Mapletree Ind vs. Keppel REIT: Is the "AI Tax" Worth It?

The “Boring” money is waking up. As the Fed cuts rates, the window to lock in distressed yields on blue-chip assets is shutting fast—here is the data-driven shortlist for your CPF and SRS capital.

If you’ve been holding cash or sitting in T-Bills for the last two years waiting for the “perfect” bottom, you have likely already missed it. But don’t panic. The pivot has officially started, and for Singaporean investors, this fundamentally changes the math for our dividend portfolios.

The question isn’t if you should buy REITs. The question is: Which ones are actually cheap, and which ones are just “cheap” because they are broken?

If you’re new here, welcome. I’m Iggy, your Singapore-based Private Investor and Market Researcher. Since October 2025, we’ve built a community of over 5,300 investors and produced over 1,300 videos and 400 articles. We are home to a growing ‘Inner Circle’ of over 100 paid members across YouTube and Substack.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

Table of Contents:

The Macro Shift: Why January 2026 is Different

The Screening Criteria: “Boring But Smart”

The High-Yield Heavyweights (>7%)

The Industrial & Logistics Fortresses (5.7% - 6.5%)

The Retail & Diversified Mix

The Playbook: Investor’s Action Plan

The Macro Shift: Why January 2026 is Different

Let’s cut through the noise. In December 2025, the Federal Open Market Committee (FOMC) finally eased the federal funds rate by a quarter percentage point to the 3.5% – 3.75% range.

Why does this matter for your CPF Ordinary Account (OA) or SRS funds? It’s about leverage mechanics.

REITs are essentially pass-through vehicles that rely heavily on debt to acquire properties. When interest rates were high in 2024 and 2025, interest expenses ate directly into Distributable Income (DPU). Now that the cycle has turned, we are looking at two major tailwinds:

Reduced Borrowing Costs: As old interest rate hedges roll off, refinancing becomes cheaper. This stops the bleeding on the bottom line.

Yield Spread Expansion: As risk-free rates (like the Singapore 10Y Bond) drop, the 5-7% yield on REITs becomes significantly more attractive to institutional money. This flow of funds drives share prices up.

However, a rising tide lifts all boats, but it doesn’t plug the leaks in the sinking ones. We need to be selectively aggressive.

The Screening Criteria: “Boring But Smart”

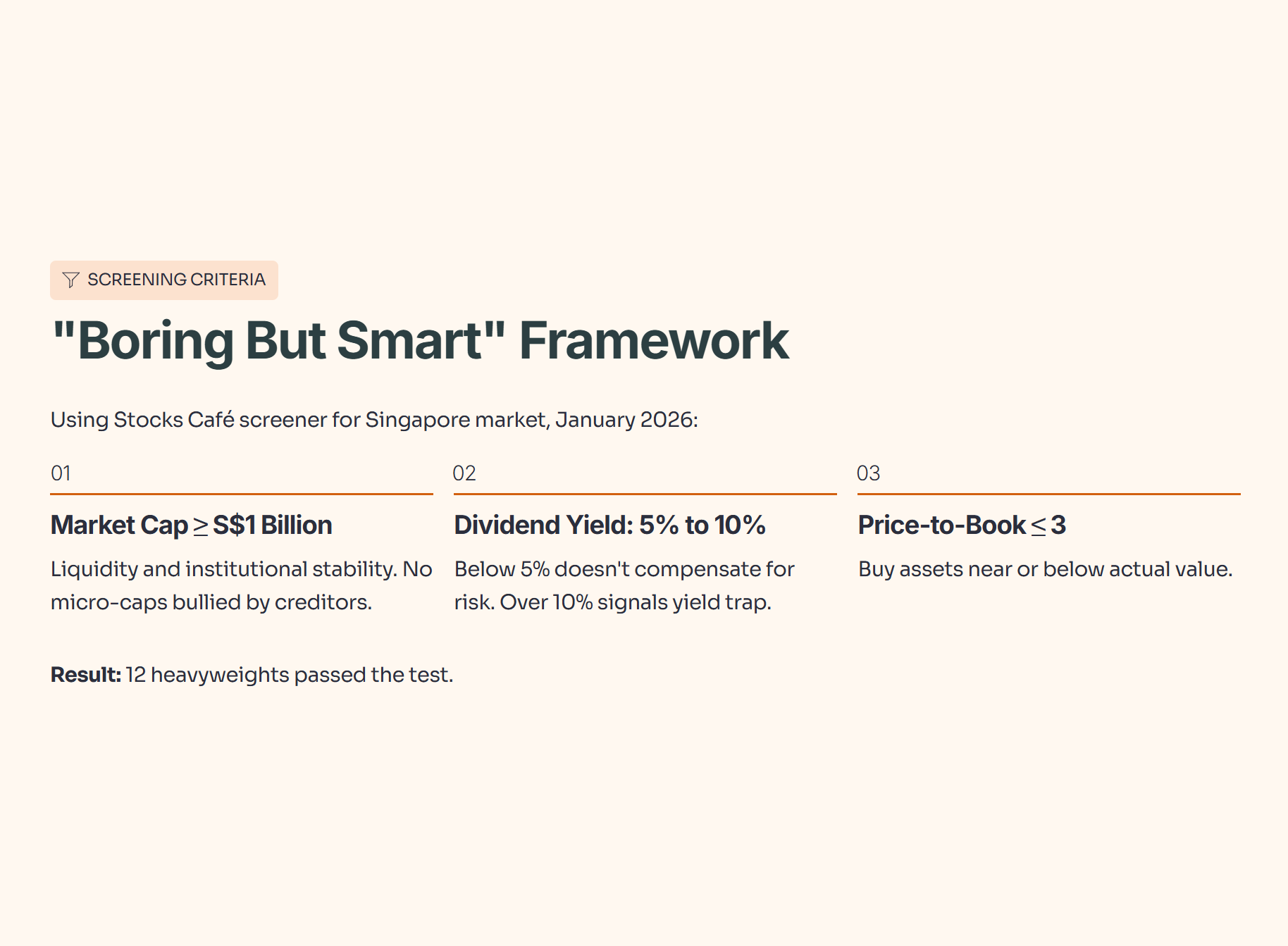

I don’t gamble with retirement money. When I screen for REITs, I use a strict “Boring but Smart” framework. Using the Stocks Café screener, I applied the following filters to the Singapore market for January 2026:

Market Capitalization ≥ S$1 Billion: We want liquidity and institutional stability. No micro-caps that get bullied by creditors.

Dividend Yield: 5% to 10%: Anything below 5% isn’t compensating us enough for risk over the CPF SA 4% floor. Anything consistently over 10% is usually a “yield trap” signal (distress).

Price-to-Book (P/B) Ratio ≤ 3: We want to buy assets near or below their actual value.

Here is the shortlist of 12 heavyweights that passed the test.

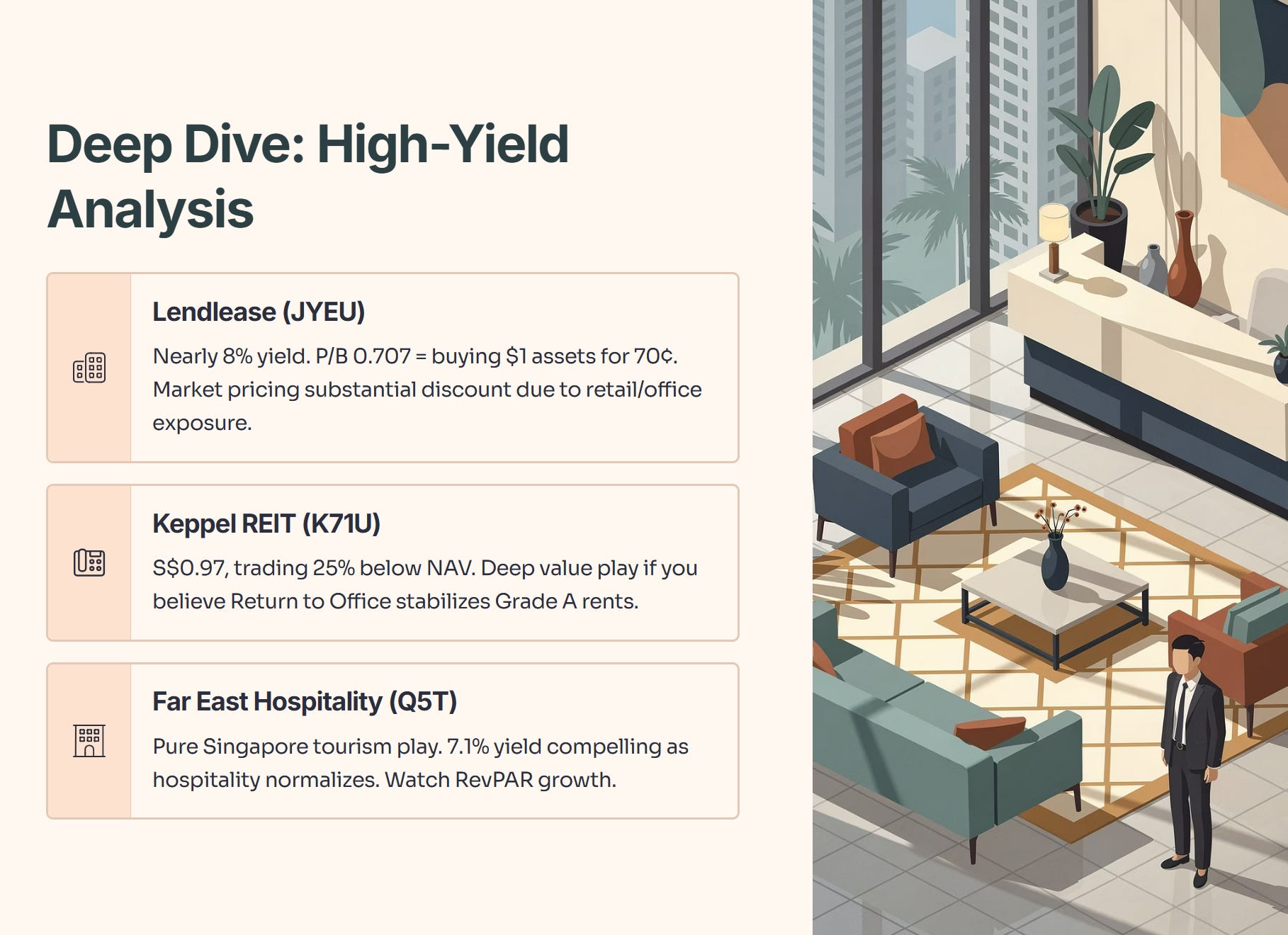

1. The High-Yield Heavyweights (>7%)

The screen threw up three names yielding over 7%. In a 3.5% interest rate world, a 7% yield is massive—but we need to check under the hood for rot.

Lendlease (JYEU) is topping the chart with nearly 8% yield. Trading at a P/B of 0.707 means you are buying $1.00 of assets for roughly 70 cents. The market is pricing in a substantial discount, likely due to concerns over their specific retail/office exposure.

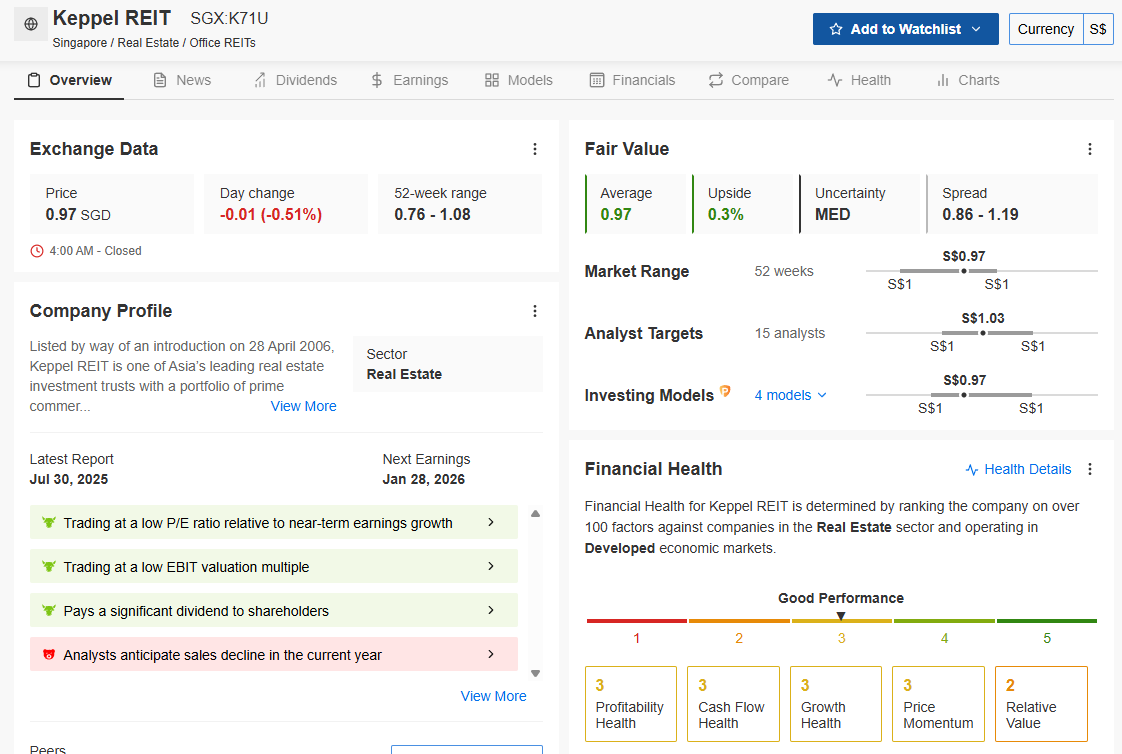

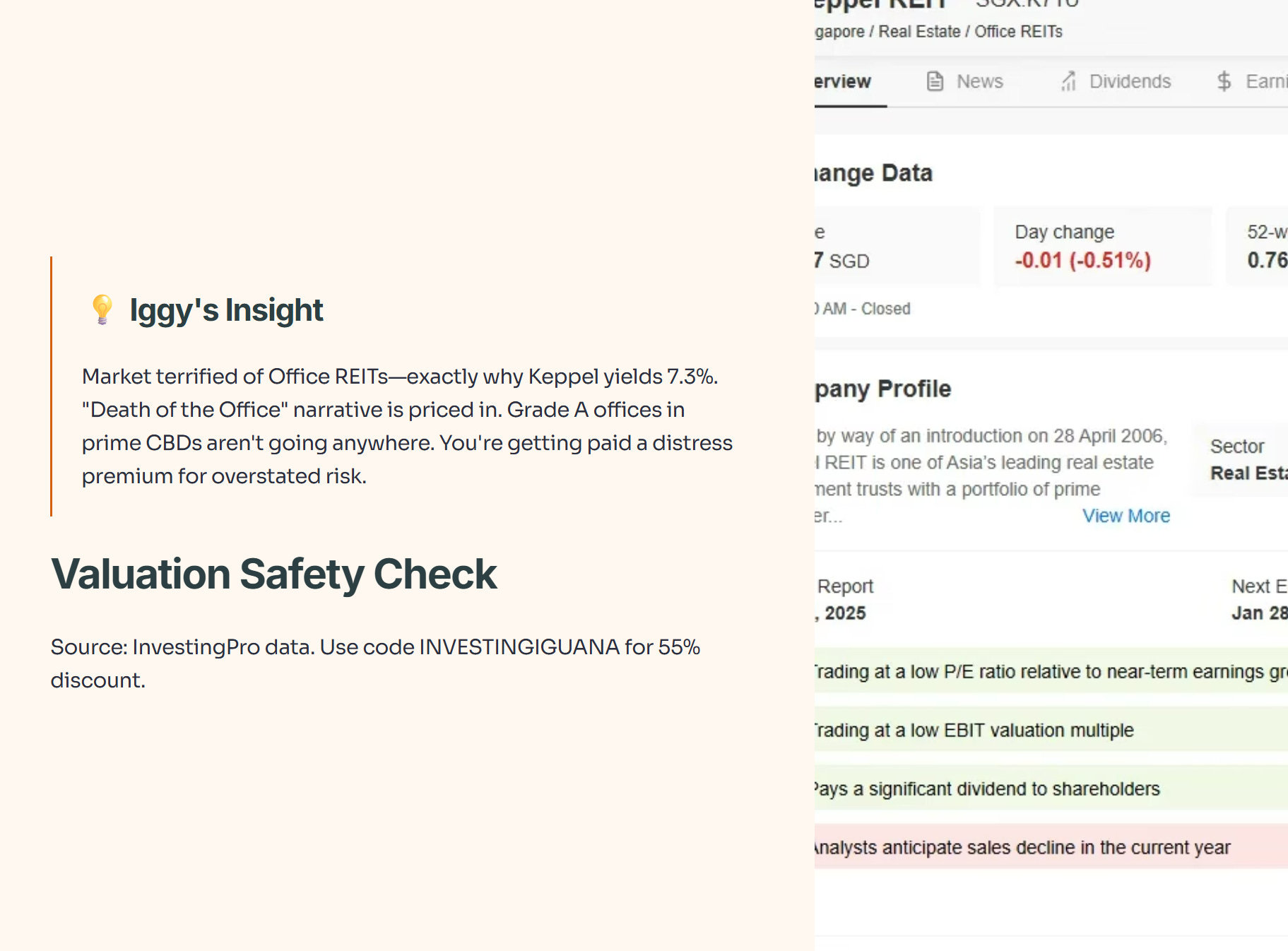

Keppel REIT (K71U) is the interesting one here for office bulls. It closed at S$0.97, trading at a roughly 25% discount to its Net Asset Value (NAV). If you believe the “Return to Office” mandates will stabilize Grade A office rents in Singapore and Australia, this is a deep value play.

Far East Hospitality (Q5T) offers a pure play on Singapore tourism. With the hospitality sector normalizing post-pandemic, a 7.1% yield is compelling, but watch their RevPAR (Revenue Per Available Room) growth carefully in the upcoming earnings.

💡 Iggy’s Insight:

The market is terrified of Office REITs, which is exactly why Keppel REIT is yielding 7.3%. The “Death of the Office” narrative is priced in. My take? Grade A offices in prime CBDs aren’t going anywhere. You are getting paid a distress premium for a risk that I believe is overstated for top-tier assets.

📊 Data Check: Valuation Safety

I don’t just guess at valuations. I check the institutional models to see if that “cheap” P/B ratio is a bargain or a warning sign.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Analysis: The InvestingPro models show a mixed bag for Keppel. The Financial Health Score is a solid 3/5 ("Good Performance"), confirming the balance sheet is not in distress. However, their Fair Value model pegs the stock at $0.97, suggesting zero upside from capital appreciation at today's price. This is purely a yield play—don't expect the stock price to moon, just collect the rent.

2. The Industrial & Logistics Fortresses (5.7% - 6.5%)

This is where the “Safe” money usually parks. These REITs are backed by secular trends in data centers, logistics, and manufacturing.

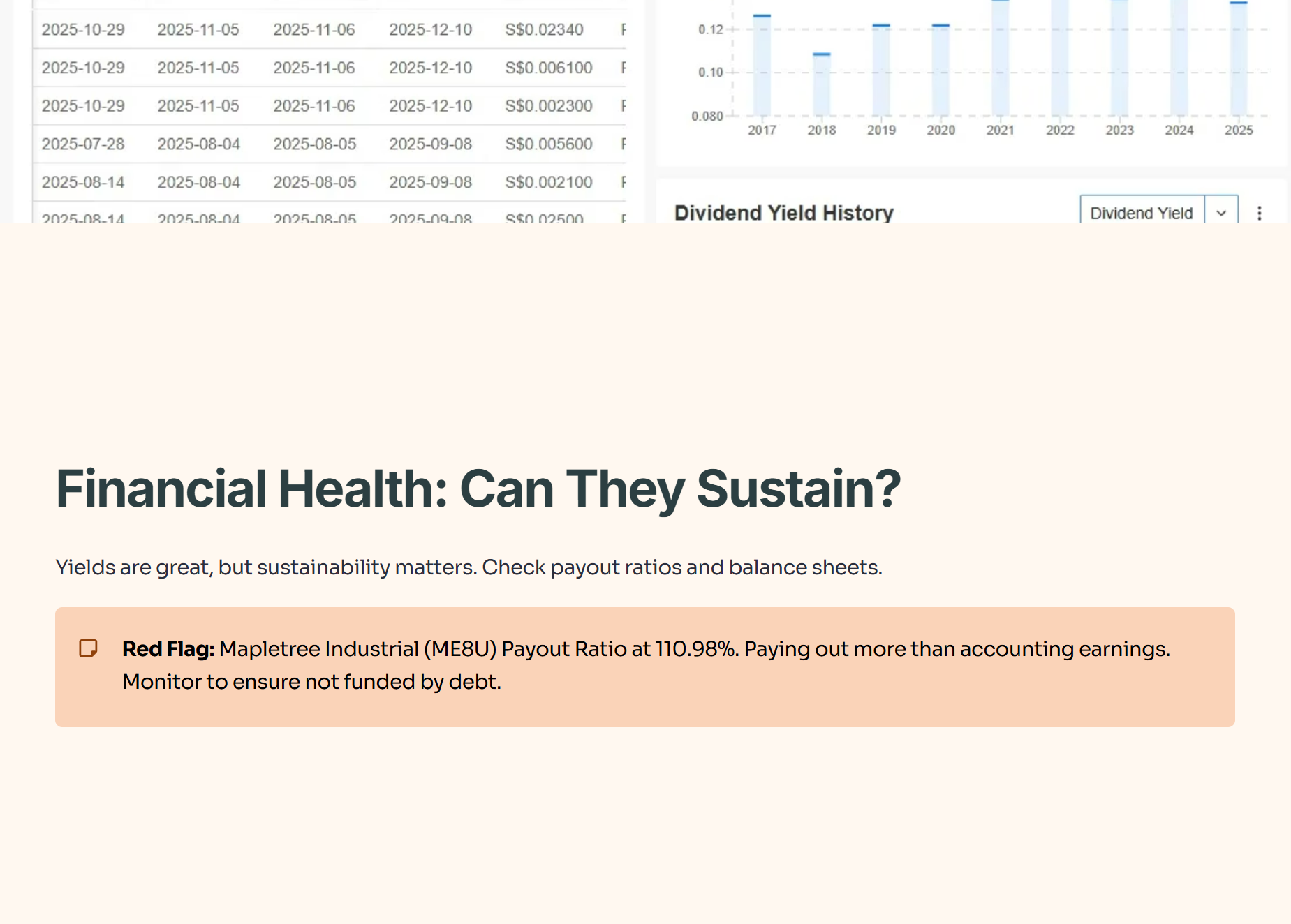

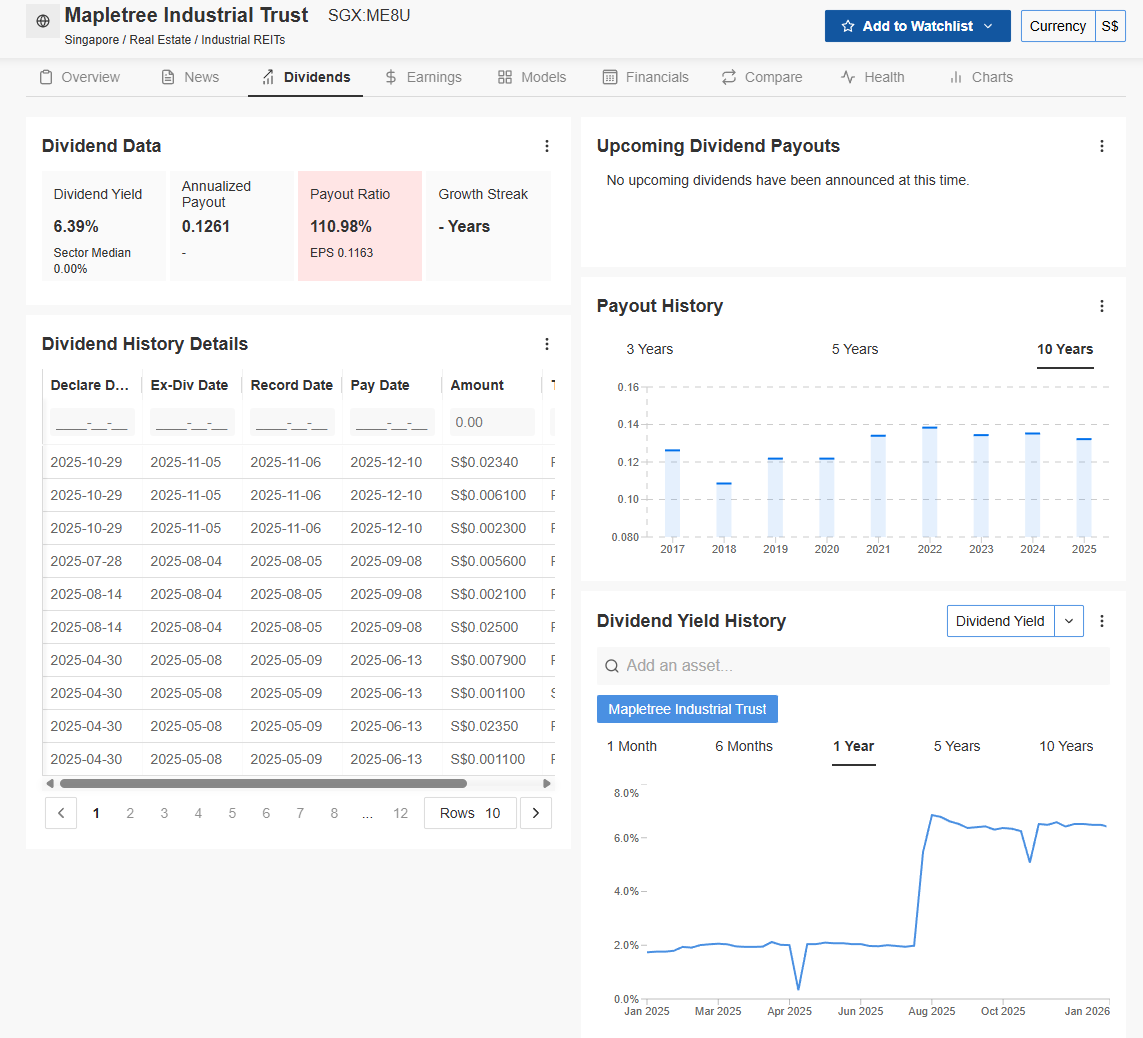

Mapletree Industrial Trust (ME8U) stands out immediately. It is the only REIT on this specific list trading at a significant premium to book (P/B 1.161). Why? The market pays a premium for Data Centers. Investors are willing to accept a 6.39% yield for the perceived safety and growth of the data center portfolio.

Mapletree Logistics Trust (M44U) and Frasers Logistics (BUOU) are trading slightly below book value. For long-term CPF holding, these are your “sleep well at night” stocks.

💡 Iggy’s Insight:

Notice the gap? You pay a 16% premium (over Book Value) for Mapletree Industrial, but you get a discount on Mapletree Logistics. This is the “AI Tax.” Everyone wants Data Centers. While ME8U is a fantastic REIT, value investors might find better risk-reward in the unloved logistics players like Frasers (BUOU). However, if you are vested in the AI trend, then ME8U is a good choice.

📊 Data Check: Financial Health

Yields are great, but can they sustain them? We need to look at the payout ratios and balance sheets.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Analysis: I spotted a red flag on the dashboard for Mapletree Industrial (ME8U). The Payout Ratio is currently listed at 110.98%. This means they are paying out more cash than their accounting earnings currently show. While REITs often pay >100% of accounting income due to depreciation, this level requires monitoring. We want to ensure this isn’t being funded by debt.

3. The Retail & Diversified Mix

Finally, we have the consumer-facing giants. This sector is a battle between defensive suburban malls and high-risk geopolitical plays.