Three “Boring” Singapore Stocks Hiding Real Growth—And Why the Market Keeps Missing It

They Look Sleepy on the Surface. But Underneath? These Dividend Darlings Are Quietly Transforming Into Growth Engines.

Here is the frustration I hear from Singaporean investors all the time: “I want growth, but I also want dividends. I want exposure to the big trends—AI, clean energy, aviation—but I can’t find Singapore stocks that actually deliver both.”

Most local investors feel stuck between two extremes:

Chasing US Tech stocks (like Nvidia or Microsoft) at all-time highs with zero yield.

Settling for “boring” Singapore banks or REITs that pay dividends but offer little capital appreciation.

The Problem: We’re All Looking at the Wrong Story

The problem isn’t that growth stocks don’t exist in Singapore. The problem is that we are looking at them through an outdated lens.

While everyone is busy overpaying for US tech at 50x earnings, smart money is looking for the “pick and shovel” plays closer to home. Why overpay for the AI hype when you can buy the critical infrastructure powering it—right here on the SGX—at valuations that actually make sense?

Three of Singapore’s most overlooked stocks are currently in the middle of massive transformations. The market hasn’t caught up yet. But when it does, patient investors who own them today could see serious upside.

This is the story of Singtel, Sembcorp Industries, and ST Engineering—and why what you think you know about them might be holding you back from real wealth.

In This Article:

• The Problem: We’re All Looking at the Wrong Story

• 1. Singtel (SGX: Z74): The Telco Hiding a Data Centre Powerhouse

• 2. Sembcorp Industries (SGX: U96): From “Black” Energy to “Green” Growth

• 3. ST Engineering (SGX: S63): The Defense Contractor With a Hidden Aviation Empire

• The Investment Thesis: Why These Three Matter Now

• The Bottom Line

• Actionable Takeaways

1. Singtel (SGX: Z74): The Telco Hiding a Data Centre Powerhouse

The Boring Surface Story

Walk into any Singtel shop, and it feels like stepping back in time. You’re buying phone plans. You’re paying your monthly broadband bill. The narrative for years has been: “5G is coming, but it’s low-margin and capital-intensive. Expect slow growth and stable (but flat) dividends.”

That is the story the market is still telling.

The Real Story: Nxera Is Transforming Everything

Here is what most investors miss: Singtel isn’t just a telco anymore. It is becoming a regional data centre powerhouse.

The growth engine is a subsidiary called Nxera. This isn’t a side project. This is the future of Singtel. They are making a bold bet that data centre capacity—especially AI-ready capacity—is the real prize.

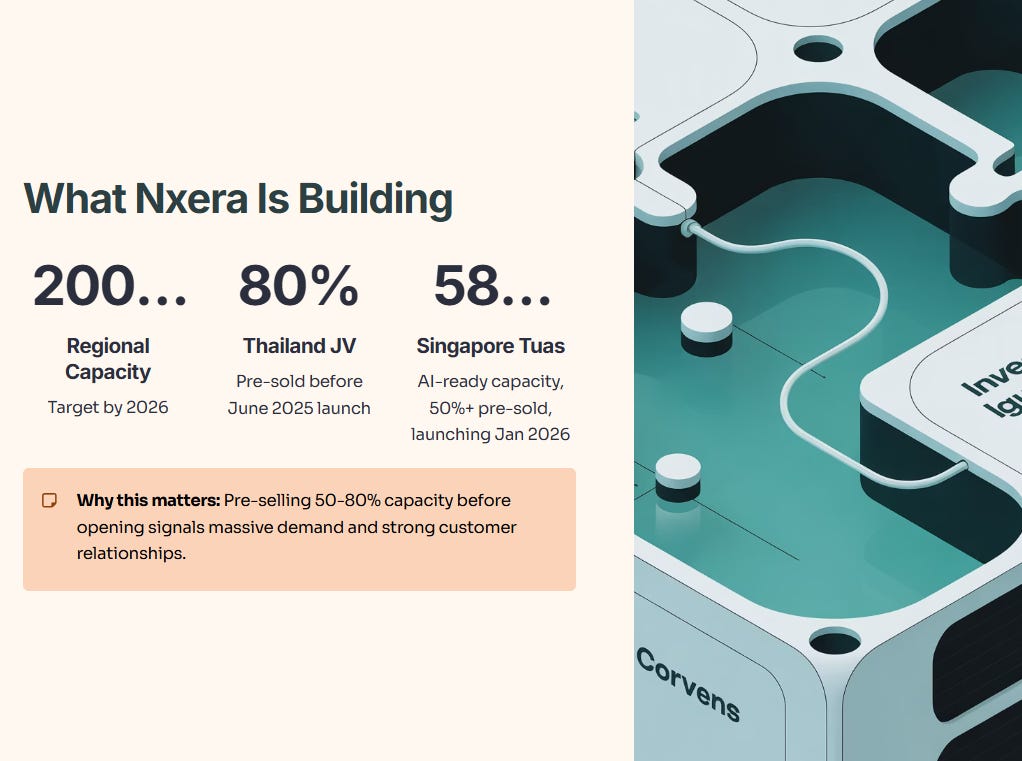

What Nxera Is Building (And How Fast)

Overall Goal: 200MW regional capacity by 2026.

Thailand (JV): Launching June 2025 (Undisclosed capacity, 80% pre-sold).

Singapore Tuas: Launching Jan 2026 (58MW AI-Ready capacity, 50%+ pre-sold).

Why this matters: Pre-selling 50–80% of capacity before a facility even opens tells you two things. First, there is massive demand for data centre space in Southeast Asia. Second, Singtel has the relationships to lock in customers years before competitors catch on.

The Tuas facility is built specifically for the AI revolution. It features liquid cooling systems (essential for handling heat from intensive AI workloads) and direct access to Nvidia’s latest GPUs. Singtel is essentially offering “AI-as-a-service.”

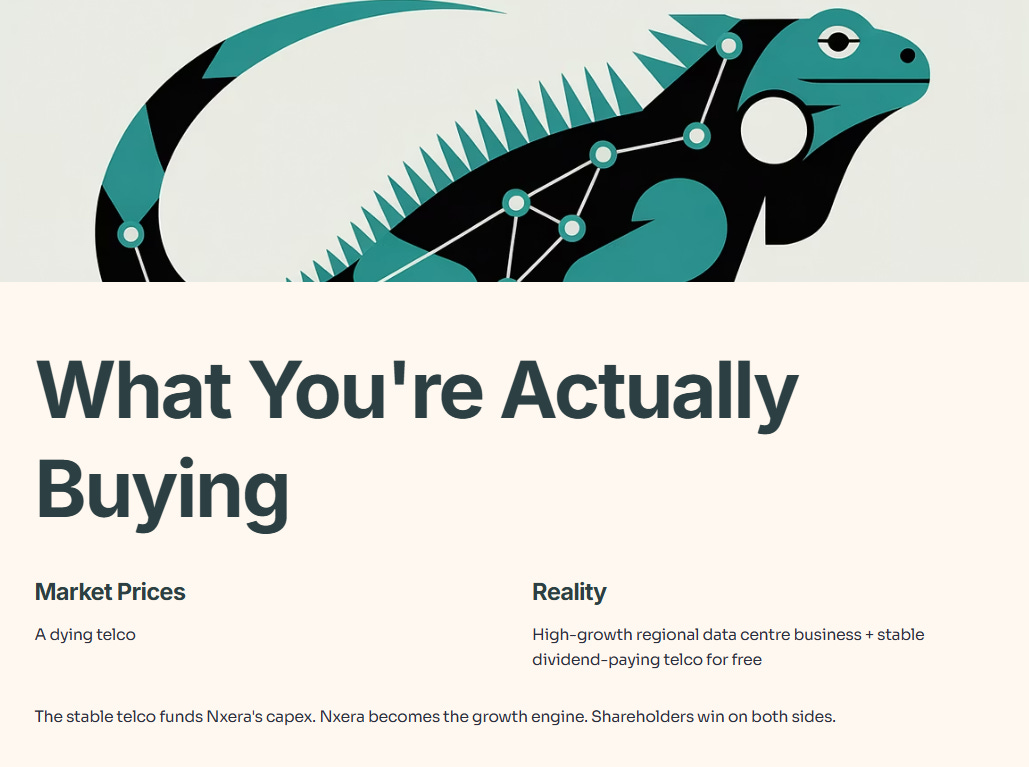

Iggy’s Take: What You’re Actually Buying

The market prices Singtel as a dying telco. But what you’re actually buying is a high-growth regional data centre business—and you’re getting the stable, dividend-paying telco for free.

The stable telco business funds the capex for Nxera. Nxera becomes the growth engine. Shareholders win on both sides.

2. Sembcorp Industries (SGX: U96): From “Black” Energy to “Green” Growth

The Boring Surface Story

Sembcorp Industries. Say that name to most Singapore investors, and what do they think? “Industrial conglomerate. Old-economy. Fossil fuels.”

The narrative suggests Sembcorp is a relic of Singapore’s past, clinging to gas assets while the world moves to renewables. It’s stable. It pays a dividend. But growth? The market says forget it.

The Real Story: A S$10.5 Billion Green Bet

Sembcorp is currently executing one of Singapore’s most aggressive corporate pivots. From 2024 to 2028, they are investing S$10.5 billion into renewables. That represents 75% of their total capital spend. They aren’t hedging their bets; they are going all-in.

The Green Transformation at a Glance

Original 2025 Target: 10GW Capacity (Already beaten).

New 2028 Goal: 25GW gross installed capacity.

Current Status: ~19.3GW (Existing portfolio + pending projects).

Why this matters: Sembcorp has already smashed their 2025 renewable capacity target. They are now shooting for 2.5x growth by 2028. That isn’t incremental improvement; that is exponential transformation.

Furthermore, on Jurong Island, they are piloting a “battery stacking” solution to increase energy storage without eating up land—a game-changer for land-scarce Singapore.

Iggy’s Take: The Cash Cow Funds the Growth Story

Here is the key insight: Sembcorp’s stable, boring gas business is generating the predictable cash flow needed to fund this massive renewables expansion.

The market is slowly waking up to this shift, but many investors still mentally price Sembcorp as a “gas company.” That is the disconnect. This is a “green growth” stock hiding inside a boring energy utility.

3. ST Engineering (SGX: S63): The Defense Contractor With a Hidden Aviation Empire

The Boring Surface Story

ST Engineering is Singapore’s trusted defense contractor. They build things for the government. Reliable. Sleepy. Safe. That is how most investors frame it

The Real Story: One of the World’s Largest “Garages” for Planes

Here is what is hiding in plain sight: ST Engineering is one of the world’s premier providers of aircraft MRO (Maintenance, Repair, and Overhaul). Think of them as the high-tech garage for the world’s airlines—and business is booming.

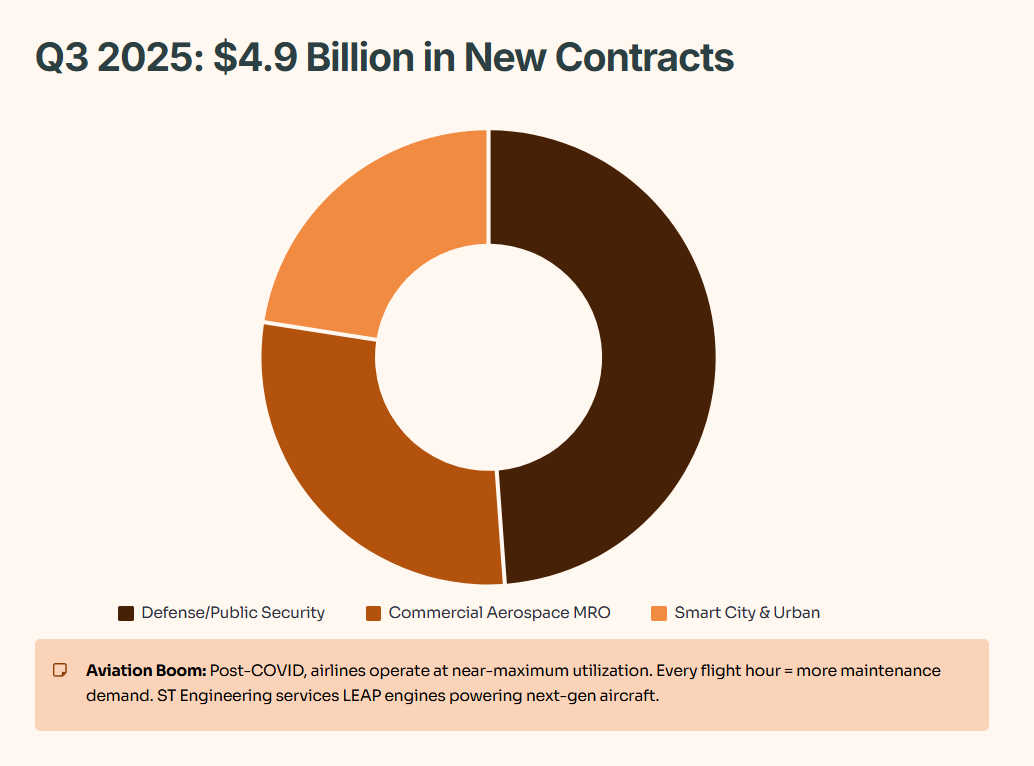

In Q3 2025 alone, ST Engineering secured $4.9 billion in new contracts.

Commercial Aerospace MRO: $1.4 billion (29% of wins).

Smart City & Urban Solutions: $1.1 billion (22% of wins).

Defense/Public Security: $2.4 billion (49% of wins).

Why Aviation Is Booming Post-COVID, the world is flying harder than ever. Airlines are operating aircraft at near-maximum utilization. Every flight hour means more wear and tear. Every aircraft needs regular maintenance.

ST Engineering is also a premier provider for LEAP engines—the cutting-edge engines powering next-generation aircraft. As airlines upgrade their fleets, this maintenance segment is set to explode.

Iggy’s Take: Aviation Exposure Without the Airline Risk

Most investors buy ST Engineering for safety. They don’t realize they are buying exposure to one of the biggest global tailwinds: the aviation boom.

Airlines are volatile; they crash when oil prices spike or travel demand dips. But maintenance? That is mandatory. ST Engineering gets paid whether the airline makes a profit or not. You are buying the pick-and-shovel play of the travel industry.

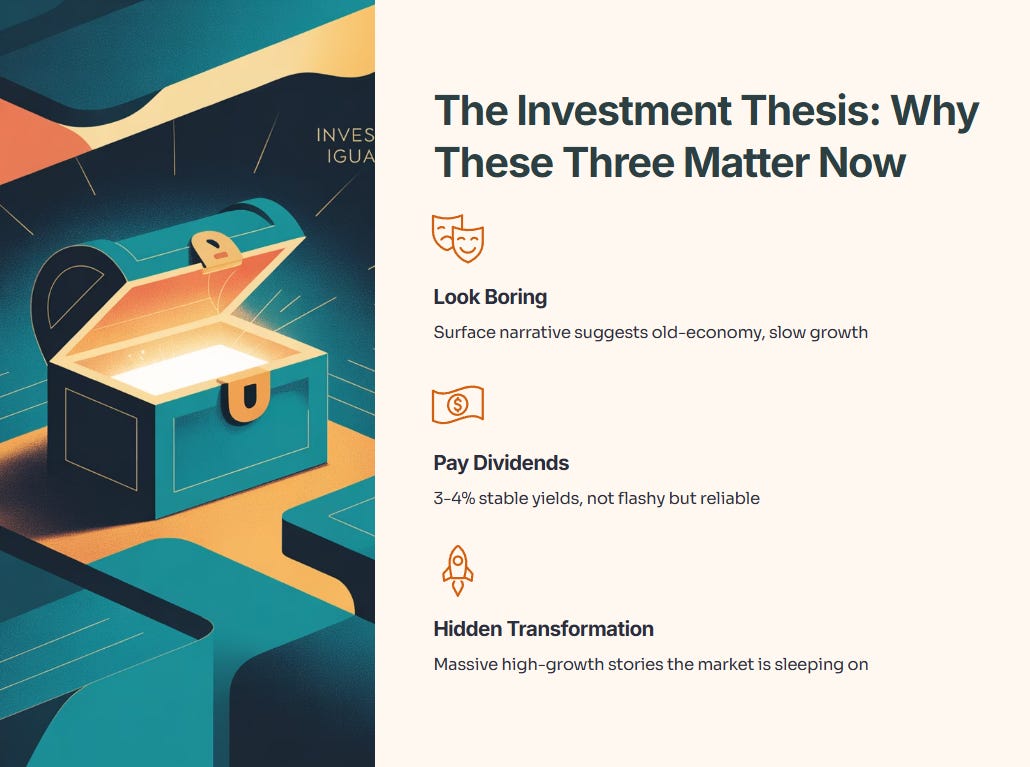

The Investment Thesis: Why These Three Matter Now

What do Singtel, Sembcorp, and ST Engineering have in common?