STOP Trading ASEAN 'Growth at All Costs': The Governance Trap Hiding in Your REITs 🦖 EP1289

The headline screams “Geopolitics,” but the balance sheet screams “Governance.” Here is why the Jakarta-Bandung railway debacle matters for regional risk premiums and Singaporean capital.

Right now, headlines are dominated by Indonesia’s “Whoosh” high-speed rail. The narrative is simple: China trapped Indonesia in debt.

But if you look closer, that narrative is wrong. And believing it is dangerous for your portfolio.

The real story involves cost overruns, a corruption probe launched in October 2025, and a governance breakdown in Jakarta. For Singaporean investors with exposure to ASEAN markets, regional banks, or infrastructure plays, this isn’t just political drama. It is a case study in Governance Risk.

Let’s strip away the noise and look at the numbers.

In This Article:

• The Whoosh: Operational Success, Financial Black Hole

• The Governance Gap

• The Regional Ripple Effect: Why Singapore Investors Should Care

• The “Debt Trap” vs. The “Governance Trap”

• What To Do Next

• The Verdict

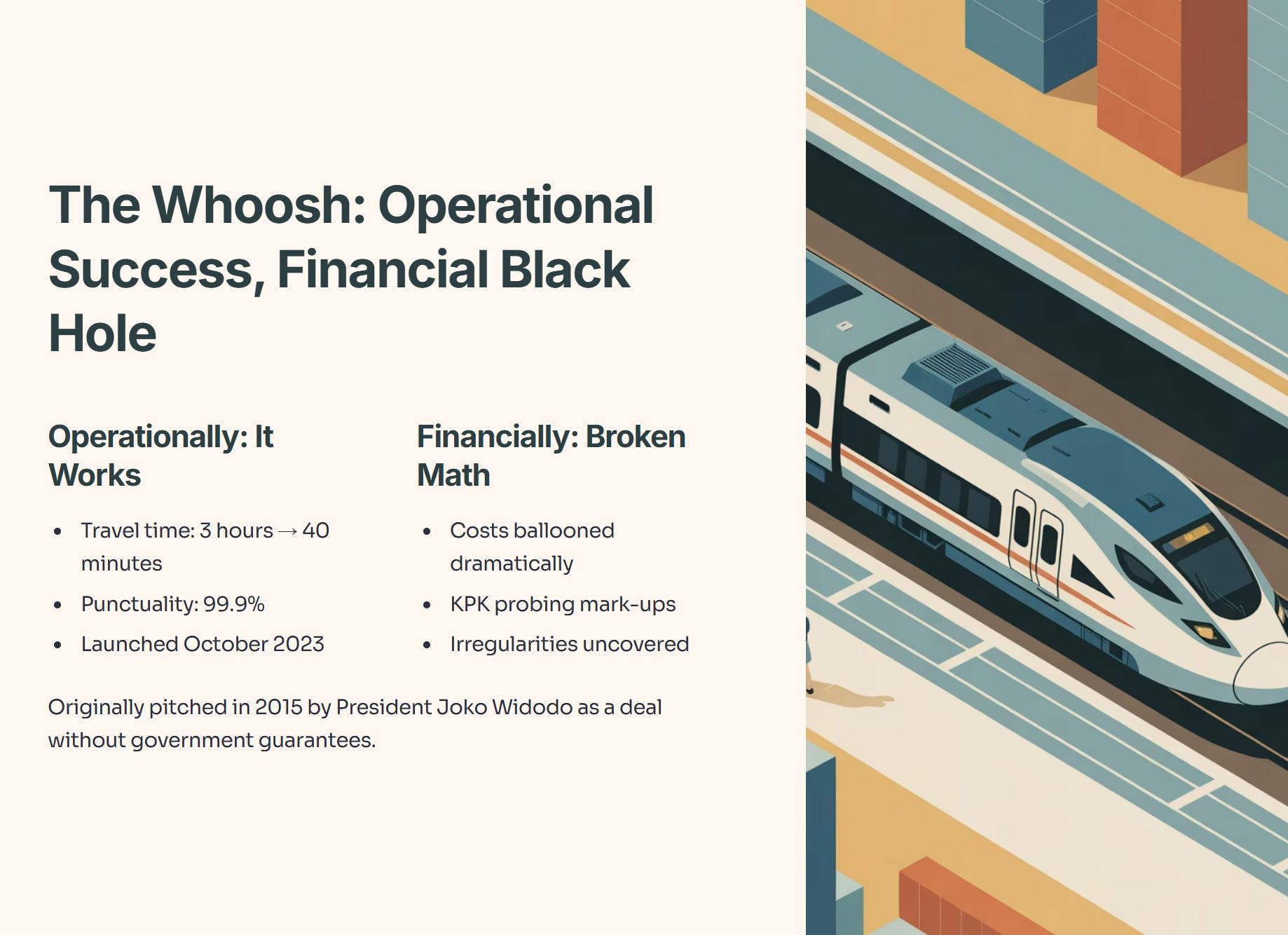

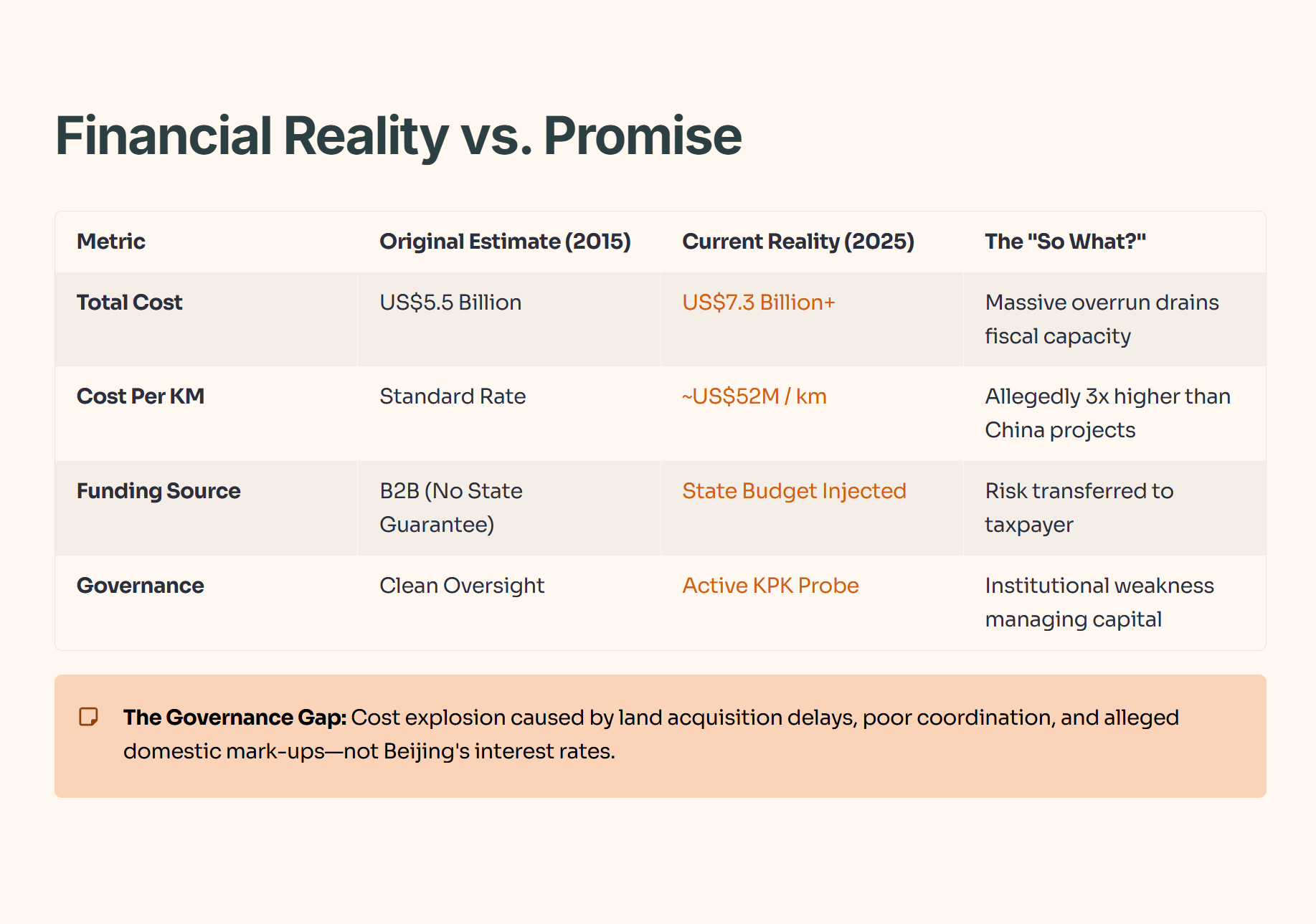

The Whoosh: Operational Success, Financial Black Hole

In October 2023, the Jakarta-Bandung “Whoosh” launched to genuine fanfare. Operationally, it works. It cuts travel time from three hours to 40 minutes and boasts 99.9% punctuality.

Financially, however, the math is broken.

The project was originally pitched in 2015 by President Joko Widodo as a pragmatic deal: China would build it without government guarantees. Fast forward to today, and the costs have ballooned, leading to a probe by Indonesia’s Corruption Eradication Commission (KPK) into mark-ups and irregularities.

Here is the financial reality vs. the promise:

The Governance Gap

The cost explosion wasn’t caused by Beijing’s interest rates. It was caused by land acquisition delays, poor inter-ministerial coordination, and allegedly, domestic mark-ups.

Iggy’s Insight:

The media loves the “predatory China” narrative because it sells clicks. But as investors, we lose money if we buy the wrong story. The Whoosh failure is a failure of Indonesian execution, not Chinese lending.

Why does this matter to your SGX portfolio? Because when you buy a regional conglomerate or a bank with ASEAN exposure, you aren’t just buying their growth—you are underwriting their governance risks. If a state-backed megaproject can bleed cash like this, it forces us to apply a higher discount rate to any regional infrastructure play.

The Regional Ripple Effect: Why Singapore Investors Should Care

Singapore’s direct exposure to this specific debt is minimal. However, the macro implications are significant for anyone holding a diversified portfolio.

In its November 2024 financial stability review, MAS flagged that emerging market vulnerabilities could trigger rapid capital outflows. When a major ASEAN economy like Indonesia faces a fiscal squeeze from megaprojects, three things happen:

Fiscal Tightening: Money spent servicing debt is money not spent on productivity. This slows growth.

Credit Contagion: If risk sentiment shifts, international capital pulls back from the region, not just the country.

Refinancing Risk: Corporations with heavy Indonesian exposure may face higher borrowing costs.

Regional Fiscal Health Snapshot

The “Debt Trap” vs. The “Governance Trap”

Indonesia is currently negotiating a “financial reset” with Chinese creditors. Interestingly, China has been flexible, discussing extended terms and interest rate adjustments.

The problem isn’t the lender; it’s the borrower’s internal coordination. The new sovereign wealth fund, Danantara, is weighing options, but different ministers are giving conflicting statements. This uncertainty is what kills valuation.

Iggy’s Insight:

This is the “Alpha” for today: Avoid the lazy “Growth at all costs” trade in ASEAN.

The Whoosh proves that operational success (the train runs) does not equal investment success (the project loses money). When evaluating regional REITs or Telecos, do not just look at their revenue growth. Look at their Capex discipline.

If a company has a history of massive capital projects with “strategic” (political) rather than “economic” (profit) justifications, stay away. I would rather hold a boring Singapore bank with disciplined book value growth than an exciting regional infrastructure play with a hole in its balance sheet.

What To Do Next