FLCT: Why I’m Ignoring UOB’s $1.30 Buy Rating (Numbers Don’t Lie) 📉 | EP1602🦖

And it’s not the BUY call paying you. It’s S$5m asset sales propping 2.95¢ DPU

UOB Kay Hian BUY on FLCT ($1.30) on 6 May 2026

One Number To Rule Them All

A single 99.8 percent occupancy figure is doing a lot of heavy lifting right now. It is the number the institutional analyst leads with, the number the headlines repeat, and the number that is supposed to make you feel safe about your retirement income sitting in this trust. But here is what that number does not show you — the interest coverage is cracking, and that crack just tripped the hardest gate in my forensic screen. This audit is about what the headline is hiding.

My job is simple, even if the balance sheet is not. I go through the numbers that the press release skips — the debt, the interest bill, the cash flow — so that the Singaporean investor building or living off a dividend portfolio gets the same clarity that the big institutions take for granted.

I have been watching the logistics space in Singapore and Australia for a while now. The physical assets are impressive. The warehouses are full. But impressive buildings and a healthy balance sheet are two very different things, and right now Frasers Logistics and Commercial Trust is showing me one without the other.

Section 1 — What The Analyst Is Saying

UOB Kay Hian analyst Jonathan Koh maintains a BUY rating on Frasers Logistics and Commercial Trust, ticker BUOU, with a target price of S$1.30. His case rests on one central idea: the income paid to unitholders — called the Distribution Per Unit, or DPU, which works like a dividend for REIT investors — is recovering, driven by strong rental increases across the logistics portfolio.

The Australian warehouses in New South Wales are doing particularly well, with rents jumping 71.7 percent on renewal. The trust also just acquired a logistics property in the Netherlands for S$64.1 million, which should add to income immediately. And in Singapore, 83 percent of the space that Google vacated at Alexandra Technopark has already been committed to new tenants, with leases starting in early 2027.

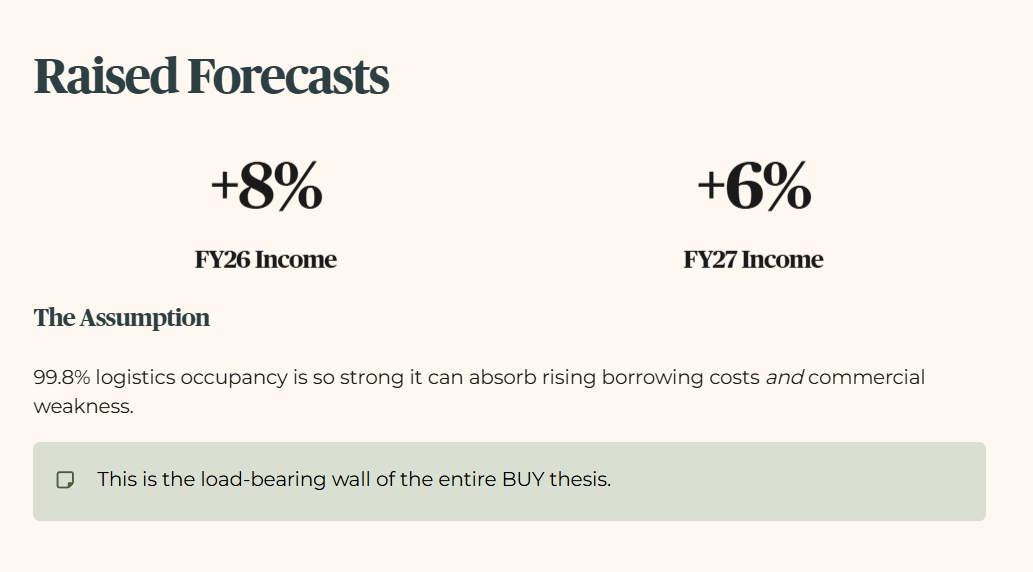

The analyst has raised his income forecasts by 8 percent for this financial year and 6 percent for next year on the back of these moves.

The assumption holding all of this together: the logistics portfolio is so full — 99.8 percent occupied — that it can absorb rising borrowing costs and weakness in the commercial properties.

Section 2 — Iggy’s Forensic Screen

This is where I put the numbers through my own filter — not to argue with the analyst, but to ask a different question. Not “can this REIT grow?” but “is my retirement money safe here right now?”

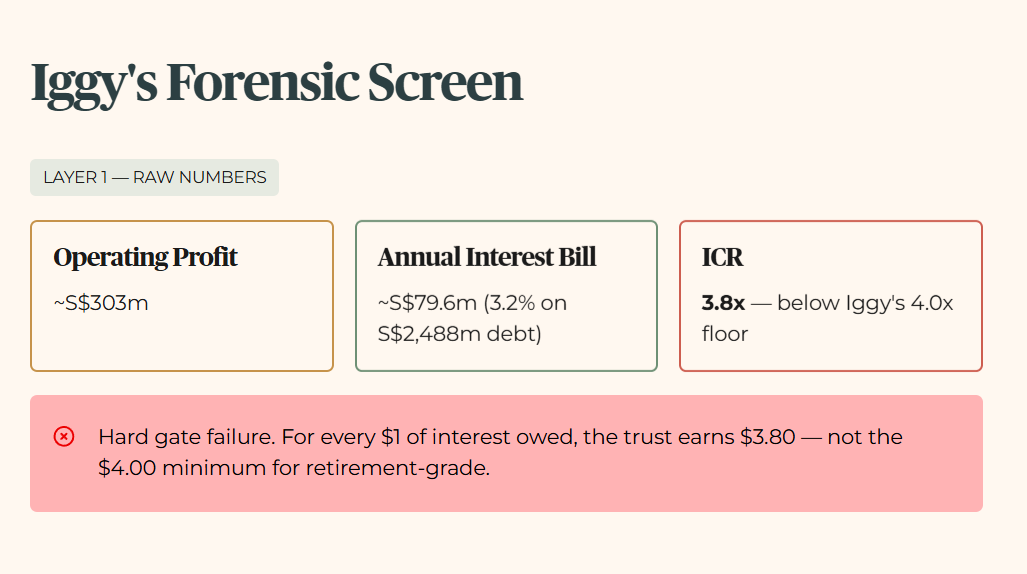

Layer 1 — The Raw Numbers The trust currently earns roughly S$303 million in operating profit before interest and tax. Its annual interest bill is approximately S$79.6 million, based on a borrowing cost of 3.2 percent on S$2,488 million of total debt. That gives an Interest Coverage Ratio — ICR — of 3.8 times. In plain English: for every dollar of interest the trust owes, it is earning three dollars and eighty cents. My minimum for a retirement-grade holding is four dollars. It just missed, and that is a hard gate failure in my system.

Layer 2 — Trend Check We do not have a clean five-year ICR history for this session, so I cannot show you exactly how far it has fallen. What I can tell you is that 3.8 times is not where a trust with this level of debt should be sitting, and the direction of travel — rising borrowing costs, commercial vacancies — suggests it is not about to improve quickly on its own.

Layer 3 — How It Compares We will cover the peer comparison in Section 4. The short version: the sector is under pressure across the board.

Layer 4 — What Happens If Rates Climb If borrowing costs nudge up just 10 percent — from 3.2 percent to about 3.5 percent — the annual interest bill rises to S$87.5 million. The ICR drops to 3.46 times. That is not a cliff, but it is the wrong direction for a trust that is already below my floor.

Layer 5 — What This Means For Your Money If you are 55 or older with CPF or SRS funds in this trust, a sub-4x ICR is the balance sheet equivalent of a household running low on its emergency fund. The income is still coming in, but the buffer has thinned. If something unexpected hits — a tenant leaves, rates spike, a property gets revalued down — there is less cushion between you and a distribution cut.

Iggy’s Financial Health Checklist

Iggy’s Forensic Zone: Zone 4 — Caution

[ZONE BOILERPLATE EXPLAINER — INSERT FROM MASTER TEMPLATE HERE]

Four Soft Flags Found:

Total debt is 7.8 times operating earnings — well above the 5x level where I start getting uncomfortable.

The trust is trading at S$0.99 against an InvestingPro fair value of S$0.77 — you are paying a 28.6 percent premium for an asset with a cracked ICR.

Two occupancy failures — Singapore logistics at 94.3 percent and the commercial portfolio at 88.4 percent both fall below my 95 percent threshold for prime assets.

The average debt maturity is 2.8 years — meaning a significant chunk of borrowing needs to be refinanced relatively soon, in an environment where rates are not falling as fast as anyone hoped.

Section 3 — The Dividend: Is It Real?

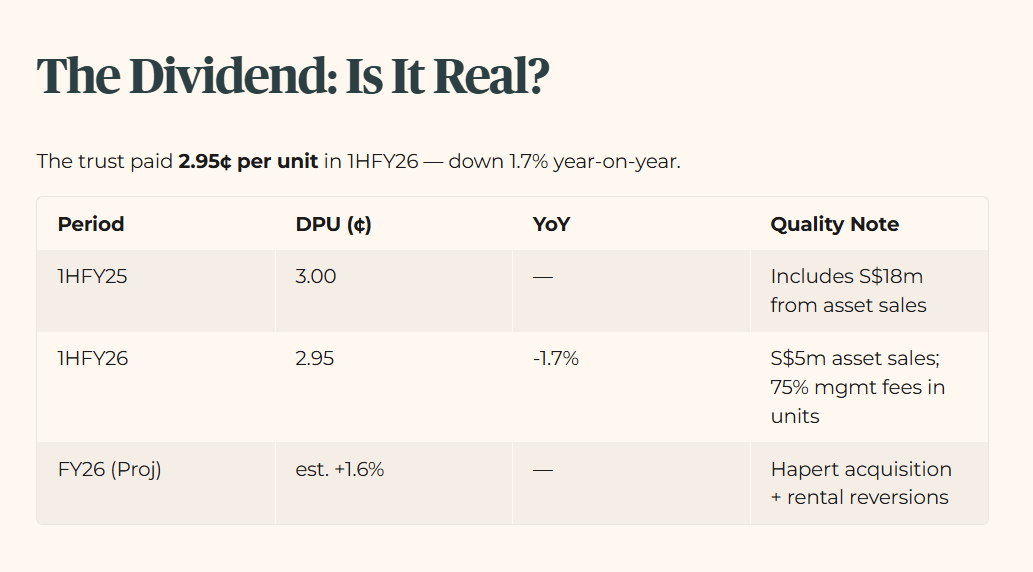

The trust paid 2.95 cents per unit in the first half of this financial year. That is down 1.7 percent from the same period last year. The analyst expects recovery. I want to look at where the income is actually coming from before I accept that story.

Dividend Trajectory Table

Two things are propping up the current distribution. First, the trust is using proceeds from selling assets to top up the income — that money only comes around once. Second, it is paying 75 percent of its management fees in newly issued units rather than cash. That preserves cash for distributions today, but it slowly dilutes existing unitholders over time. Neither of these is alarming on its own, but together they tell me the dividend is in a support phase, not a growth phase. The organic income is not yet strong enough to stand alone.

But once you run the stress‑test on how much of that 2.95¢ DPU is riding on one‑off asset sales and scrip fees rather than recurring cash flow, the sustainability picture looks very different.