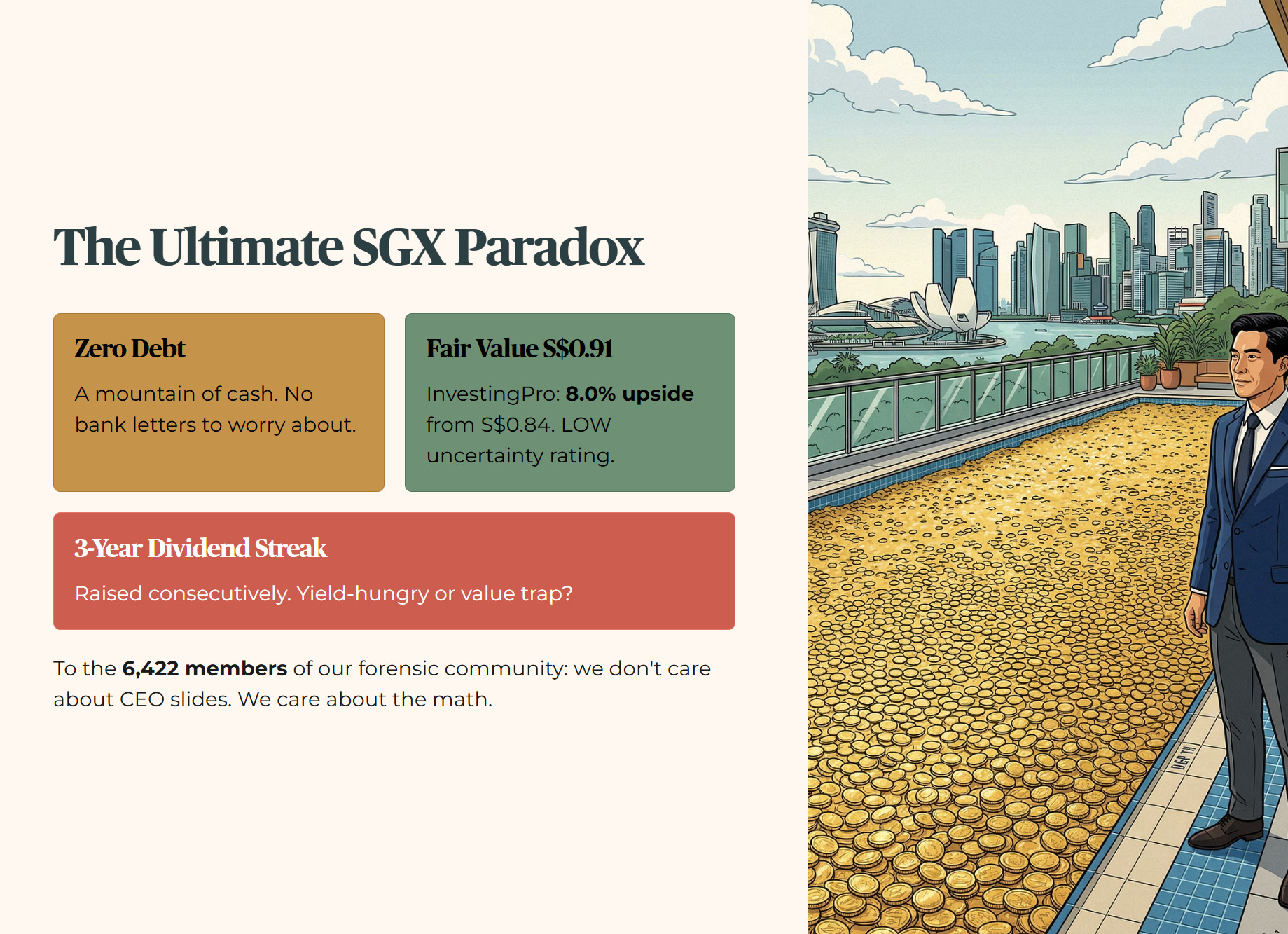

🦎 Valuetronics (SGX: BN2): 3 Reasons for a Forensic Stance and 3 Red Flags (The Honest Audit)

The yield screen shows 6.2%, but the cash pile is worth half the company. How can a business be this rich yet this unloved?

It is the ultimate paradox of the SGX tech sector. You have a company with zero debt and a mountain of cash that could fill an Olympic-sized swimming pool in Toa Payoh. Yet, at S$0.84 , the market treats it like a sunset business waiting for the lights to go out. InvestingPro assigns a LOW uncertainty rating with a Fair Value of S$0.91 —an 8.0% upside. The company has raised its dividend for three consecutive years. Is this a mispriced fortress or a value trap designed to lure in yield-hungry retirees? We are going to look behind the curtain.

To the 6,422 members of our forensic community: you know the drill. We don’t care about the CEO’s “visionary” slides. We care about the math. We are going to weigh the bull case against the bear case with the cold, clinical eye of a Skeptical Arbitrator.

In This Article:

The Financial Snapshot (The Baseline)

Iggy’s Insight

The 3 Good (The Bull Case)

Good 1: The “Cash-Rich” Valuation Floor

Good 2: The ICE Margin Expansion Pivot

Good 3: The “China Plus One” Vietnam Hedge

The 3 Red Flags (The Bear Case)

Red Flag 1: Revenue Atrophy and the “Shrinking Meal” Syndrome

Red Flag 2: The Customer Concentration “Silent Killer”

Red Flag 3: The “Non-Cash” Earnings Trap

InvestingPro Reality Check

The Singaporean Context (The Iggy Angle)

The Weighing Scale (Compliance Strict)

Iggy's Verdict

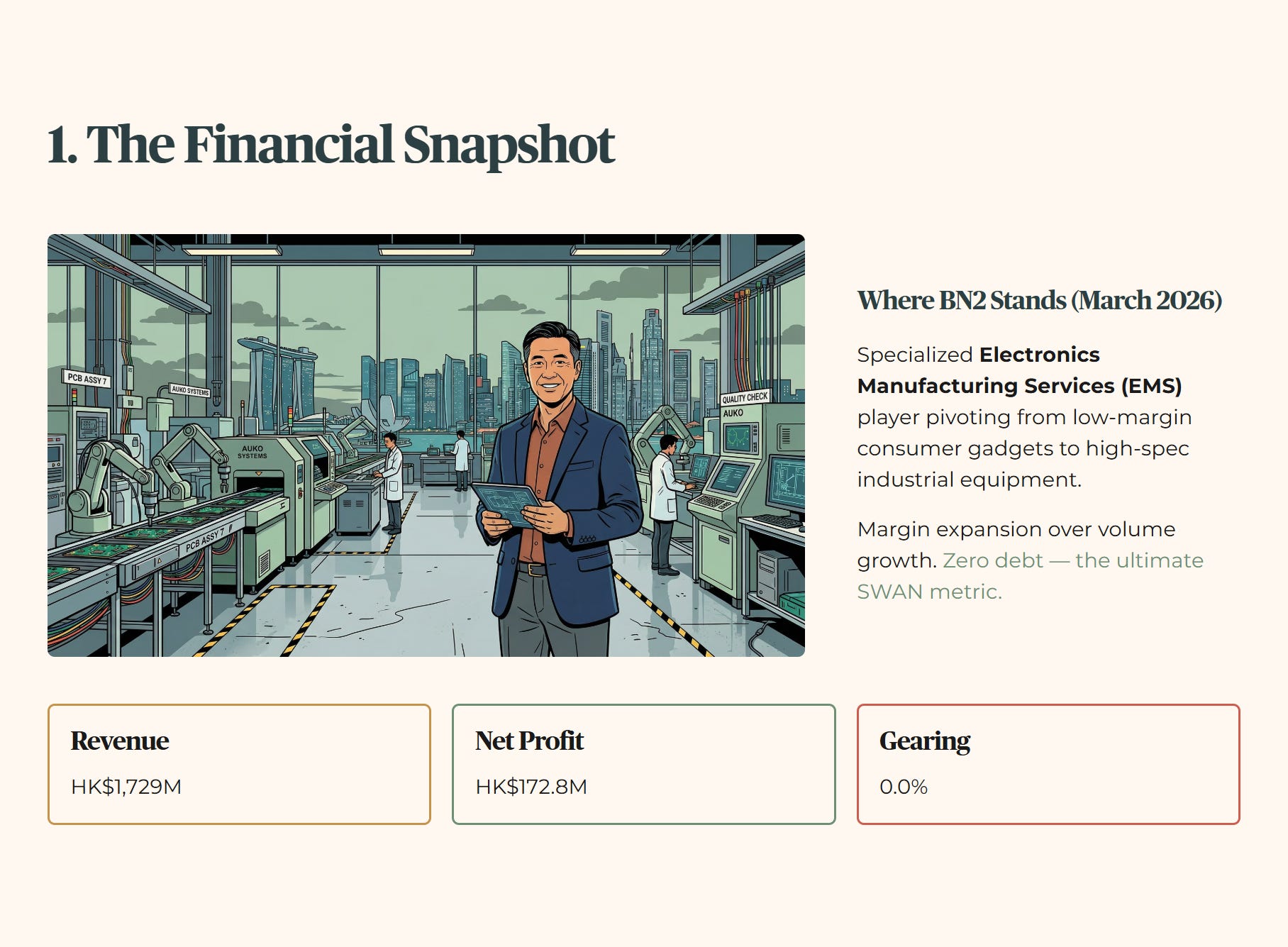

The Bottom Line1. The Financial Snapshot (The Baseline)

Before we dive into the “Good” and “Bad,” we need to establish where Valuetronics (BN2) actually stands. As of March 2026, the company remains a specialized player in the Electronics Manufacturing Services (EMS) space. They have spent the last three years trying to pivot away from low-margin consumer gadgets like electric shavers toward high-spec industrial equipment.

The latest figures show Revenue at HK$1,729 million and a Net Profit of HK$172.8 million . While the top line looks like it is stuck in a stagnant HDB lift, the bottom line has shown surprising resilience. This is a story of margin expansion over volume growth. The company’s gearing is 0.0% —they don’t owe the banks a single cent . InvestingPro confirms the company holds more cash than debt on its balance sheet. For a Singaporean investor managing a benchmark comparison for their portfolio, this zero-debt status is the ultimate sleep-well-at-night (SWAN) metric.

The Double-Entry Rule: The figure that most encourages a forensic stance is the 0.0% Gearing. In a world where interest rates are a permanent headache, being debt-free is like owning your HDB outright without a mortgage—you just don’t worry about the bank’s next letter. However, the most concerning figure is the (HK$8.7M) Free Cash Flow. It doesn’t matter how high your “accounting profit” is if the cash isn’t actually hitting the bank account at the end of the day .

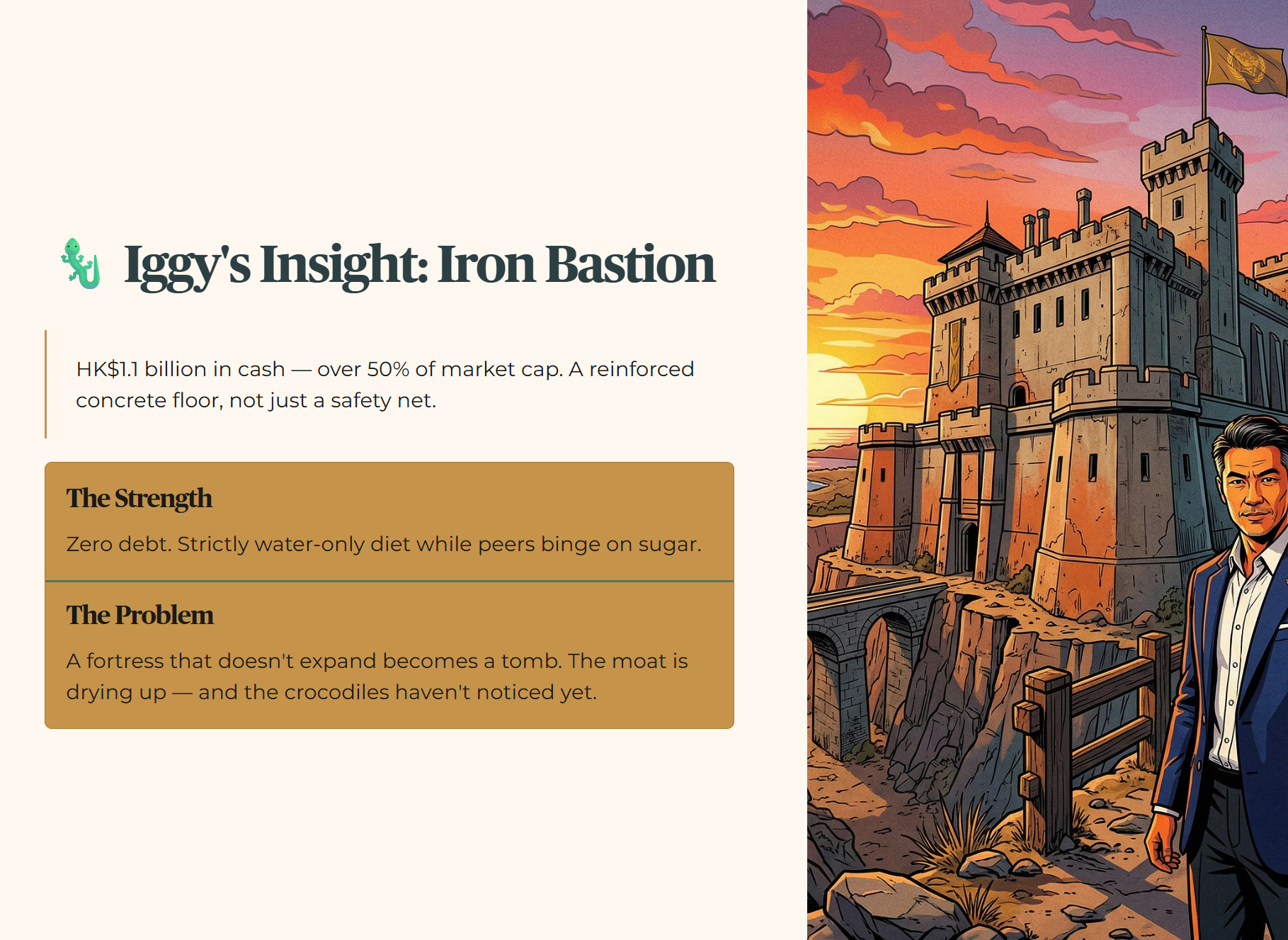

🦎 Iggy’s Insight

Valuetronics is currently an Iron Bastion. Most companies use debt like a sugary drink to get a temporary energy boost, but BN2 is strictly on a water-only diet. They are sitting on HK$1.1 billion in cash, which represents over 50% of their market cap . This isn’t just a safety net; it’s a reinforced concrete floor. But here is the problem: a fortress that doesn’t expand eventually becomes a tomb. The management is sitting on so much cash they could buy a small town, yet they are barely growing the top line. The fortress is standing, but the moat is drying up—and the crocodiles have not noticed yet.

“Now that we’ve established the ‘fortress’ is real, the only question that matters is this: what’s the hard valuation floor—and what specific evidence would flip BN2 from ‘cash-rich bargain’ into ‘cash-rich trap’?”