Trump 2.0 vs. SGX: Why Regional Stocks Are The “Kill Zone” 🦖 #1267

While the market obsesses over the US Federal Reserve and the “Trump Trade,” a silent crisis is unfolding in Southeast Asia that directly threatens your SGX dividends.

While the market obsesses over the US Federal Reserve and the “Trump Trade,” a silent crisis is unfolding in Southeast Asia that directly threatens your SGX dividends. Here is the forensic analysis on how the currency crash is hitting Jardine C&C, Delfi, and your favourite S-REITs.

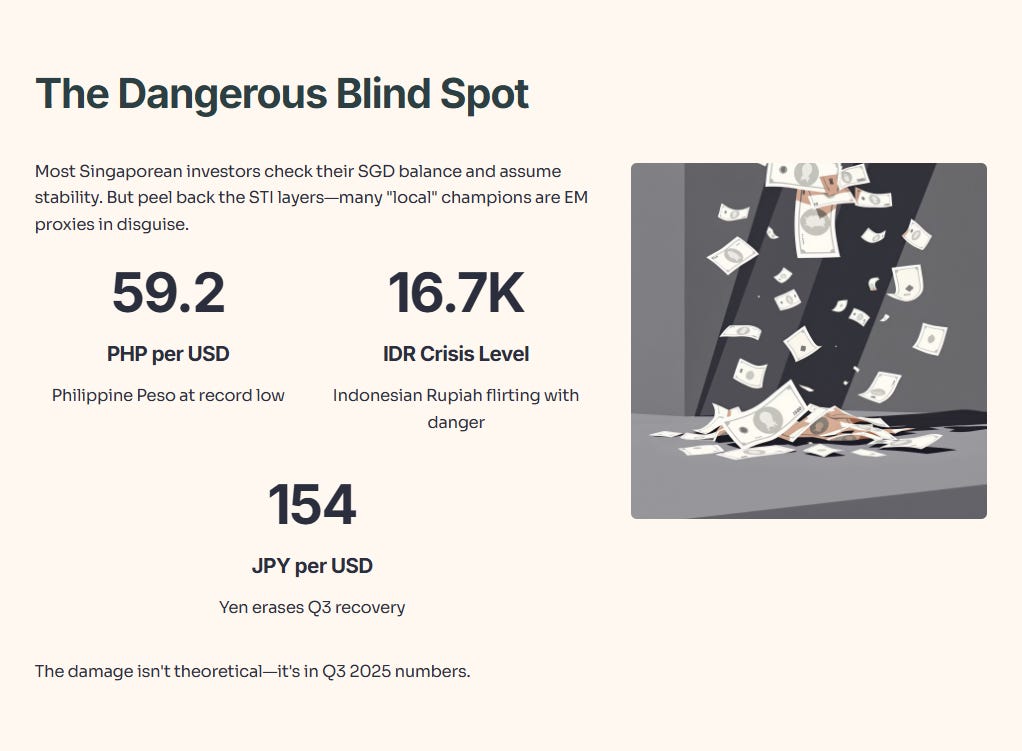

Most Singaporean investors operate with a dangerous blind spot. We look at our portfolio balance in Singapore Dollars ($SGD$) and assume it is stable. But if you peel back the layers of the Straits Times Index (STI), you realize that many of our “local” champions are actually Emerging Market (EM) proxies in disguise.

And right now, those emerging markets are bleeding.

The Philippine Peso ($PHP$) has crashed past 59.2 per USD (a record low). The Indonesian Rupiah ($IDR$) is flirting with crisis levels near 16,700. And perhaps most critically for yield hunters, the Japanese Yen ($JPY$) has slipped back above 154 per USD as of mid-November 2025, erasing the brief recovery we saw in Q3.

I have gone through the latest Q3 and 9M 2025 financial statements released this week. The damage isn’t theoretical anymore—it is in the numbers.

Here is my deep-dive analysis on the mechanics of this crash and which stocks are in the blast zone.

In This Article:

• 🔍 The Macro Context: The “Payback Effect” & The Ghost of 2013

• 🚨 Sector Watch 1: The Regional Conglomerates (The Forensic View)

• 1. Jardine Cycle & Carriage (SGX: C07)

• 2. Delfi Limited (SGX: P34)

• 3. Thai Beverage (SGX: Y92)

• 🏗️ Sector Watch 2: The S-REIT Divergence

• ⚠️ Scenario Analysis: The “Pain Thresholds”

• 🦎 Iggy’s Analyst Playbook: How to Position Now🔍 The Macro Context: The “Payback Effect” & The Ghost of 2013

To understand why your portfolio is taking a hit, we have to look beyond the daily headlines. We are currently witnessing a macroeconomic setup that eerily mirrors the 2013 “Taper Tantrum.”

Back in 2013, when the US Fed hinted at raising rates, capital fled Southeast Asia overnight, crushing the “Fragile Five” economies (including Indonesia). Today, in late 2025, we are seeing a similar dynamic, but with a new catalyst: The “Trump 2.0” Trade.

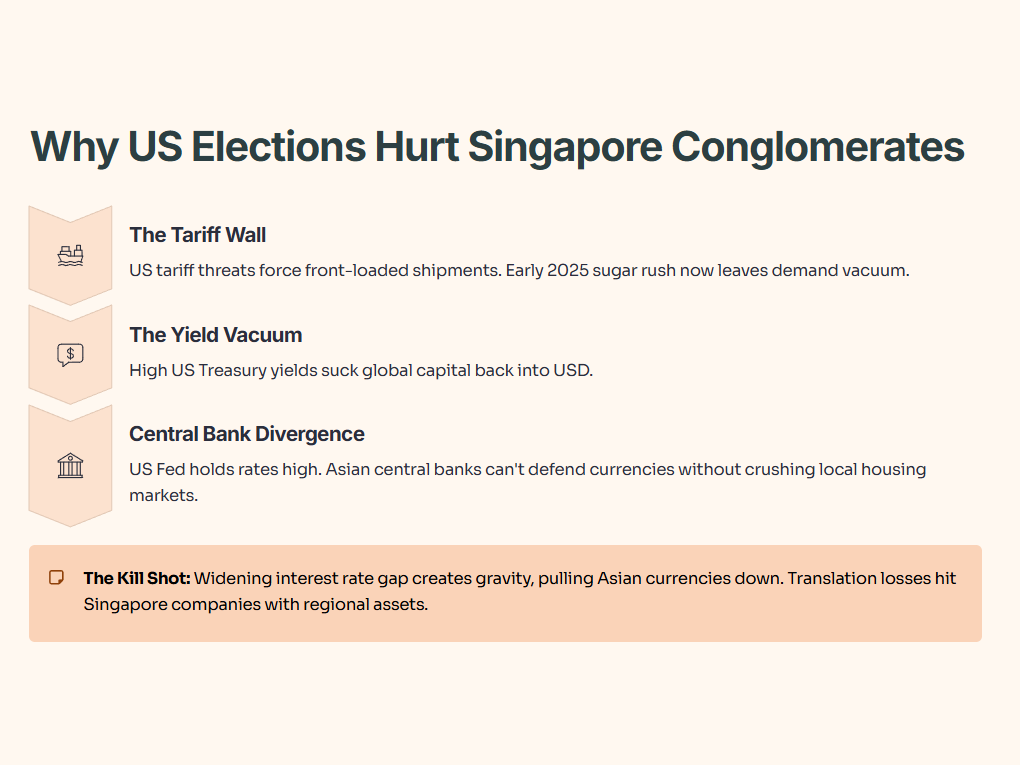

Why does a US election result hurt a Singaporean conglomerate? Connect the dots:

The Tariff Wall: The threat of US tariffs forces Asian exporters to front-load shipments. That “sugar rush” happened in early 2025. Now, the orders are drying up, leaving a vacuum in demand.

The Yield Vacuum: With US Treasury yields remaining stubbornly high (driven by inflation expectations from Trump’s fiscal policies), global capital is being sucked back into the US Dollar.

Central Bank Divergence: This is the kill shot. The US Fed is holding rates high. Meanwhile, Asian central banks (Bank of Indonesia, Bank of Japan) are desperate to stimulate their slowing local economies. They cannot raise rates to defend their currencies without crushing their local housing markets.

The Result: A widening interest rate gap that acts as gravity, pulling Asian currencies down against the Greenback and the Singdollar. For Singapore companies with regional assets, this creates a massive “Translation Loss” headwind.

🚨 Sector Watch 1: The Regional Conglomerates (The Forensic View)

If you own companies that earn in Rupiah or Dong but report in SGD, your earnings are shrinking even if the business is operationally sound. Let’s look at the forensics.

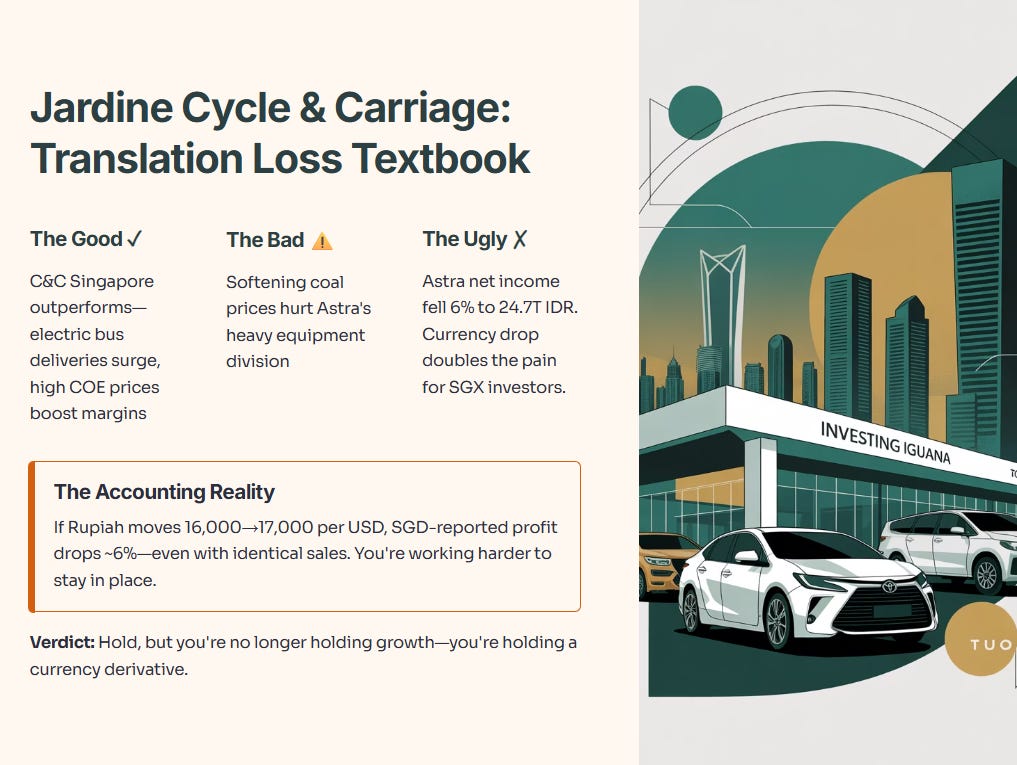

1. Jardine Cycle & Carriage (SGX: C07)

The “Translation Loss” Textbook Case

The News (Nov 10, 2025): JC&C released their Interim Management Statement claiming “underlying profit broadly similar.” However, the market sold the stock down because smart money read the footnotes.

The Forensic Analysis:

The pain is concentrated in Astra International, their Indonesian crown jewel. Astra’s net income fell 6% to 24.7 trillion Rupiah. But for SGX investors, the pain is double. You suffer the operational drop plus the currency drop.

The Good: Cycle & Carriage Singapore is outperforming, driven by a surge in electric bus deliveries and high COE prices.

The Bad: Coal prices have softened, hurting Astra’s heavy equipment division.

The Ugly (The Accounting Reality): This is a classic “Translation Risk.” Even if Astra sells the exact same number of Toyotas next month, if the Rupiah moves from 16,000 to 17,000 against the USD, the profit reported in Singapore Dollars drops by roughly 6%. You are working harder to stay in the same place.

Verdict: Hold, but you are no longer holding a growth stock; you are holding a currency derivative.

2. Delfi Limited (SGX: P34)

The “Double Whammy” Margin Crush

The News (Nov 11, 2025): The “Chocolate King” saw 9M 2025 EBITDA drop 17.1%. This is a sharp reversal from previous years.

The Forensic Analysis:

Delfi is suffering from a brutal mismatch in its currency exposure, known as the “Input/Output Squeeze.”

The Good: People are still eating chocolate. Demand remains relatively sticky.

The Bad: Sales are denominated in Indonesian Rupiah ($IDR$).

The Ugly: The raw material (Cocoa beans) is priced in US Dollars ($USD$). Cocoa prices are already at record highs due to supply shortages. When the IDR crashes against the USD, Delfi pays more for beans but collects less value from chocolate bars. This destroys Gross Profit Margins (down 130 basis points).

Verdict: The stock looks “cheap” on P/E, but it is a value trap until the USD/IDR exchange rate stabilizes.

3. Thai Beverage (SGX: Y92)

The Vietnam Drag

The Situation: ThaiBev’s Spirits division, the strongest part of the business, saw a 5.4% drop in EBITDA. At first glance, this looks like a performance issue with their core brands, but the real trouble is hiding in the numbers.

The Forensics: SABECO and Currency Risk

ThaiBev owns a giant chunk of SABECO, Vietnam’s biggest brewer.

SABECO sells huge amounts of beer in Vietnam, mostly priced in Vietnamese Dong (VND).

In 2025, the VND lost even more value. Why? Vietnam’s central bank devalued the currency to make its exports cheaper and more attractive globally, especially with new international trade risks and a strong US Dollar .

Every time SABECO earns revenue in VND, that income shrinks when they convert it to Thai Baht, and shrinks again when it’s reported in Singapore Dollars (SGD).

SABECO’s Q3/2025 numbers show this pain: revenues fell 16% year-on-year, despite net profit making a short-term jump due to lower raw material costs. The drop in revenue is mostly linked to currency and weaker market demand, not operational issues alone.

Verdict: looks weaker on paper this year, but the real culprit is currency risk from its Vietnam business. SABECO’s beer profits in Vietnamese Dong turn into smaller returns when exchanged for Thai Baht and Singapore Dollars. That means even if sales stay strong locally, ThaiBev’s reported profits drop. For investors, this “currency drag” is a silent portfolio killer—masking solid operations with weak results.

🏗️ Sector Watch 2: The S-REIT Divergence

The Q3 2025 earnings season has created a massive divergence between “Singapore Pure Plays” and “Regional Bets.”

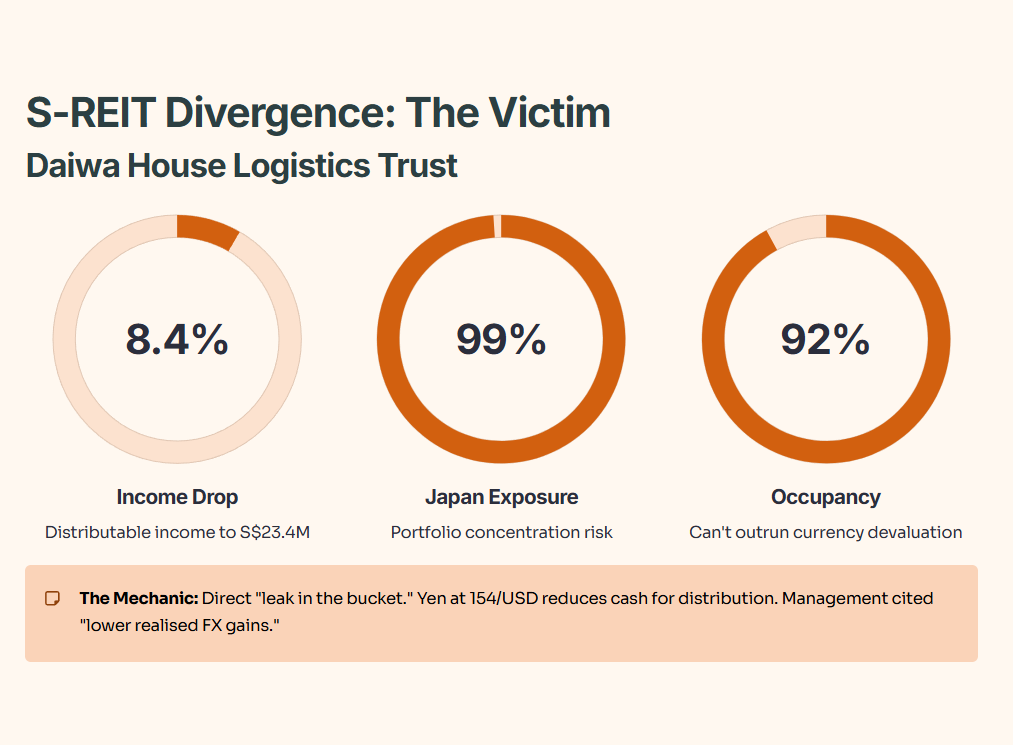

The Victim: Daiwa House Logistics Trust (SGX: DHLU)

The Result: Distributable income dropped 8.4% to S$23.4 million.

The Mechanic: Daiwa House Logistics Trust is showing the classic signs of a currency squeeze. Despite maintaining high occupancy (about 92%) and solid asset performance in Japan, distributable income dropped 8.4% to S$23.4 million. The main reason? The Japanese Yen sank to 154/USD, slicing into the real cash Singapore investors get back. Even tight cost controls and new tenant signings can’t offset this. Management noted “lower realised foreign exchange gains,” reminding us that even strong asset operations can be completely undone when the local currency moves the wrong way. For investors, it’s a direct hit: you’re earning less, not because of poor management, but because of the relentless power of currency devaluation.

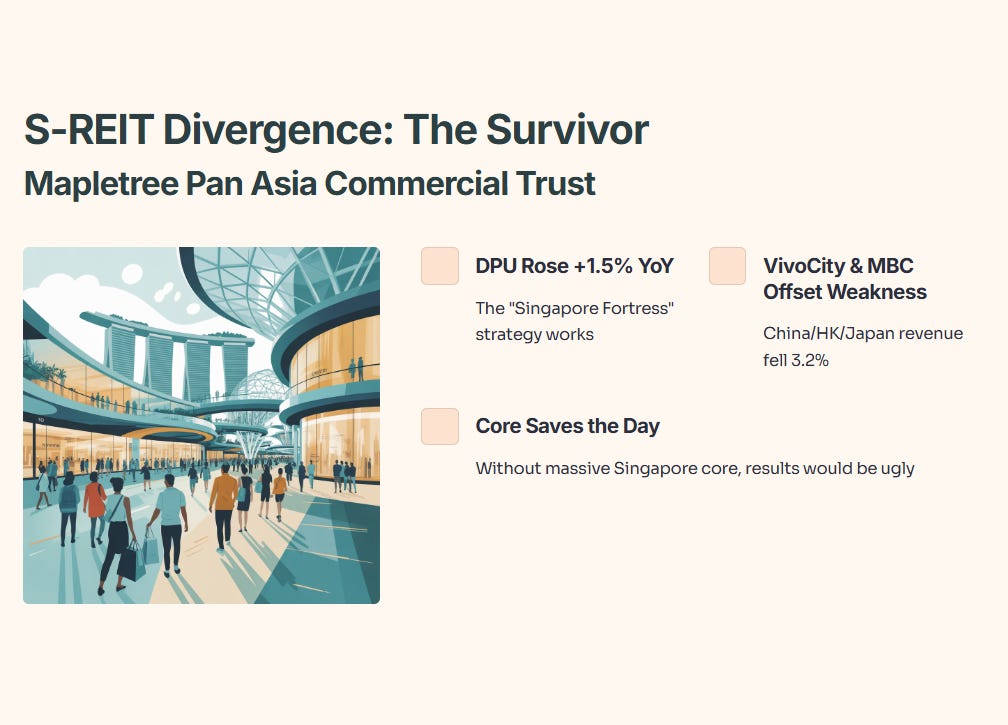

The Survivor: Mapletree Pan Asia Commercial Trust (SGX: N2IU)

The Result: DPU rose slightly (+1.5% YoY).

The Mechanic: Mapletree Pan Asia Commercial Trust managed a small DPU increase (+1.5% YoY), bucking the regional trend. The key driver was strong performance from its Singapore assets—VivoCity and Mapletree Business City delivered more income, acting as a buffer against falling revenue from overseas holdings (China, Hong Kong, Japan, down 3.2%). If not for its solid “Singapore Fortress” foundation, the results would have taken a big hit. The trust’s heavy domestic exposure is what kept earnings healthy in a tough currency and market climate.

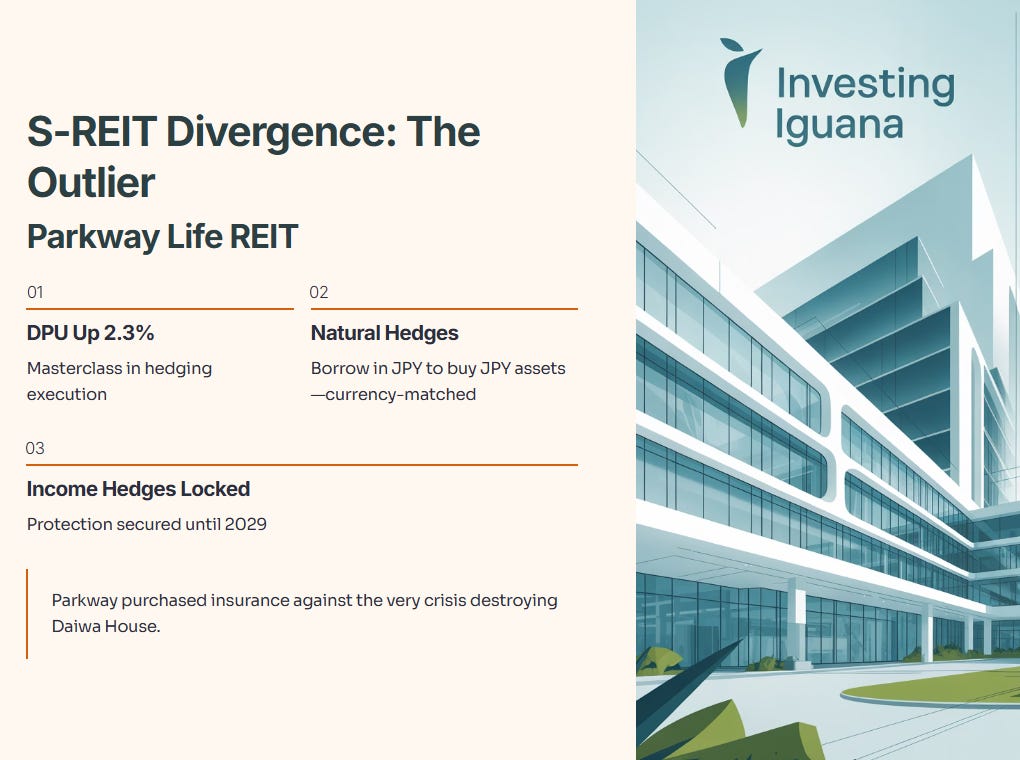

The Outlier: Parkway Life REIT (SGX: C2PU)

The Result: DPU up 2.3%.

The Mechanic: Parkway Life REIT delivered a 2.3% increase in DPU by showing real skill in risk management. The trust uses “natural hedges”—it borrows in Japanese Yen to buy Japanese assets—so currency swings don’t hurt its income. Plus, Parkway has hedged most of its income out to 2029, giving it locked-in protection. While others like Daiwa House suffer from Yen weakness, Parkway’s careful hedging acts like insurance against currency shocks, directly shielding its cash distributions for investors.

⚠️ Scenario Analysis: The “Pain Thresholds”

We cannot predict the exact exchange rate tomorrow, but we can identify the breaking points. Here are the levels where “uncomfortable” becomes “critical” for your portfolio.

Scenario Analysis: The Pain Thresholds

Every portfolio has hidden red lines—points where currency moves flip from annoying to outright destructive. For Japanese assets, the critical USD/JPY rate is above 160. At this level, energy import costs surge, pressuring the Bank of Japan for frantic interventions. Unhedged Japanese REITs, like Daiwa House Logistics Trust , would see double-digit declines in their cash distributions, putting investor income at real risk. Hedged names, such as Parkway Life REIT , can absorb this shock, but anyone without protection is exposed.

In Indonesia, USD/IDR crossing 17,000 signals panic for major companies dependent on consumer demand, especially Astra . The central bank would likely jack up interest rates to defend the currency, knocking down affordability for cars and loans, and causing ripple effects across corporate earnings.

For Singapore’s property trusts, a USD/SGD above 1.40 means persistent interest rate pain. High leverage exacerbates this, as SOR/SORA rates remain elevated and financing costs bite deeper into DPU. REITs carrying more than 40% gearing risk payout declines as their debt costs rise faster than growth in rental income or asset values. In sum, each “pain threshold” is a warning: ignore these inflection points and portfolio returns can quickly move from stable to unstable.