74% of AI Chips Are Made By One Company And It’s Terrifying | 🦖EP1557

No TSMC = no iPhone, no ChatGPT, no DBS app

Silicon Sovereign: Why 74% of the World’s AI Future Runs Through One Foundry — And What It Means for Your Heartland Portfolio

The number that stopped me was not the yield. It was the seventy-four percent.

In a global economy where most industrial giants fight for single-digit margin improvements, TSMC has quietly reached a level of dominance that defies standard market physics. When seventy-four percent of your revenue comes from advanced nodes that no other entity on the planet can manufacture with consistent yield, you are no longer a participant in a market. You are the market.

The consensus narrative is obsessed with geopolitical headlines and the “Taiwan discount.” It is failing to price this anomaly into long-term models. The forensic trail does not lead to a tech story. It leads to a structural monopoly that acts as the sole enabler for the artificial intelligence era.

For the Singaporean investor managing a transition toward retirement adequacy, this shift represents a fundamental realignment of the risk-reward map.

In This Article:

The TSMC Story

Section 2 The Local Impact The Wallet

Section 3 The Data Proof The Evidence

Section 4 The SGX Sector Map Scenario Matrix and Sector Watch

Section 5 The Singapore Investor Playbook Shock Absorption and Retirement Impact

Section 6 The Forensic Conclusion

Iggy’s Forensic Compliance Standards Standard Disclaimer

The TSMC Story

We are operating in an environment where a six-month Singapore T-bill offers a 1.47% yield. The CPF Special Account remains a sanctuary benchmark at four percent. Against this backdrop, the TSMC story is not about chasing the next shiny object in a brokerage app. It is about identifying the “Monopolistic Floor” that protects a portfolio’s growth engine when traditional yield-bearing assets are being compressed.

The stake for a forty-five-year-old professional in Bedok or Toa Payoh is the potential for a massive “Forensic Gap” between TSMC’s intrinsic value as the world’s silicon sovereign and a market price that still treats it like a cyclical foundry play.

On the surface, the geopolitical noise makes the stock look risky. But here is the uncomfortable truth. If TSMC stops, the global economy stops. Your entire portfolio, from industrial REITs to bank dividends, will face a shock that no amount of diversification can fully absorb.

🦎 Iggy’s Insight

The psychological gap between institutional rhetoric and raw data has reached a breaking point. Fund managers publicly debate the “silicon shield” and potential supply chain disruptions. But the same institutions are quietly increasing their allocations to the only company capable of fabricating the chips that power their own trading algorithms. The market is pricing TSMC for a conflict it cannot survive, while ignoring a monopoly it cannot live without. The data shows that the AI infrastructure phase is not a bubble. It is a total customer reorganization. The forensic punchline is simple. You are not buying a semiconductor stock. You are buying a toll booth on the only road to the future of compute.

Section 2: The Local Impact (The Wallet)

The cost of living in the Singapore heartland has a direct, invisible umbilical cord to the fabrication plants in Hsinchu.

When we look at household expenses in Marine Parade or Jurong East, we focus on obvious levers like electricity tariffs or the price of a chicken rice set. But the forensic reality is that the “AI tax” is being quietly integrated into every digital service and hardware replacement cycle we pay for.

If TSMC maintains its sixty-six percent gross margin, a record peak achieved in the first quarter of 2026, the cost of that margin is eventually passed down to the Singaporean consumer. Your next smartphone, your next laptop, and even the cloud services that power your workplace are all priced based on the “Debt Wall” of chip manufacturing costs. This is not a percentage in isolation. It is a structural upward pressure on the replacement cost of the technology that defines modern life.

In the context of CPF and SRS calculus, the macro environment has created a unique tension. With the six-month T-bill yield at 1.47%, the “Sanctuary” benchmark of the CPF Special Account at four percent becomes even more valuable.

For an investor searching for yield in a declining rate environment, the forensic data suggests a “Yield Trap” for those who over-prioritize short-term cash over growth enablers. TSMC, with its approximately 0.71% dividend yield, clearly fails the forensic minimum yield hurdle of 4.7% required for income-focused sanctuary assets.

Yet for a mid-career professional using an SRS account, the strategic choice is not between a two percent yield and a four percent yield. It is about whether to allocate capital to the primary growth engine of the global economy. The forensic picture suggests that as Singapore’s own semiconductor sector contributes seven percent to national GDP, the domestic heartland investor has a front-row seat to this expansion.

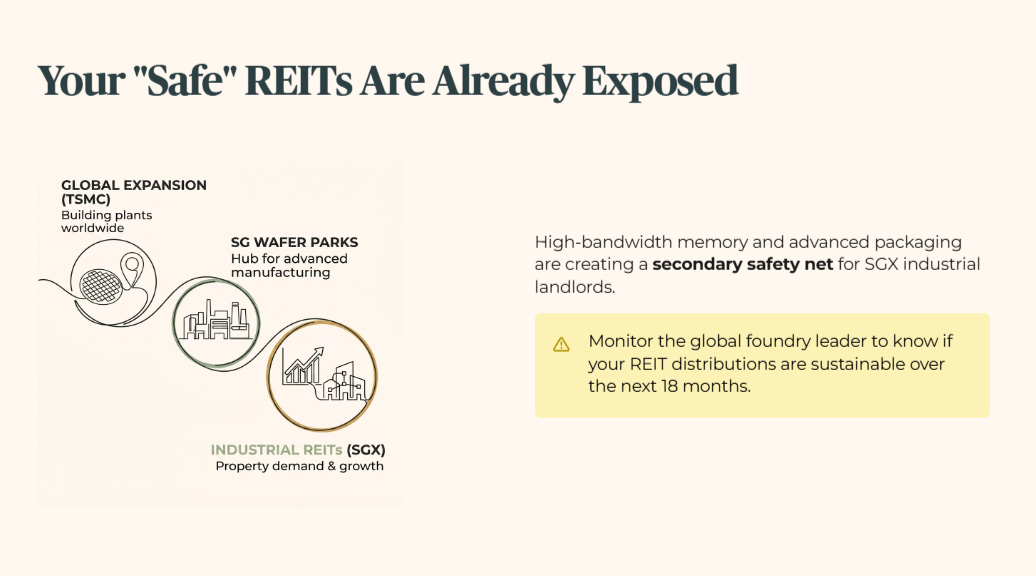

The SGX sector exposure most directly impacted by this silicon hegemony is found in our industrial REITs and electronics players. As TSMC expands its global footprint and Singapore aggressively positions itself as a critical node through Budget 2026 commitments, the valuations of localized Wafer Fab Parks become central to the portfolio.

We are seeing a historic shift. The high-bandwidth memory requirements for AI and the expansion of advanced packaging facilities are creating a secondary safety net for specific SGX-listed industrial landlords.

The wallet consequence is clear. Your exposure to the semiconductor cycle is likely already embedded in your “safe” REIT holdings. Monitoring the health of the global foundry leader is the only way to understand if those distributions are sustainable over the next eighteen months of sustained macro pressure.

🦎 Iggy’s Insight

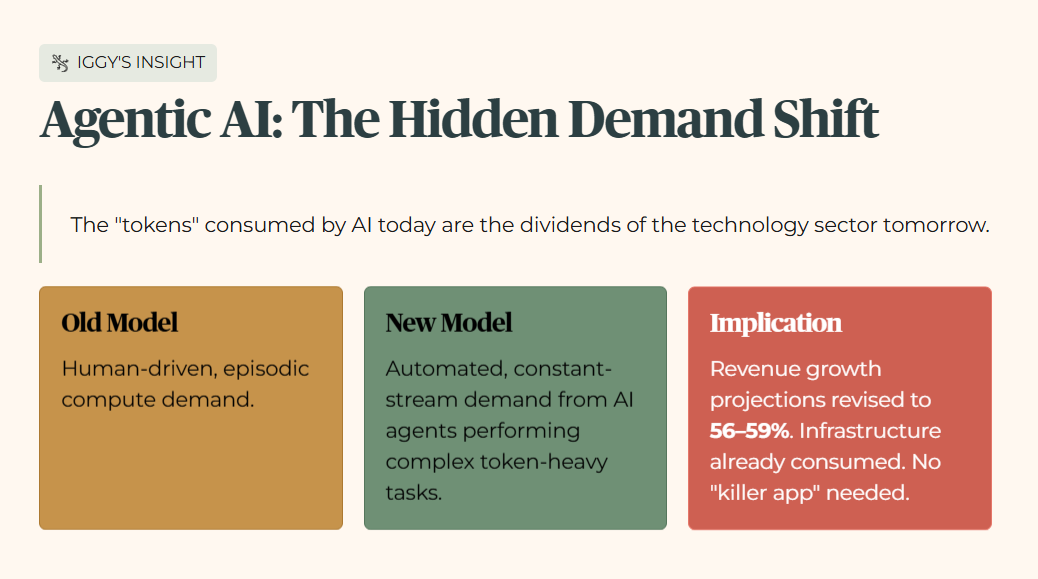

The second-order effect that most retail investors are missing is the “Agentic AI” trend. As AI agents begin to perform complex, token-heavy tasks, the consumption of compute capacity shifts from a human-driven episodic demand to an automated, constant-stream demand. This shift fundamentally changes the utilization rates of leading-edge fabs like those operated by TSMC. The market waits for a “killer app,” but the infrastructure is already being consumed at rates that justify the revised fifty-six to fifty-nine percent revenue growth projections. The forensic punchline is that the “tokens” being consumed by AI today are the dividends of the technology sector tomorrow.

Section 3: The Data Proof (The Evidence)

This is the point where the structural monopoly becomes an undeniable forensic reality.

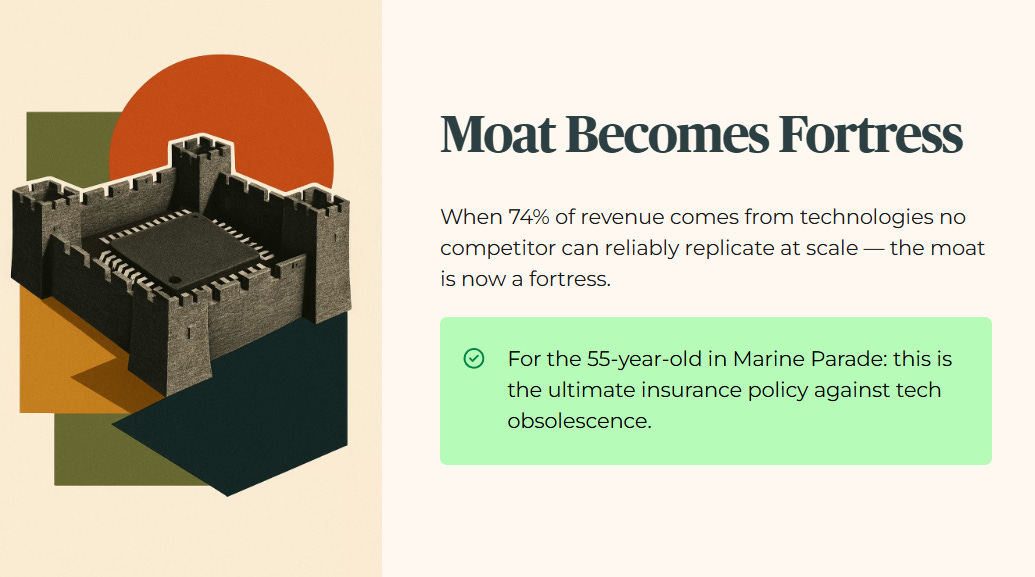

The forensic linchpin that makes the rest of the market noise irrelevant is the seventy-four percent figure.

When nearly three-quarters of a company’s revenue is generated from technologies that no competitor can reliably replicate at scale, the “moat” has become a “fortress.” For a fifty-five-year-old investor in Marine Parade with significant holdings in CPF and dividend-paying blue chips, this number represents the ultimate insurance policy against tech obsolescence.

If your portfolio relies on global growth to sustain its dividends, your reliance on that seventy-four percent share is absolute.

The consequence of this dominance is that TSMC can dictate pricing and force customers to fund its fifty-six billion dollar annual capital expenditure. It is effectively outsourcing its expansion costs to the world’s largest technology companies.

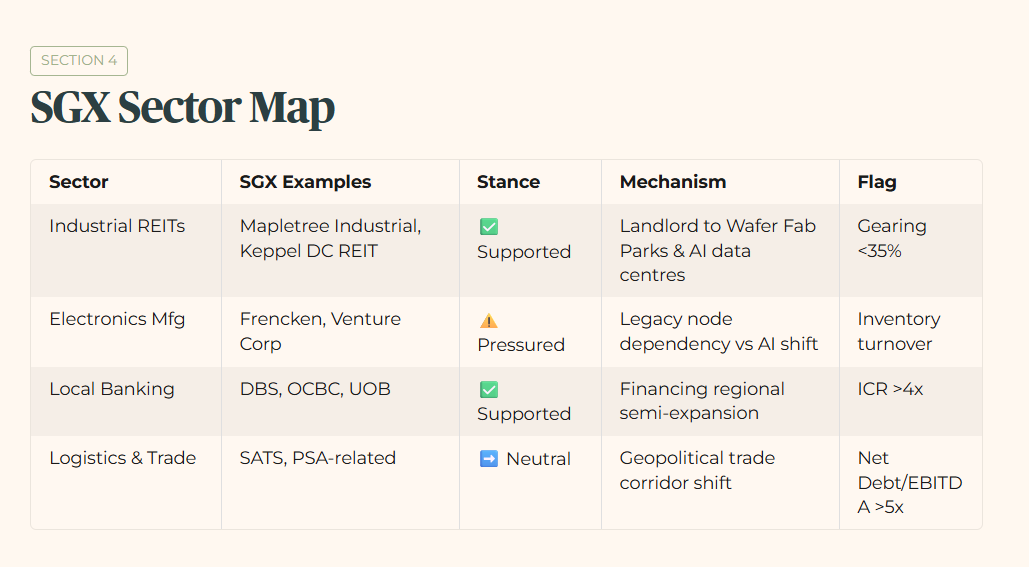

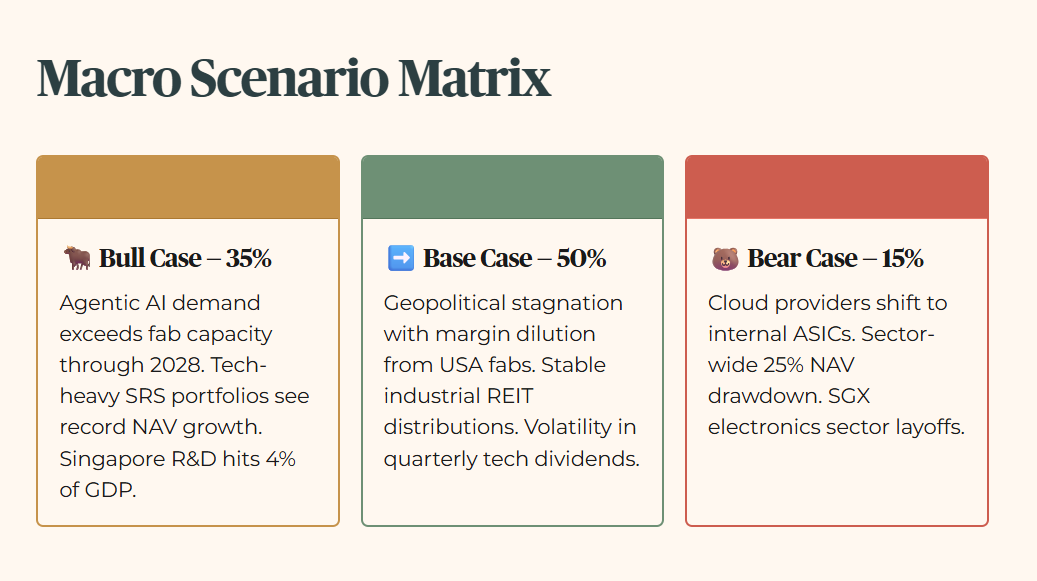

Section 4: The SGX Sector Map (Scenario Matrix and Sector Watch)

The forensic stance across the SGX universe points to cautious optimism for industrial nodes and firm skepticism for retail-facing tech.

The primary risk to the “Silicon Sovereign” thesis remains the pace at which the world’s largest cloud service providers can transition to internal chip designs.

Table 3 — Macro Scenario Matrix

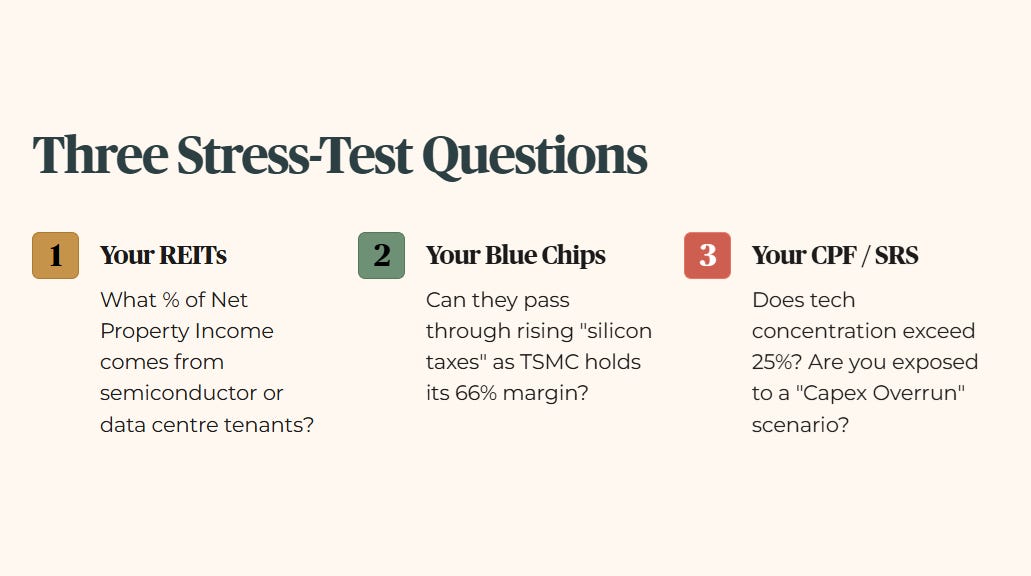

Based on the evidence presented in the scenario matrix, a heartland investor should be directing three specific stress-test questions at their own portfolio right now.

First, for your REIT holdings, what is the specific percentage of Net Property Income derived from tenants in the semiconductor or data center space?

Second, for your blue-chip positions, does the company have the pricing power to pass through the rising cost of “silicon taxes” as TSMC maintains its sixty-six percent margin?

Finally, within your CPF or SRS accounts, does your concentration in the technology sector exceed the twenty-five percent rule, leaving you exposed to a potential “Capex Overrun” scenario?

Because once you actually run those three stress-test questions against your own REIT, blue-chip, and CPF/SRS allocations, the seventy-four percent moat stops being an abstract statistic and starts redrawing your entire portfolio map.