Three Buy Calls, One Unanswered Question: Angela's CSE Global Analyst Roundup

All three analysts are bullish. But their target prices diverge by forty-six cents, and the strategic review remains unpriced.

By Angela, Market Correspondent, The Investing Iguana

I am Angela, market correspondent for The Investing Iguana. My role sits alongside Iggy’s forensic work, not inside it. Where Iggy audits balance sheets and applies the Zone System, I report what the market is saying and surface the observations that make you think. I do not apply forensic filters or zone verdicts. What I do bring is a journalist’s eye for what the numbers are not saying, where analysts agree but their assumptions diverge, and what questions the data leaves open. Think of this as the market conversation, reported clearly, with the tensions made visible.

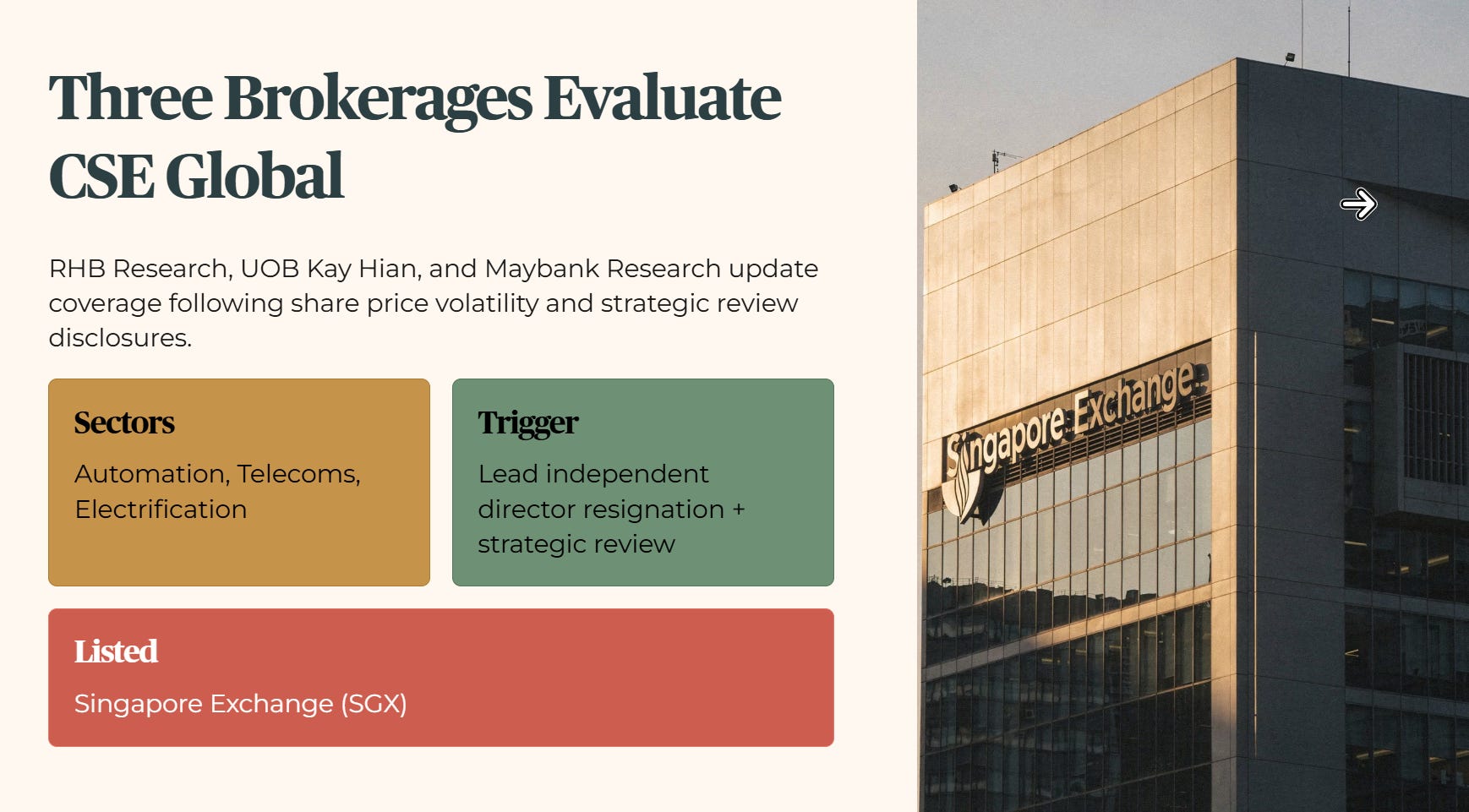

Three Brokerages Evaluate CSE Global Following Board Changes and Strategic Review Disclosures

Analysts from RHB Research, UOB Kay Hian, and Maybank Research have updated their coverage on the SGX-listed engineering group after recent share price volatility and regulatory clarifications.

CSE Global is an engineering systems provider listed on the Singapore Exchange, operating across automation, telecommunications, and electrification sectors. The company has drawn significant market attention following a sharp correction in its share price after the resignation of its lead independent director and public disclosures surrounding an ongoing strategic review. This article compiles the latest research notes from three financial institutions that have assessed the company’s governance structure, its current operational backlog, and its financial outlook.

RHB Research

Angela’s Observation

UOB Kay Hian

Maybank Research

You Shouldn’t Be Reading This Alone

Market Summary

Angela’s Observation

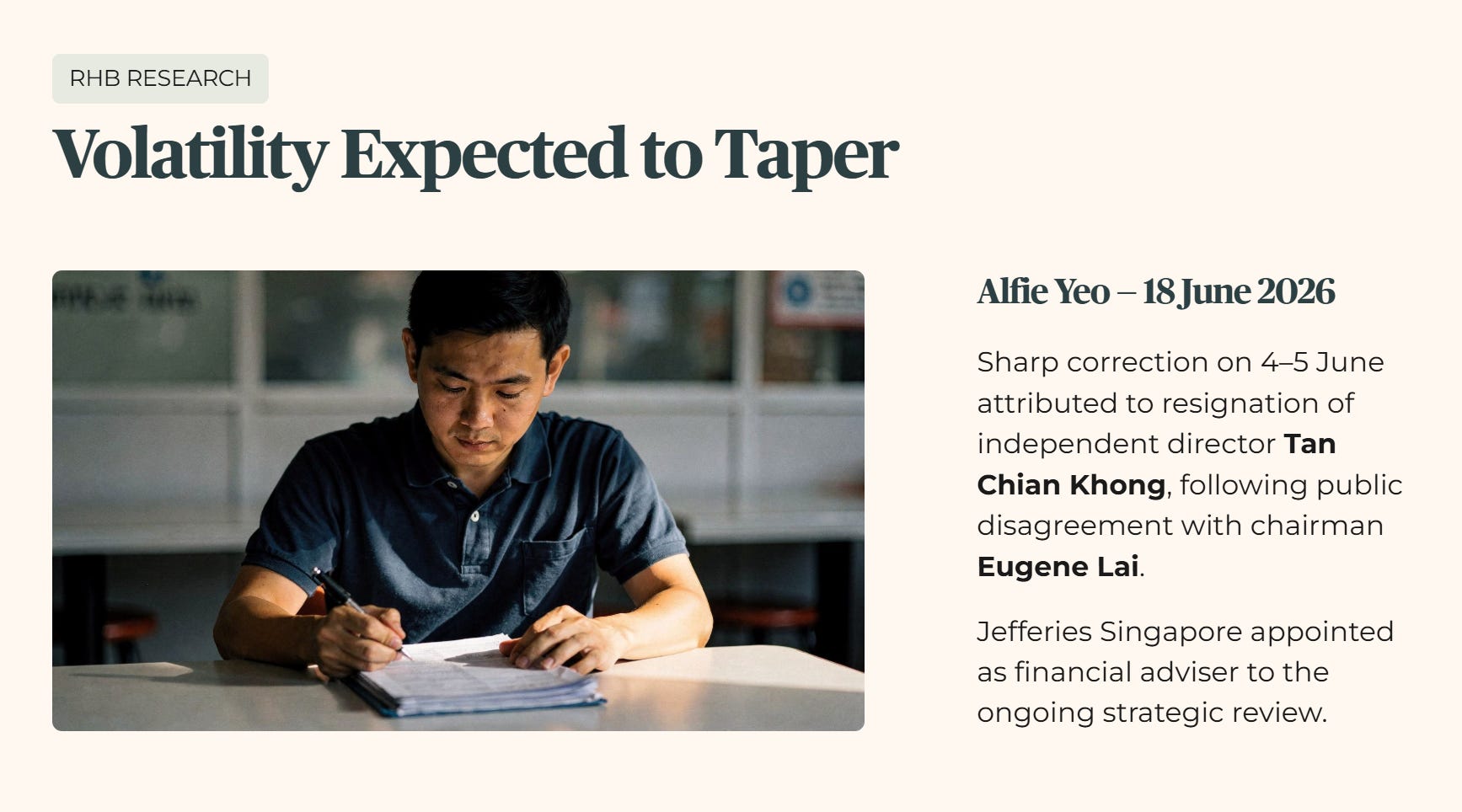

RHB Research

Alfie Yeo of RHB Research published a note on June 18 2026 stating that the recent share price volatility should begin to taper following board clarifications submitted to the Singapore Exchange. The brokerage attributes the sharp correction on June 4 and 5 to the resignation of independent director Tan Chian Khong, whose departure created a governance overhang after a public disagreement with chairman Eugene Lai over operational direction and aspects of the ongoing strategic review. Jefferies Singapore has been appointed as financial adviser to that review.

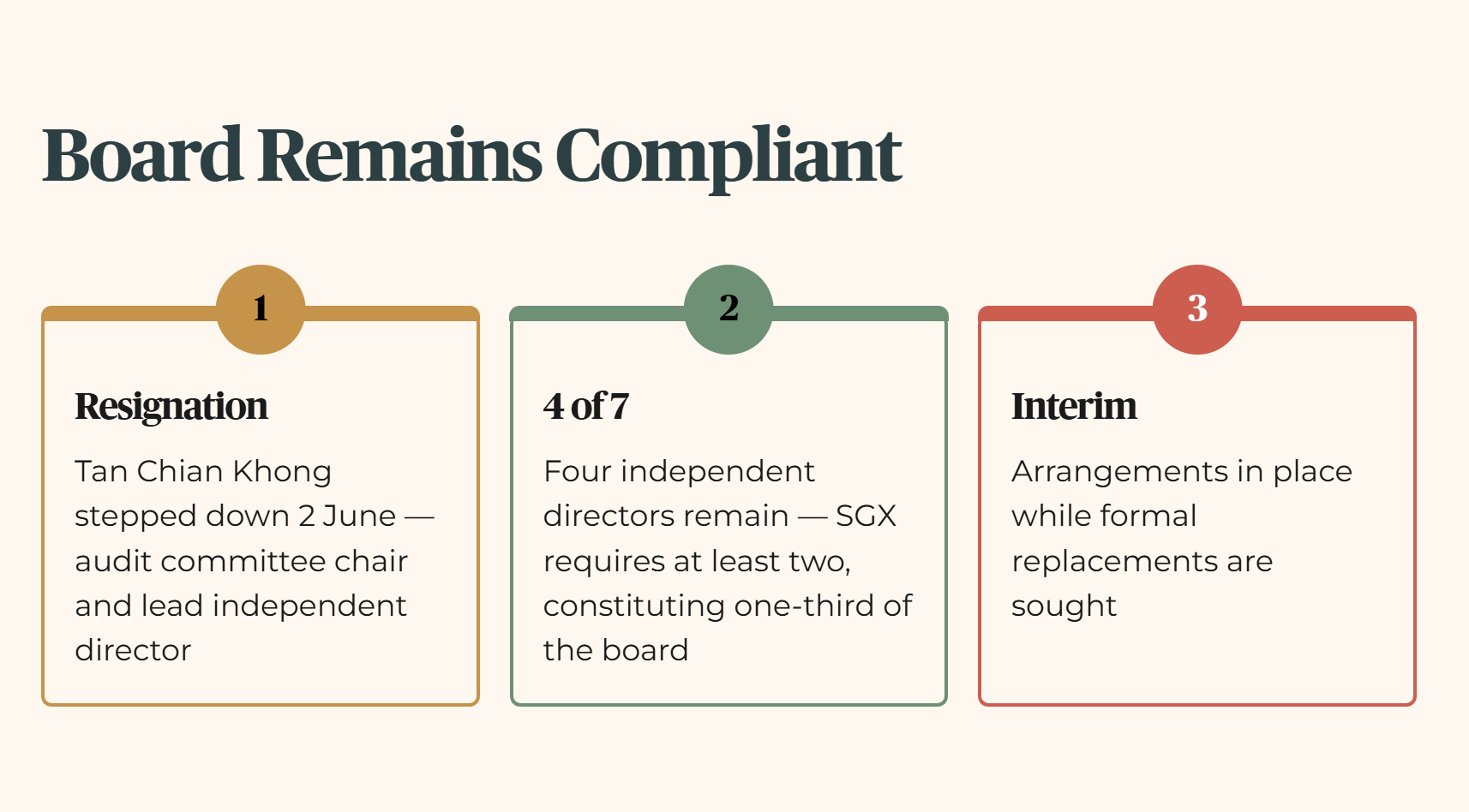

Tan Chian Khong, who served as chair of the audit committee and lead independent director, stepped down on June 2 following these disagreements. Despite his departure, four independent directors remain on the seven-member board, keeping the company compliant with Singapore Exchange requirements for at least two independent directors constituting at least one-third of the board. Interim arrangements are in place while formal replacements are sought.

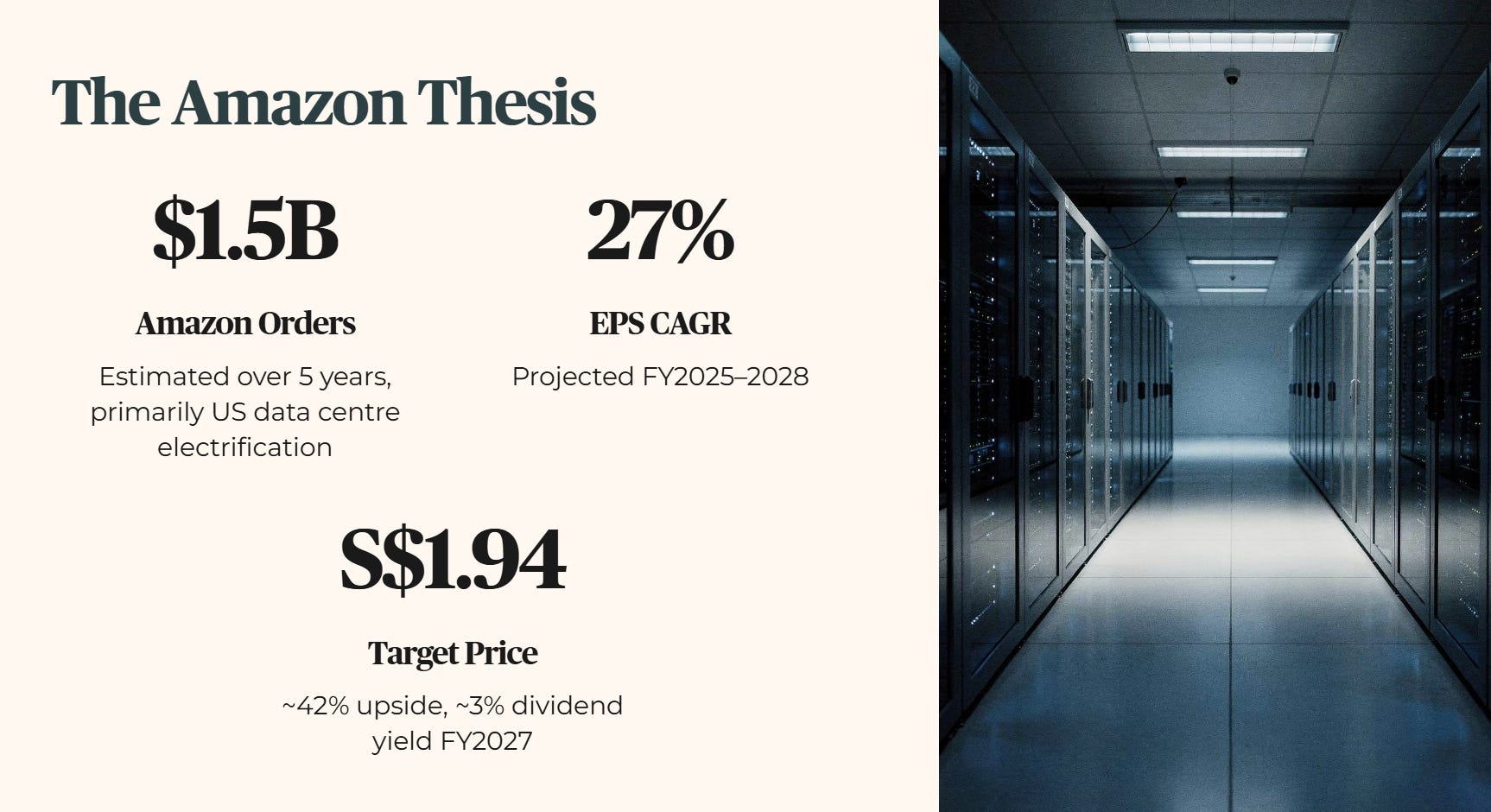

The brokerage’s positive stance rests on an estimated one billion five hundred million US dollars of orders from Amazon over the next five years, tied primarily to electrification work for Amazon’s data centres in the United States. On this basis, RHB projects a compound annual growth rate in earnings of 27 percent for financial years 2025 to 2028 and maintains a Buy rating with a target price of one dollar ninety-four Singapore cents, implying approximately 42 percent upside from recent trading levels and an estimated dividend yield of roughly 3 percent for financial year 2027.

The stock is noted to trade at around 20 times forward price-to-earnings, below the projected 27 percent earnings growth rate, representing a price-earnings-to-growth ratio of under 1. The brokerage applies a 2 percent discount to its intrinsic value estimate based on an environmental, social, and governance score of 3.0, which sits slightly below the RHB Singapore median of 3.1. Key risks identified include unexpected project cost overruns, the possibility that Amazon does not fully deliver the projected order pipeline, and any adverse developments from the strategic review that could reintroduce volatility.

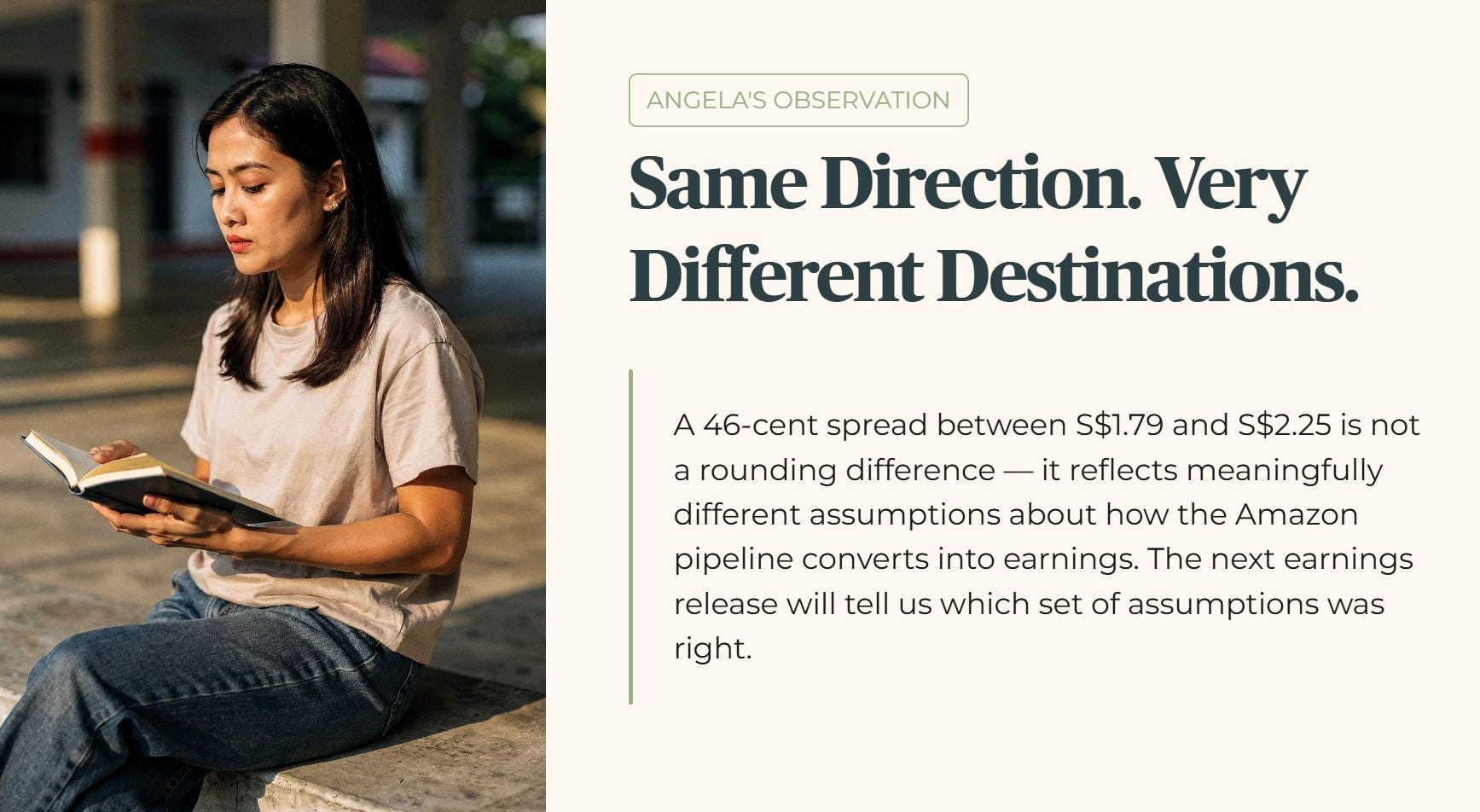

🟠 Angela’s Observation

All three brokerages share a Buy rating on CSE Global, but their target prices tell a more divided story. The gap between UOB Kay Hian’s one dollar seventy-nine Singapore cents and Maybank’s two dollars twenty-five Singapore cents is not a rounding difference. It is a forty-six cent spread representing meaningfully different assumptions about how the Amazon order pipeline will convert into earnings over five years. When analysts agree on direction but diverge this sharply on value, it is usually the underlying assumptions doing the heavy lifting. The question worth watching is which set of assumptions the next earnings release validates.

What those three Buy calls still leave unstated is how the 46‑cent spread in target prices would look if you re‑ran their earnings assumptions against a downside outcome from the Jefferies review instead of the base case baked into today’s models.