Three Things Every Singaporean Investor Must Check Before Buying Any Stock | Masterclass 101 | EP1619

Most Singaporeans can tell you the price of a stock. Almost none of them can tell you whether that stock is actually safe to own at fifty-five.

Most Singaporeans can tell you the price of a stock. Almost none of them can tell you whether that stock is actually safe to own at fifty-five.

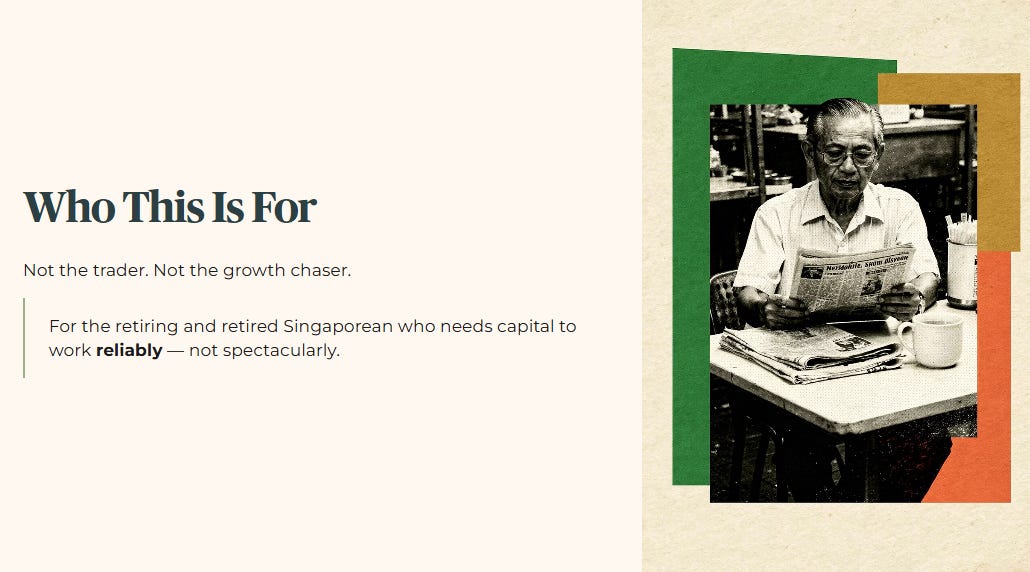

Before we get into the numbers, I want to say who I am doing this for — not the trader with a twenty-year runway, not the growth chaser hunting the next ten-bagger, but the retiring and retired Singaporean who needs their capital to work reliably, not spectacularly.

I have been covering the SGX long enough to know that the question most retail investors never ask is not “what does this stock pay?” — it is “can this stock keep paying it?” That gap between the headline number and the forensic reality is where retirement portfolios quietly come apart, and today I want to close it for good.

If you have been following Iggy for a while, you have probably heard terms like gearing ratio, interest coverage ratio, and distribution yield thrown around in the deep dives. And if you have ever felt like those terms were explained too fast, or assumed too much background knowledge, this piece is specifically for you.

This is not a dumbed-down version of forensic investing. It is the entry point — the three checks that underpin every single stock verdict I publish, translated into plain language with real consequences attached. Master these three, and you will never again look at a high-yielding stock the same way.

We will also look at how transaction costs quietly erode your returns before you even make your first trade — and what you can do about it.

In This Article:

The Traffic Light System — What Zone Is Your Stock In?

Iggy’s Five-Zone Framework — Plain Language Translation

Iggy’s Insight

The Fruit Tree Test — Why Your Dividend Is Not a Bank Interest Payment

The Three Warning Signs Your Fruit Tree Is Struggling

Iggy’s Insight

The Two Numbers That Tell You If the Balance Sheet Is Safe

Balance Sheet Safety — Plain Language Scenario Table

A Note on Transaction Friction — The Hidden Leak Most Investors Ignore

Putting It Together — Your Three-Check Forensic Starter Kit

Your Three-Check Forensic Starter Checklist

Closing

Iggy’s Forensic Disclaimer

Important Partner Disclosure

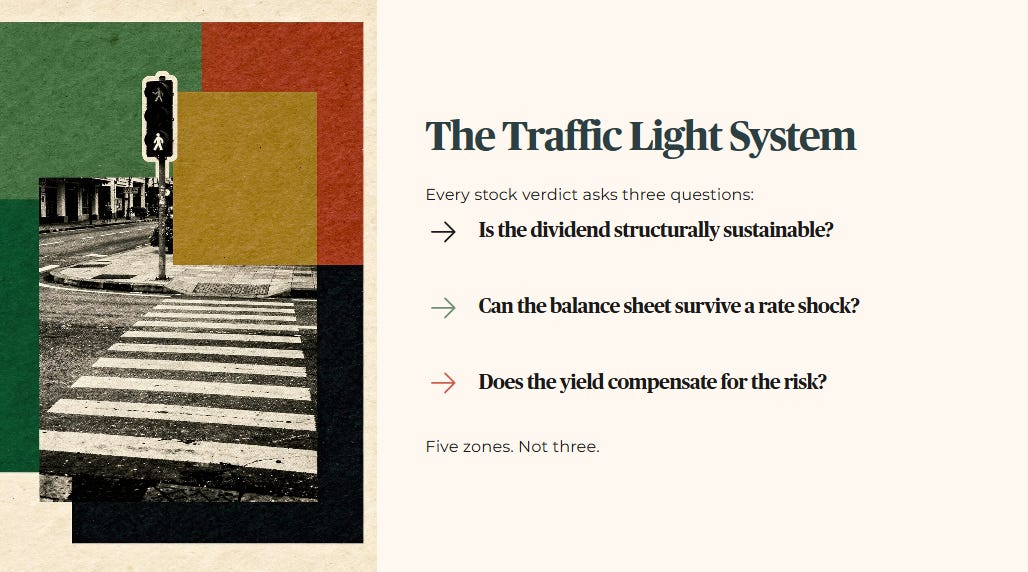

The Traffic Light System — What Zone Is Your Stock In?

Let us start with the framework that sits underneath every Iggy verdict.

When I assess a stock, I am not just asking whether it pays a dividend. I am asking whether that dividend is structurally sustainable, whether the balance sheet can survive a rate shock, and whether the yield actually compensates you for the risk you are taking. Those three questions together determine which of five zones a stock falls into.

Think of it exactly like a traffic light — but with five positions instead of three.

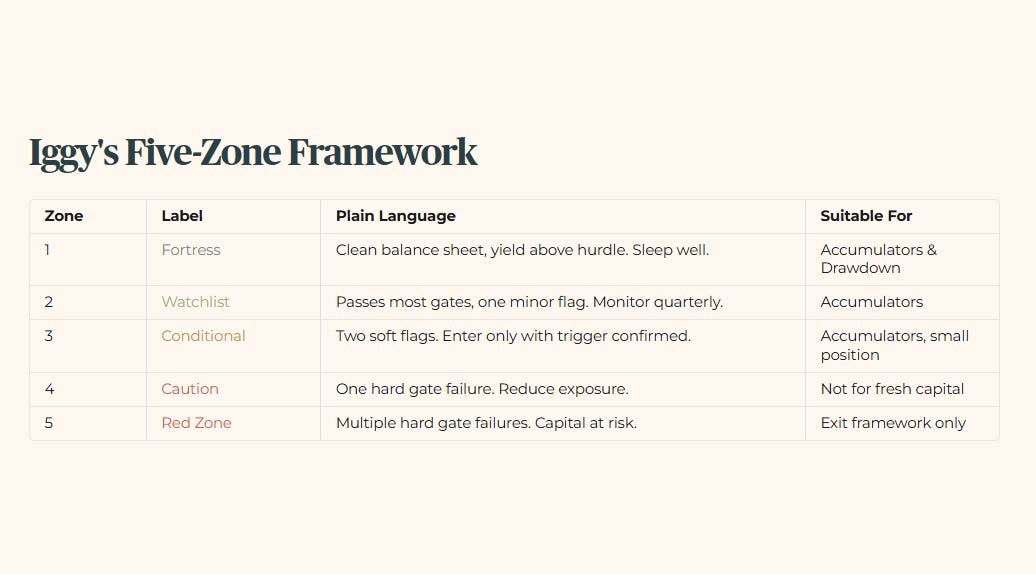

Iggy’s Five-Zone Framework — Plain Language Translation

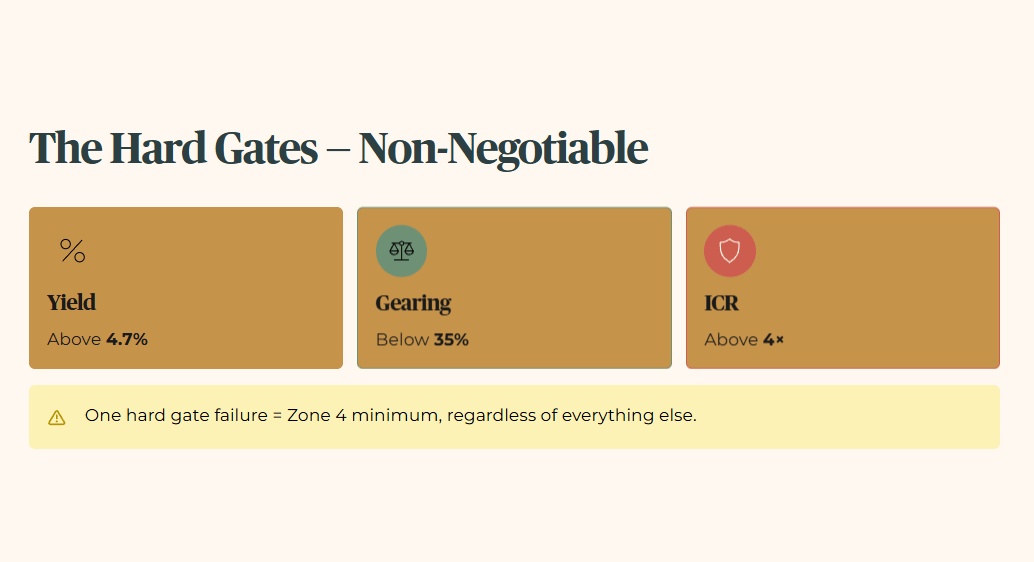

The hard gates — the non-negotiable thresholds — are yield above four point seven percent, gearing below thirty-five percent, and interest coverage ratio above four times. A single hard gate failure drops a stock to Zone Four minimum, regardless of how good everything else looks.

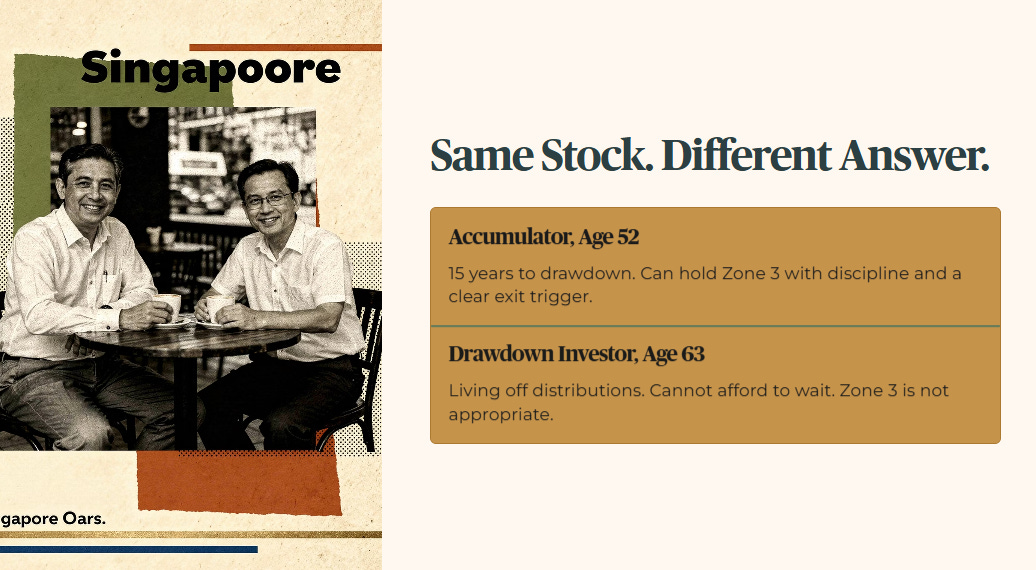

The zone that is right for you depends entirely on where you sit in your investing life. The Accumulator — still working, still building — can hold a Zone Three position with a clear exit trigger and the time to wait it out. The Drawdown Investor living off distributions cannot afford that patience. Same stock, same zone, completely different answer.

This is why the zone system matters for a beginner. You do not need to read a full annual report to get oriented. You just need to know which zone the stock is in — and what that zone means for someone at your stage of life.

Iggy’s Insight

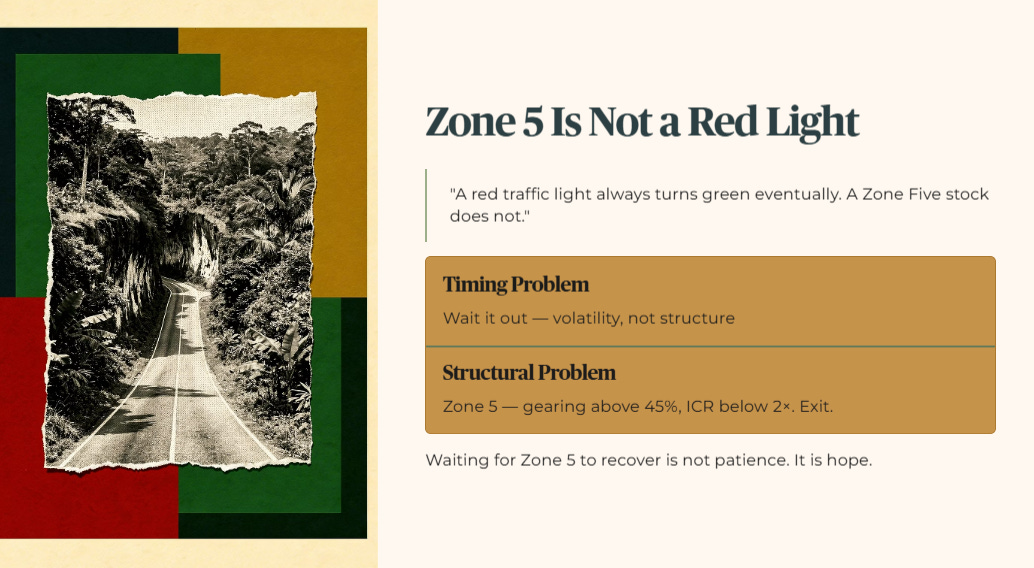

The traffic light analogy breaks down in one important way: a red traffic light always turns green eventually. A Zone Five stock does not. When gearing exceeds forty-five percent and the interest coverage ratio falls below two times, the company is not pausing at a red light — it is running out of road. The distinction matters because retail investors are conditioned to wait out volatility. Forensic investing asks a different question: is this a timing problem or a structural problem? Zone Five is almost always structural. For the Drawdown Investor in particular, waiting for a Zone Five position to recover is not a strategy. It is hope dressed up as patience.

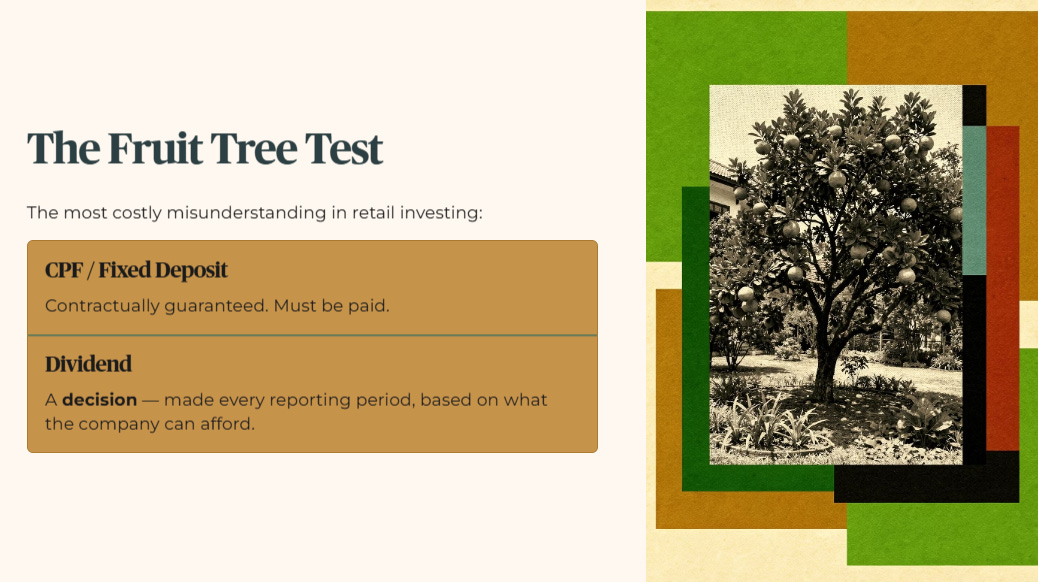

The Fruit Tree Test — Why Your Dividend Is Not a Bank Interest Payment

This is the misunderstanding that costs Singaporean retail investors the most money, and it is almost never explained clearly.

When you put money in a CPF Special Account or a fixed deposit, the interest payment is contractually guaranteed. The bank or government must pay it. There is no scenario in which they decide to pay you less because their business had a bad quarter.

A dividend does not work this way. A dividend is a decision — made by a board of directors, every single reporting period, based on what the company can actually afford to distribute after paying its operating costs, its interest bill, and its capital commitments.

Think of it like a fruit tree in your garden.

A healthy fruit tree — good soil, adequate water, no disease — produces fruit reliably season after season. You can plan around that harvest. But if the soil starts drying out, if the roots are being crowded by debt, if the tree is being forced to produce more fruit than it can naturally sustain, one dry season is all it takes for the harvest to fail. And unlike a bank deposit, nobody is legally obligated to top up your basket.

The Three Warning Signs Your Fruit Tree Is Struggling

The yield number on a stock screener tells you what the stock is paying right now. It tells you nothing about whether that payment is coming from genuine operating income or from a bucket that is quietly running dry.

This is why I always look at the earnings base underneath the yield. A fourteen percent yield from a company reporting a net loss at the shareholder level is not a gift. It is a warning.

Iggy’s Insight

The CPF Special Account currently pays four percent — guaranteed, government-backed, zero balance sheet risk. Any equity position yielding below four point seven percent is being beaten by an instrument you already have access to without taking a single dollar of equity risk. My minimum yield hurdle of four point seven percent is not arbitrary. It is the floor at which equity risk begins to make mathematical sense for a Singaporean investor managing retirement capital. Below that floor, you are not being compensated. You are being flattered by a number. For the Accumulator, dipping below the hurdle requires a specific growth catalyst to justify the yield sacrifice. For the Drawdown Investor, there is no justification. The income simply does not work.

The Two Numbers That Tell You If the Balance Sheet Is Safe

You do not need to read a full set of financial statements to assess whether a stock’s balance sheet is retirement-grade. You need two numbers. Just two.

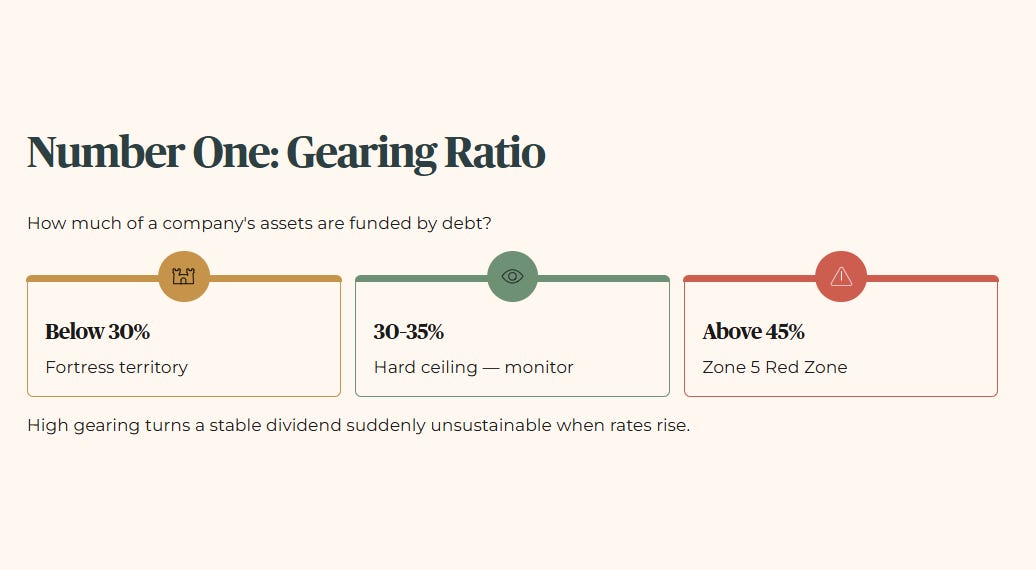

Number One: Gearing Ratio

Gearing measures how much of a company’s assets are funded by debt rather than equity. Think of it like the loan-to-value ratio on a property — except instead of a bank setting the limit, you are setting it yourself.

My hard ceiling is thirty-five percent. Below thirty percent is fortress territory. Above forty-five percent is Zone Five Red Zone.

Why does this matter at your stage of life? Because a highly geared company has a fixed, non-negotiable interest bill every single year — regardless of whether the economy is growing, whether occupancy rates are holding, or whether the distribution you were counting on gets cut. When rates rise, that interest bill expands. When revenue falls, the coverage shrinks. High gearing is the mechanism by which a seemingly stable dividend becomes suddenly unsustainable.

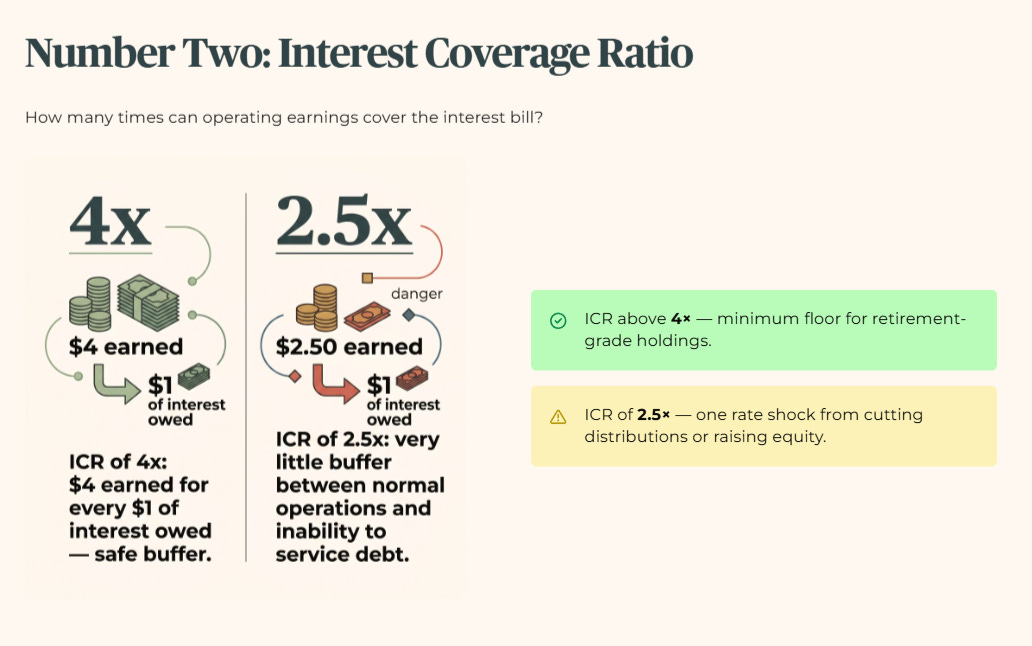

Number Two: Interest Coverage Ratio

The interest coverage ratio tells you how many times over a company can pay its interest bill from its operating earnings. An ICR of four times means the company earns four dollars of operating income for every one dollar of interest it owes. My minimum floor is four times.

An ICR of two point five times means there is very little buffer between normal operations and a situation where the company cannot comfortably service its debt without cutting distributions or raising equity.

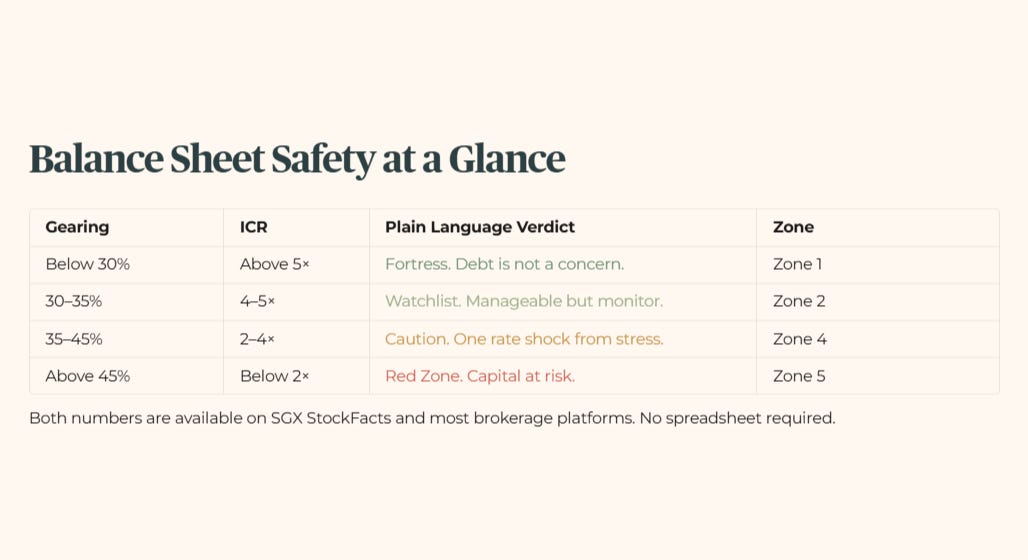

Balance Sheet Safety — Plain Language Scenario Table

These two numbers — gearing and ICR — are available on every stock’s factsheet, on SGX StockFacts, and on most brokerage platforms. You do not need to calculate them yourself. You need to know what the thresholds mean and why they exist.

A Note on Transaction Friction — The Hidden Leak Most Investors Ignore

In the world of dividend investing, we spend a lot of time talking about the yield spread — the difference between what a stock pays you and the risk-free rate. But there is a hidden leak that most retail investors completely ignore: transaction friction. If you are deploying S$10,000 into a Singapore REIT, and your broker eats a chunk of that in minimum commissions or platform fees, you are starting your investment in the red.

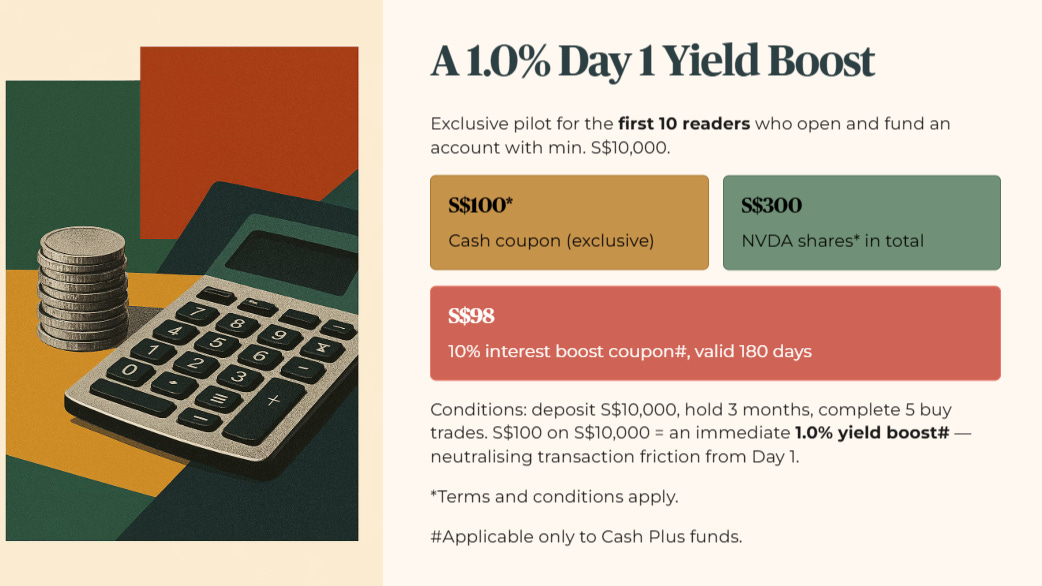

Data is only useful if you have the tools to act on it without getting eaten alive by those fees. That is why I use Longbridge. They are currently the only platform in Singapore offering Lifetime $0 Commission^ for US, HK, and SG stocks. Their data visualisation is also some of the fastest I have used, which is critical when you are timing an entry in a volatile market.

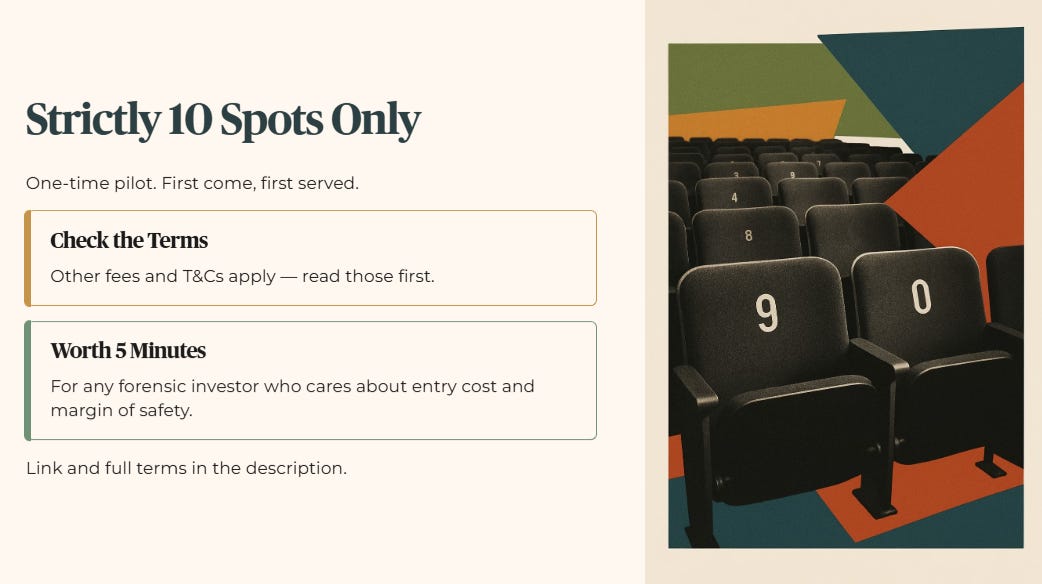

To help you plug that leak, I have partnered with Longbridge for a specific pilot programme. For the first ten readers who open and fund an account with a minimum of S$10,000, they are offering a direct S$100* cash credit on top of their generous welcome rewards. Simply put, if you deposit S$10,000, hold it for three months and complete five buy trades, you will receive an exclusive S$100 cash coupon, S$300 worth of NVDA shares in total, as well as a ten percent interest boost coupon valid for one hundred and eighty days valued at S$98.

Why does this math matter to a forensic investor? Because S$100 on a S$10,000 deposit is an immediate one percent Day One Yield Boost. It is the simplest way to neutralise transaction friction and protect your margin of safety before you even buy your first share.

This is a one-time pilot, strictly limited to the first ten spots. Link and full terms are in the description. Other fees and terms and conditions apply, so read those first. But for a forensic investor who cares about entry cost, this is worth five minutes of your time.

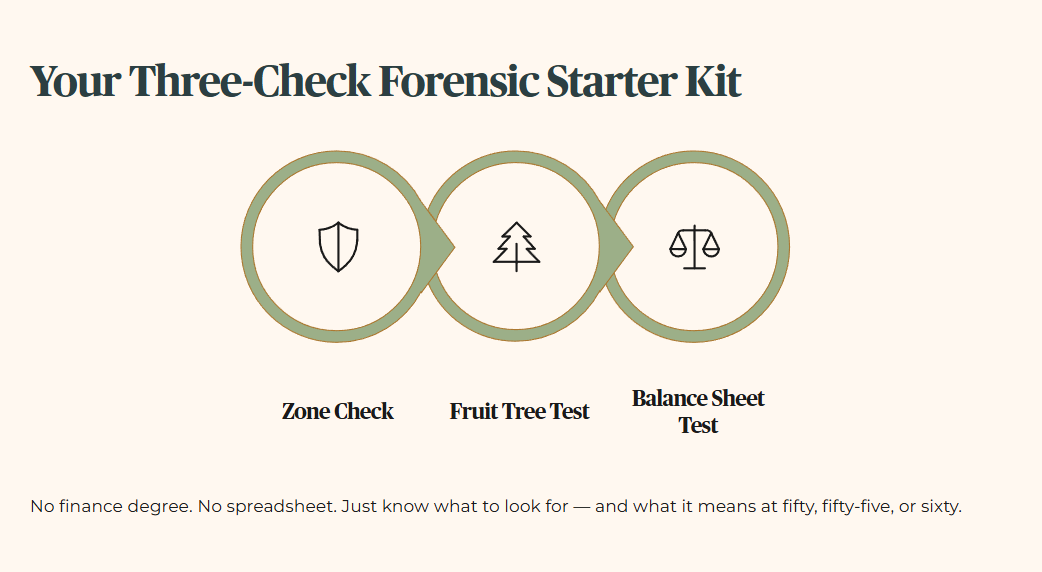

Putting It Together — Your Three-Check Forensic Starter Kit

You now have the three tools that underpin every single Iggy verdict.

The zone system tells you where a stock sits on the safety spectrum before you read a single line of analysis. The fruit tree test tells you whether the yield you are being offered is coming from genuine operating income or from a bucket being quietly depleted. And the two balance sheet numbers — gearing and ICR — tell you whether the company has the structural strength to keep paying you through a rate cycle, a recession, or a sector downturn.

None of these require a finance degree. None require you to build a spreadsheet. They require you to know what to look for — and what the numbers actually mean for a Singaporean investor at fifty, fifty-five, or sixty who cannot afford to treat their retirement capital as a learning experience.

Your Three-Check Forensic Starter Checklist

If a stock fails any one of these three checks, it does not automatically mean you cannot own it. It means you need to understand exactly what risk you are taking — and whether that risk is appropriate for your stage of life.

The Accumulator at fifty-two with fifteen years to drawdown can hold a Zone Three position with discipline and a clear exit trigger. The Drawdown Investor at sixty-three living off distributions cannot. Same stock. Completely different answer.

Closing

Forensic investing is not complicated. It is disciplined. The three checks in this masterclass are the same ones I apply to every name I cover — from the Zone One fortress REITs to the Zone Five positions that should never have been held at retirement weight in the first place.

If you want to see these three checks applied to real stocks in real time — with the full soft flag breakdown, zone trajectory commentary, and zero-day access before the free versions drop — that is exactly what Iggy’s Elite Investors receive with every forensic audit I publish.

The link is below. The first ten Longbridge spots are also below. Start with the balance sheet. Everything else follows.

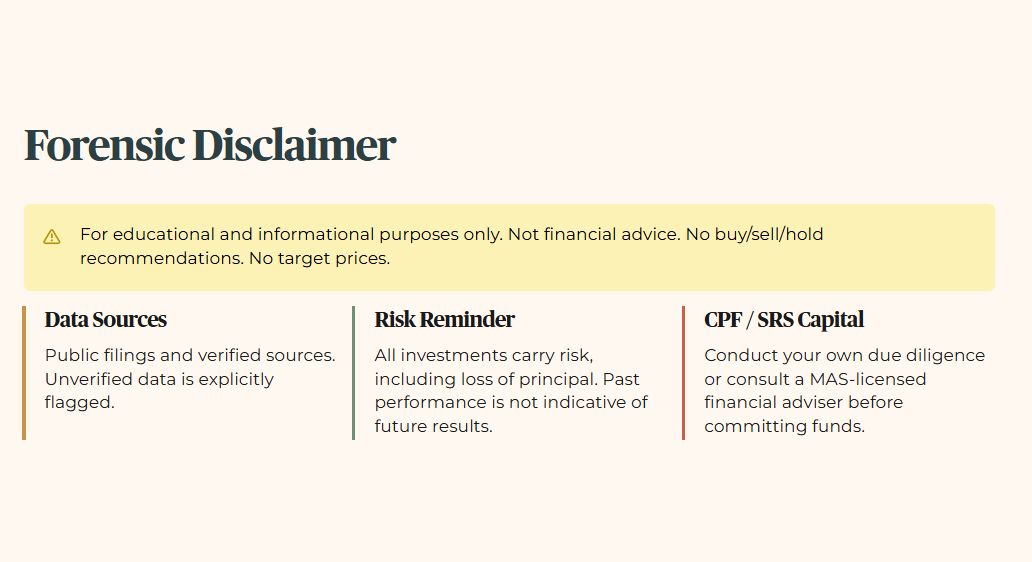

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.

Important Partner Disclosure

This content is a paid collaboration with Longbridge Singapore. It is intended for general awareness and does not constitute investment advice or a recommendation for any specific financial product.

Licensing Note: The presenter is not a licensed financial adviser. Views expressed are solely those of the presenter and do not necessarily reflect the position of Longbridge Singapore. Investments involve risk; you may lose your principal. This advertisement has not been reviewed by the Monetary Authority of Singapore. Always seek independent professional advice if unsure.