Venture Corp at S$22.10: Why I’m Not Following This Phillips "BUY" Call

Phillip Securities sees an AI super-cycle. Iggy sees a 4.18% yield on a cyclical hardware play priced for perfection. Both are right — for different investors.

Venture Corporation — Analyst Rating Review

Phillip Securities just stamped a S$22.10 target on Venture Corporation based on an artificial intelligence super-cycle. But when you strip away the tech euphoria, you are paying a premium for a stock yielding well below our absolute minimum hurdle. Institutional analysts play a momentum game. Retirement portfolios cannot afford to buy the hype and ignore the math.

Welcome back to another forensic teardown. I have been watching the chatter around Venture Corporation lately as the market hunts for local proxies to the global semiconductor and AI boom. Every kopitiam uncle with a brokerage account has an opinion on this one right now. Let us put the broker enthusiasm aside and run the actual numbers to see if this narrative holds water for a real-world income portfolio.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

Section 1 — The Analyst’s Case

Section 2 — Iggy’s Forensic Screen

Dimension One — Valuation

Dimension Two — Income

Dimension Three — Execution Risk

Dimension Four — Ownership Signal

Dimension Five — Who Is This For

Section 3 — The Dividend Trajectory

Section 4 — The Forensic Gap

Section 5 — What To Watch Next

Closing — The Forensic Stance

Iggy’s Forensic Disclaimer

Section 1 — The Analyst’s Case

Phillip Securities has upgraded Venture Corporation from an Accumulate to a BUY rating. They lifted their price target significantly to S$22.10, up from their previous S$16.80 mark. The core argument rests on an AI-driven earnings recovery. The broker notes that first-quarter 2026 revenue finally returned to top-line growth after twelve consecutive quarters of year-on-year decline.

This reversal was fuelled specifically by an 11.2 percent surge in demand for AI-related infrastructure products. These include networking interface cards, test and measurement equipment, and semiconductor components feeding into the massive global deployment of data centres. The broker is applying a 25x forward price-to-earnings multiple — meaning they are willing to pay twenty-five times the company’s expected annual earnings — to justify this higher valuation. They argue that Venture should move away from historical valuations and trade closer to its US-listed peers, which currently command a 33x forward multiple. The house also points to a fortress balance sheet, highlighting that Venture holds over S$1 billion in net cash. This effectively insulates it from the elevated rate environment.

THE LOAD-BEARING ASSUMPTION: Venture Corporation’s recent top-line bump is not a temporary cyclical blip. It is the start of a multi-year, high-margin growth super-cycle driven by structural AI data centre demand that justifies a permanent valuation re-rating.

That is a bold thesis. Let us see if the numbers agree.

Section 2 — Iggy’s Forensic Screen

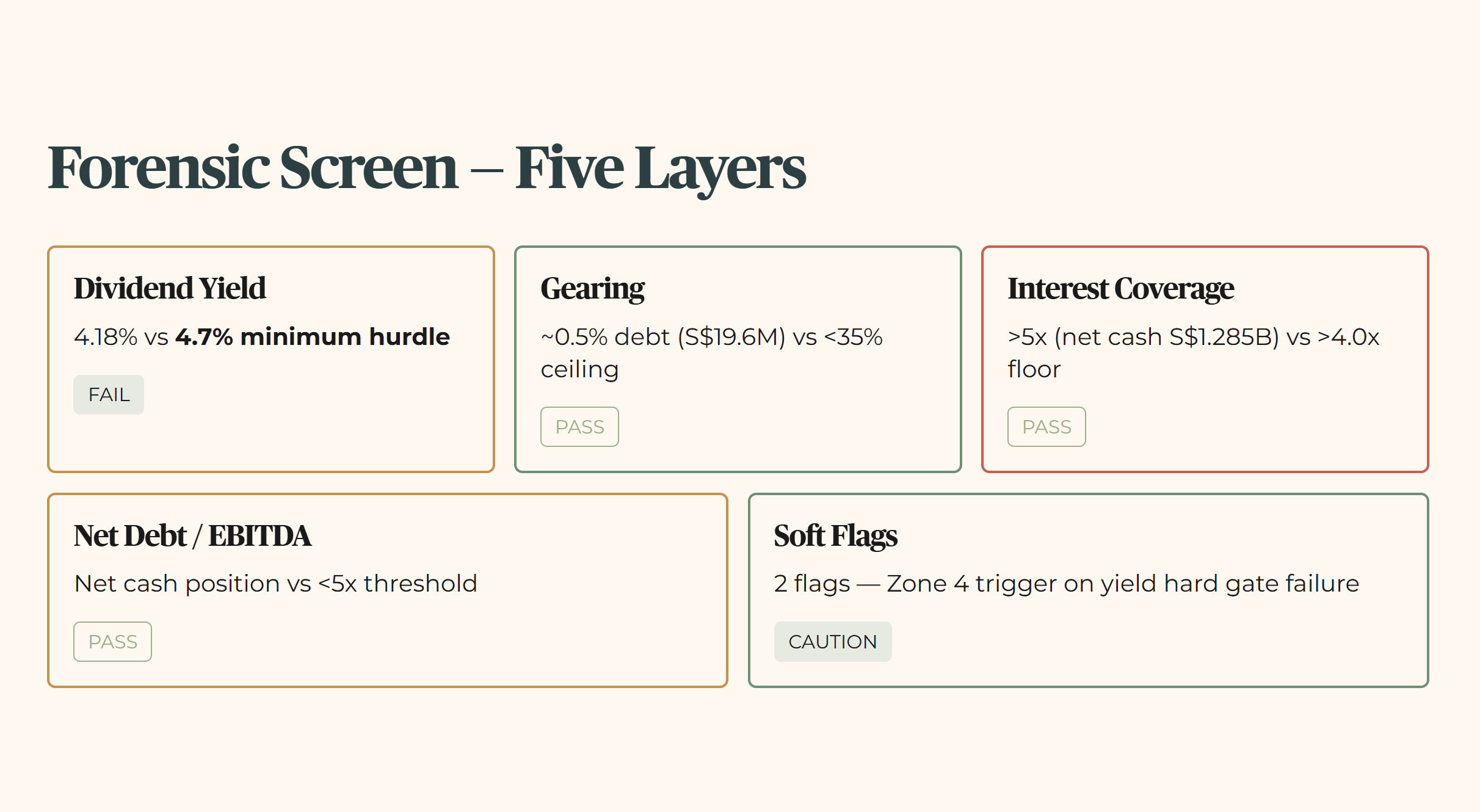

To test that assumption, we apply the five-layer forensic audit — the framework I use to determine whether any stock qualifies for a retirement income portfolio. We strip away the narrative and look strictly at the verified data.

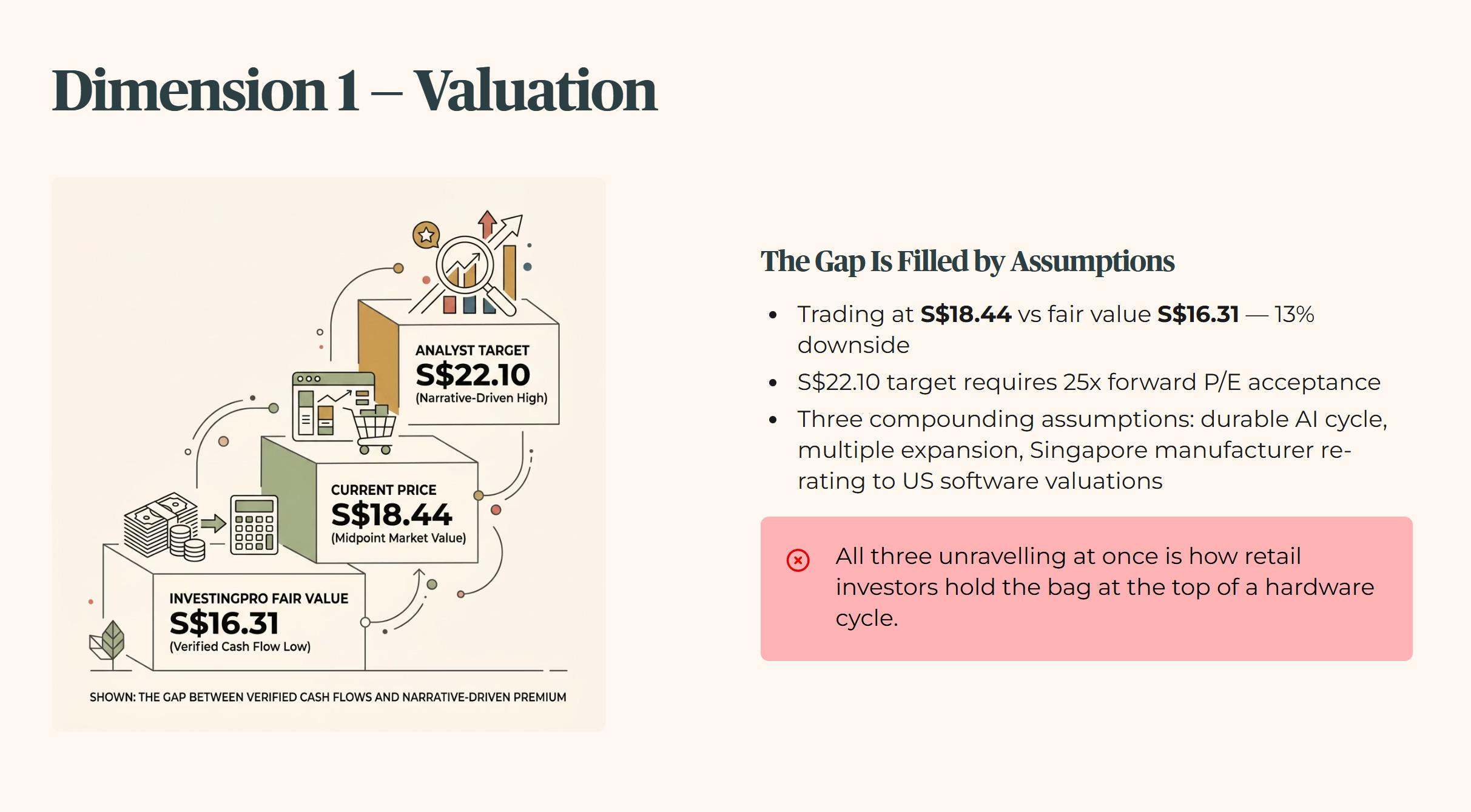

Dimension One — Valuation

The stock is trading at S$18.44 against an InvestingPro average fair value of S$16.31 — a gap of S$2.13, or roughly 13 percent of downside from where you are buying today. The analyst’s S$22.10 target requires the market to accept a 25x forward earnings multiple. That gap between S$16.31 and S$22.10 is not filled by verified cash flows. It is filled by three compounding assumptions: that an AI super-cycle is durable, that multiple expansion is justified, and that a Singapore contract manufacturer deserves to re-rate toward US software valuations. Each of those assumptions can unravel independently. All three unravelling at once is how retail investors end up holding the bag at the top of a hardware cycle.

Dimension Two — Income

This is where the retirement case runs into a wall. Venture is paying a dividend yield of 4.18 percent against our 4.7 percent minimum yield hurdle — a shortfall of fifty-two basis points before you account for any equity risk. Your CPF Special Account guarantees 4.0 percent with full capital protection. Accepting 4.18 percent from a cyclical semiconductor manufacturer means you are earning just eighteen basis points above risk-free for absorbing the full volatility of a hardware cycle. That is not a risk premium. That is a rounding error dressed up as an income play.

The payout ratio makes it worse. Venture is distributing S$0.75 per share against earnings of S$0.79 — a payout ratio of 101 percent. The dividend is not being funded by earnings growth. It is being sustained by a billion-dollar cash reserve accumulated in better years. Think of it like a hawker uncle who built up his savings during the good decades and is now dipping into the ang pow money to keep the stall running. Admirable discipline — but not a foundation you want to build a retirement portfolio on.

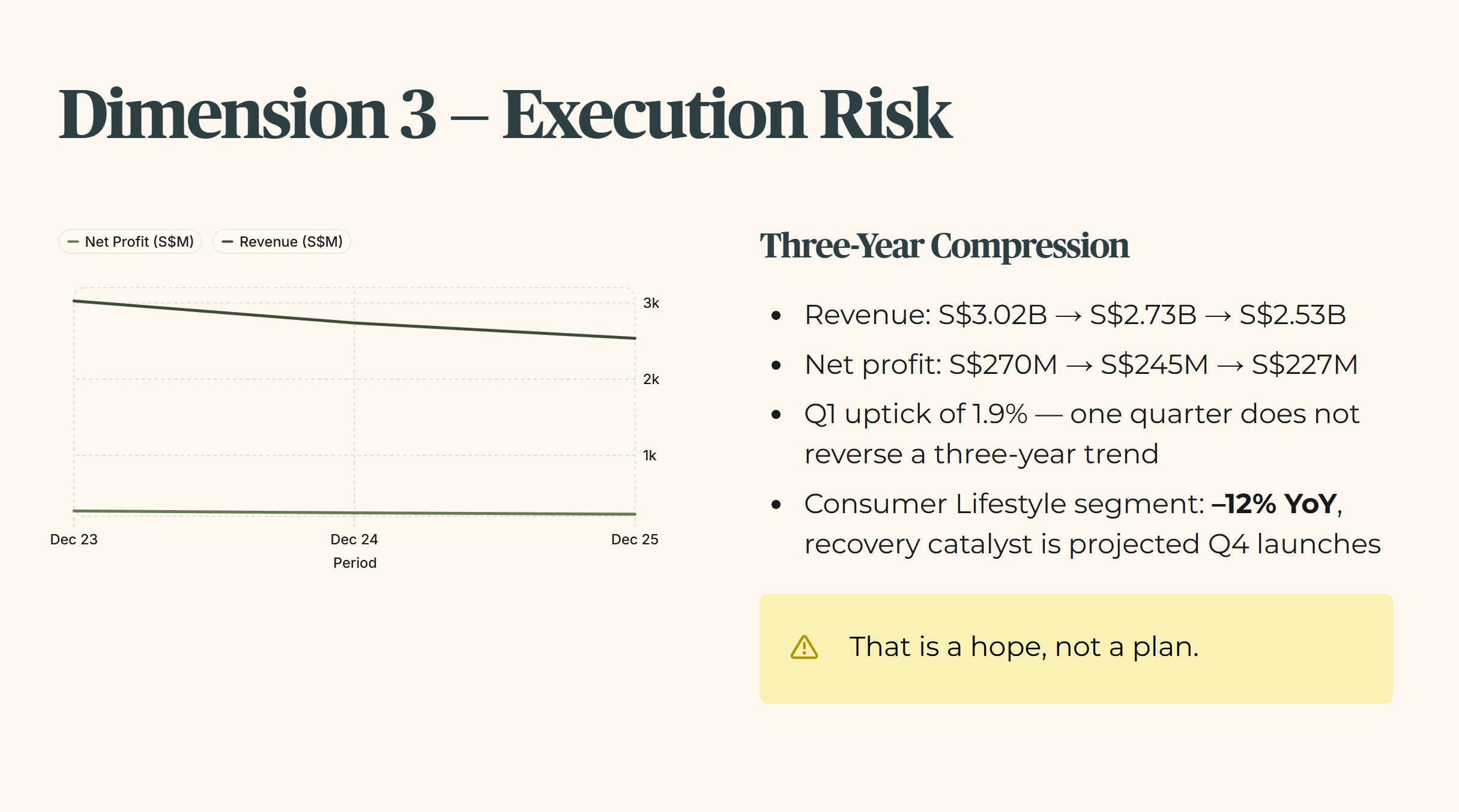

Dimension Three — Execution Risk

Over the last three fiscal periods, the revenue trend tells a story of structural compression rather than temporary softness. It dropped from S$3.02 billion in December 2023 to S$2.73 billion in 2024, and further to S$2.53 billion by the end of 2025. Net profit followed the same staircase down: from S$270 million to S$245 million to S$227 million. The recent quarter showed a 1.9 percent year-on-year uptick — encouraging, but one quarter does not reverse a three-year trend. Two consecutive periods of revenue compression is a confirmed soft flag under our framework.

The company is also carrying a Consumer Lifestyle segment in active decline — down 12 percent year-on-year — with projected fourth-quarter product launches as the named recovery catalyst. That is a hope, not a plan. If we stress-test with a 10 percent macro shift — a strengthening Singapore Dollar eating into export margins, or a pause in AI infrastructure capital expenditure — the 4.18 percent yield faces immediate downward pressure. Venture’s fortunes are tied tightly to global enterprise hardware budgets staying robust across multiple cycles simultaneously.

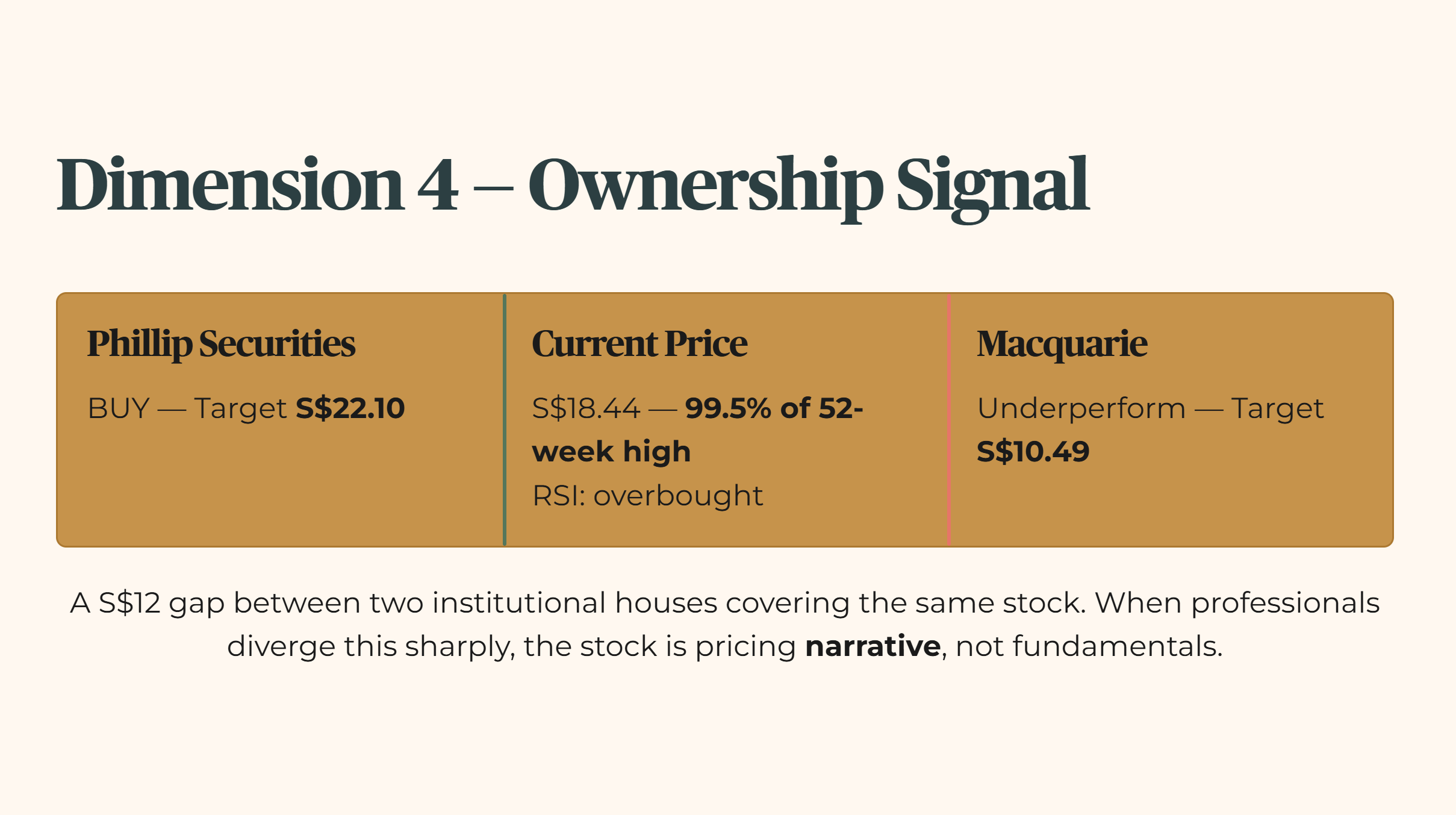

Dimension Four — Ownership Signal

The stock is trading at 99.5 percent of its 52-week high at S$18.44 against a range of S$10.92 to S$18.75. The RSI flags overbought conditions. More telling is the analyst divergence: Phillip Securities has a BUY at S$22.10 while Macquarie is sitting at Underperform with a S$10.49 target — a gap of nearly S$12 between two institutional houses covering the same stock. When professionals are that far apart, the stock is not pricing fundamentals. It is pricing narrative. Retail investors who absorb that narrative divergence carry the full downside when the story shifts.

Dimension Five — Who Is This For

Here is the honest answer. For a growth investor with a long runway and tolerance for cyclical drawdowns, the AI infrastructure thesis is coherent. If the data centre build-out sustains multi-year momentum and Venture captures a disproportionate share of Asian contract manufacturing, a 25x multiple may prove conservative in hindsight. That is a legitimate institutional bet and it deserves to be stated fairly.

But retirement income investing operates under a completely different mandate. A 55-year-old Singaporean structuring a portfolio for drawdown needs every allocation to carry its weight in verified, sustainable cash — not hope, not narrative, not a billion-dollar piggy bank that is already being drawn down. These are two different investor profiles with two different forensic requirements. This channel exists for the second.

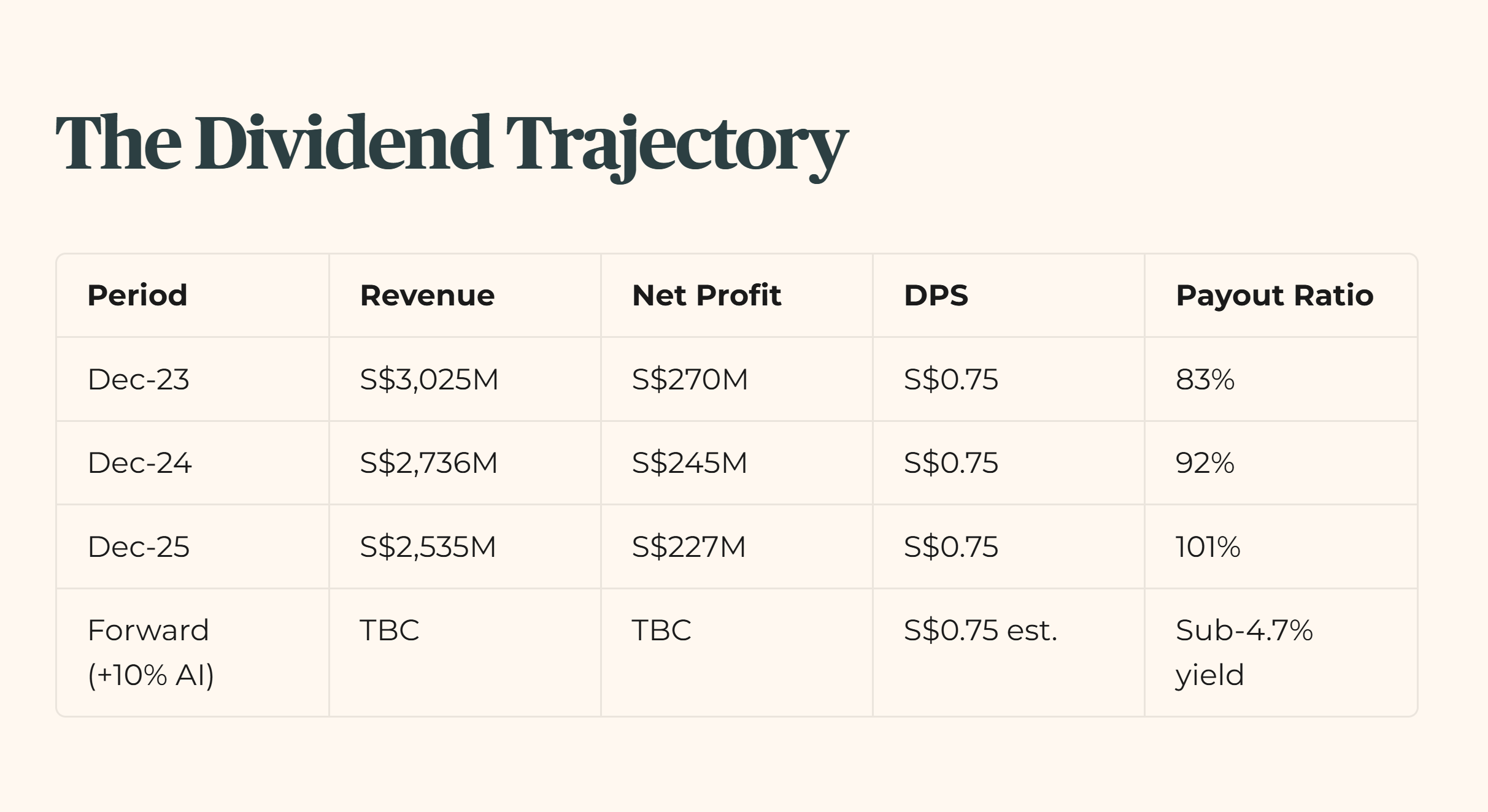

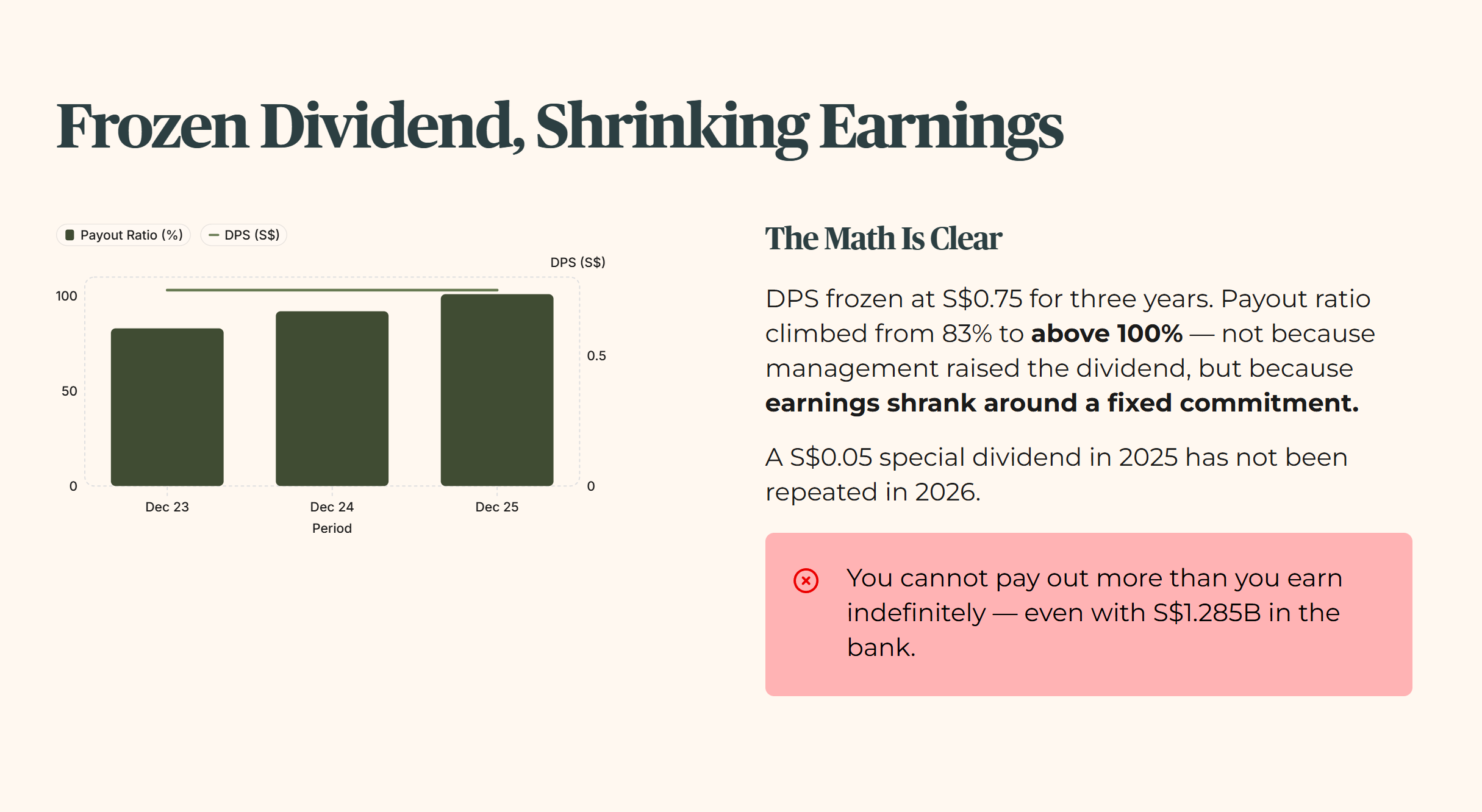

Section 3 — The Dividend Trajectory

The dividend per share has been frozen at S$0.75 across three consecutive years while revenue and profit have compressed steadily beneath it. The payout ratio has climbed from roughly 83 percent to above 100 percent as a result — not because management raised the dividend, but because earnings shrank around a fixed commitment. The 2025 interim cycle did include a modest S$0.05 special dividend, which has not been repeated in 2026 so far. The company can sustain this for now given the net cash fortress, but the mathematical ceiling is real. You cannot pay out more than you earn indefinitely, even with S$1.285 billion in the bank.

Section 4 — The Forensic Gap

The gap between these two verdicts is not about who is right and who is wrong. It is about what the stock is actually being asked to do in your portfolio. The institution is pricing in an extended growth runway and willing to accept 4.18 percent today because they expect the price to run hard toward S$22.10. That logic works if you are playing for capital gains.

For a retail investor relying on cash flow, accepting a yield below our 4.7 percent minimum means taking on full equity volatility for a return that barely beats the risk-free CPF Special Account rate. You are paying a growth premium and receiving an income consolation prize. The analyst is valuing Venture like a Silicon Valley software darling. The reality is a contract manufacturer operating in a highly cyclical hardware space, where multiple expansion is the first thing the market takes back when sentiment turns.

Do not subsidise institutional exit liquidity by buying the narrative at the top of a hardware cycle.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Section 5 — What To Watch Next

Three forensic triggers to track if you are holding this stock or monitoring the AI thesis:

July 2026 Earnings Momentum: Watch the top-line revenue figure carefully. Does the 1.9 percent first-quarter uptick hold and accelerate, or was it a seasonal blip in a multi-year compression story? One quarter of growth after twelve of decline is a green shoot, not a harvest.

Consumer Lifestyle Segment Recovery: The 12 percent year-on-year decline in this division is the quiet drag behind the AI excitement. Monitor whether the projected fourth-quarter product launches actually move the needle — or whether management quietly stops talking about it by the next earnings call.

Special Dividend Signal: The 2025 cycle included a S$0.05 special payout that has not been repeated in 2026. Watch whether management reinstates it as a signal of earnings confidence, or whether the regular S$0.75 itself comes under pressure as the cash pile is drawn down to bridge the gap between what the company earns and what it pays out.

The payout ratio and yield math above clear our first forensic hurdle — but the next section’s dividend trajectory, and the gap between institutional targets and CPF-backed cashflow, is where the retirement verdict actually lands.