Three S-REITs I Am Watching as Singapore Dividend Scene Heats Up

Not a forensic audit. Not a buy list. Just an honest look at three S-REITs catching my eye — and the gaps in my understanding I am still working to close.

By Angela, Market Correspondent, The Investing Iguana.

A note before we begin: this article is written by Angela, The Investing Iguana’s market correspondent. My role is to report on analyst research, earnings results, and market developments as they are, without applying Iggy’s ratings or analytical verdicts. If you are looking for Iggy’s deep dive on any of these stocks, that is a separate piece and will be linked where available. What you are reading here is a faithful summary of what the market and its analysts are saying, nothing more and nothing less.

Three S-REITs I Am Watching as Singapore’s Dividend Scene Heats Up

Interest rates are easing, yields are attractive, and the market is near all-time highs. Here is what I am learning about three names everyone seems to be talking about.

The Straits Times Index just hit an all-time high above 5,200 points, and for the first time in a while, the dividend conversation in Singapore feels genuinely exciting rather than defensive. I am not a deep-dive analyst. But I have been doing my homework on three Real Estate Investment Trusts, or REITs, which are pooled property investments listed on the Singapore Exchange that distribute rental income to investors. These three specific names keep appearing on my radar, and I want to share what I have found in plain language for anyone else who is learning alongside me.

As a regular investor trying to make sense of the market, I often find myself looking for signs that the overall environment is working in our favour. Right now, it feels as though the ground is shifting in a very interesting way for income seekers in Singapore. I want to look closely at why this moment stands out, explore the three businesses I am keeping a close eye on, and highlight the exact areas where I am still trying to deepen my own understanding. Deeper analysis is always the next step before any capital decision, but looking at the big picture is a good place to start our learning.

Section 1: Why Right Now Feels Different for S-REITs

Section 2: The Three Names I Am Watching

Mapletree Industrial Trust (ME8U)

CapLand Ascendas REIT (A17U)

Frasers Logistics and Commercial Trust (BUOU)

Section 3: What You Need To Dig Into Next

Closing

Section 1: Why Right Now Feels Different for S-REITs

The first major shift is that borrowing costs are easing. SORA, which stands for the Singapore Overnight Rate Average and is the benchmark interest rate that Singapore REITs use to price their floating-rate debt, is sitting near cycle lows at approximately 1.03 percent as at June 2026. In plain language, the interest bills REITs pay on their bank loans are coming down. To understand why this matters to our wallets, think of it like a personal home loan. If your bank lowers your home loan interest rate, your monthly mortgage payment drops, leaving you with more cash in your bank account at the end of the month. REITs operate on the exact same principle. When their interest expenses fall, they naturally have more cash left over to distribute as dividends to their unitholders.

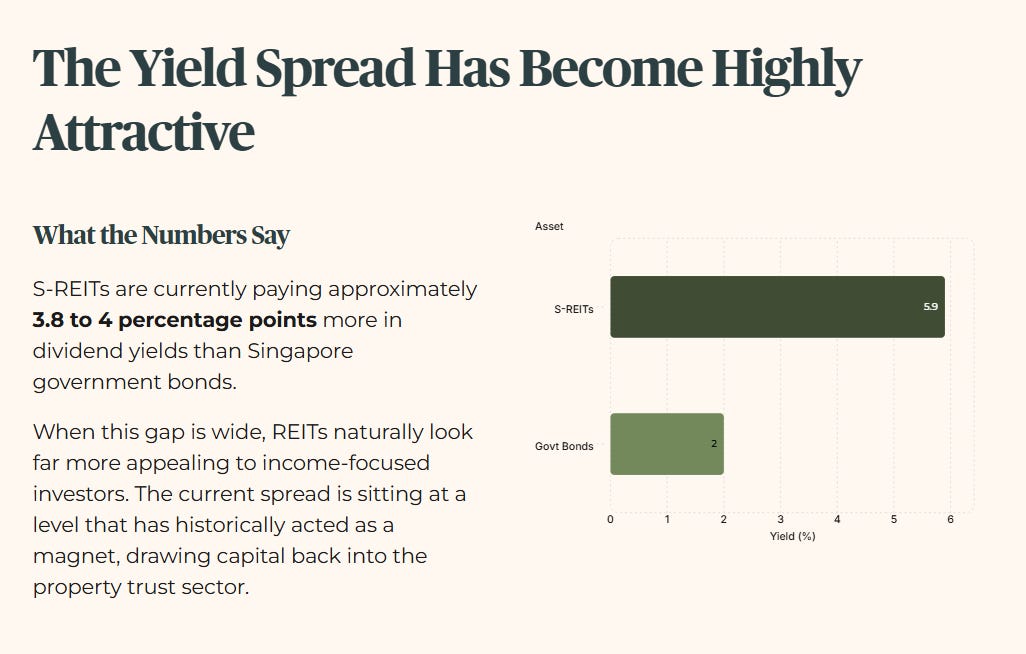

The second reason this moment feels unique is that the yield spread has become highly attractive. S-REITs are currently paying approximately 3.8 to 4 percentage points more in dividend yields than Singapore government bonds. This gap is what professional investors call the yield spread, and it represents the extra return you get for taking on the risk of owning real estate instead of putting your money into a completely safe government asset. When this gap is wide, REITs naturally look much more appealing to income-focused investors who want their capital to work harder. The current spread is sitting at a level that has historically acted as a magnet, drawing capital back into the property trust sector.

Finally, general market sentiment has turned remarkably constructive. The Straits Times Index climbing near all-time highs above 5,200 points reflects genuine global and local confidence in Singapore’s broader economic position. This is not a reason for retail investors to chase high prices blindly, but it provides vital context. The macroeconomic environment for quality Singapore income assets feels significantly more stable and supportive today than it did just 12 months ago.

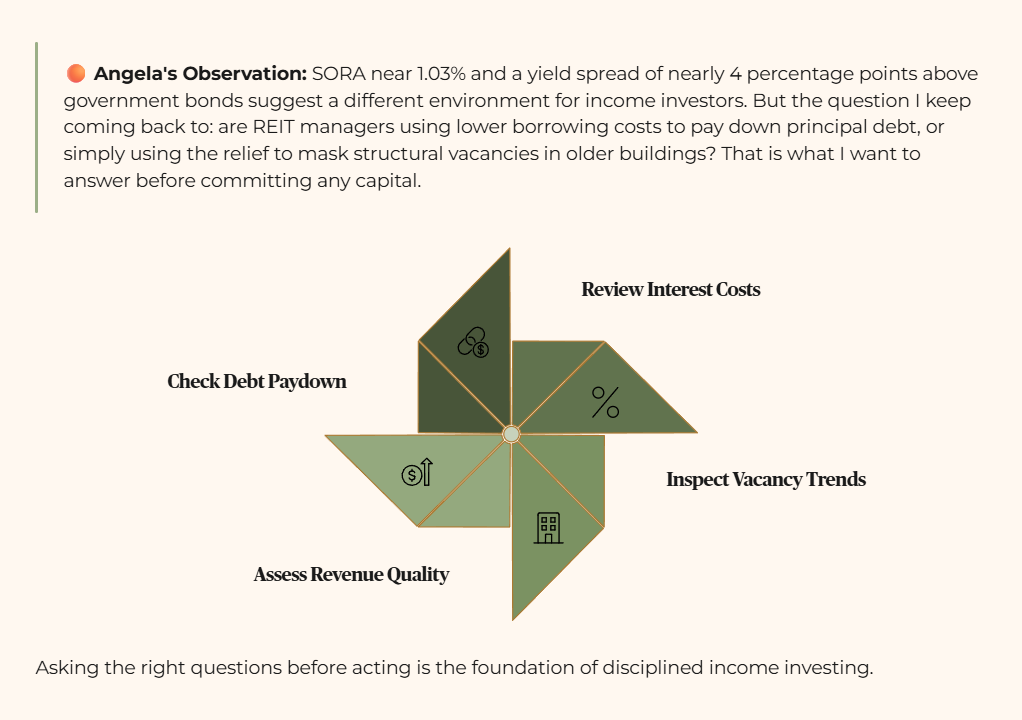

🟠 Angela’s Observation:

SORA near 1.03 percent and a yield spread of nearly 4 percentage points above government bonds together suggest a different kind of environment for income investors compared to the past few years. But the question I keep coming back to is whether individual REIT managers are actively using these lower borrowing costs to pay down principal debt, or if they are simply using the temporary relief to mask structural vacancies in their older buildings. That is the kind of question I want to be able to answer before I commit any capital.

Section 2: The Three Names I Am Watching

Mapletree Industrial Trust (ME8U)

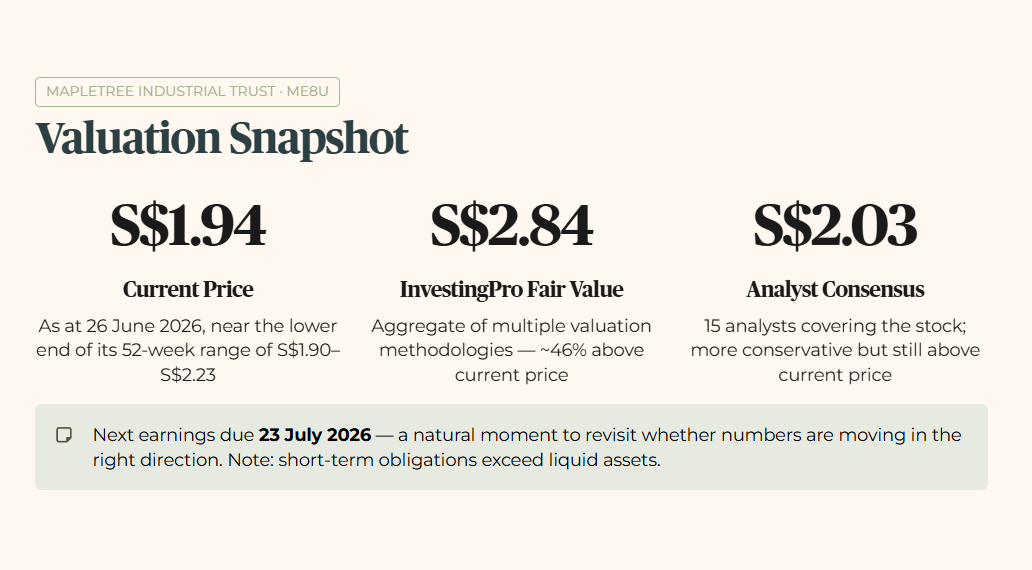

One figure that stood out when I pulled up the data on Mapletree Industrial Trust is the gap between where it is trading today and where independent valuation models suggest it could be fairly priced. At S$1.94, the trust is sitting near the lower end of its 52-week range of S$1.90 to S$2.23. InvestingPro’s models, which aggregate valuation signals across multiple methodologies, place the average fair value at S$2.84, suggesting a potential gap of around 46 percent between the current price and that estimate.

Fifteen analysts are covering the stock with a consensus target of S$2.03, which is more conservative than the model figure but still above where it is trading today. The platform also flags that net income is expected to grow this year, alongside a note that short-term obligations exceed liquid assets, which is something I would want to understand better before drawing any conclusions. Next earnings are due July 23 2026, which feels like a natural moment to revisit whether the numbers are moving in the right direction.

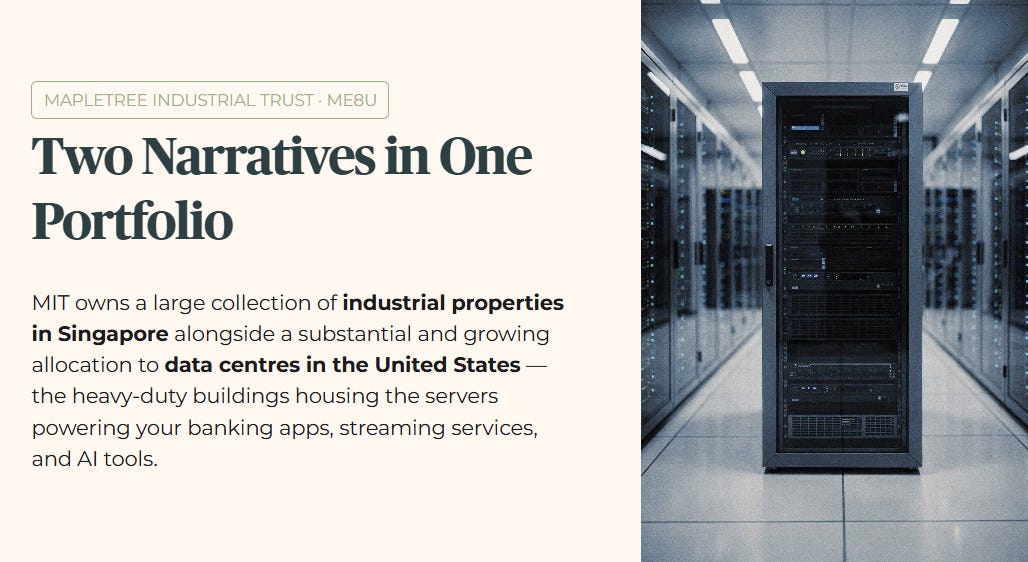

This trust presents two distinct investment narratives rolled into a single portfolio. It owns a large collection of industrial properties in Singapore alongside a substantial and growing allocation to data centres located in the United States. For anyone new to this space, data centres are the heavy-duty physical buildings that house the rows of computer servers powering everything from your daily banking application to your favourite evening streaming service.

This data centre narrative is something we can see and experience in our daily lives. Every single time a person interacts with an artificial intelligence tool, streams a high-definition video, or makes a digital payment at a hawker stall, a server inside a data centre somewhere in the world is running hot. Mapletree Industrial Trust has positioned itself to capture this demand by renting out these specialised spaces to major technology corporations. The trust is currently trading at S$1.94 as at June 26 2026, and I am tracking its price movements to understand how the market values this blend of traditional industrial factories and modern digital infrastructure.

Whether the numbers behind this REIT clear a strict income investor’s thresholds is a question I would want answered before committing any capital. That is the deeper research I am still learning to do.

The next thing Angela does is run each of these three REITs through a strict yield, gearing, and interest coverage screen — and the moment those numbers hit the 4.7% / 35% / 4.0x thresholds, the story you have just read looks very different.