SGX Alert: The Valuation Trap in "Safe" Stocks

Sheng Siong and CapitaLand Ascott Trust just entered the “waiting room.” Here’s why smart money is watching them closely.

The headlines for the December 2024 STI review were delightfully boring: “No Changes to Top 30 Constituents.”

If you are a passive investor just dollar-cost averaging into the ES3 or G3B ETFs, you probably shrugged and went back to your coffee. But if you care about where institutional capital flows before it hits the mainstream news, you just missed the most important signal of the quarter.

While the main index stood still, the Reserve List—the exclusive five-stock waiting room for the STI—underwent a significant surgical procedure. Olam Group and Yangzijiang Financial were cut. Sheng Siong and CapitaLand Ascott Trust (CLAS) were drafted in.

Why does this matter? Because the Reserve List isn’t just a “backup plan.” It is a watchlist for liquidity. When a stock enters this list, it forces fund managers, shadow-indexers, and institutional desks to pay attention.

Let’s break down the mechanics of this rotation and what it implies for your portfolio strategy in 2025.

In This Article:

• The New Reserve List Hierarchy

• Iggy’s Insight:

• Sheng Siong: The Boring Wealth Compounder

• Iggy’s Insight: The data confirms a classic “quality premium” problem.

• CapitaLand Ascott Trust (CLAS): The Comeback Kid

• Iggy’s Insight:

• The Exits: Why Olam and Yangzijiang Were Dropped

• Valuation Reality Check: The Analyst vs. Math Battle

• Iggy’s Insight: This image is a warning shot. Look at the divergence:

• The Investor’s Playbook: What To Do Now

The New Reserve List Hierarchy

For the uninitiated, the Reserve List consists of the five highest-ranking non-constituents by market capitalization. If any of the top 30 drop out (due to privatization, delisting, or collapse), the top name here gets the call-up.

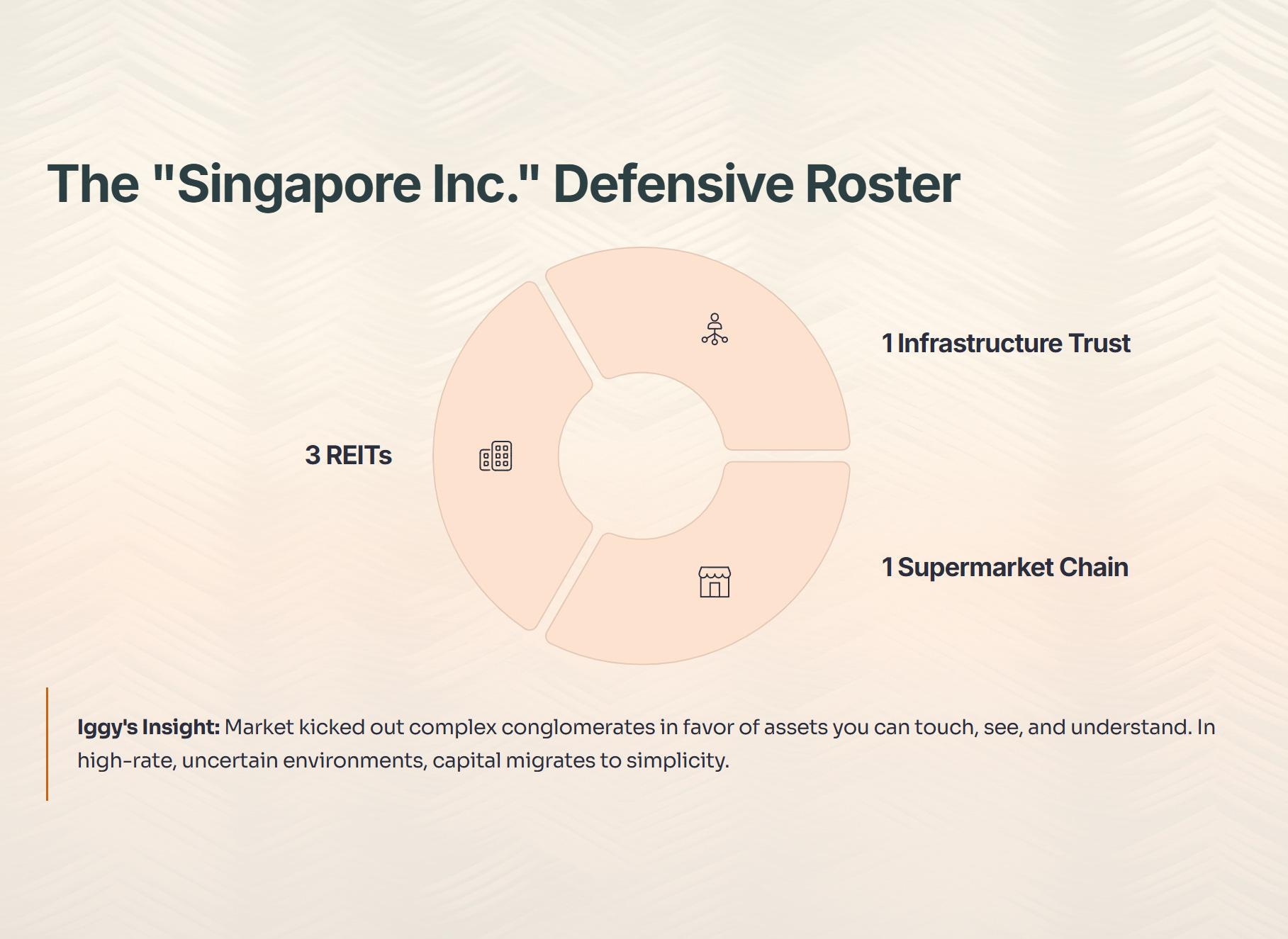

Here is the refreshed lineup effective December 23, 2024:

Iggy’s Insight:

Notice the composition here? Three REITs, one Infrastructure Trust, and one Supermarket chain. This is the “Singapore Inc.” defensive roster. The market effectively kicked out the complex conglomerates (Olam) and opaque financial holdings (Yangzijiang) in favor of assets you can touch, see, and understand. In a high-rate, uncertain environment, capital migrates to simplicity.

Sheng Siong: The Boring Wealth Compounder

Sheng Siong entering the reserve list is a validation of its “slow and steady” approach. But investors need to be careful: Good Company ≠ Good Stock Price.

Many investors ignore Sheng Siong because it lacks “excitement.” It doesn’t have AI exposure. It doesn’t have a flashy overseas expansion plan. It just sells groceries in the heartlands.

But here is why the Reserve List inclusion matters: Visibility. Foreign institutions often screen Singapore for “Blue Chip” proxies. By sitting on the Reserve List, Sheng Siong now appears on screens that filter for “Near-Large Cap” liquidity.

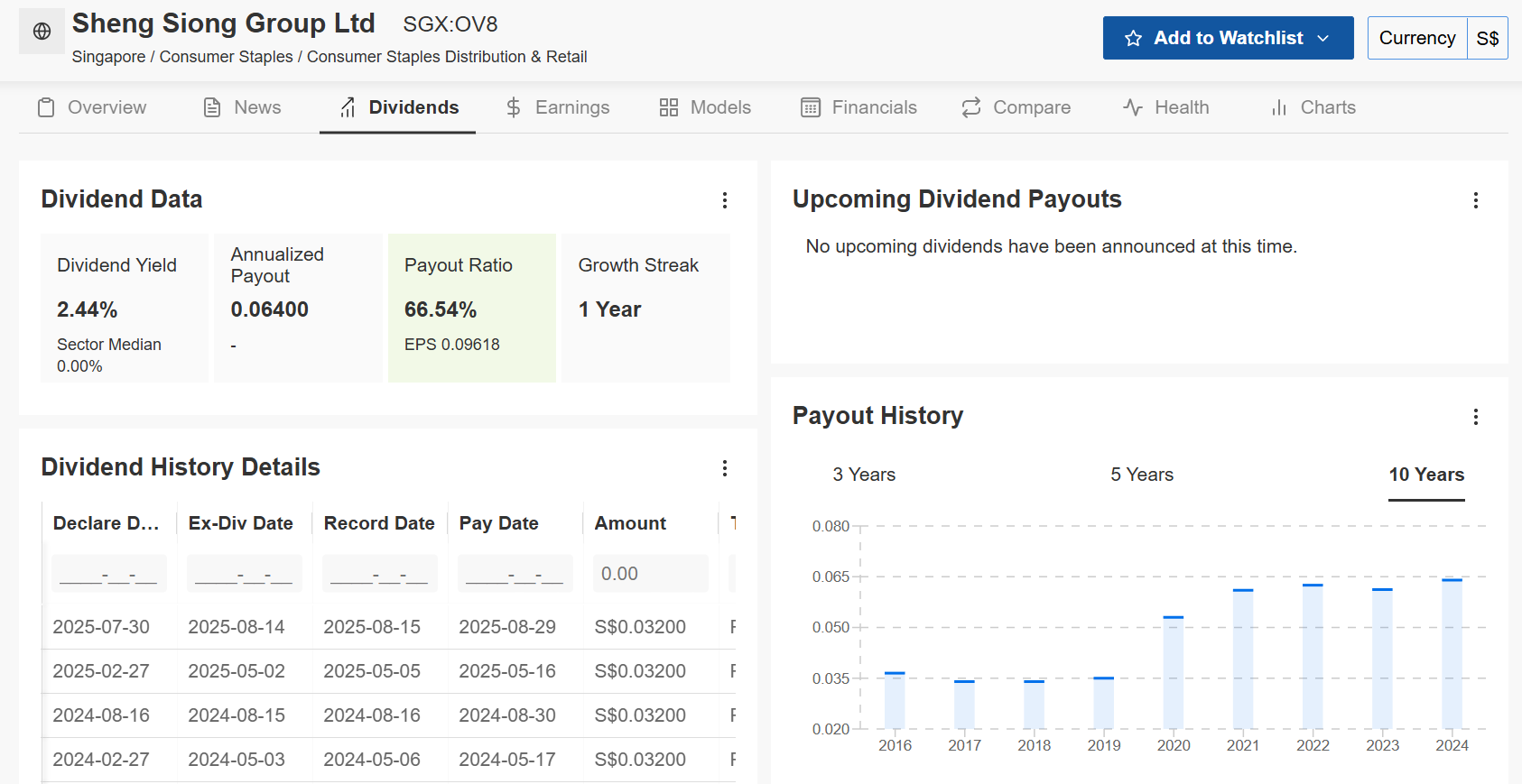

Is the dividend actually safe? Let’s look at the health score and dividend data.

Source: InvestingPro by Investing.com (Data as of December 2024). Premium members can use code INVESTINGIGUANA for up to 50% off.

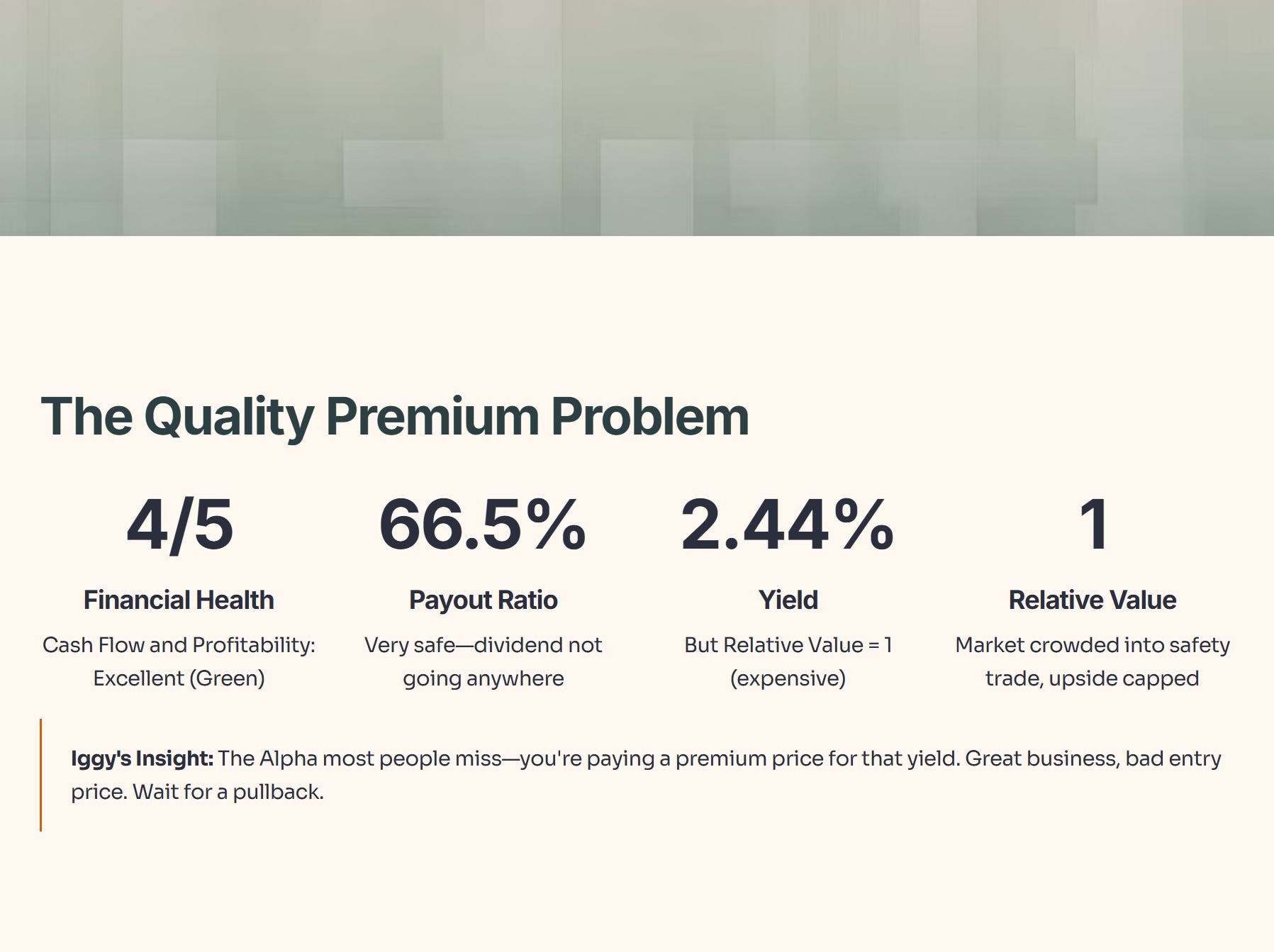

Iggy’s Insight: The data confirms a classic “quality premium” problem.

Look at the Financial Health (4/5). The Cash Flow and Profitability scores are excellent (Green), and the Payout Ratio is a very safe 66.5%. This dividend is not going anywhere.

HOWEVER, look at the red box on the far right: Relative Value is a 1.

This is the “Alpha” most people miss. The market has already crowded into this trade for safety, pushing the valuation up until it is mathematically expensive. You are paying a premium price for that 2.44% yield. The Reserve List news might pump the price further, but at a “Relative Value” of 1, the upside is capped.

Verdict: Great business, bad entry price. Wait for a pullback.

CapitaLand Ascott Trust (CLAS): The Comeback Kid

CLAS is an interesting case. It exited the list in September 2024, only to claw its way back in by December. This volatility in its ranking reflects the market’s tug-of-war regarding hospitality REITs.

On one hand, RevPAU (Revenue Per Available Unit) has been recovering as global travel normalizes. On the other hand, the high-interest-rate environment punishes REITs with global portfolios due to currency headwinds and refinancing costs.

The fact that CLAS beat out Olam to reclaim its spot suggests that the market capitalization has stabilized relative to the agribusiness giant. It signals that the “sell-down” in hospitality REITs may have found a floor.

Iggy’s Insight:

Don’t conflate “Reserve List Entry” with “Immediate Buy.” CLAS is sensitive to global macroeconomics. If the US goes into a hard recession, travel budgets get cut, and CLAS suffers. However, its presence here makes it the liquidity leader for the hospitality sector. If you want exposure to travel recovery without betting on a risky airline, this is the institutional pick.

The Exits: Why Olam and Yangzijiang Were Dropped

We need to talk about the losers. Olam Group and Yangzijiang Financial (YZJ Fin) were removed.

1. Olam Group: The complexity penalty. Olam is undergoing massive restructuring, spinning off Olam Agri and Olam Food Ingredients. The market hates uncertainty. Until the corporate structure is crystal clear, institutional capital demands a discount.

2. Yangzijiang Financial: The “Black Box” problem. Unlike YZJ Shipbuilding (which builds ships—simple), the Financial arm is an investment holding company. Valuing it requires trusting the valuation of its underlying private investments. In this market climate, investors prefer the tangible cash flow of a supermarket (Sheng Siong) over the theoretical book value of a financial investment firm.

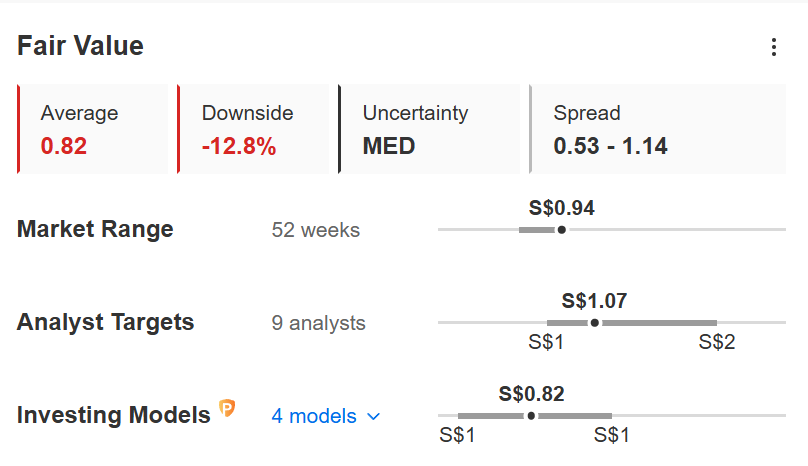

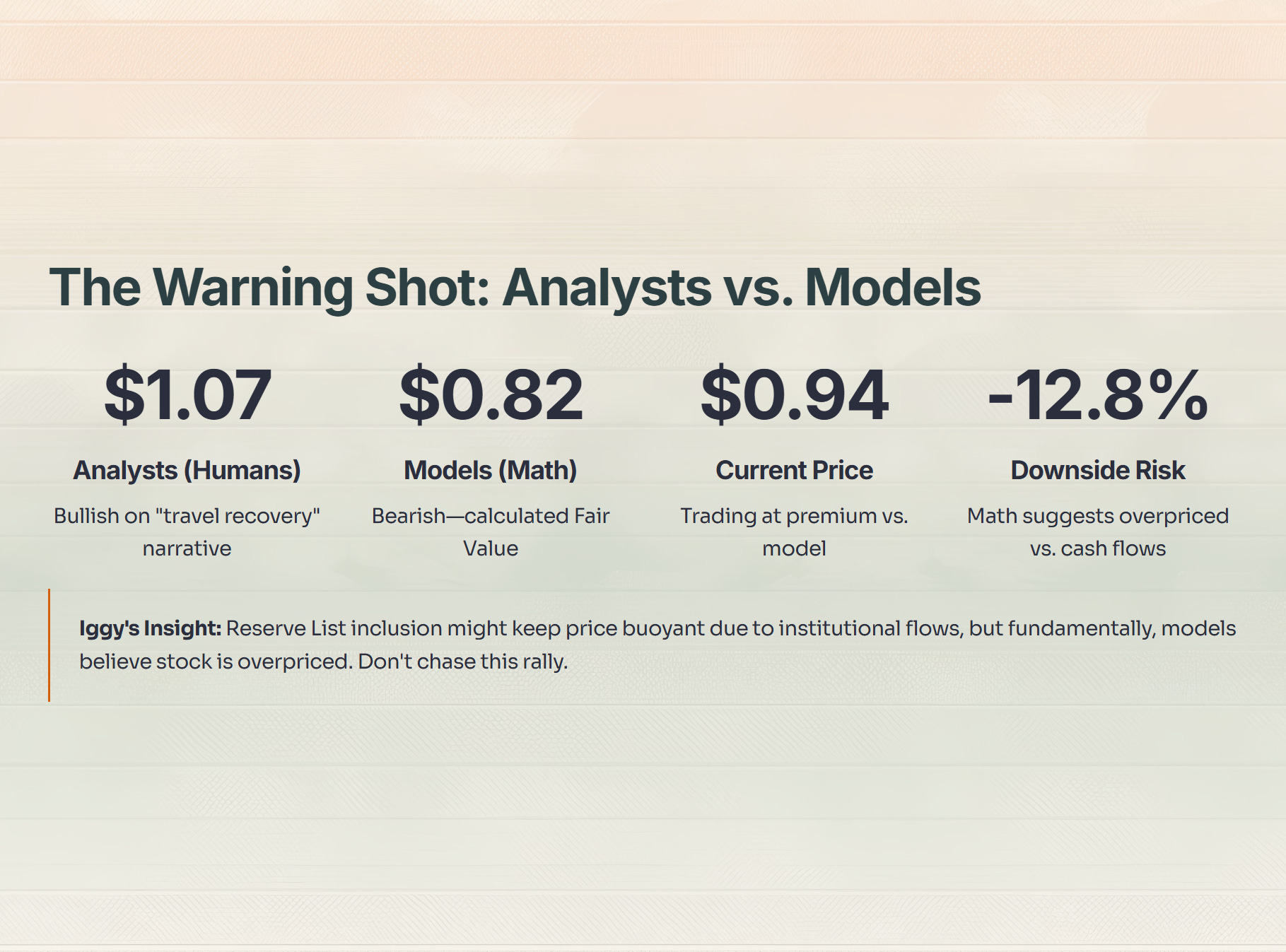

Valuation Reality Check: The Analyst vs. Math Battle

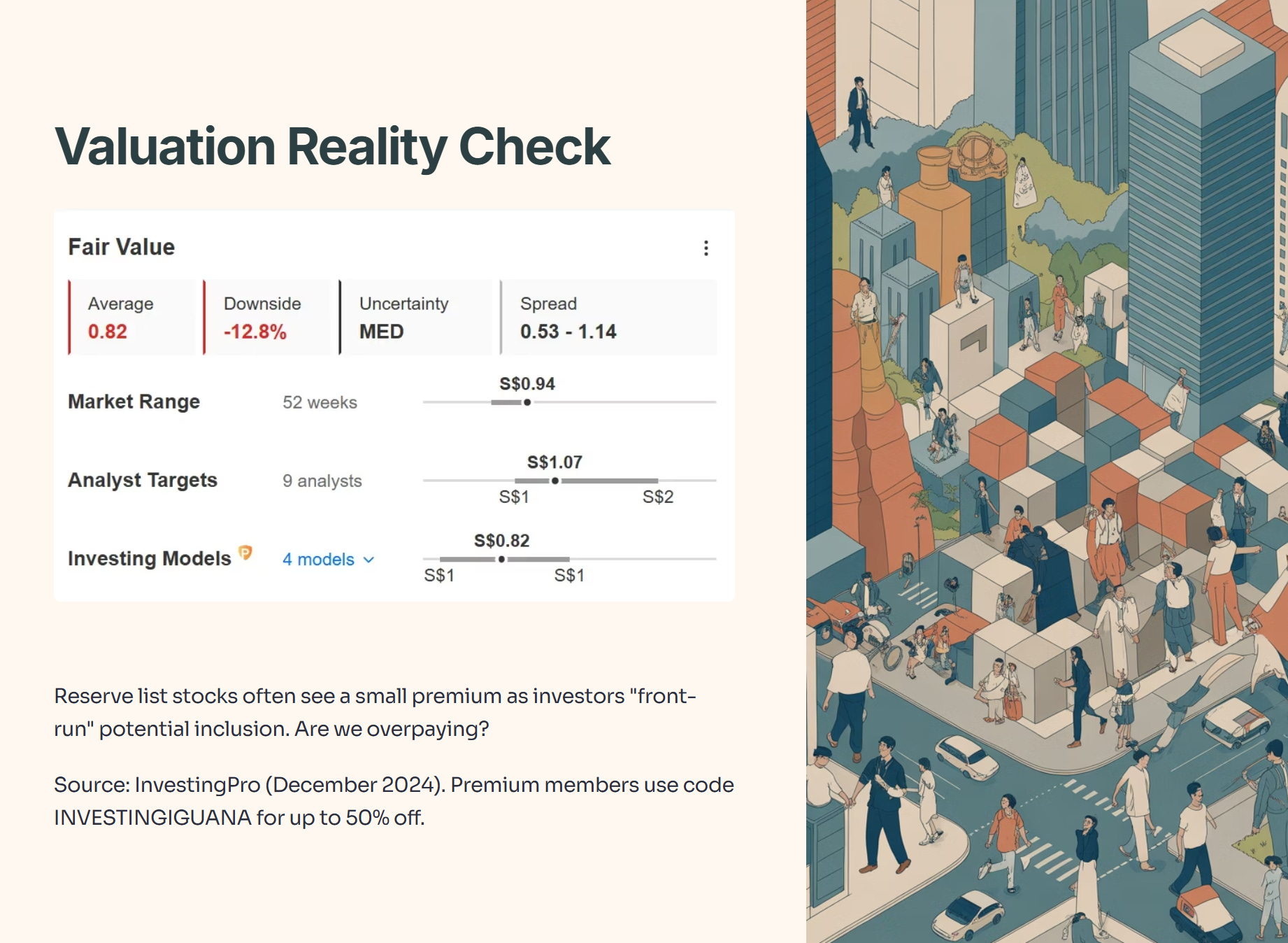

We know the story behind CapitaLand Ascott Trust’s return to the list, but is the price right? This is where retail investors usually get hurt—they follow the “Buy” ratings from brokerages without checking the raw numbers.

I ran the valuation models to see if the current price of S$0.94 is justified.

Source: InvestingPro by Investing.com (Data as of December 2024). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Insight: This image is a warning shot. Look at the divergence:

The Analysts (Humans): They are bullish, with an average target of S$1.07. They are betting on the “travel recovery” narrative.

The Models (Math): They are bearish, calculating a Fair Value of only S$0.82.

Who is right? The stock is currently trading at S$0.94. That means if you buy today, you are paying a premium against the model’s fair value. The math suggests a -12.8% downside.

The Reserve List inclusion might keep the price buoyant for a while due to institutional flows, but fundamentally, the models believe the stock is overpriced relative to its cash flows. Do not chase this rally.

The Investor’s Playbook: What To Do Now