Temasek’s S$434B Warning: Why The "Old" SGX Strategy Is Dead

The sovereign wealth fund just split into three. Here is what that tells us about the end of the “easy money” era and where the smart money is going next.

If you only read the headlines this week, you probably saw one number: S$434 billion. That is Temasek’s record Net Portfolio Value (NPV). It’s a nice number. It makes us feel good about our national reserves.

But if you are a serious investor, the absolute number is irrelevant.

The real story—the one that directly impacts how you should be positioning your own SRS and cash portfolio for 2026—is buried in the structural changes announced alongside the earnings. Temasek isn’t just growing; it is fundamentally changing its shape. On August 28, 2025, they announced a split of their investment operations into three distinct legal entities.

Why fix it if it isn’t broken? Because the “old way” of managing a global portfolio—treating DBS the same way you treat a Silicon Valley AI startup—is dead.

Here is the deep dive into what this restructuring means, and how you can clone their strategy.

In This Article:

• Part 1: The Restructuring—A Signal Hidden in Plain Sight

• Part 2: The “New Bets”—Where Temasek Thinks the Money Is

• Theme 1: AI Infrastructure (The “Pick and Shovel” Play)

• Theme 2: The Pivot to India (The Consumption Story)

• Part 3: The “Capital Recycling” Engine

• Part 4: Iggy’s Verdict—The “So What?” for Singapore Investors

• Part 5: The Definitive Conclusion—The End of “Easy Money”Part 1: The Restructuring—A Signal Hidden in Plain Sight

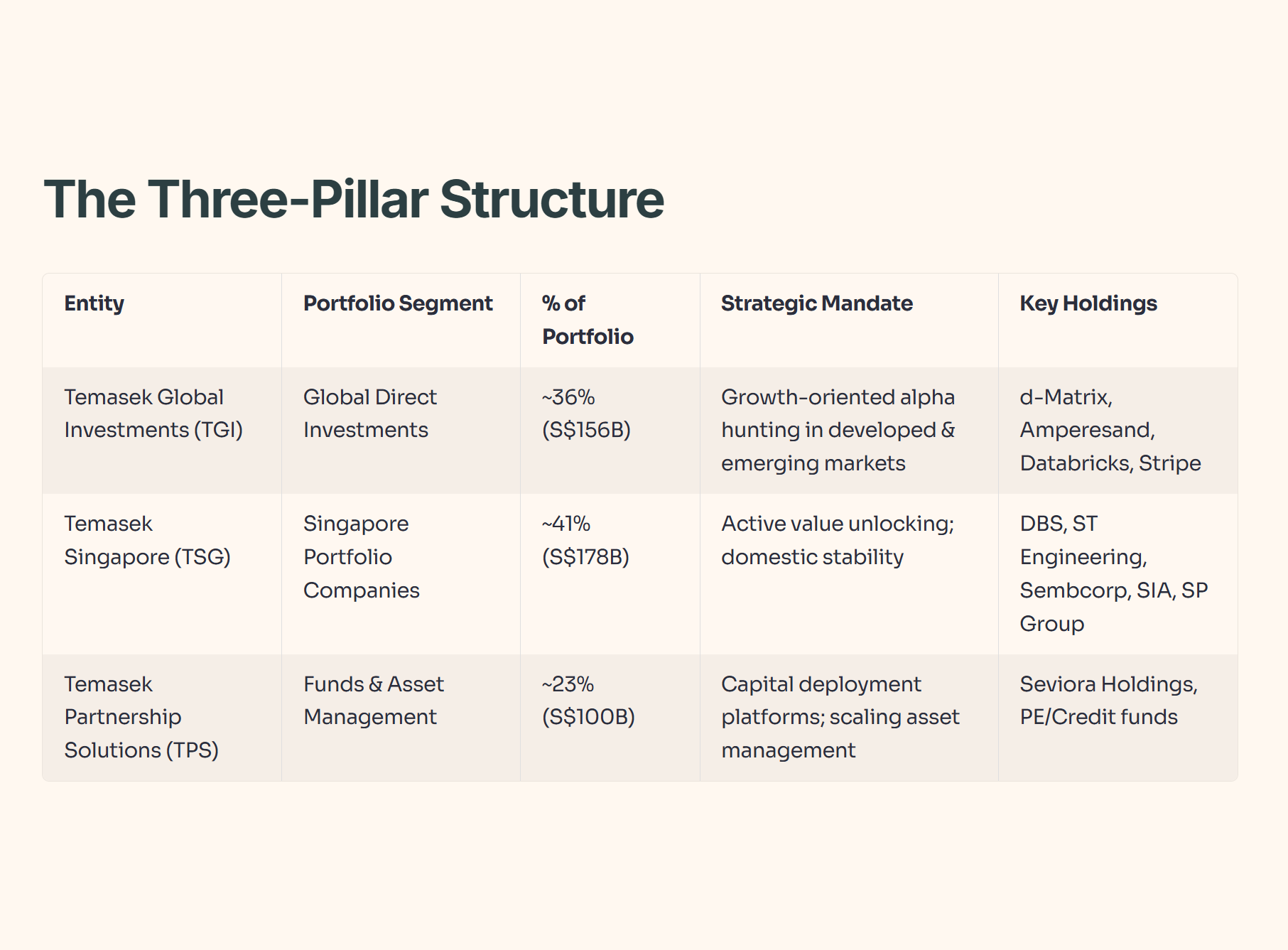

Effective April 1, 2026, Temasek is no longer just “Temasek.” It is evolving into a triad. This isn’t just bureaucratic shuffling; it is a strategic admission that we are living in a fragmented world that requires specialized engines.

The three new entities are:

Temasek Global Investments (TGI): The “Hunter.” Focused on global growth and alpha.

Temasek Singapore (TSG): The “Shield.” Focused on Singapore portfolio companies (the defensive core).

Temasek Partnership Solutions (TPS): The “Scaler.” Focused on asset management and capital platforms.

Why this matters to you:

For decades, we’ve looked at Temasek as a monolith. Now, they are separating their “Safety Bucket” (TSG) from their “Growth Bucket” (TGI). This is exactly how you should structure your own portfolio—separation of church and state between your dividend payers and your moonshots.

Iggy’s Insight:

This split is the ultimate signal that “active management” is coming to the SGX. With a dedicated entity (TSG) focused solely on Singapore portfolio companies, I expect a surge in consolidation and restructuring among our local blue chips (think Sembcorp, Keppel, ST Engineering). They are no longer just “holdings”; they are now assets that need to be optimized to protect the core. If you are holding these stocks, do not sell—the value unlocking is just beginning.

Table 1: The Three-Pillar Restructuring—Portfolio Segments & Strategic Focus

Part 2: The “New Bets”—Where Temasek Thinks the Money Is

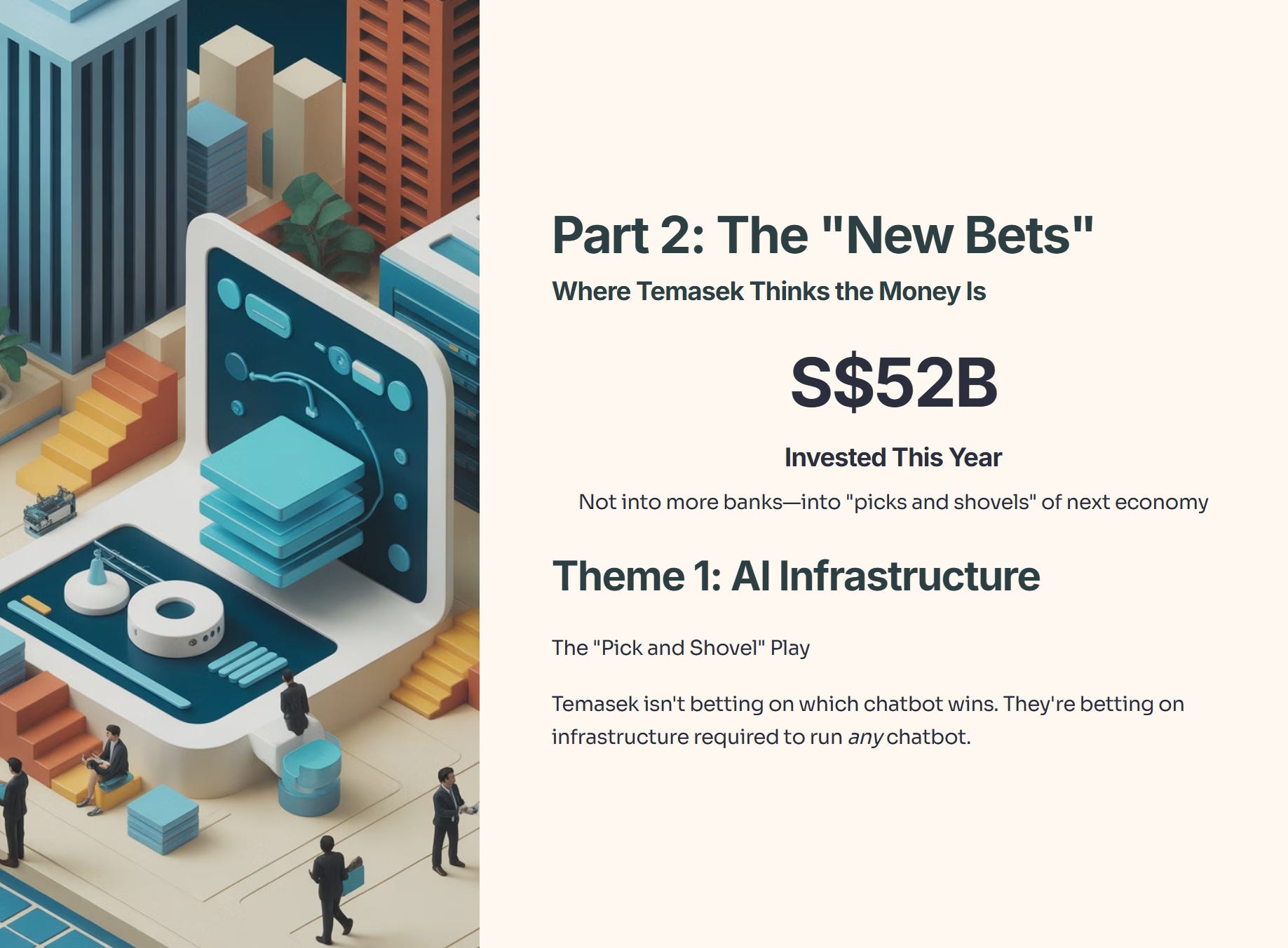

Temasek invested S$52 billion this year. Where did it go? It didn’t go into buying more banks. It went into the “picks and shovels” of the next economy.

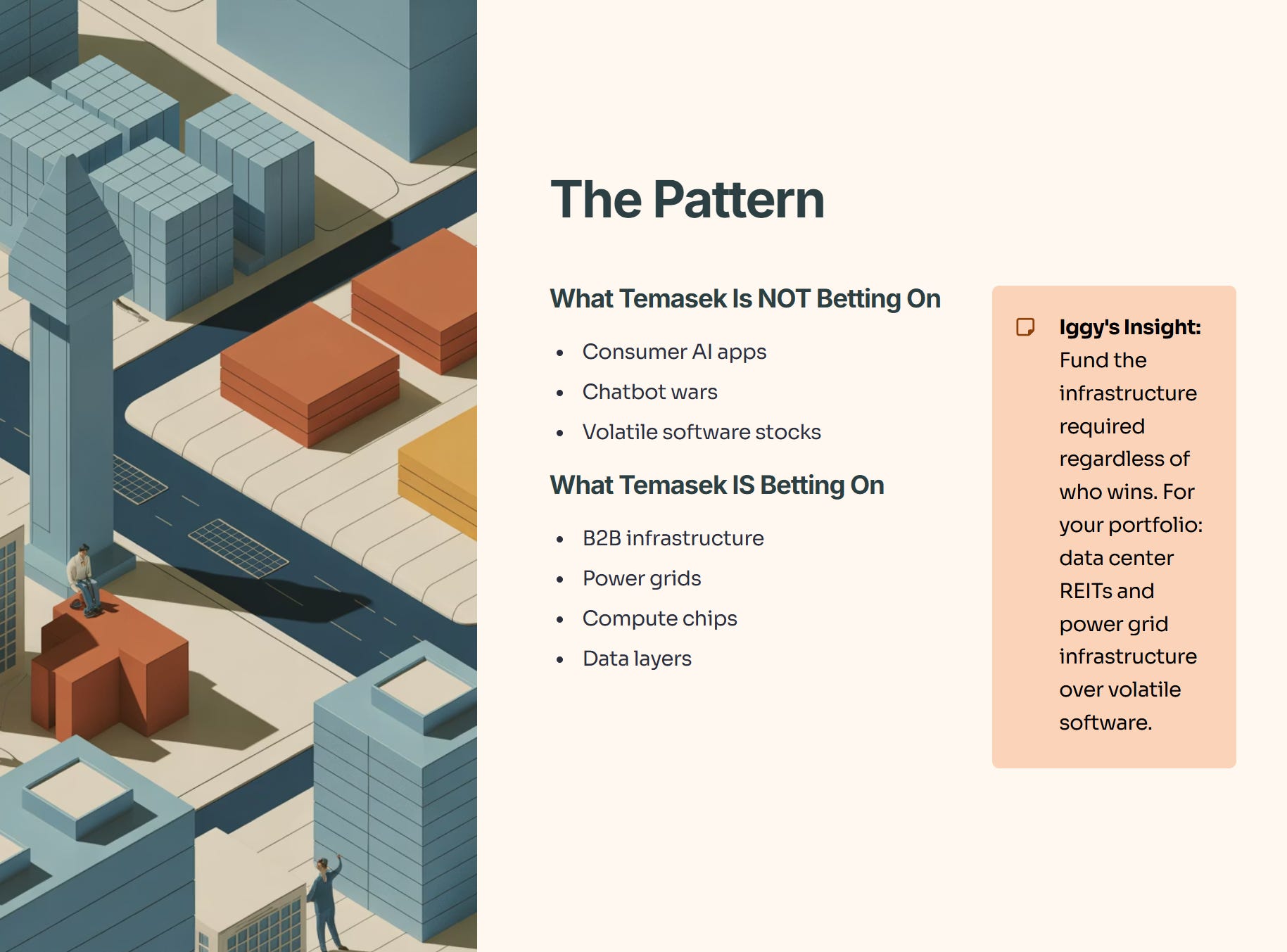

Theme 1: AI Infrastructure (The “Pick and Shovel” Play)

Temasek isn’t betting on which chatbot will win. They are betting on the infrastructure required to run any chatbot. This is the “safe” way to play a bubble.

Explore

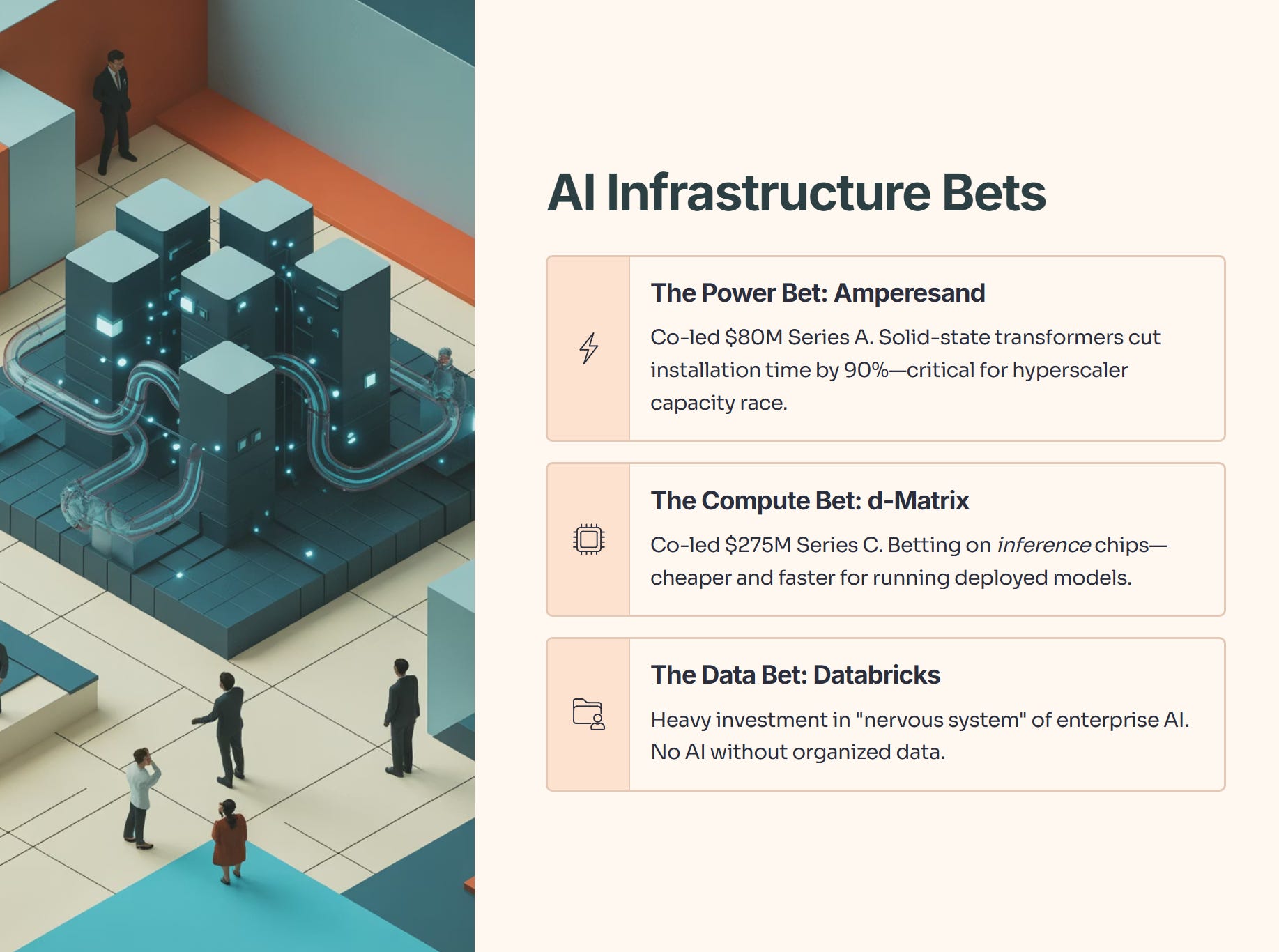

The Power Bet (Amperesand): AI eats electricity. Temasek co-led an $80M Series A into Amperesand to solve the data center power bottleneck. Their solid-state transformers cut installation time by 90%—a critical need when hyperscalers are racing to build capacity.

The Compute Bet (d-Matrix): Everyone bought NVIDIA for training. Temasek is betting on d-Matrix for inference (running the models). They co-led a $275M Series C because d-Matrix chips are cheaper and faster for running models once they are actually deployed.

The Data Bet (Databricks): You can’t have AI without organized data. Temasek remains heavily invested here, betting on the “nervous system” of enterprise AI.

Iggy’s Insight:

Notice the pattern? None of these are “consumer” AI apps. They are B2B infrastructure. The market is currently obsessed with whoever creates the “smartest” AI. Temasek is ignoring that noise and funding the power, the chips, and the data layers that are required regardless of who wins the chatbot war. For your portfolio, look for listed equivalents—data center REITs and power grid infrastructure rather than volatile software stocks.

Theme 2: The Pivot to India (The Consumption Story)

For the first time, the divergence is undeniable.

China Exposure: Dropped from 22% → 18%.

India Exposure: Rose from 6% → 8%.

This is a geopolitical calculation. China is facing structural headwinds (deflation, trade wars). India is hitting its “consumption S-curve”—the moment when the middle class starts buying cars, insurance, and branded snacks.

Temasek put its money where its mouth is by appointing former DBS CEO Piyush Gupta as Chairman of Temasek India. They also bought a $1B stake in Haldiram’s (snacks). This is a bet on the Indian stomach and wallet.

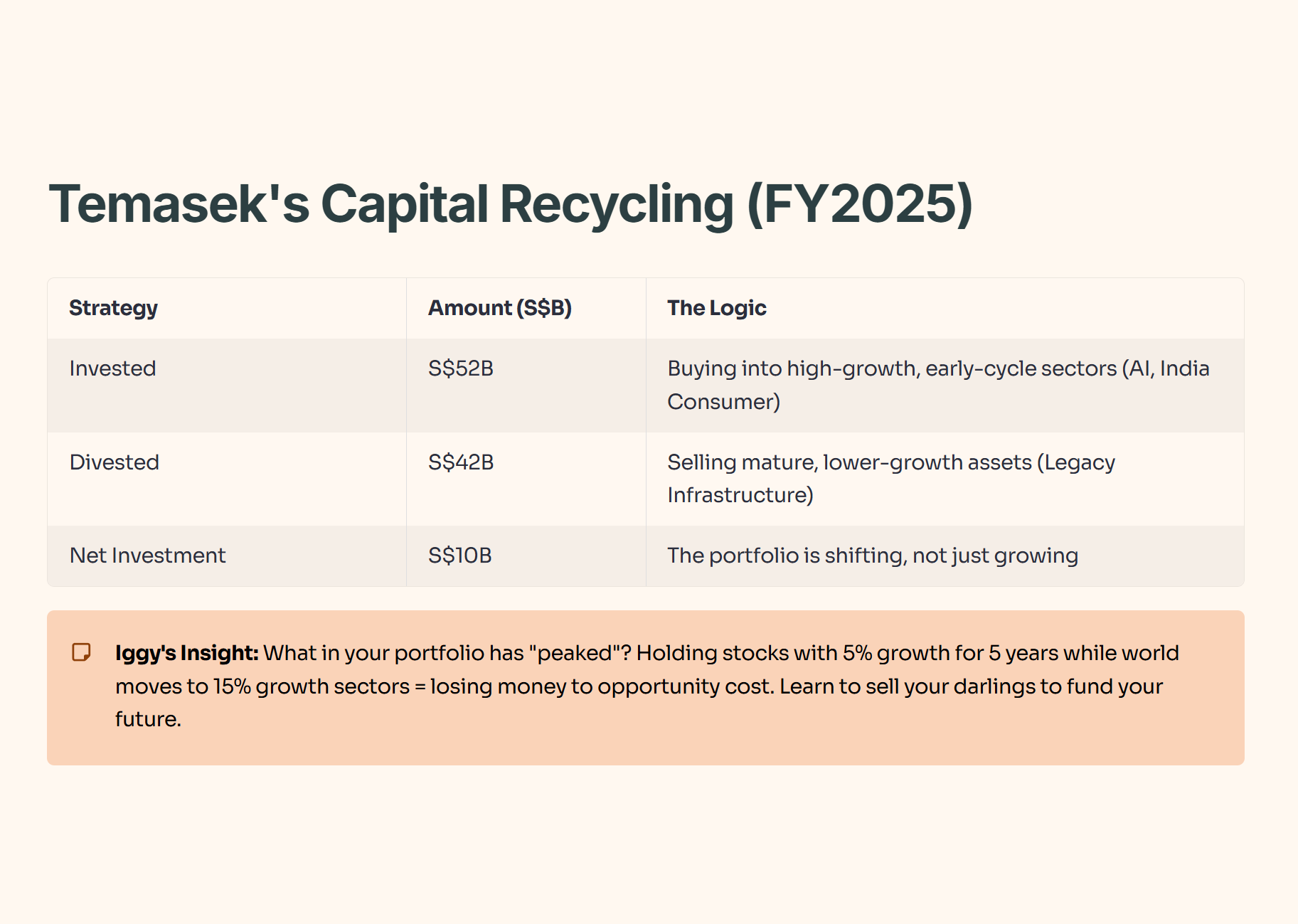

Part 3: The “Capital Recycling” Engine

Here is the most important metric that retail investors ignore: Divestment.

Temasek sold S$42 billion worth of assets this year.

Most retail investors fall in love with their winners. They hold them until they stagnate. Temasek ruthlessly sells mature assets (like Pavilion Energy or mature infrastructure) to free up cash for higher-growth opportunities.

Table 2: Temasek’s Capital Recycling (FY2025)

Iggy’s Insight:

If Temasek is selling S$42B of assets, you need to ask yourself: “What is in my portfolio that has ‘peaked’?” If you are holding stocks that have given you 5% growth for 5 years while the world moves to 15% growth sectors, you are losing money to opportunity cost. Learn to sell your darlings to fund your future.

Part 4: Iggy’s Verdict—The “So What?” for Singapore Investors

So, how do we translate S$434 billion of institutional strategy into a Singaporean’s personal portfolio?