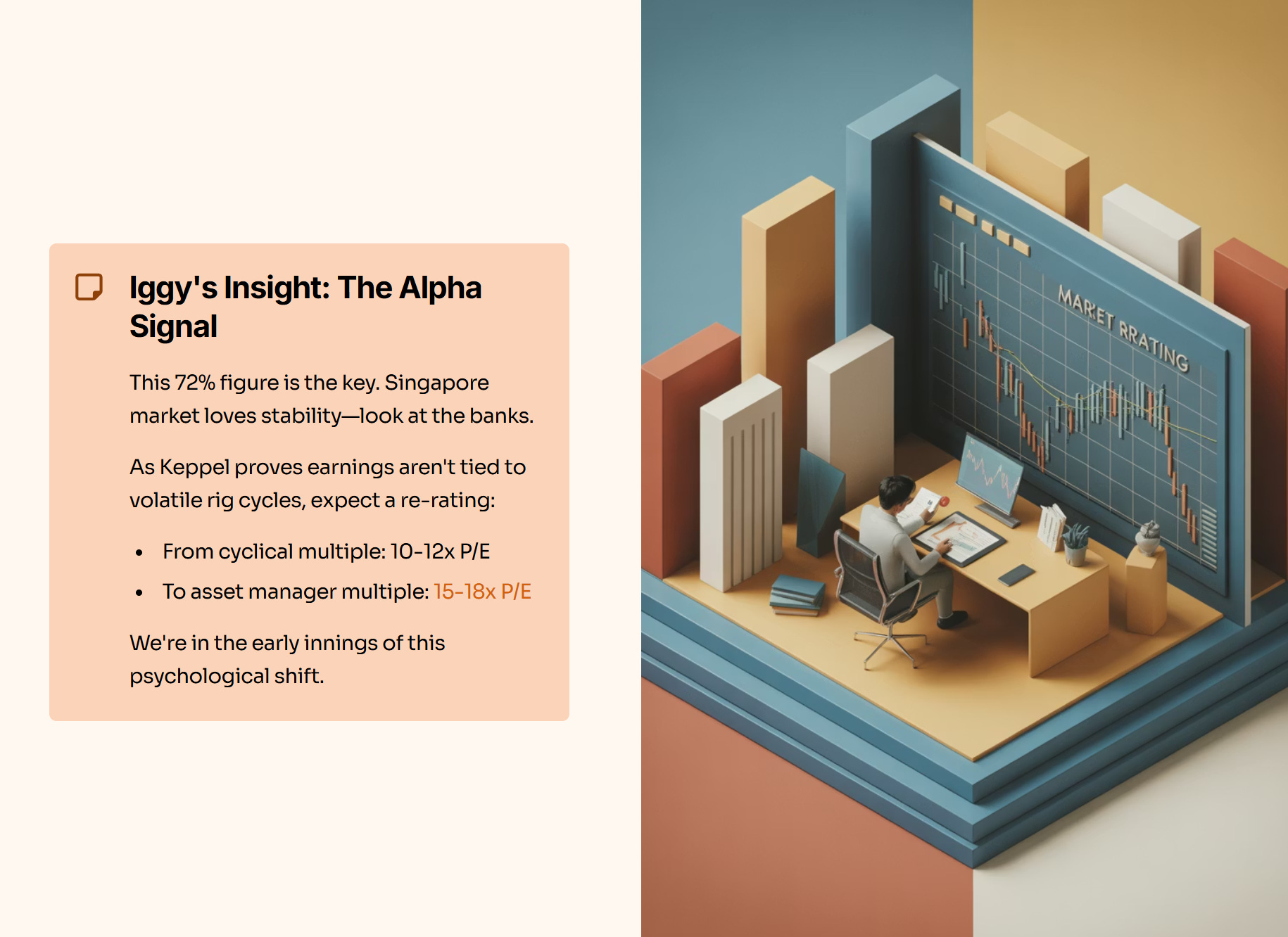

Recurring income now makes up 72% of net profit.

In 2021, that number was just 21%. This is the single most important metric for long-term investors. “Old Keppel” had to hunt for new contracts every January 1st to survive. “New Keppel” starts the year with hundreds of millions in management fees locked in.

Iggy’s Insight:

This 72% figure is the “Alpha” signal. The Singapore market loves stability (look at the banks). As Keppel proves that its earnings are no longer tied to the volatile cycle of rig building, the market will eventually re-rate the stock from a cyclical multiple (10-12x P/E) to an asset manager multiple (15-18x P/E). We are in the early innings of this psychological shift.

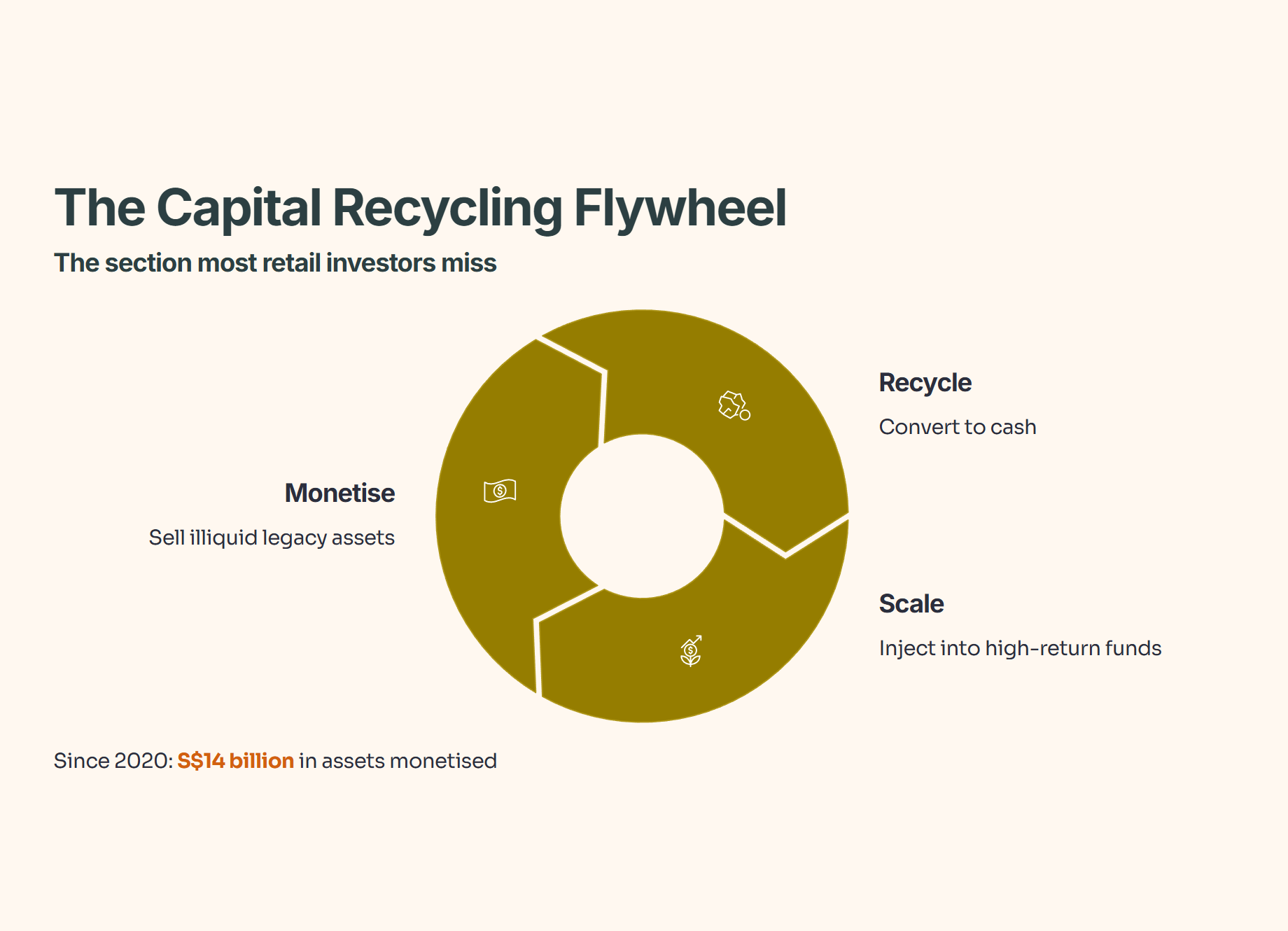

The Mechanics: The “Capital Recycling” Flywheel

This is the section most retail investors miss.

Keppel isn’t just holding assets; it is aggressively churning them. The strategy is simple but ruthless: Monetise -> Recycle -> Scale.

Since 2020, they have monetised over S$14 billion in assets. They take illiquid legacy assets (like old shipyards or non-core property), sell them, and inject that cash into high-return funds like their data centre or private credit funds.

Why does this matter?

It avoids dilution. Most companies need to issue new shares (Rights Issues) to raise cash for growth, which hurts you, the shareholder. Keppel funds its own growth by selling its own junk.

Iggy’s Insight:

Think of this as “housekeeping for profit.” By moving assets off their own balance sheet and into the funds they manage, they achieve two things:

They get cash upfront.

They earn a recurring management fee on that same asset forever.

It is the ultimate financial alchemy, and it is the engine driving their target of S$200B Funds Under Management (FUM) by 2030.

The Three Engines: It’s Not Just Property

Keppel has reorganized into three integrated divisions. This isn’t just corporate speak; it’s about synergy.

1. Infrastructure: Boring is Beautiful

They have moved from volatile power trading to long-term contracts. By the end of 2024, roughly 70% of Keppel’s power generation capacity is contracted for 3+ years.

The Bull Case: This is now effectively a utility business hiding inside a growth stock.

2. Connectivity: The AI Play

This is the jewel. Between data centres (DCs) and the Bifrost subsea cable, Keppel is owning the “plumbing” of the internet.

The Stats: DC capacity grew from 650 MW to over 1.2 GW planned.

The Moat: They are building Singapore’s first floating data centre. This solves the land scarcity issue and uses seawater for cooling—a competitive advantage that pure-play DC operators cannot easily replicate.

3. Real Estate: The “Aermont” Factor

The acquisition of Aermont Capital (a European manager) was expensive (S$1.4B), but it was strategic. It instantly gave Keppel a foothold in Europe and access to private credit markets. This diversifies them away from the struggling Chinese property market.

The “Uncle” Test: Addressing the Dividend (3.3%)

I get this question constantly: “Iggy, why buy Keppel at 3.3% yield when DBS gives me 6%?”