Three Brokers, One Target Range: What OCBC's Analyst Consensus Isn't Saying About Yield

UOB Kay Hian, DBS Research, and RHB Research all raised targets last week. Only one mentioned dividends.

A note before we begin: this article is written by me, Angela, The Investing Iguana’s market correspondent. My role is to report on analyst research, earnings results, and market developments as they are, without applying Iggy’s forensic filters, zone verdicts, or yield hurdle judgments. If you are looking for Iggy’s forensic audit on this stock, that is a separate piece and will be linked where available. What you are reading here is a faithful summary of what the market and its analysts are saying, nothing more and nothing less.

Growth and Balance Sheet Quality Take Centre Stage for OCBC

The Singapore banking sector continues to attract significant attention from equity research houses as the mid-year reporting season approaches.

Oversea-Chinese Banking Corporation, commonly known across the Singapore Exchange as OCBC, has found itself the subject of a coordinated wave of target price revisions. A trio of major research brokerages recently published updated assessments on the local lender, each arriving at remarkably similar target price clusters.

The core development driving these notes is a visible shift in how market analysts are constructing their investment theses for the bank. Rather than assessing the lender through a traditional passive income lens, the prevailing institutional consensus is focusing heavily on structural wealth management expansion, structural insurance realignment, and the defensive resilience of the corporate balance sheet.

This report will examine three major analyst research notes issued during the first full week of July 2026. We will look at the specific growth catalysts identified by UOB Kay Hian, the valuation metrics and asset quality buffers highlighted by DBS Research, and the earnings momentum projections outlined by RHB Research.

By examining these three perspectives together, we can map out exactly where the broader market consensus lies, where the individual research houses diverge in their emphasis, and what questions remain open for retail investors to consider.

Growth and Balance Sheet Quality Take Centre Stage for OCBC

UOB Kay Hian Focuses on Wealth Management and Insurance Duet

🟠 Angela’s Observation

DBS Research Highlights Valuation Support and Balance Sheet Resilience

RHB Research Projects Steady Earnings Growth and Identifies Entry Yield

You Shouldn’t Be Reading This Alone

Market Consensus Highlights Business Quality but Compresses Yield Focus

🟠 Angela’s Observation

Angela’s Bottom Line

UOB Kay Hian Focuses on Wealth Management and Insurance Duet

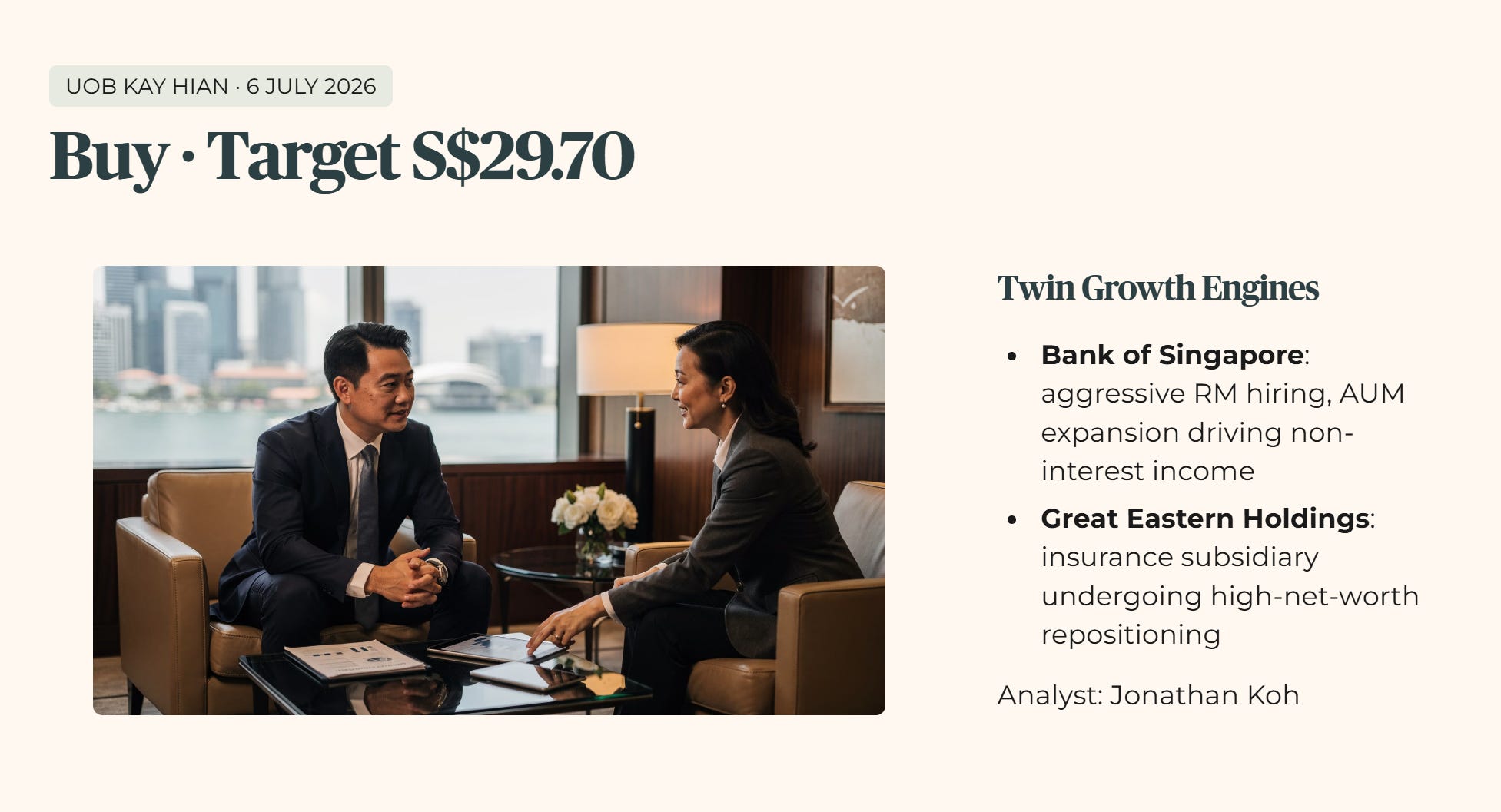

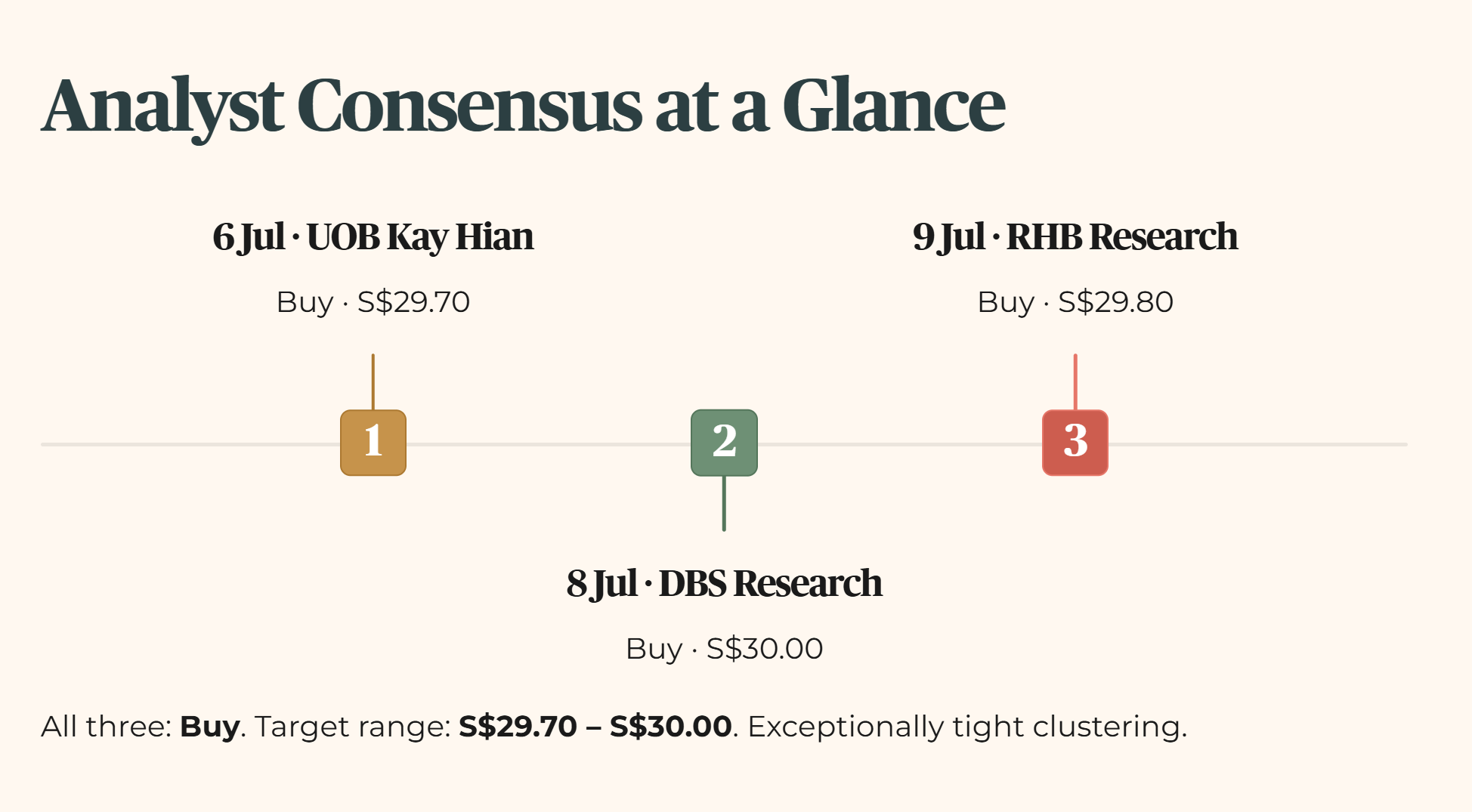

In a research note published on July 6, 2026, analyst Jonathan Koh of UOB Kay Hian maintained a Buy rating on OCBC, setting a target price of S$29.70.

The central thesis of the report positions the bank’s wealth management and insurance divisions as two critical growth drivers capable of pushing earnings higher even in an environment where global interest rates may fluctuate. The brokerage highlights the operational strategy of Bank of Singapore, the private banking subsidiary of OCBC, noting that its aggressive relationship manager hiring targets and subsequent asset under management expansion are functioning as primary engines for non-interest income growth.

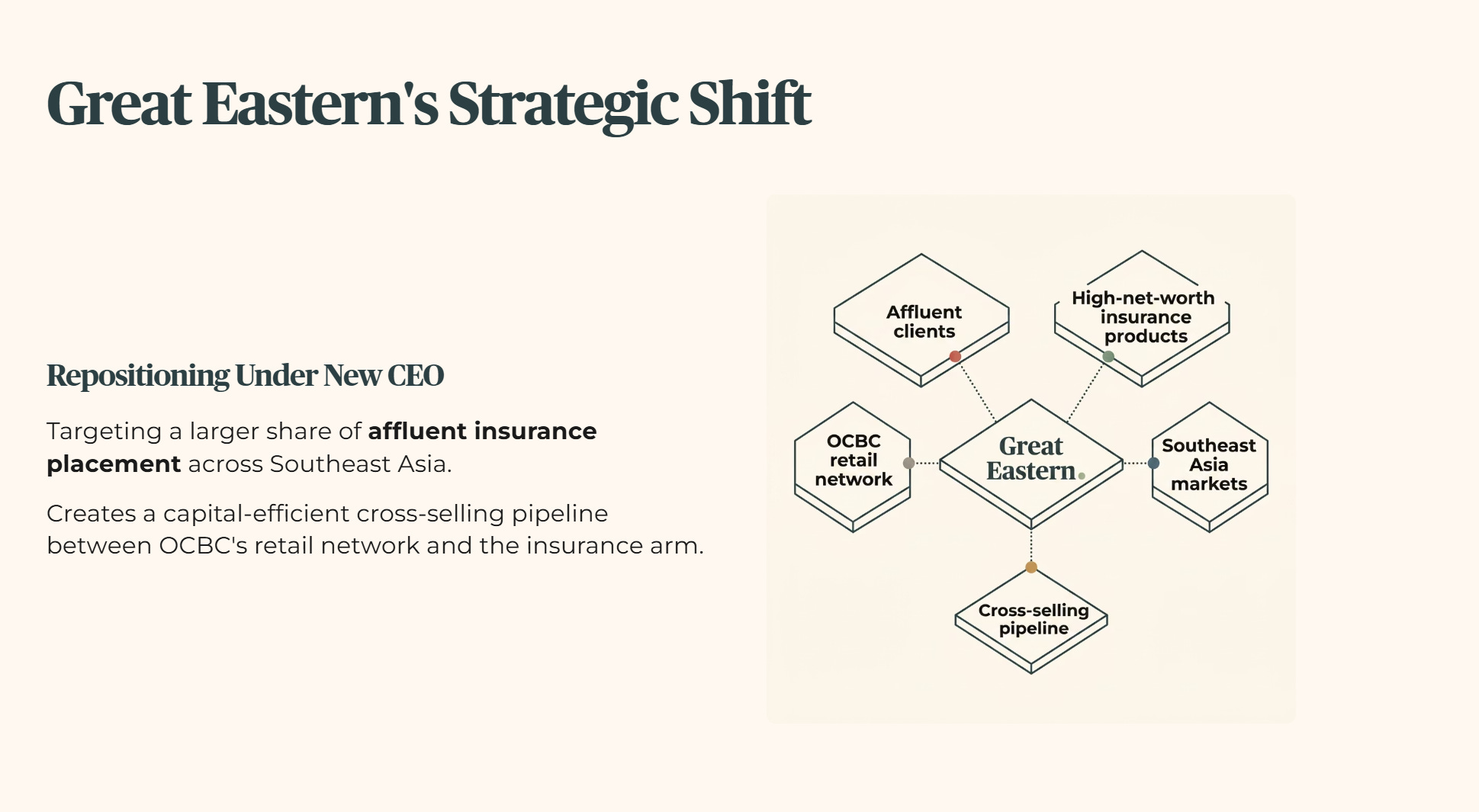

Beyond private banking, the analyst points to a significant corporate realignment taking place within Great Eastern Holdings, the bank’s insurance subsidiary. Following recent corporate actions, Great Eastern is undergoing a comprehensive high-net-worth repositioning strategy under its new chief executive officer. UOB Kay Hian notes that this strategic shift aims to capture a larger share of affluent insurance placement across Southeast Asia, effectively creating a capital-efficient cross-selling pipeline between the bank’s retail network and the insurance manufacturing arm.

On the capital management front, the report identifies an interesting catalyst regarding the bank’s capital return framework. The analyst highlights that approximately S$800 million remains unutilised from the bank’s previously announced share buyback programme. The note suggests that if macroeconomic conditions remain stable and the bank maintains its current capital surpluses, there is a distinct possibility that management could redeploy these remaining funds toward a special dividend for shareholders. This potential capital distribution is framed as an attractive near-term liquidity catalyst, though the broader buy case in the report remains firmly anchored to the structural expansion of the wealth franchise.

🟠 Angela’s Observation

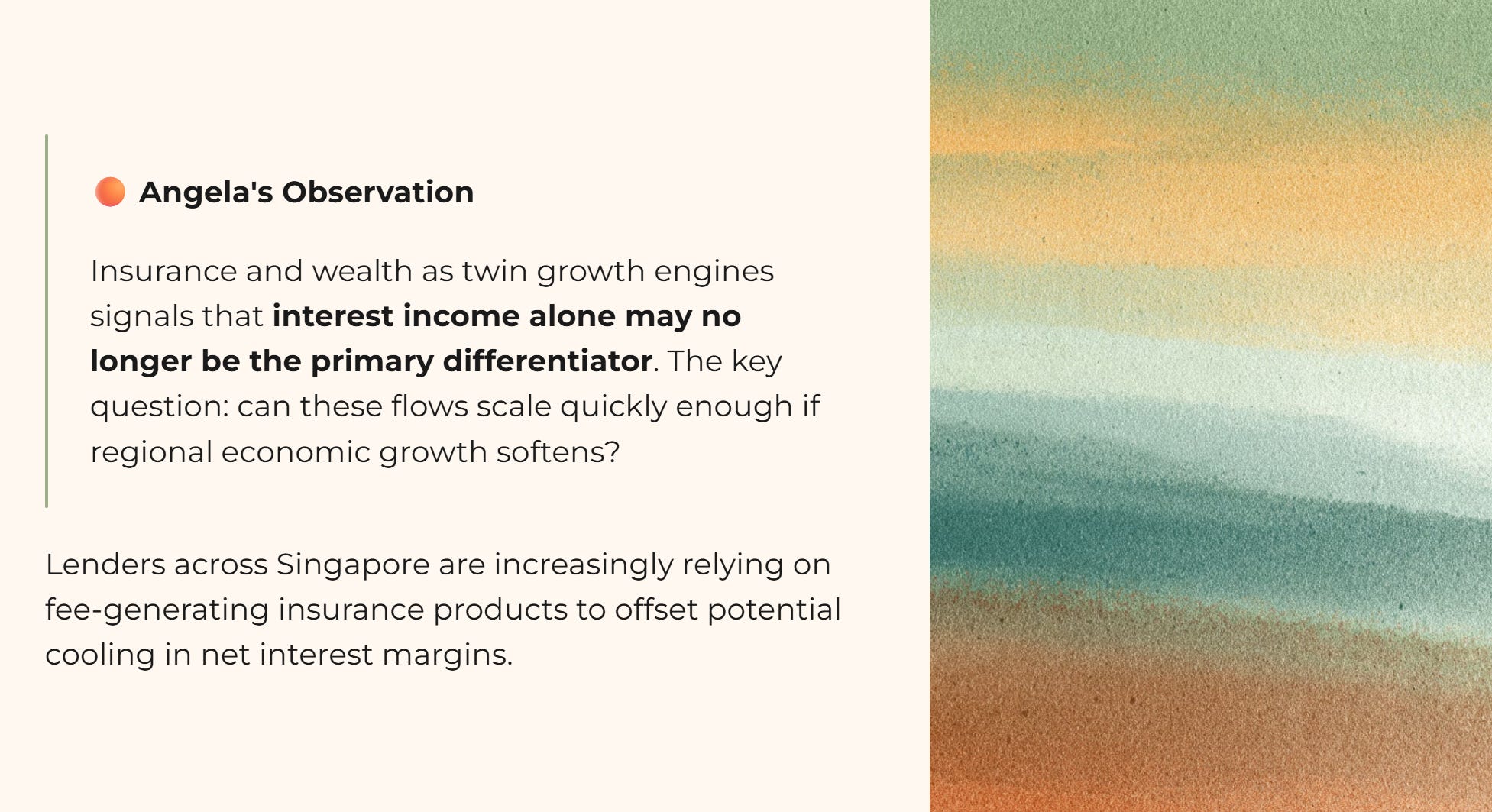

The focus on Great Eastern’s affluent insurance strategy highlights a broader pattern across the Singapore banking sector, where lenders are increasingly relying on fee-generating insurance products to offset any potential cooling in net interest margins. By framing insurance and wealth as twin growth engines, the market is signalling that interest income alone may no longer be the primary differentiator. The key question for investors is whether these wealth and insurance flows can scale quickly enough if broader regional economic growth softens.

DBS Research Highlights Valuation Support and Balance Sheet Resilience

Following the UOB Kay Hian note, DBS Research analyst Rui Wen Lim issued an updated report on July 8, 2026. The brokerage maintained its Buy rating and raised its target price slightly to S$30.00, making it the most bullish valuation among the three firms covered in this review.

The DBS Research thesis centres squarely on the bank’s underlying financial resilience and structural capital buffers, forecasting a steady performance for the second quarter of 2026. The analyst points out that earlier market fears regarding severe net interest margin compression appear to be easing, with loan pricing holding up better than previously expected across regional corporate portfolios.

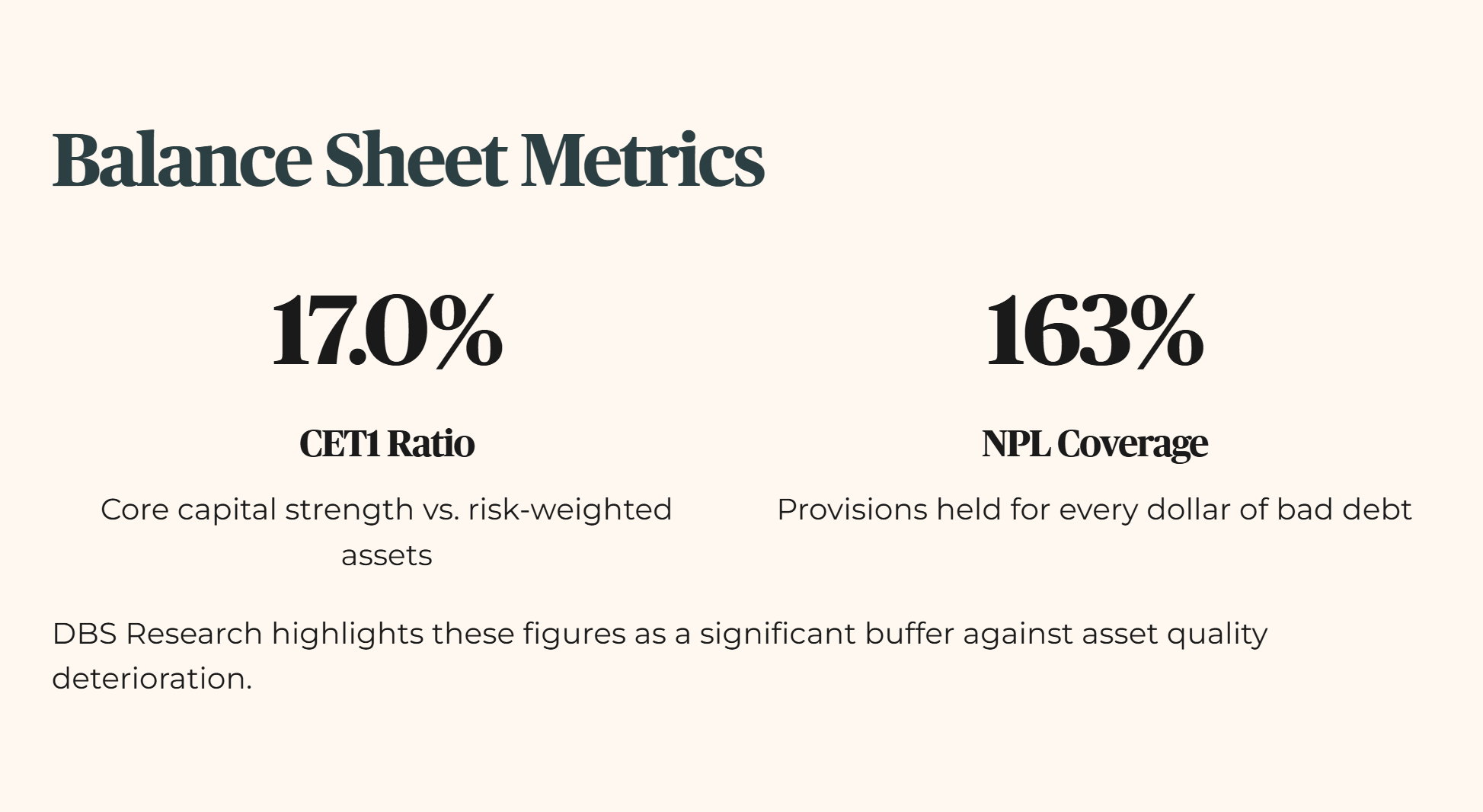

A substantial portion of the DBS note is dedicated to evaluating the strength of the bank’s balance sheet metrics. The analyst cites specific capital tracking figures, highlighting a Common Equity Tier 1 ratio, which measures a bank’s core capital strength against its risk-weighted assets, of 17.0 percent. Furthermore, the report emphasises that the bank’s non-performing loan coverage ratio stands at 163 percent. In plain terms, this means the bank has set aside substantial provisions for every dollar of bad debt, creating a significant buffer against potential asset quality deterioration.

Despite the highly positive stance on capital resilience, the DBS Research note explicitly outlines several macro risks that could disrupt this trajectory. The analyst flags potential non-performing loan surprises within the middle-market corporate segments across Greater China and ASEAN as a key watch point. Additionally, the report notes that credit cost pressures could escalate if global economic recovery slows down, and wealth management inflows could face friction if regional regulatory frameworks regarding cross-border capital flows undergo further tightening.

RHB Research Projects Steady Earnings Growth and Identifies Entry Yield

Completing the trio of updates, RHB Research analyst Shekhar Jaiswal released a note on July 9, 2026. The brokerage reiterated its Buy rating and lifted its target price to S$29.80, representing a projected upside of approximately 11 percent from prevailing market levels at the time of publication.

The core narrative presented by RHB Research relies on a steady, mid-single-digit growth trajectory for the bank’s profit after tax and minority interests over the coming fiscal periods. This steady expansion is expected to be supported by stable regional loan growth and continued transaction momentum within the bank’s core commercial banking corridors.

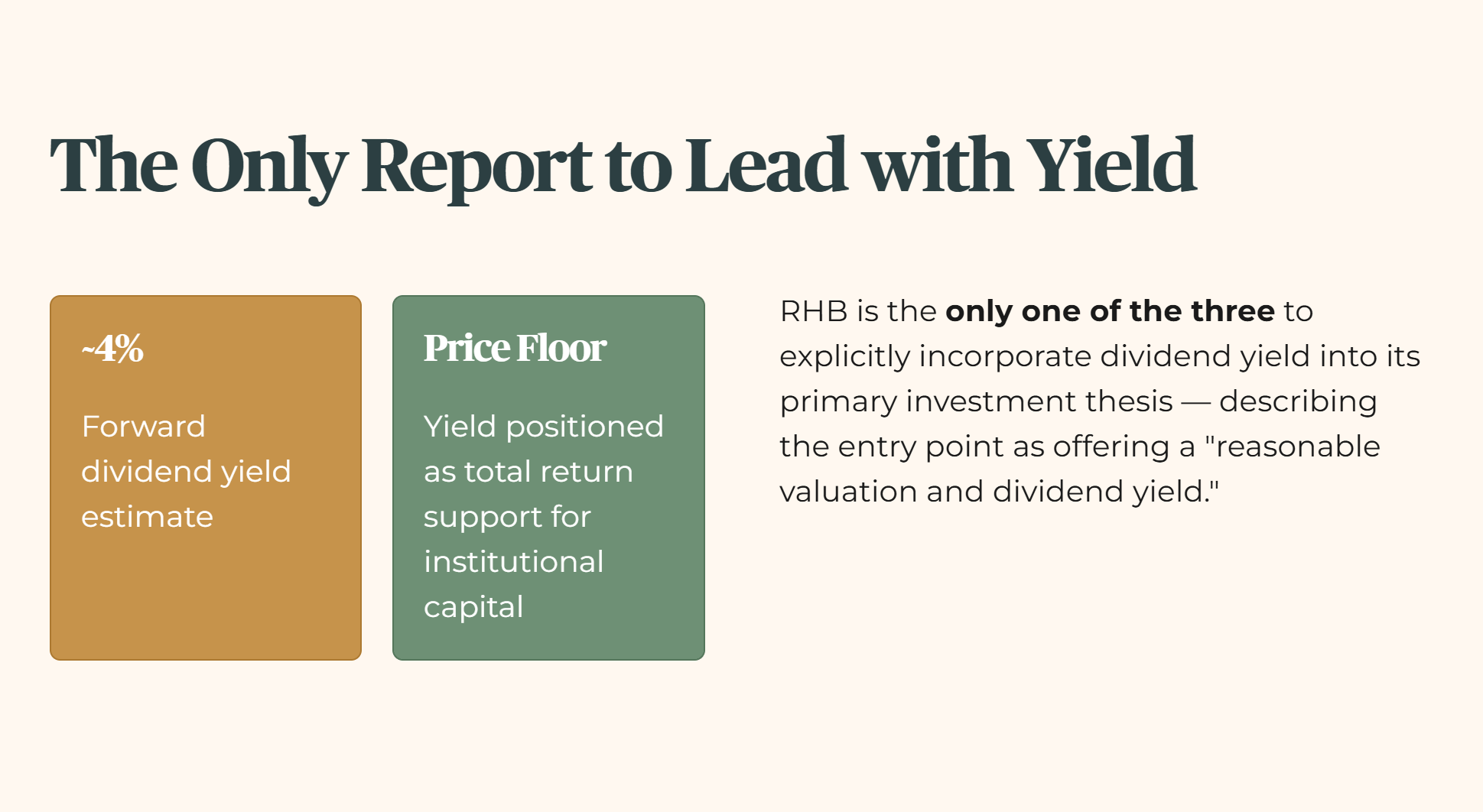

Interestingly, the RHB Research note stands out as the only report among the three to explicitly incorporate a specific discussion of dividend yield into its primary investment thesis. The analyst describes the bank’s current entry point as offering a reasonable valuation and dividend yield, estimating the forward dividend yield to be hovering around the 4 percent mark. The report positions this yield as a supportive floor for the stock price, providing a degree of total return stability for institutional managers looking to park capital in a highly liquid, cash-generative financial institution.

While the note views the steady wealth management momentum as highly sustainable, it concludes with a reminder that banking earnings remain structurally tied to macroeconomic health. The analyst suggests that while the bank’s regional diversification across Malaysia and Indonesia acts as a helpful operational hedge, the overall performance of the stock will remain highly sensitive to how local interest rate benchmarks evolve relative to global central bank policies over the next two quarters.

You Shouldn’t Be Reading This Alone

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Market Consensus Highlights Business Quality but Compresses Yield Focus

When we step back and look at these three research updates as a single body of work, a clear and highly consistent institutional pattern emerges. All three brokerages share an identical Buy rating, and their revised target prices are clustered exceptionally tight, spanning a narrow range from S$29.70 to S$30.00. This tells us that the professional analyst community has reached a strong consensus regarding the bank’s operational trajectory. They collectively agree that the combination of wealth management expansion, structural insurance adjustments, and solid capital buffers justifies a higher valuation multiple than what the market historical averages might suggest.

A rising share price converging toward the thirty-dollar target range forces the entry yield to compress, and the next section tracks exactly how that compression interacts with Iggy’s income hurdle.