The Singapore AI Advantage: 7 Companies to Eyeball NOW

Most Singaporean investors are missing the AI goldmine hiding in plain sight on the SGX - here's your complete playbook to capture this $4.64 billion opportunity before institutional money floods in

The Singapore AI Advantage

Most investors think AI = US mega-cap tech. That narrow view leaves a lot of money on the table. Singapore has built the rails that AI needs to run: power, connectivity, and data centers. This market-driven base creates investable cash flow today, not just far-off promise. The result is a set of SGX-listed names that tie directly to AI’s rising compute needs, with solid yields and room for re-rating.

Why This Market Beats Hong Kong and Tokyo

Singapore is a central hub for global AI infrastructure deals. While customer billing records show up to 18–22% of NVIDIA’s global revenue is ‘assigned’ to Singapore, this mainly reflects how global customers use Singapore as an invoicing base. Actual hardware shipped into Singapore is far smaller (less than 2%), but the billing numbers underline Singapore’s importance as a strategic center for AI purchasing and distribution. If calculated on ‘revenue assigned,’ it suggests over $600 per capita—though much of that demand is regional, not local.

The government's National AI Strategy 2.0, launched in December 2023, commits over S$1.6 billion in funding while attracting $26 billion in tech giant investments. This isn't just government spending - it's strategic infrastructure development that creates sustainable competitive advantages.

Singapore’s AI market is growing rapidly—estimates range from $1 billion in 2024 to between $4.6 billion and as much as $16 billion by 2030, depending on the forecast source. Compound annual growth rates are commonly listed at 28%–42%, with some industry analysts projecting even faster expansion for generative AI solutions.

But unlike other AI hubs, Singapore offers something unique: immediate liquidity through SGX-listed companies that provide direct exposure to this growth story.

In this piece, I’ll do three things:

Map the AI value chain to SGX stocks with real exposure

Give clear Buy/Hold calls and entry tactics for CPF/SRS

Lay out risks, second-order effects, and a step-by-step action plan

I’ve spent the last cycle working with Singaporean portfolios through several tech booms. The edge here is the blend of infrastructure cash flows and cyclical chip leverage. If the US is the brain of AI, Singapore is the spine. Let’s build around that spine.

The Hidden Champions on SGX You Can Buy Today

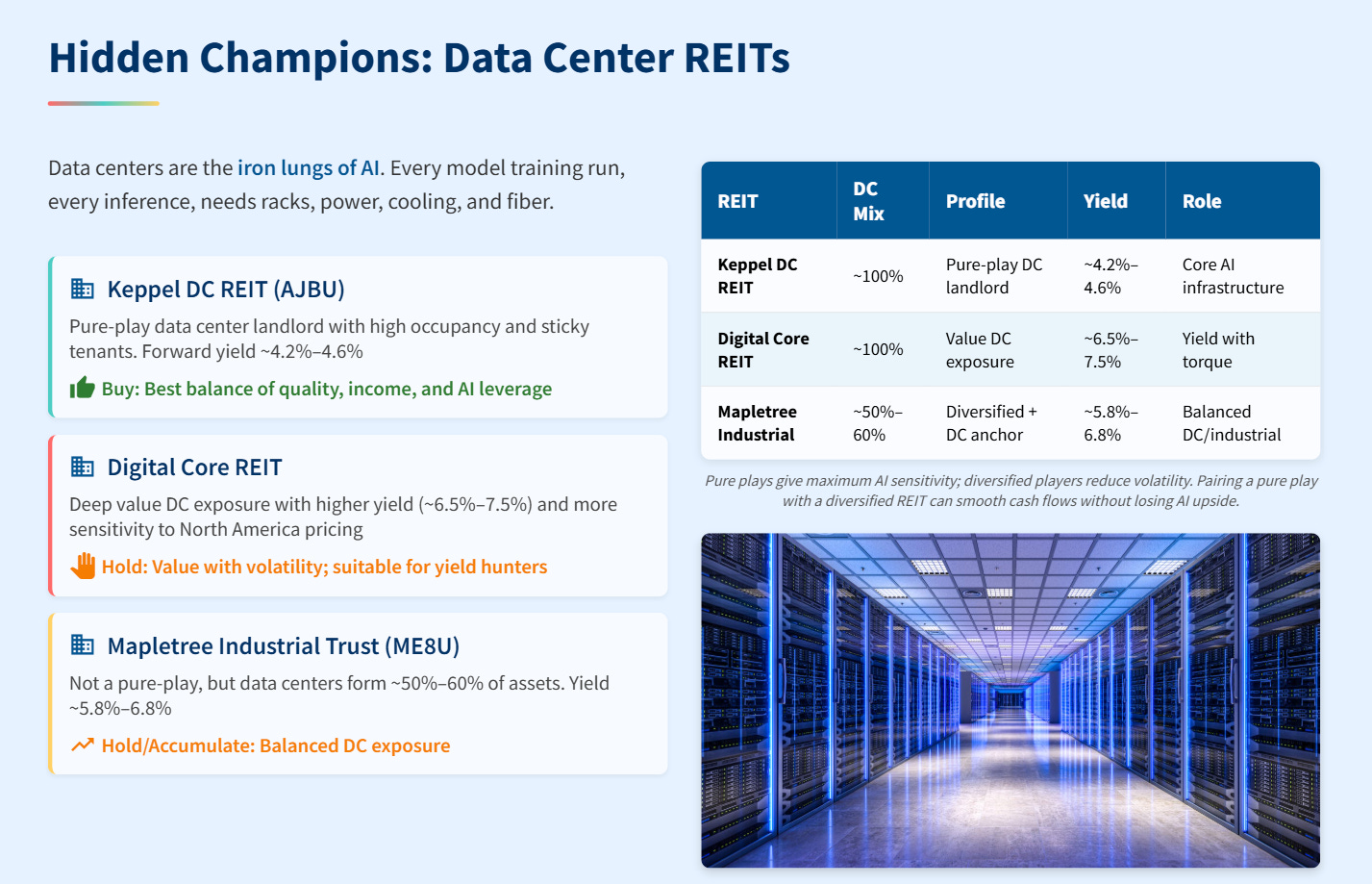

Data Center REITs: The AI Powerhouses

This table compares the key DC REITs on yield, DC mix, and role in an AI strategy. It helps investors choose between pure-play growth (Keppel DC), deep value (Digital Core), and a balanced REIT (Mapletree Industrial).

Data centers are the iron lungs of AI. Every model training run, every inference, needs racks, power, cooling, and fiber. That’s why local DC REITs sit at the center of this theme.

Keppel DC REIT (AJBU): Pure-play data center landlord with high occupancy and sticky tenants. Forward yield sits around the mid-4% range based on recent pricing. Leases have built-in escalations. DC capacity demand keeps rising as training and inference scale. Current price around S$2.31 offers attractive entry, especially considering the REIT's portfolio occupancy remains high at 95.8% with a healthy weighted average lease expiry of 6.9 years. Based on the closing price of S$2.330 per unit on 30 June 2025, the annualized distribution yield would be 4.41%.

Digital Core REIT (USD counter available): Digital Core REIT (DCRU) trades at deep value, with a forecast 2025 yield closer to 7.9%…, though it's suffered from market pessimism with a -30.92% three-year performance. However, recent strategic moves, including the acquisition of a 20% stake in an Osaka data center for US$86.7 million, signal management's commitment to growth.

Mapletree Industrial Trust (ME8U): Not a pure-play, but data centers form a large share of assets. This gives a balance between DC growth and industrial stability.

Buy/Hold:

Keppel DC REIT — Buy: Best balance of quality, income, and AI leverage.

Digital Core REIT — Hold: Value with volatility; suitable for yield hunters with strong stomachs.

Mapletree Industrial Trust — Hold/Accumulate on dips for diversified DC exposure.

Pure plays give maximum AI sensitivity; diversified players reduce volatility. Yield spreads reflect risk, tenant mix, and geography. Pairing a pure play with a diversified REIT can smooth cash flows without losing AI upside.