The Premium Analysis: Venture Corp’s “Upgrade” is a Wake-Up Call, Not a Green Light

Why Most Investors Will Miss the Real Message Behind Venture Corporation’s Latest Move – and How to Turn Uncertainty into Actionable Advantage Across Your SGX Portfolio

If you think Venture’s target price upgrade signals a simple turnaround, think again. In this premium analysis, I rip into the real numbers, decode the risks behind the headline, and offer you a superior framework for reading blue-chip signals in Singapore’s fast-evolving market.

The Premium Analysis: Venture Corp’s “Upgrade” is a Wake-Up Call, Not a Green Light

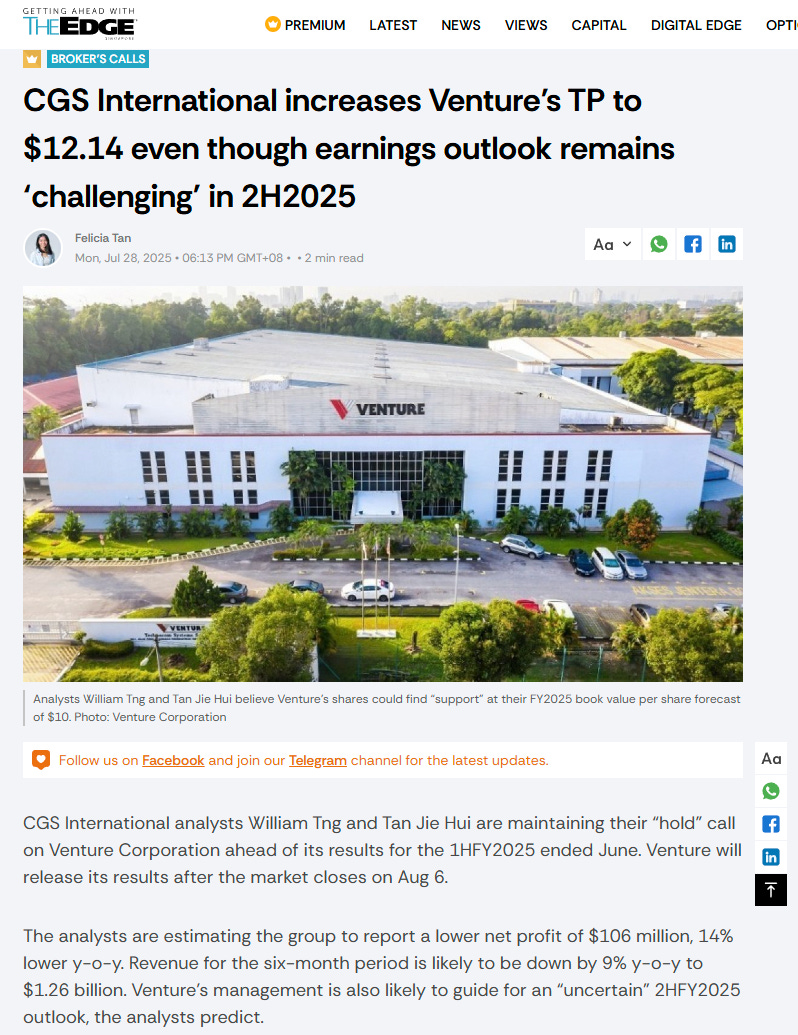

When a household-name blue chip like Venture Corporation appears in every earnings headline, Singaporean investors pay attention. But most walk away missing what actually matters. You might see a higher target price ($12.14 from CGS International), mild analyst optimism, and a stable dividend – and believe the bottom is in. But here’s the truth: these aren’t buy signals in disguise. They’re your cue to go deeper, especially now as SGX blue chips hold near record highs and macro risk clouds are brewing on every horizon.

This post is for discerning Singapore investors who want more than the headlines. If you’re tired of recycled talking points, and want to make sense of Venture’s real outlook as of July 28, 2025, you’re in the right place. We’ll walk through the newest data, what’s moving the price, what big fund managers are actually doing behind the scenes – and what’s next for your money, whether you care about CPF transfers, dividends, or simply avoiding costly mistakes.

Let’s get into the signals that matter – and why now is the best time in years to learn how to interpret corporate action, central bank risk, and SGX blue-chip psychology.