Two Industrial REITs, One Forensic Lens: CapLand Ascendas REIT versus Mapletree Industrial Trust

Behind the 6% Yields: What Balance Sheets Reveal About Retirement Safety

Both of these industrial REITs yield above 6 percent, and both have data centre exposure everyone is excited about. One REIT fails three of my balance sheet gates. The other is balanced precariously on two of them. If you hold either for retirement income, you need to see what the balance sheet is hiding.

Growth chasers may accept the risk. Retirees focused on wealth preservation and dependable drawdown income should not. My forensic standard, built around a 4.7 percent minimum yield hurdle and strict balance sheet gates, is designed to protect that. Today, we put two of the biggest heavyweights on the Singapore Exchange under the microscope to see if their income foundations match their blue‑chip branding.

Think of these ratios like health markers in a medical report. I check them so retirees in Singapore building dividend portfolios get the same forensic clarity that institutional investors take for granted.

The Yield Picture

The Gearing Picture

The ICR Picture

Financial Health Checklist

How Iggy Rates Every Stock

The Occupancy and Data Centre Picture

Valuation and Analyst Consensus

The Bottom Line

Why These Two Names Now

We are sitting at the final trading day of the first half of 2026, and the STI is consolidating near record highs. That kind of market attention matters because when a stock trades actively at record-high valuations, retail investors follow the crowd into names they assume are safe simply because everyone else is buying. For the week ended June 26 2026, CapLand Ascendas REIT (SGX: A17U) alone saw 88 million units traded, with Mapletree Industrial Trust (SGX: ME8U) also registering significant volume, and both sat comfortably within the weekly top active counters.

Both are industrial giants aggressively repositioning toward digital infrastructure. Both yield above 6 percent at current market prices, comfortably clearing my minimum 4.7 percent forensic hurdle. Most importantly for retail investors, both are backed by powerhouse sponsors, CapitaLand Investment and Mapletree Investments respectively.

The forensic question here is not whether these are good businesses or whether their sponsors have deep pockets. They do. The question is whether the income they distribute is sitting on a foundation strong enough for retirement capital at current valuations. In an all-time-high market regime where the STI is operating above 5,000, balance sheet discipline is non-negotiable for incremental buying decisions.

The Yield Picture

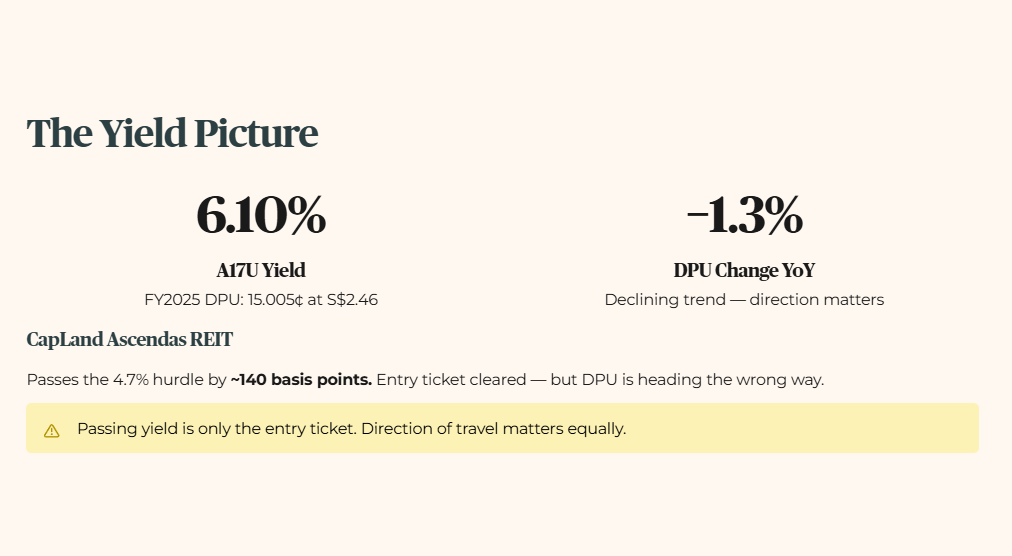

Let us begin with the good news: both names clear my minimum yield hurdle early and clearly. But passing the yield test is merely the entry ticket. The direction of travel matters just as much as the headline number today.

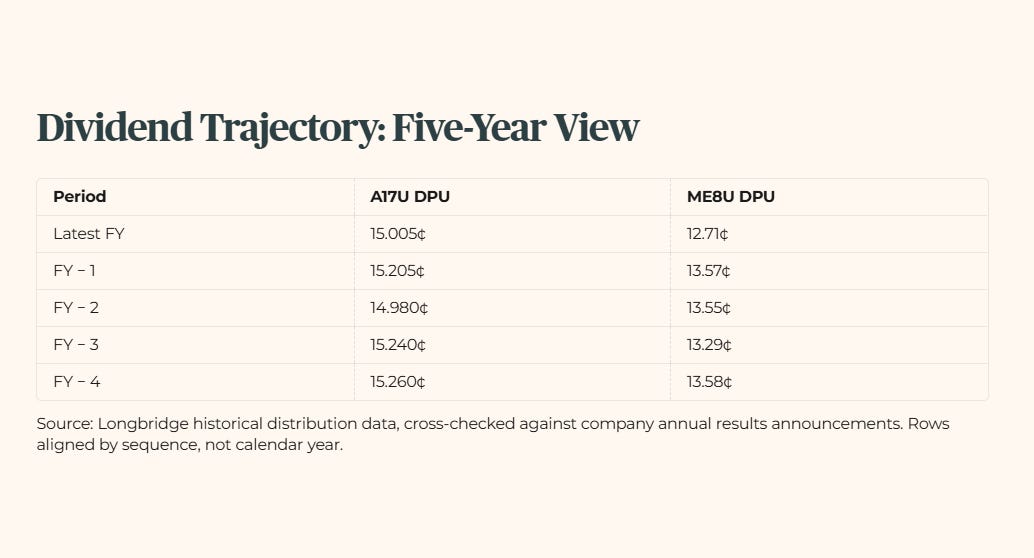

For CapLand Ascendas REIT, the FY2025 DPU came in at 15.005 cents, confirmed from the CapitaLand primary results release. At a stock price of S$2.46, this translates to a trailing yield of approximately 6.10 percent. It passes my minimum hurdle of 4.7 percent by roughly 140 basis points. However, this DPU declined 1.3 percent year on year.

Mapletree Industrial Trust presents a higher headline number. Its FY2026 DPU stands confirmed at 12.71 cents. At a stock price of S$1.93, this gives us a trailing yield of approximately 6.58 percent, passing my hurdle by a very healthy 188 basis points. But looking closer reveals a sharper decline, DPU dropped 6.3 percent year on year. If we exclude a prior year divestment gain to get an honest, like-for-like read, the adjusted DPU still declined by 3.2 percent. Management cites property divestments in Singapore, North America data centre lease non-renewals, and foreign exchange headwinds from a weaker US dollar and Japanese yen against our strong Singapore dollar as the primary culprits.

If you are drawing on these distributions for retirement living expenses, a 3 to 6 percent annual DPU decline compounds into a meaningful income shortfall over a five to ten year horizon. The yield today does not guarantee the yield in three years. Zoom out to five years and the picture sharpens further: CapLand Ascendas REIT has been broadly flat with a mild wobble, while Mapletree Industrial Trust has round-tripped a period of growth back down to below where it started.

Dividend Trajectory, Five-Year View

Note: A17U and ME8U report on different fiscal year ends, so rows are aligned by sequence, latest complete financial year and four years prior, not by calendar year. Source: Longbridge historical distribution data, cross-checked against company annual results announcements.

The Gearing Picture

This is where the structural paths of these two trusts diverge most visibly under our forensic lens.

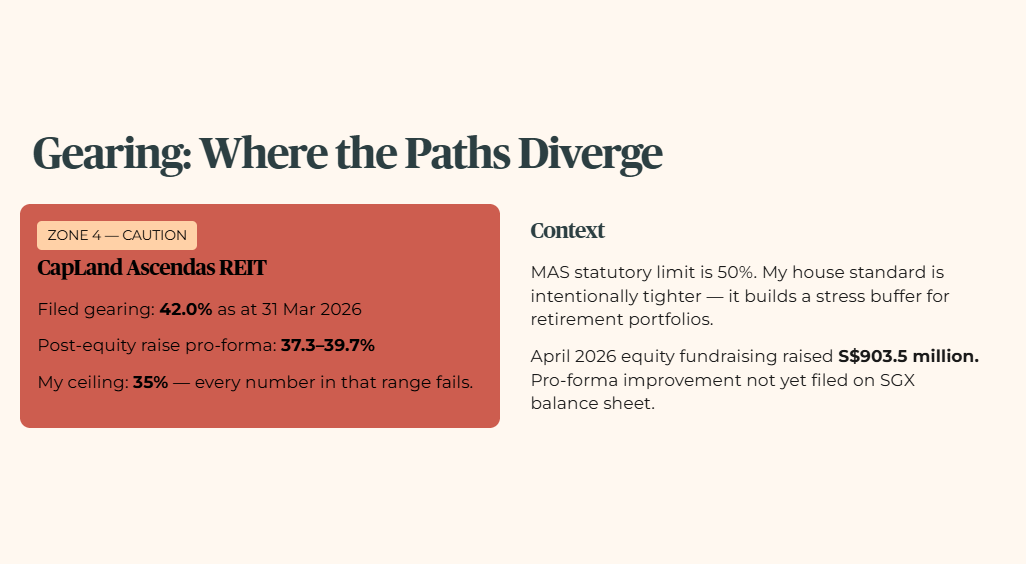

Iggy’s Forensic Zone: Zone 4, Caution (CapLand Ascendas REIT, SGX: A17U)

GEARING ALERT

CapLand Ascendas REIT filed an aggregate leverage (gearing ratio, the percentage of a REIT’s total assets that are funded through borrowed debt) of 42.0 percent as at 31 March 2026. This is a clear hard gate failure against my strict 35 percent house ceiling. Management has guided a pro-forma leverage of approximately 37.3 percent following their April 2026 equity fundraising that raised S$903.5 million. However, a separate DBS research note paints a more conservative pro-forma picture of 39.7 percent post-acquisitions. The honest range for retail investors to track is 37 to 40 percent. Every number in that range breaches my 35 percent ceiling.

To be entirely fair, CapLand Ascendas REIT is not in regulatory distress. The Monetary Authority of Singapore sets a statutory limit of 50 percent. My house standard is intentionally tighter because it builds in a necessary stress buffer for retirement portfolios.

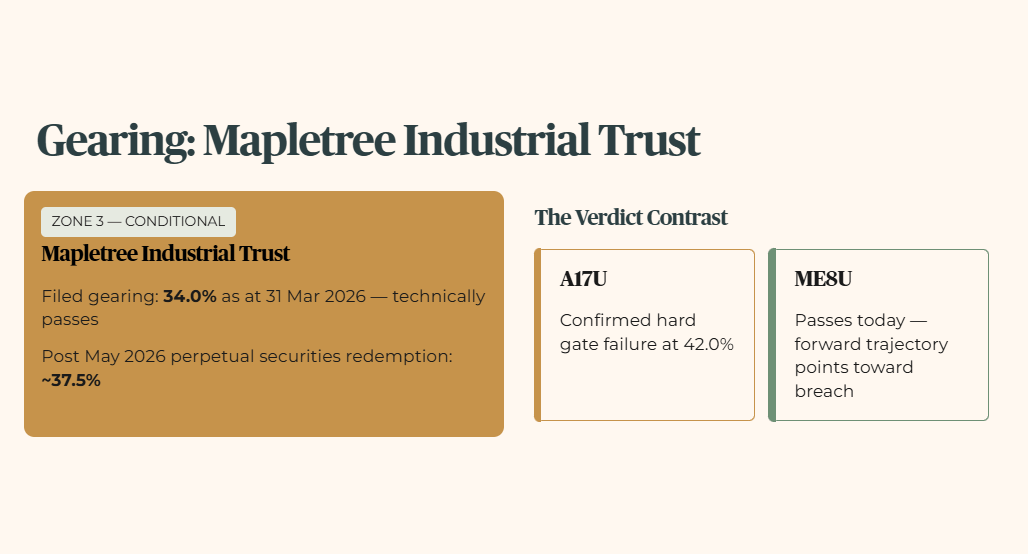

Iggy’s Forensic Zone: Zone 3, Conditional (Mapletree Industrial Trust, SGX: ME8U)

Mapletree Industrial Trust filed an aggregate leverage of 34.0 percent as at 31 March 2026. This technically passes my 35 percent ceiling at the filed level. However, this was completed before their May 2026 redemption of existing perpetual securities, a type of bond with no fixed maturity date, which a REIT can redeem or keep paying interest on indefinitely. Management’s pro-forma guidance indicates that post-redemption, gearing will rise to approximately 37.5 percent.

The gearing verdict is distinct. CapLand Ascendas REIT has a confirmed, filed hard gate failure at 42.0 percent. Mapletree Industrial Trust passes on paper today but its forward trajectory points toward a breach.

The gearing figures clear the statutory ceiling comfortably, but the next section’s full forensic verdict on those same ratios is where the retirement‑grade risk picture finally comes into focus.