Don't Be The Kiasu Index Investor: The iEdge Next 50 Trap in Valuemax | 🦖

Chasing the iEdge Next 50 rebalance might leave you with a thinner slice of fish than your CPF-SA.

You feel it at the wet market every Sunday morning. The fishmonger hasn’t changed the price of the sea bass, but the slice you get in the bag is undeniably thinner. That silent, invisible squeeze on your purchasing power is the exact same dynamic playing out in the Singapore stock market right now. And let’s be honest, the mainstream narrative is currently fixated on the shiny momentum of mid-cap equities, driven entirely by the highly publicised “SGX Next 50 Shuffle”. But here is the uncomfortable truth: institutional index tracking creates a forced buying mechanism that often masks severe structural vulnerabilities hiding deep in the balance sheet. Welcome to the latest zero-day forensic report for our Elite Investors.

Before we even look at the individual companies, we must understand the machinery of the market. The real catalyst here is not a sudden explosion in pawnshop visits or a sudden global shortage of medical ointment. The trigger is the iEdge Singapore Next 50 Index rebalancing, effective March 23, 2026. When an index rebalances, institutional fund managers who track that index do not have the luxury of choice; they are structurally forced to buy the new entrants to match the index weightings.

This is the financial equivalent of a neighbourhood kopitiam suddenly being awarded a Michelin Bib Gourmand. The queue that forms the next day isn’t necessarily because the prawn noodles got better overnight; it is because the guidebook told everyone to show up. We saw the immediate market reaction on March 11, 2026, when the average daily trading turnover (ADT) for prospective components spiked by 18% to S$261 million. This forced liquidity is what has pushed Valuemax Group Ltd and Haw Par Corporation Ltd into the spotlight. But as forensic investors, we do not buy the queue; we audit the kitchen.

In This Article:

Step 1: The Health Check (Solvency and The Debt Wall)

Mandatory Financial Health Checklist

Iggy’s Insight The Debt Wall Check

Step 2: The Wealth Check (Yield & Cash Flow)

Note on the Stress-Test Buffer

Iggy’s Insight The Yield Trap Warning

Step 3: The Price Check (Valuation and The Forensic Gap)

Iggy’s Insight The Forensic Verdict

Step 4: The Bottom Line (The Forensic Stance)

InvestingPro Reality Check

Iggy’s Verdict

About Iggy & the Elite Investors

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Step 1: The Health Check (Solvency and The Debt Wall)

The primary question for any asset in this interest rate environment is whether it can survive its upcoming Debt Wall. We are auditing for solvency, checking if the underlying foundation can withstand the weight of extended holding periods. We apply raw factual analysis and historical benchmarks to determine the strength of the structural frame.

Mandatory Financial Health Checklist

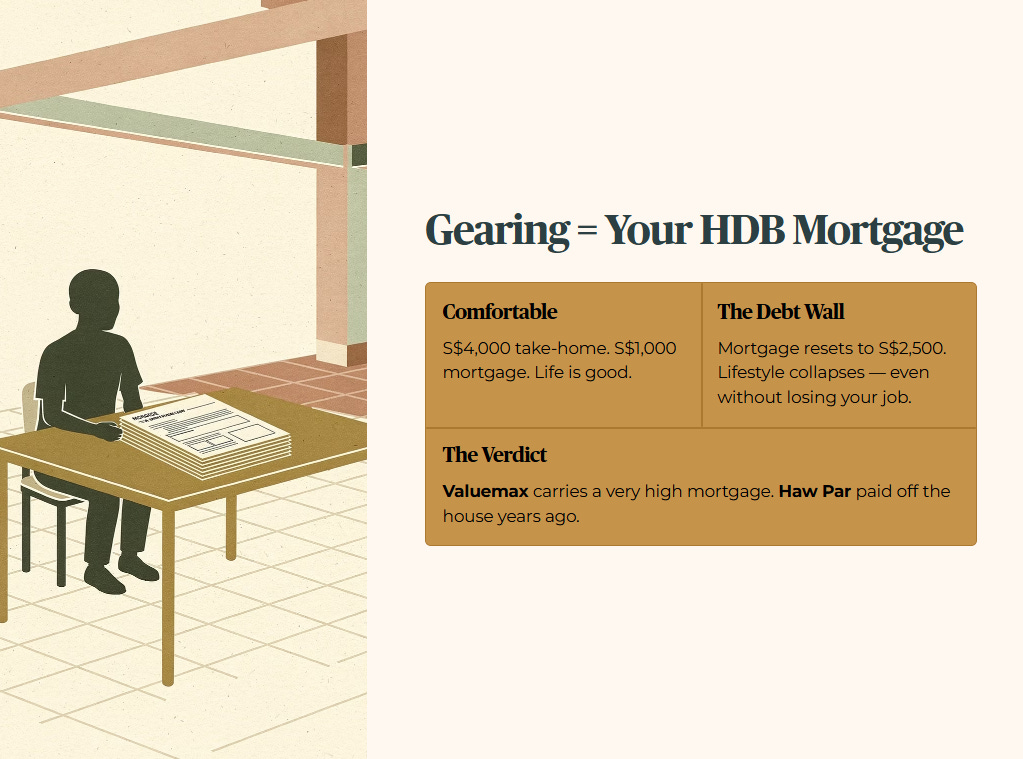

Valuemax is running an aggressive expansionary burn. A gearing ratio of 1.43x means the company is heavily reliant on debt to fund its loan book. While management argues this is standard for pawnbroking, any sharp drop in collateral value—specifically gold prices—could force them into a tight corner. Conversely, Haw Par operates with a true Fortress Balance Sheet. An interest coverage ratio of 173x with effectively zero net debt means they are entirely insulated from borrowing costs.

Think of Gearing like the monthly mortgage on your HDB flat. If your take-home pay is S$4,000 and your mortgage is S$1,000, you are comfortably geared. But if your mortgage resets to S$2,500 due to rising rates—hitting the Debt Wall—your lifestyle collapses even if you didn’t lose your job. Valuemax is carrying a very high mortgage; Haw Par paid off the house years ago.

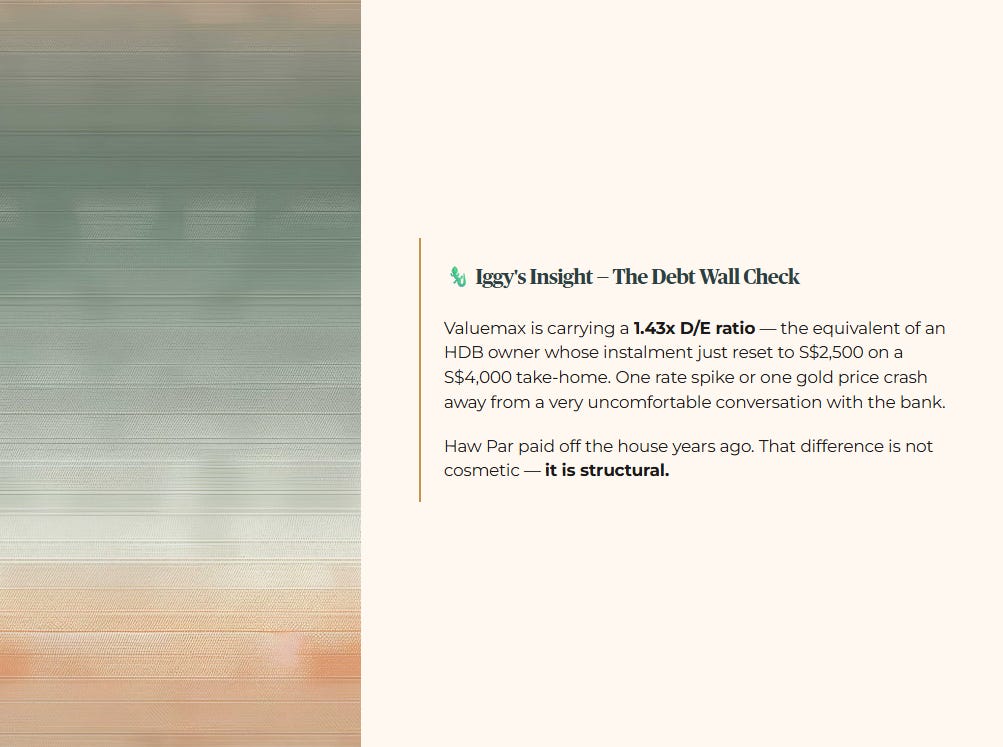

🦎 Iggy’s Insight The Debt Wall Check

Gearing is just your mortgage in disguise. Valuemax is carrying a 1.43x debt-to-equity ratio — the equivalent of an HDB owner whose monthly instalment just reset to S$2,500 on a S$4,000 take-home. The house isn’t on fire yet, but one rate spike or one gold price crash away from a very uncomfortable conversation with the bank. Haw Par paid off the house years ago. That difference is not cosmetic — it is structural.

Step 2: The Wealth Check (Yield & Cash Flow)

We must distinguish between an Organic NPI and an Engineered Yield. A yield is only as good as the cash flow that funds it. Retail headlines will scream about Haw Par’s trailing 9.06% dividend yield. Ignore it. That figure is a massive distortion caused by a one-off special dividend in 2024. If you buy based on that headline, you are walking straight into a Yield Trap. The honest, forward-looking ordinary yield is roughly 2.7%.

Valuemax, meanwhile, offers a 3.73% yield. But remember from our health check that their Free Cash Flow is negative (-S$170.5m). They are essentially borrowing money to lend money to pay a dividend.

Note on the Stress-Test Buffer: For this audit, I apply a Stress-Test Buffer using a conservative floor of 3.2% as our working “risk-free” benchmark. While the current spot rate for 6-month MAS T-bills is approximately 1.36%, I test the thesis against this “higher-than-spot” hurdle. If the math holds at 3.2%, the Margin of Safety at current levels is a fortress. We audit for the storm, not just the sunny day.

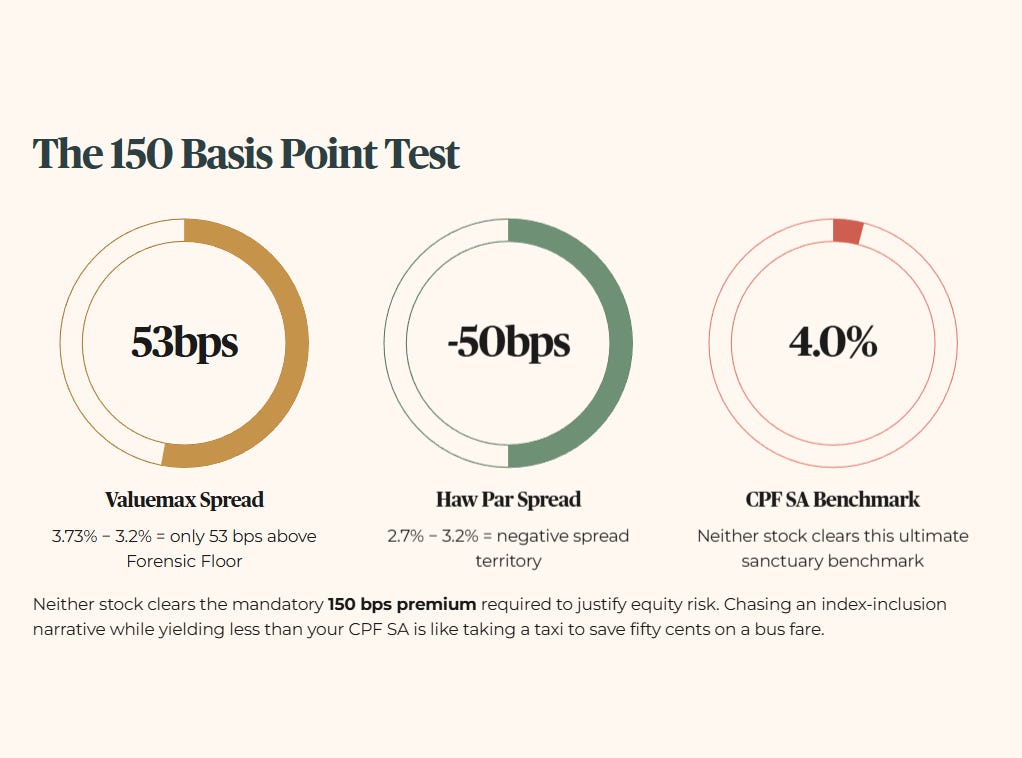

Applying the Iggy Forensic Floor of 3.2%, we check the 150 Basis Point Threshold:

Valuemax: 3.73% - 3.2% = 0.53% (53 bps spread).

Haw Par (Ordinary): 2.7% - 3.2% = -0.50% (-50 bps spread).

The ultimate sanctuary benchmark is the CPF Special Account, currently yielding 4.0%. Neither Valuemax nor Haw Par’s ordinary dividends clear this hurdle, let alone offer the mandatory 150 basis point premium required to justify equity risk. For a 60-year-old Bedok investor locking up capital, chasing an index-inclusion narrative while yielding less than your CPF SA is like taking a taxi to save fifty cents on a bus fare. The math simply does not support the risk.

🦎 Iggy’s Insight The Yield Trap Warning

Neither stock clears the 150 basis point premium above Iggy’s 3.2% Forensic Floor. Haw Par’s ordinary yield is actually negative spread territory. For a 60-year-old Bedok investor, locking up capital in an index-inclusion story that yields less than your CPF SA is like taking a taxi to save fifty cents on a bus fare. The arithmetic does not lie. Know what you are actually being paid to take on the risk.

In the next section, I’ll walk you line by line through the Forensic Gap maths that explains why one of these “Next 50 darlings” is quietly selling at a 23% discount to its real balance-sheet value while the other is already pricing in a penthouse it hasn’t finished building.