UI Boustead REIT IPO: Don't Be the Tai Seng "Smart Money" Auntie

Buying a REIT with 10% vacancy is like paying full price for a 10-piece wing bucket and finding one wing missing.

SECTION 1: THE CATALYST (Why Now?)

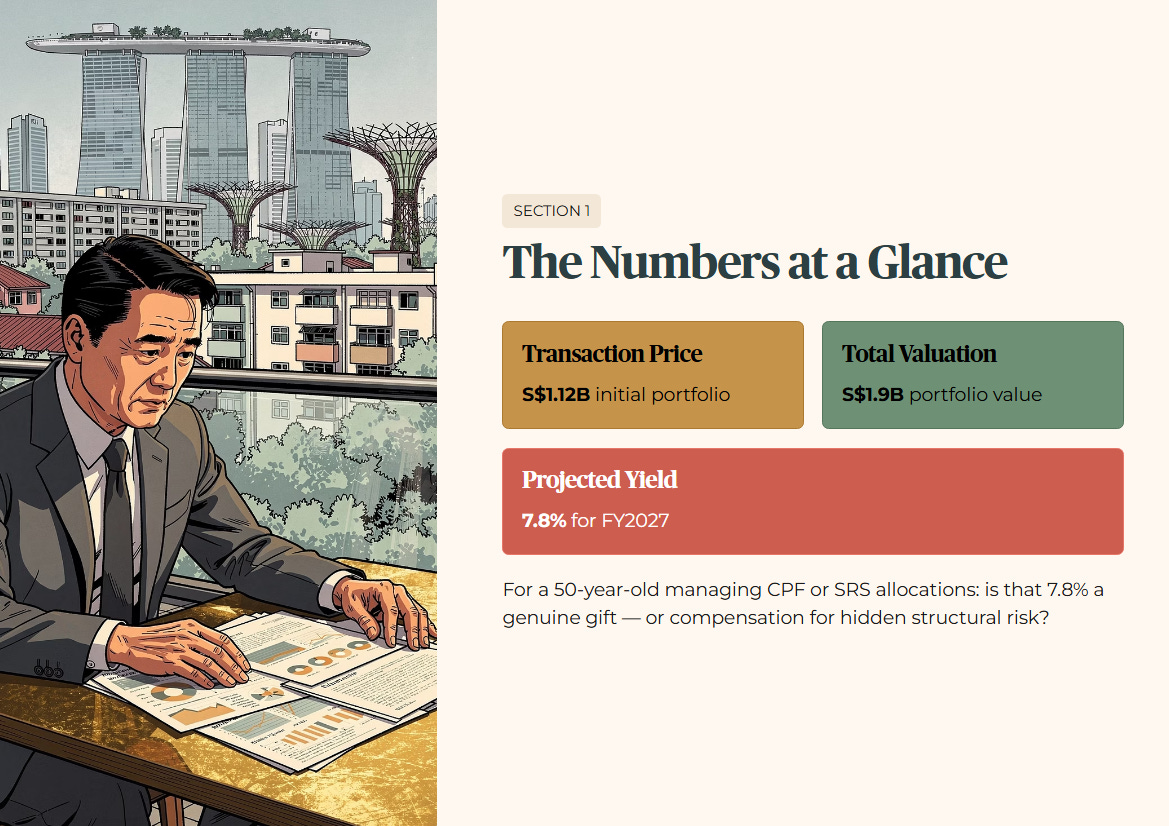

Look, the crowd at the Bedok Marketplace isn’t talking about interest rates; they’re talking about the price of a bowl of laksa. But while the average Singaporean is feeling the squeeze of a shrinking paycheck, the “Smart Money” is lining up for the biggest REIT IPO since 2017. The official lodgement of the UI Boustead Real Estate Investment Trust prospectus on February 26, 2026, followed by the public offer launch on March 5, has sent ripples through the financial district. This isn’t just another listing; it is a S$1.2 billion play in a market that has been starved of high-quality industrial debuts.

Understand, the timing here is everything. We are currently navigating the “Battle for 5,000” in the Straits Times Index while dodging the “Middle East Escalation” involving Israel, Iran, and the USA. This global tension has slapped us with an “Energy Tax” through oil volatility and a “Duration Tax” because interest rates are staying higher for longer than anyone wanted. Right?

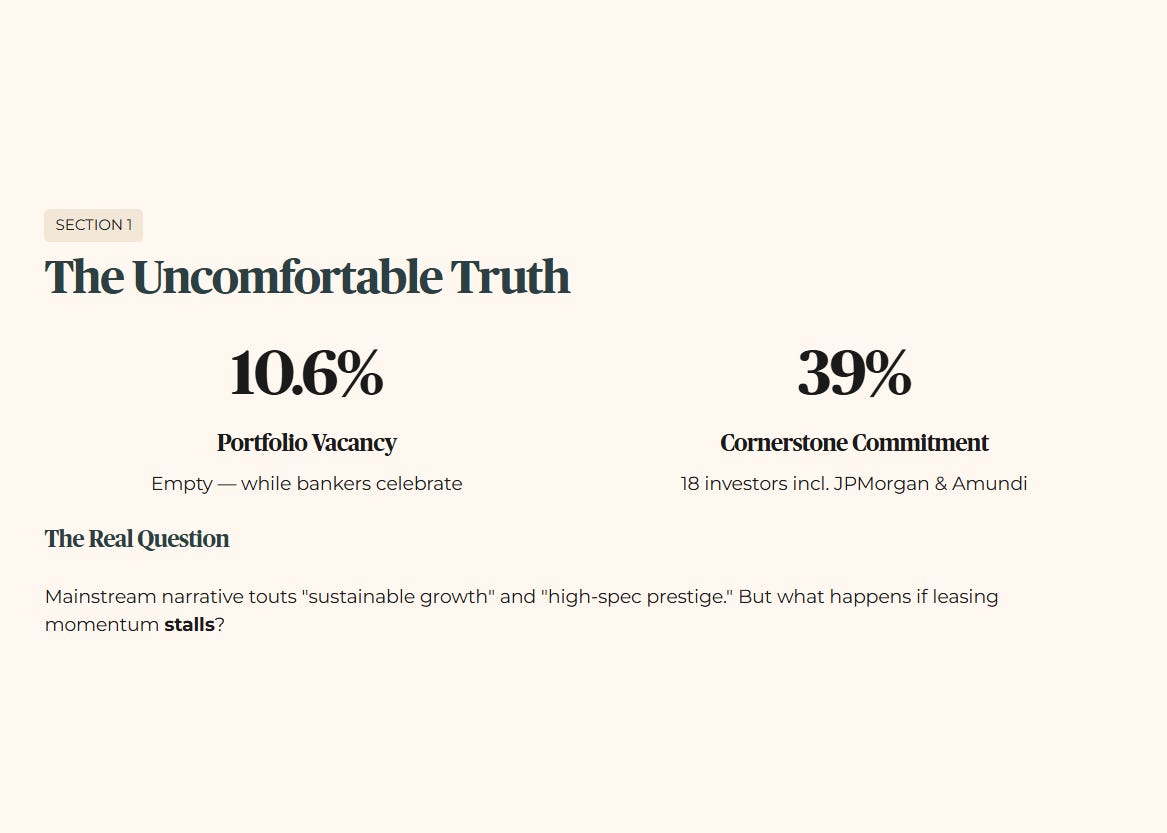

And let’s be honest, the mainstream narrative is shouting about “sustainable growth” and “high-spec prestige.” But here is the uncomfortable truth: the forensic stance suggests a portfolio that is 10.6% empty. While the bankers celebrate the 39% commitment from 18 cornerstone investors—including heavyweights like JPMorgan Asset Management and Amundi—we need to look at what happens if the leasing momentum stalls.

Currently, our 6,400+ free subscribers are seeing this data with a 14-day lag, while our Elite 190 members have already dissected the zero-day forensic breakdown. The total transaction price for this initial portfolio is roughly S$1.12 billion, against a total valuation of S$1.9 billion. For a 50-year-old Singaporean managing a benchmark comparison against CPF or SRS allocations, the real question is whether that 7.8% projected yield is a genuine gift or a compensation for hidden structural risks.

In This Article:

SECTION 1: THE CATALYST (Why Now?)

SECTION 2: THE HEALTH CHECK (Solvency)

SECTION 3: THE WEALTH CHECK (Yield & Cash Flow)

SECTION 4: THE PRICE CHECK (Valuation)

SECTION 5: THE BOTTOM LINE (Iggy’s Forensic Stance)

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite 190

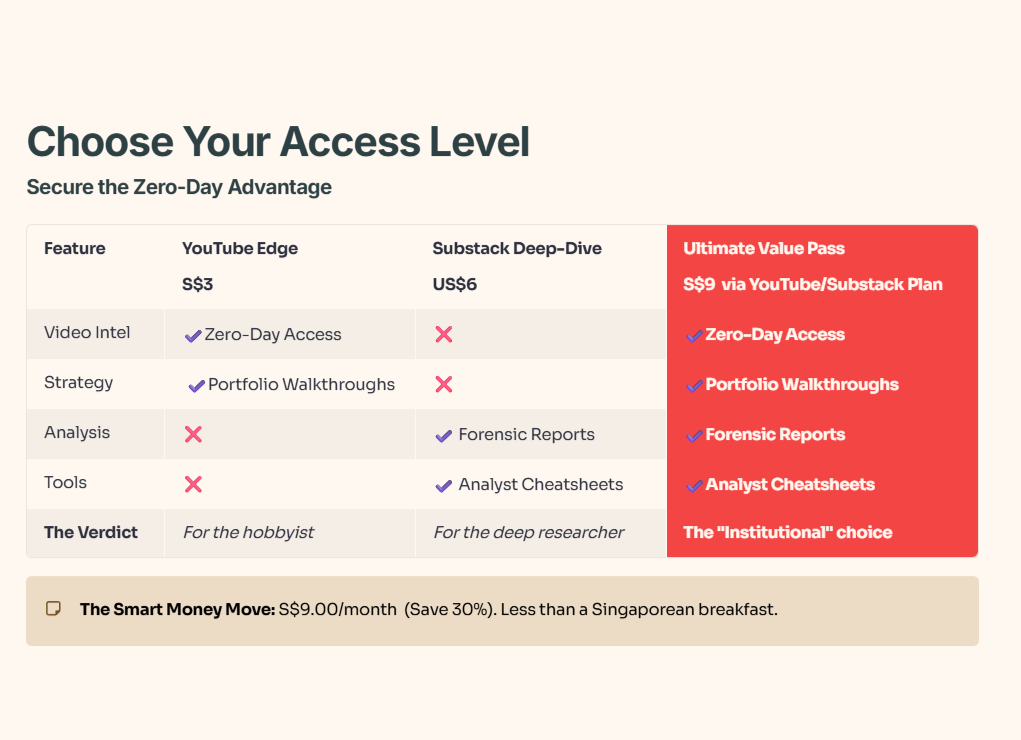

Stop Guessing. Start Auditing. Why do most retail investors fail? Because they read the “Marketing Brochure” while the Elite 190 read the “Forensic Footnotes.” For the cost of one casual lunch, you get the full Equity Evaluation & Growth Income Strategy (EEGIS) toolkit:

Zero-Day Intel: Get my audits before the market reacts.

The Vault: Full access to every forensic scorecard and risk-free spread audit.

Institutional Edge: Cheatsheets designed for the “Bedok-to-Boardroom” investor.

Join 190 high-conviction investors who value math over narratives.

👉 [Upgrade to the Elite 190 Vault]

SECTION 2: THE HEALTH CHECK (Solvency)

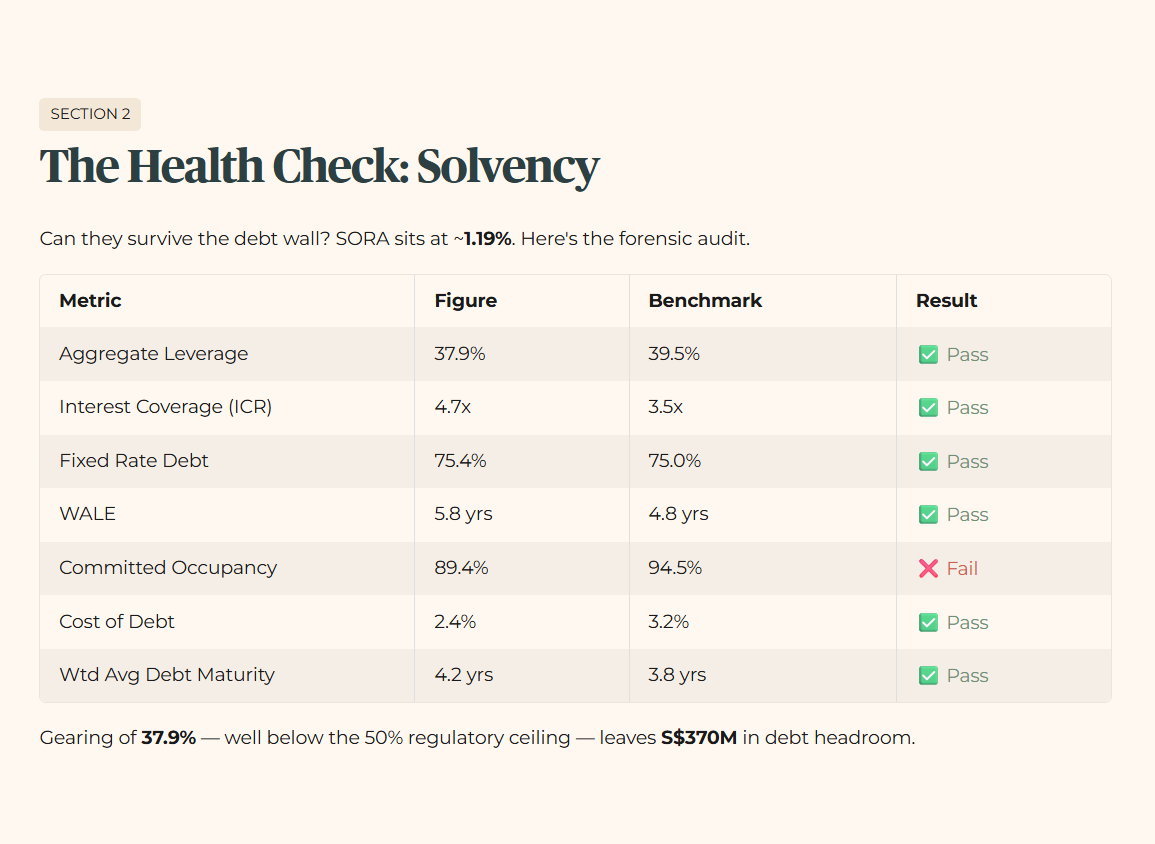

The first question any serious investor asks at the Kopitiam is: “Can they survive the debt wall?” In a world where the Singapore Overnight Rate Average sits around 1.19% (average for now), we need to know if the manager is playing defense or just playing for time.

Financial Health Checklist (Forensic Audit)

The balance sheet shows a capital structure built for the current “Higher for Longer” climate. The gearing of 37.9% is well below the 50% regulatory ceiling, leaving S$370 million in debt headroom.

Educational Note: Gearing

Gearing is like the car loan on your private hire vehicle. If your gearing is too high, one “engine breakdown”—like a major tenant defaulting—can leave you stranded on the PIE without the cash to fix the problem or pay your dividends.

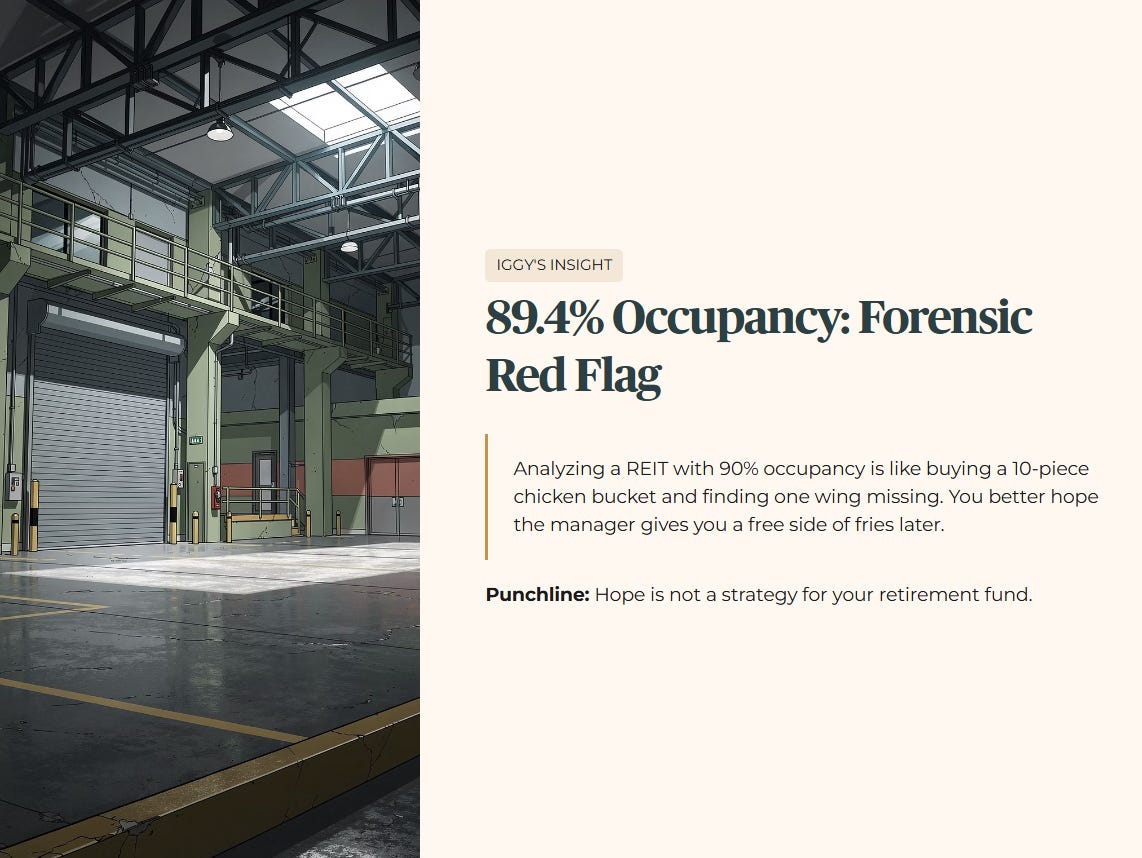

The Interest Coverage Ratio of 4.7x is the star of the show here. It provides a massive safety buffer compared to older industrial REITs that are struggling with 3x coverage. However, we cannot ignore the occupancy. The manager expects to hit 98% by March 2027, but today, it’s a leaky bucket.

Iggy’s Insight: The balance sheet is solid, but that 89.4% occupancy is a “Forensic Red Flag.” You are essentially reviewing a building that is 10% empty while waiting for a “recovery” that the manager promises is just around the corner. Analyzing a REIT with 90% occupancy is like buying a 10-piece chicken bucket and finding one wing missing; you better hope the manager gives you a free side of fries later. Punchline: Hope is not a strategy for your retirement fund.

SECTION 3: THE WEALTH CHECK (Yield & Cash Flow)

Is the payout organic or engineered? We have to audit the fuel. The projected 7.8% yield for the 2027 financial year is significantly higher than the sector average of 6.4%.

Is the payout organic or engineered? We have to audit the fuel. The projected 7.8% yield for the 2027 financial year is significantly higher than the sector average of 6.4%.