The Ultimate Sembcorp 1H2025 Results Deep Dive: Is This Your Next Power Play?

Most investors saw falling revenue and a sharp sell-off. The better story is a business shifting to higher-quality earnings with a larger renewables engine and a stronger dividend.

Most investors saw falling revenue and a sharp sell-off. The better story is a business shifting to higher-quality earnings with a larger renewables engine and a stronger dividend. This post breaks down the 10 most important slides, quantifies what matters, and ends with a clear call: buy, hold, or sell, and at what price.

Why This Matters Now

Sembcorp is not the same utility it was three years ago. It now runs a barbell model: stable gas and power in Singapore on one side, fast-growing renewables in India, China, and ASEAN on the other. That mix can smooth earnings in down cycles and compound value in up cycles. The 1H2025 print showed both sides working. Revenues fell, but underlying profit held. The dividend stepped up. The renewables machine scaled again.

In this deep dive, we unpack what the market missed, where the risks lie, and how to size a position. We will look at cash flow durability, renewables execution, China curtailment, India project quality, and capital allocation. Then we'll map these into a valuation range and a price target with buy/hold/sell guidance.

The 10 Slides That Matter, Decoded

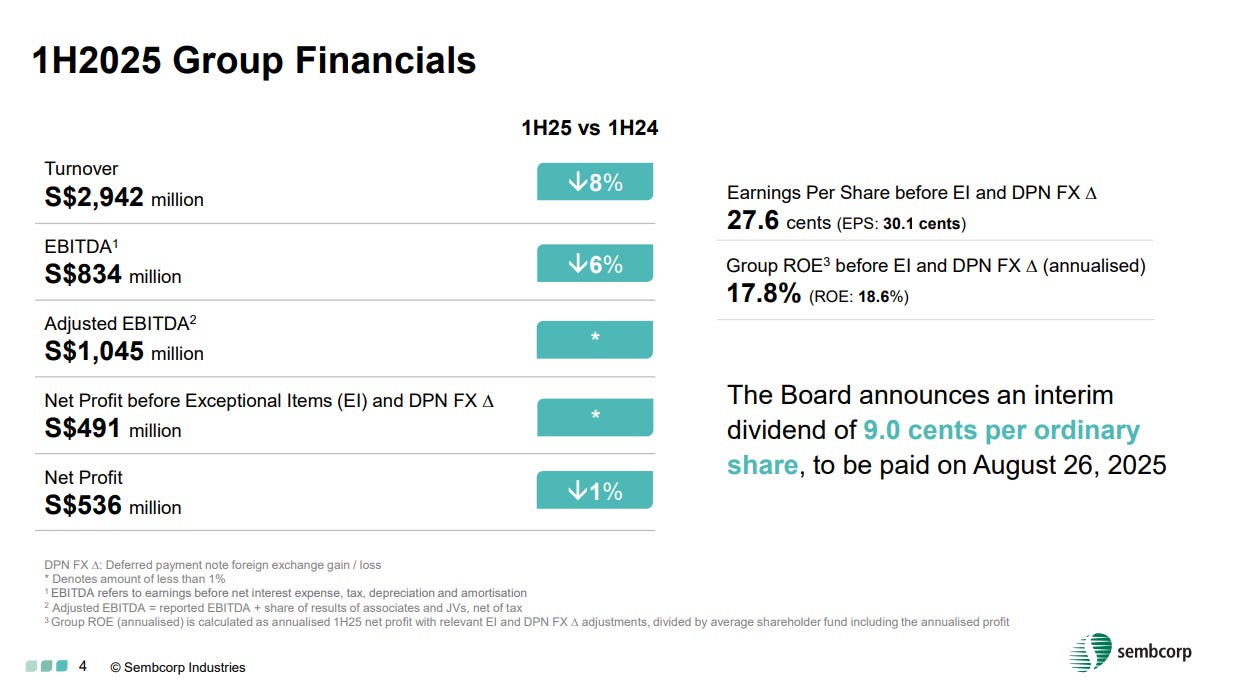

1) Group Financial Overview - Slide 4: Key Financials

Revenue fell 8% but underlying profit held steady at S$491 million versus S$489 million in 1H2024. That reads like a firm in control of its mix and costs, not one losing its edge. The interim dividend jumped 50% to 9 cents per share.

Key metrics: Turnover S$2.94 billion (down 8%), EBITDA S$834 million (down 6%), Net profit S$536 million (down 1%), EPS 30.1 cents (down 1%). ROE before exceptional items was 17.8%.

Why it matters: This is steady execution in a soft power price environment. The 50% dividend lift suggests confidence in cash flows. For a utility-transition name, that is a strong signal.