The Retirement Paradox: Why A 5 Million Dollar Portfolio Still Feels Like Poverty (Singapore Retirement Deep-Dive)

Because a $5M block of ice still melts fast under the Geylang sun

If you walk into any kopitiam in Singapore right now, whether it is in Bedok, Jurong, or right here in the CBD, you will see it. The uncles are drinking their coffee and staring intensely at their phones. They are looking at their brokerage accounts. Many of these individuals are sitting on five million dollars in liquid net worth. For the headlines, that is a celebration of Singapore’s economic miracle. It feels safe.

But here is the uncomfortable truth that momentum investors often forget: that five million dollars is a depreciating block of ice sitting in the afternoon sun.

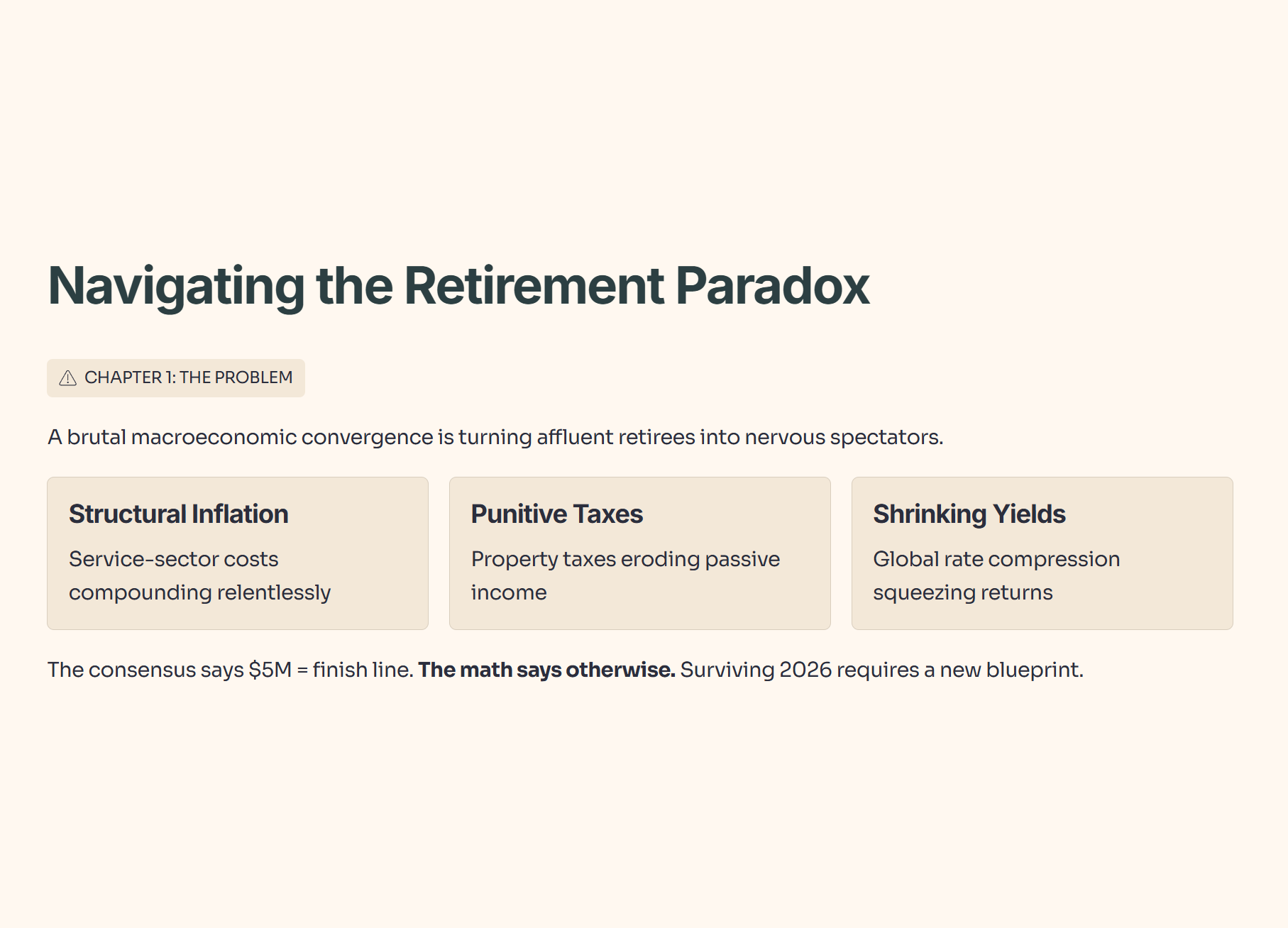

We are navigating the Retirement Paradox. This is a brutal macroeconomic convergence where structural service-sector inflation, punitive property taxes, and shrinking yields have turned affluent retirees into nervous spectators. The consensus narrative tells you that hitting the five-million-dollar mark means you have crossed the finish line. The math suggests otherwise. To the 170+ Paid Elite Members reading this, you already know we do not trade on feelings. We trade on forensic data. And the data shows that surviving 2026 requires an entirely new blueprint.

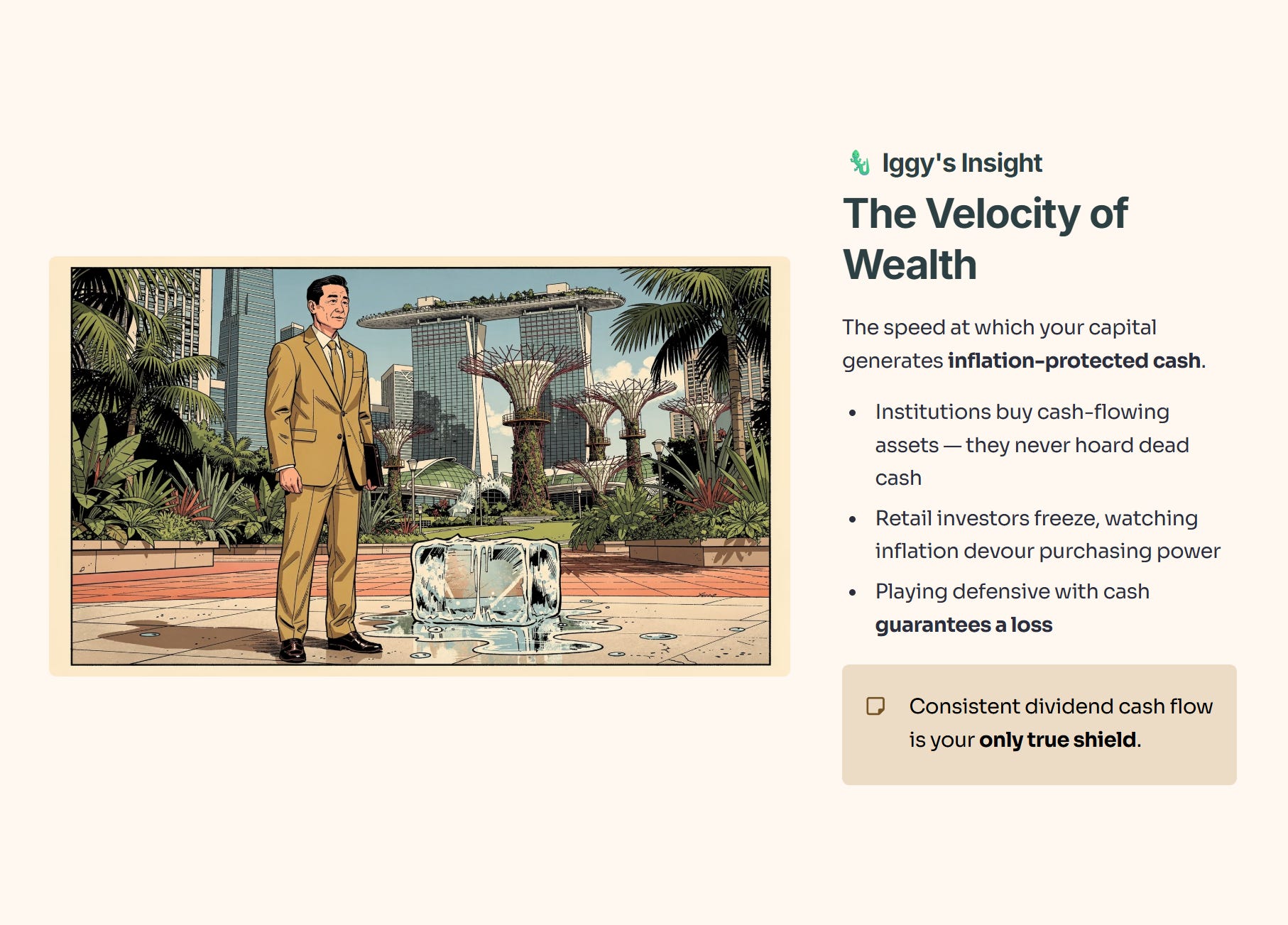

🦎 Iggy’s Insight

Let’s define that term. The “velocity of wealth” is simply the speed at which your capital generates inflation-protected cash. Institutions understand this perfectly. They do not hoard dead cash in a high-inflation environment; they buy cash-flowing assets. Retail investors, however, often freeze. They sit on a five-million-dollar pile, terrified to deploy it, watching inflation eat their purchasing power like a hungry diner at a mixed rice stall. This means playing defensive with cash is actually a major risk. You are essentially guaranteeing a loss. Consistent dividend cash flow is your only true shield.

In This Article:

The Local Impact (The Wallet)

How inflation attacks your fixed living costs

Why CPF is the iron bastion of Singapore retirement

Why DBS dividends are your new “salary”

The Data Proof (The Evidence)

How rising maintenance makes 5 million feel small

Why zero-yield growth stocks are mathematically broken

Three forensic questions to stress-test your portfolio

The Strategic Landscape (Scenario Matrix)

When macro intensifies and services explode

The fragile comfort of the base case

What happens if macro fully reverses

The Singapore Investor Playbook

The 25 percent concentration rule

Calculating your sleep-at-night (SAN) score

Using yield spreads to choose between DBS and CPF

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 170

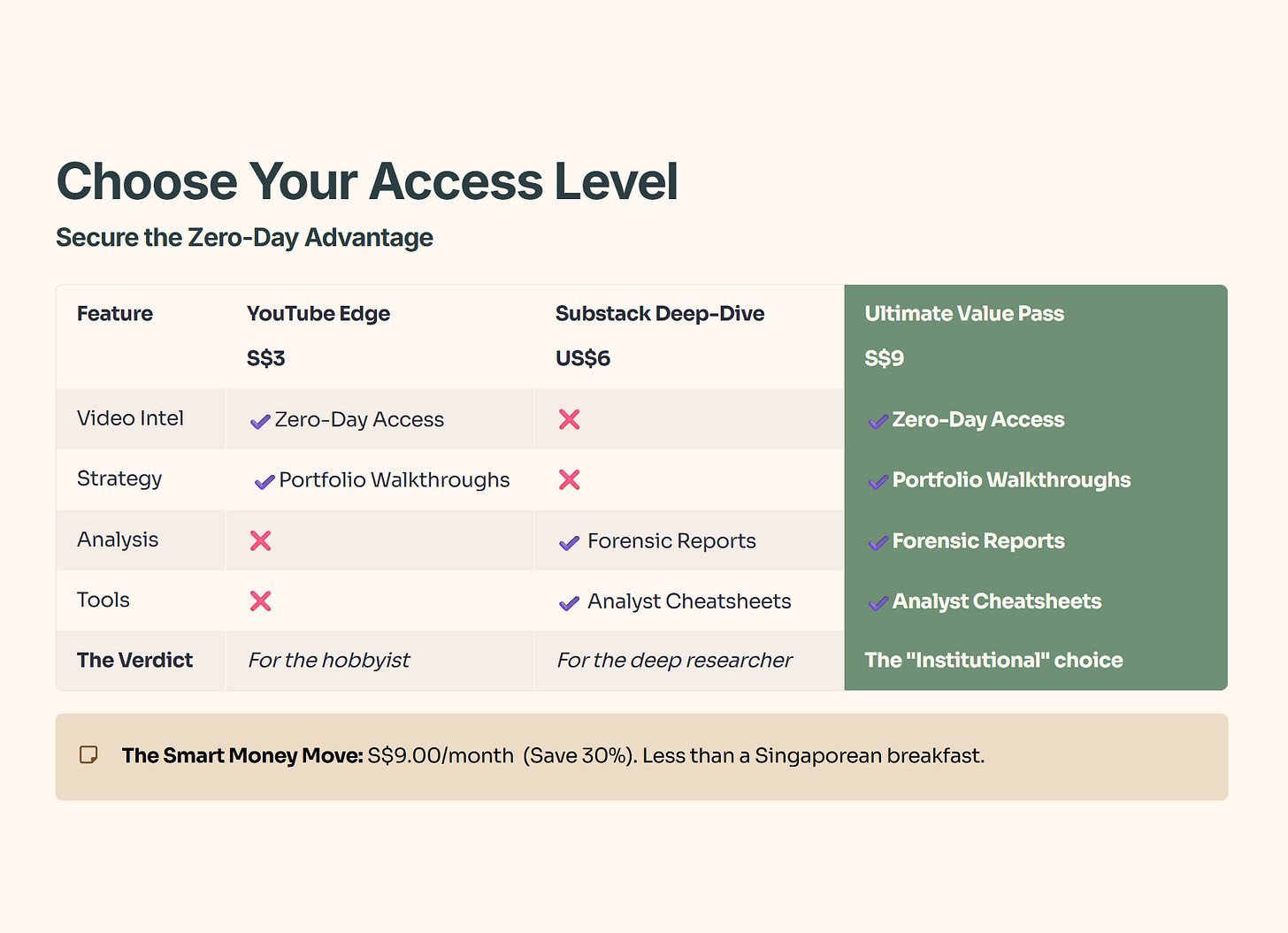

In the Singapore market, the gap between a smart entry and becoming someone else’s exit liquidity can be as little as 48 hours. That’s the cost of informational lag.

Free subscribers get my analysis up to 14 days later. The Elite 170 get it the moment it’s ready.

Your Edge: The S$9 Ultimate Value Pass bundles zero-day video intel, forensic reports, and analyst cheatsheets into one institutional-grade feed — for less than a Singaporean breakfast.

The Local Impact (The Wallet)

This paradox is not an abstract global problem. It is a highly localized, deeply uncomfortable Singaporean reality. We need to translate this global yield compression and domestic inflation narrative directly to your household.

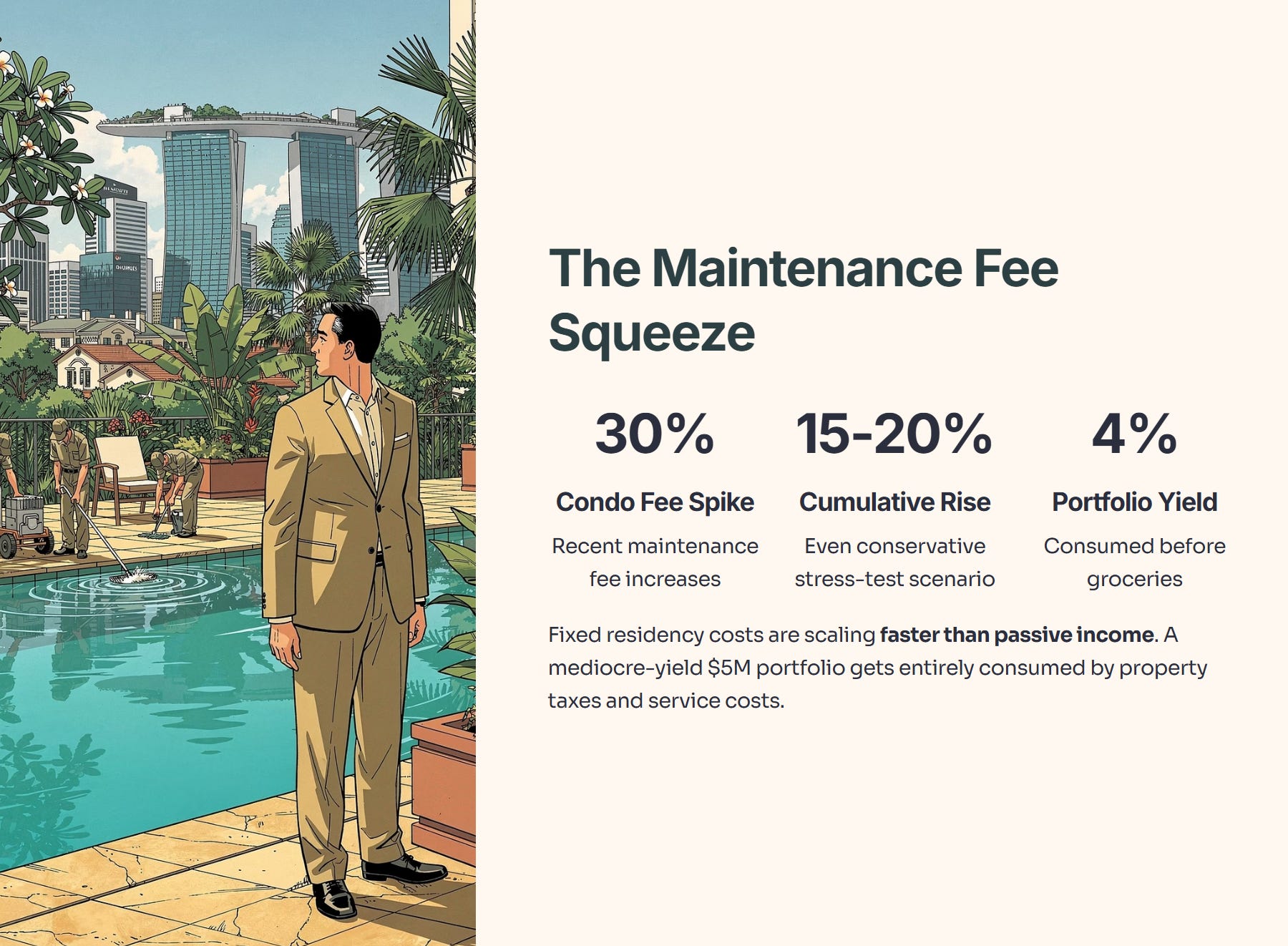

First, we must audit the impact on jobs and income. While headline consumer price index figures hovered around 1.4 percent in early 2026, housing maintenance and repair costs spiked an agonizing 27.9 percent. Historically, this benchmark usually tracks closer to 2 or 3 percent during stable economic cycles. In terms of peer context, Singapore’s service inflation is hyper-concentrated in labor due to wage reforms and manpower quotas.

If this structural labor shortage intensifies, private condominium maintenance fees—already up 30% in recent periods —could continue outpacing inflation. While doubling over five years is a stress-test scenario, even a 15-20% cumulative increase would consume a significant portion of a 4% portfolio yield.

Even if the labor crunch reverses slightly, we still face a permanently higher plateau of service costs. This means your fixed residency costs are scaling faster than your passive income. A five-million-dollar portfolio generating a mediocre yield will be entirely consumed by property taxes and service salaries before you even buy your groceries.

Second, we must examine the impact on the Central Provident Fund and Supplementary Retirement Scheme. The interest rate for the Special Account (SA) and Retirement Account (RA) remains anchored at a 4.0 percent floor. Historically, this rate has provided an unshakeable foundation across multiple market crashes. There is no developed market equivalent that offers a government-backed, risk-free 4.0 percent yield in a shrinking global rate environment. If global interest rates drop further, the yields on commercial bank deposits will collapse, making this floor infinitely more valuable. If global rates unexpectedly spike, the CPF still acts as the ultimate shock absorber. This means the CPF is the “iron bastion” of your retirement. You must leverage this fully, maximizing your retirement sums before taking external market risks.

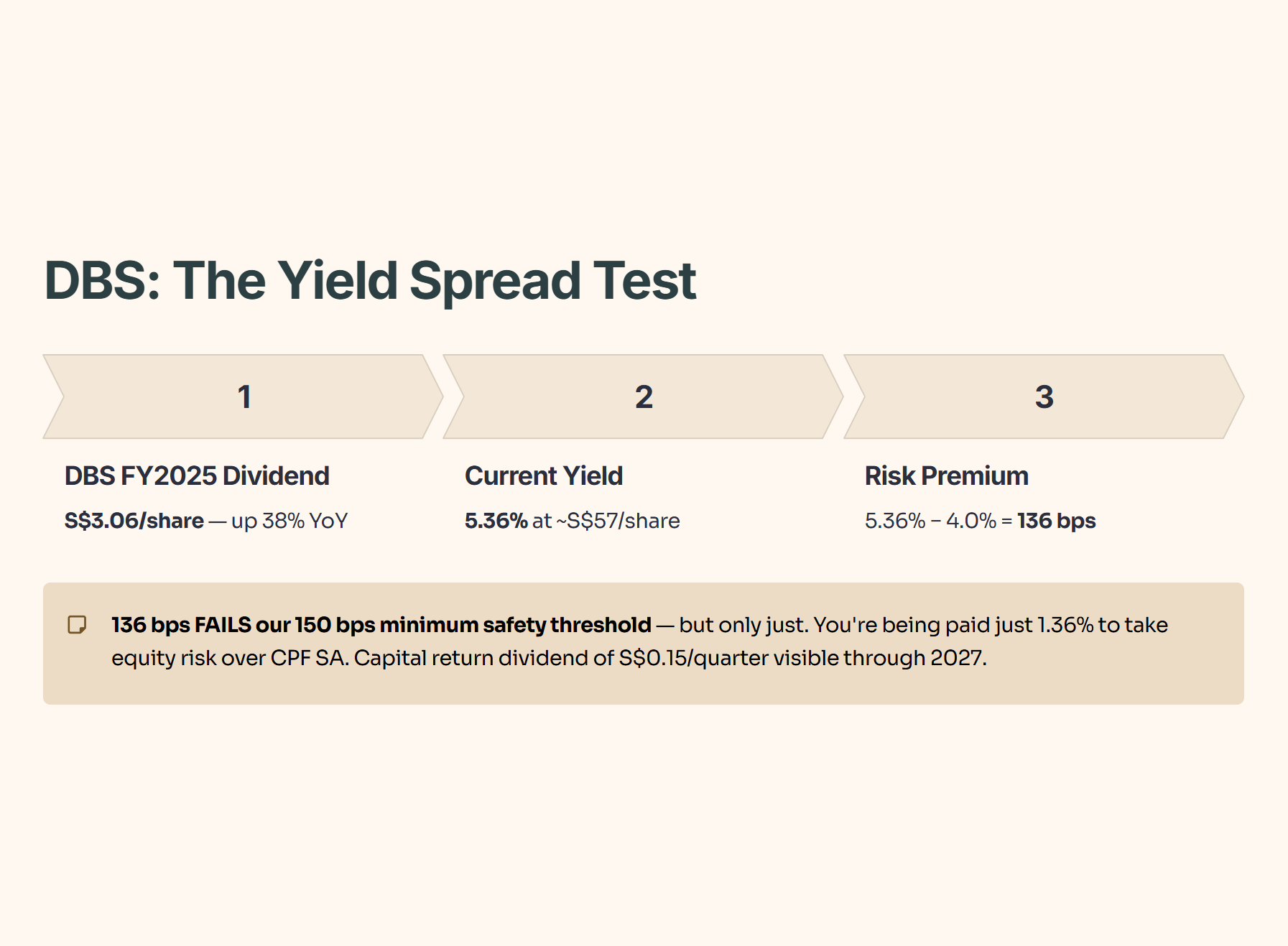

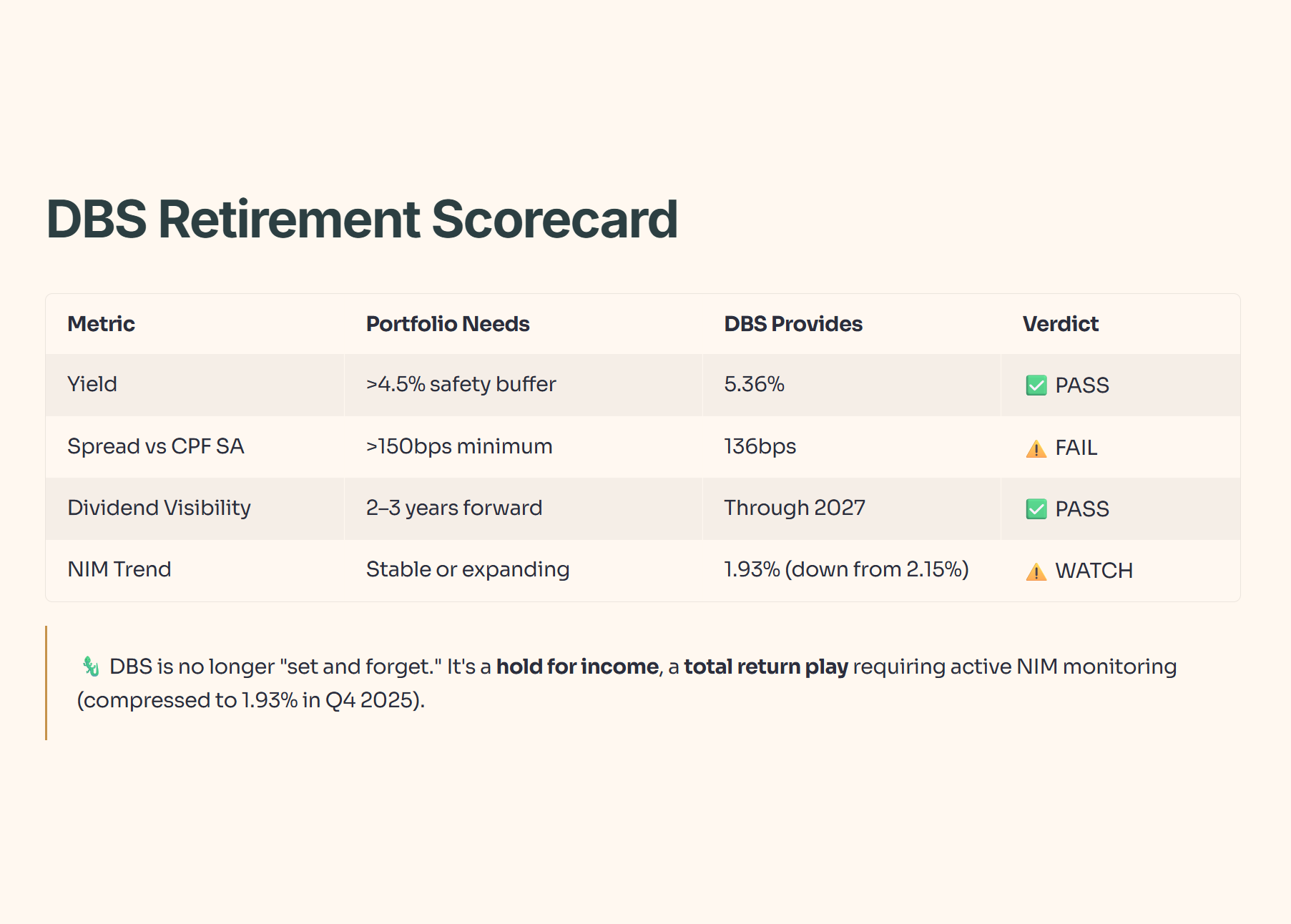

Third, we turn to the local stock market. The benchmark local bank, DBS, declared a total FY2025 dividend of S$3.06 per share—a 38% increase from the prior year . At the current share price of approximately S$57, this translates to a yield of 5.36% .

Let’s apply the Yield Spread Formula:

Risk Premium = 5.36% (Asset Yield) − 4.0% (CPF SA Risk-Free Rate) = 136 basis points

At 136bps, this fails our 150bps minimum safety threshold—but only just. For the income investor in Bedok or Jurong, DBS offers a slim premium over the risk-free rate. The bank plans to maintain its S$0.15 quarterly capital return dividend through 2027 , providing visibility. But at this spread, you are being paid just 1.36% to take equity risk instead of parking money in your CPF Special Account.

🦎 Iggy’s Insight

DBS is no longer a "set and forget" retirement holding at current prices. It is a hold for income, a total return play requiring active monitoring of NIM trends, which compressed to 1.93% in Q4 2025 .

“Now here’s the part most retirees miss: if DBS is no longer ‘set-and-forget’ at today’s yield spread, the real question is exactly what to hold instead—and what numbers to check so you don’t become exit liquidity.”