The S$0.77 Illusion: Auditing Phillip Securities’ Hyper-Growth Thesis on LHN Limited

When rapid franchise scaling masks structural friction: A forensic deep-dive into whether LHN's 6.5% dividend yield is built to last.

Against the Wall: Why a 14% Drop in Revenue Changes the Co-Living Math for Your Retirement Portfolio

LHN Limited trades at S$0.62. That is 6.9% above what independent valuation tools say the business is worth. The company also carries a significant debt load. The forensic framework I use sets a minimum yield of 4.7% and strict debt ceilings before any stock qualifies for a retirement portfolio.

Institutional analysts like the rapid growth of the Coliwoo co-living brand. But if you are managing your own retirement savings, you need to ask a different question. Can this aggressive growth model protect your money if other parts of the business stall? This audit strips away the institutional optimism and looks only at the numbers that support your retirement runway.

The heat in Singapore has been hovering around forty degrees this week. The shaded balcony still feels like an oven. When the afternoon glare hits the plants, you quickly learn which roots are genuinely deep and which ones are just surviving on surface water. Real estate portfolios face the same test when easy money dries up.

Before we get into the numbers, I want to be clear about the two types of investors reading this. If you have a long runway and a higher appetite for risk, some of what follows will feel conservative. It is meant to. This framework exists for the retiring or retired Singaporean who needs capital to work reliably — the investor who cannot afford a structural shock to their income stream.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

The Analyst's Case

Iggy's Forensic Screen

The Dividend Trajectory

The Forensic Gap

What To Watch Next

The Forensic Stance

Section 1 — The Analyst’s Case

Phillip Securities Research maintains a BUY rating on LHN Limited. They have reduced their target price from S$0.85 to S$0.77. That reduction comes from a higher discount applied to Coliwoo (SGX: W8W), LHN’s core co-living division. They now apply a 20% discount instead of the previous 10% framework.

The institutional thesis remains tied to rapid operational scaling of the co-living segment. Room inventory grew 38% year-on-year to 3,568 keys. Revenue increased 17% to S$26.9 million during the first half of fiscal year 2026.

The analyst points to strong performance from recent property launches. Coliwoo Midtown on Middle Road reached 55% occupancy within weeks of its March 2026 debut. The broader portfolio maintains an average occupancy rate of 97%. Looking ahead, the institutional growth model relies on 1,021 additional rooms in the pipeline. The company has stated a long-term corporate target of 10,000 rooms by 2030.

The report also highlights strategic growth levers. These include expansion into service-worker dormitories for health and retail sectors, alongside optimisation of Work+Store facilities into higher-value industrial storage options.

The property development segment is treated as a temporary, non-structural drag. The 55 Tuas South Avenue 1 industrial project contributed zero revenue during the first half of the fiscal year. The analyst expects management’s shift toward renting out remaining unsold inventory to stabilise segment book values. The remaining non-co-living business units are valued collectively using a standard 10x price-to-earnings multiple (a valuation method that compares the stock price to annual earnings). Property development assets continue to be held at book value.

THE LOAD-BEARING ASSUMPTION: The institutional thesis assumes that the high-velocity operational expansion and strong rental cash flows of the Coliwoo co-living arm can completely absorb and neutralise structural capital stagnation within the property development segment.

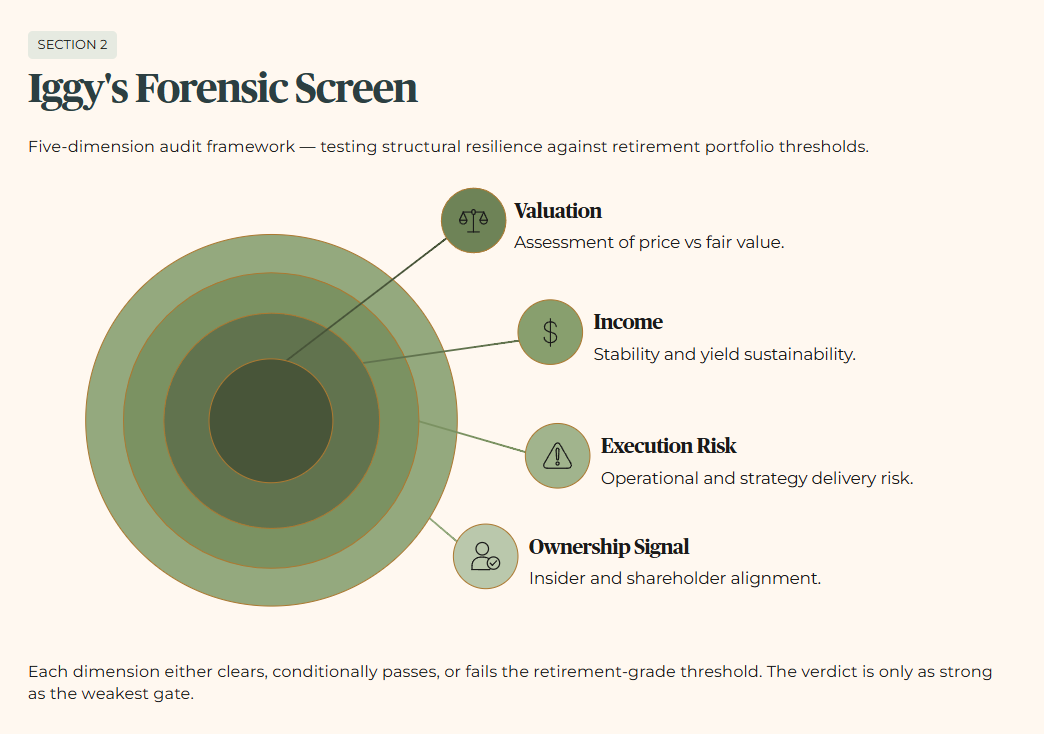

Section 2 — Iggy’s Forensic Screen

Our forensic review runs LHN Limited through a five-dimension audit framework. This tests its structural resilience against the thresholds I require before any stock enters a retirement portfolio.

Dimension One — Valuation

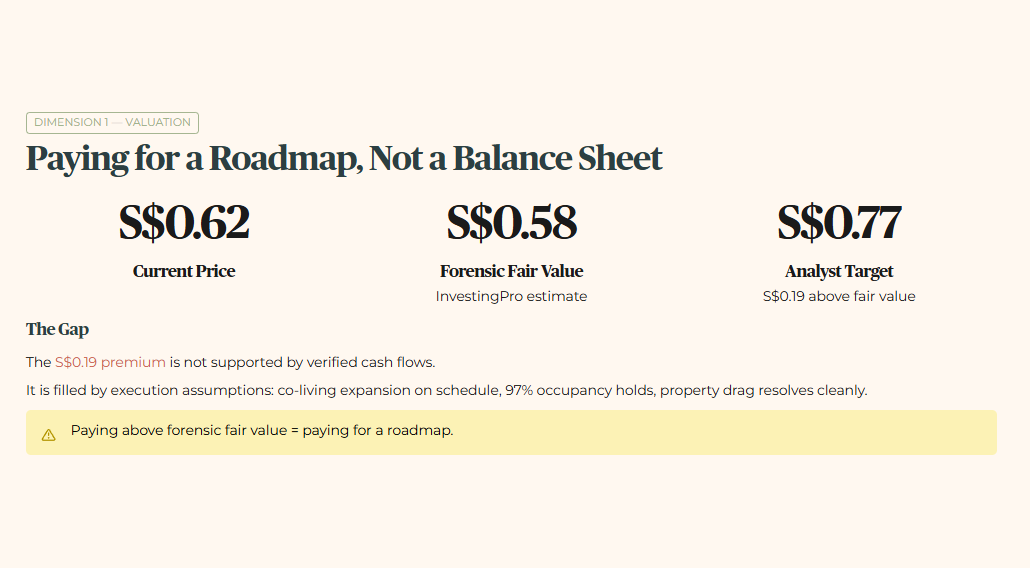

LHN Limited trades at S$0.62. The InvestingPro fair value — an independent estimate of what the business is worth based on verified cash flow data — sits at S$0.58. That is a 6.9% premium. The analyst’s target price of S$0.77 sits S$0.19 above the forensic fair value. That gap of S$0.19 is not supported by verified cash flows. It is filled by execution assumptions — specifically, that the co-living expansion runs on schedule, occupancy holds at 97%, and the property development drag resolves cleanly. When you pay above forensic fair value today, you are paying for a roadmap, not a balance sheet.

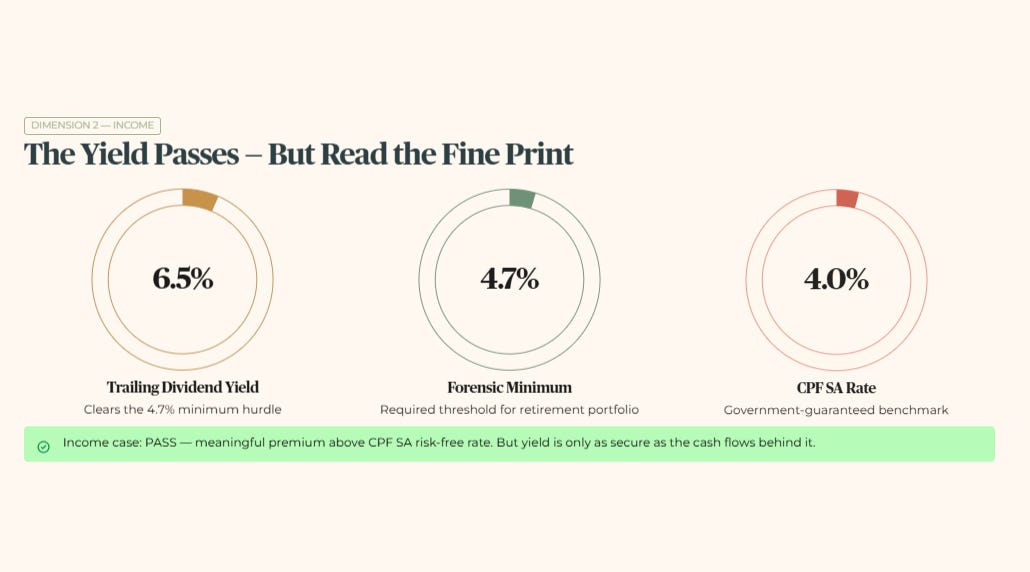

Dimension Two — Income

The trailing dividend yield sits at 6.45%, which I will carry as 6.5% throughout this piece. That clears my 4.7% minimum yield hurdle — the income threshold I require before any stock qualifies for a retirement portfolio — and sits well above the 3.2% forensic floor. For context, CPF SA currently pays 4.0% with a government guarantee behind it. LHN’s yield offers a meaningful premium above that risk-free benchmark. The income case passes. But that yield is only as secure as the cash flows supporting it. We examine that in Dimensions Three and Four.

Dimension Three — Execution Risk

LHN’s trailing twelve-month revenue stands at S$122 million. On a semi-annual run rate, first-half fiscal year 2026 revenue shows a 14% year-on-year decline — contracting from S$35 million in the March 2025 quarter to S$30 million in the March 2026 quarter. The driver is stalled property sales at Tuas South.

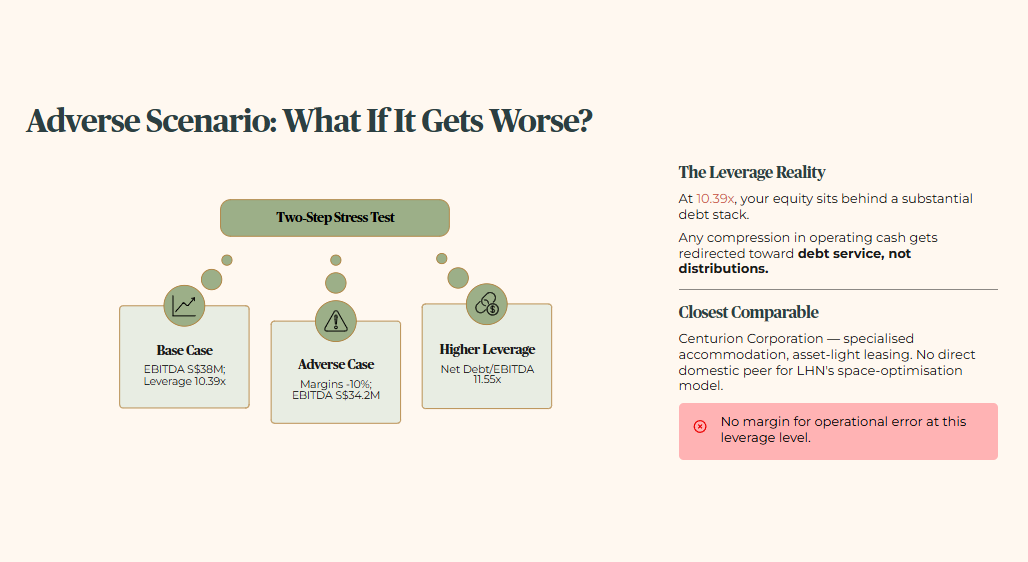

Total debt stands at S$450 million against S$55 million in cash. That creates a net debt position of S$395 million. EBITDA — earnings before interest, tax, depreciation and amortisation, which measures operating cash generation — sits at S$38 million on a trailing twelve-month basis. That produces a net debt to EBITDA ratio of 10.39x, meaning it would take more than ten years of current operating earnings to repay all debt. This crosses our red-flag threshold of 10x.

The interest coverage ratio — the number of times operating income covers annual interest payments — sits at 3.79x against my 4.0x hard floor. This is a marginal miss of 21 basis points, not a structural collapse. I am retaining Zone 3 — Conditional rather than dropping to Zone 4 for three documented reasons. First, operating cash flow of S$55 million on a trailing twelve-month basis covers the interim dividend with meaningful headroom. Second, co-living occupancy of 97% supports near-term interest servicing capacity. Third, the Lim family’s April 2026 accumulation — discussed in Dimension Four — signals management conviction in forward cash flow stability. This is a conditional pass, not a clean one. If ICR does not recover above 4.0x by the November 2026 earnings cycle, Zone 4 becomes the correct assignment.

Consider an adverse forward scenario. Suppose property development assets remain frozen and co-living operational margins compress by 10% due to rising local utility and maintenance costs. EBITDA would fall to S$34.2 million. The net debt to EBITDA ratio would push to 11.55x — meaning it would now take more than eleven and a half years of earnings to pay down all debt, well beyond the red-flag threshold. Any structural compression in cash from operations at that leverage level gets redirected toward debt service, not distributions.

The debt structure above maps the floor — but the April 2026 insider accumulation in the next section introduces a documented override that changes the Zone 3 Conditional assignment.