Weekly Market Movers 29 Nov 2025: The "Easy 4%" is Dead. Here’s Where the Money Went.

T-Bill yields just crashed to 1.39%. We analyze why capital is flooding into Frasers Logistics and Jardine—and leaving cash behind.

The STI just smashed a record high while T-Bill yields crashed to 1.39%. Here is the deep-dive analytics on why the rally in Frasers Logistics and Jardine isn’t a fluke—and why I’m looking at the laggards.

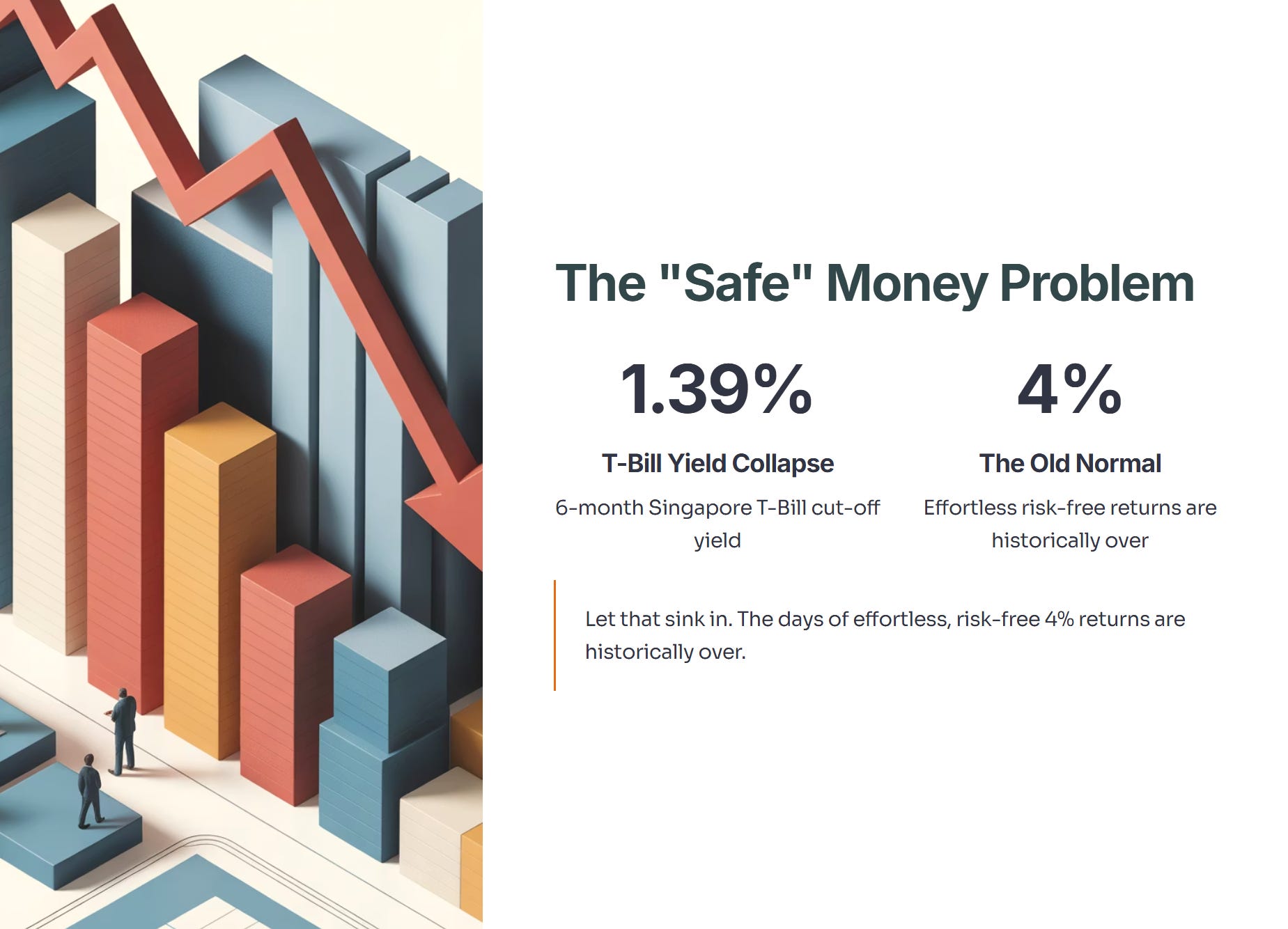

The “Safe” Money Problem

If you tried to bid for a T-Bill this week, you likely faced a rude awakening. The cut-off yield for the latest 6-month Singapore T-Bill has collapsed to 1.39%.

Let that sink in. The days of effortless, risk-free 4% returns are historically over.

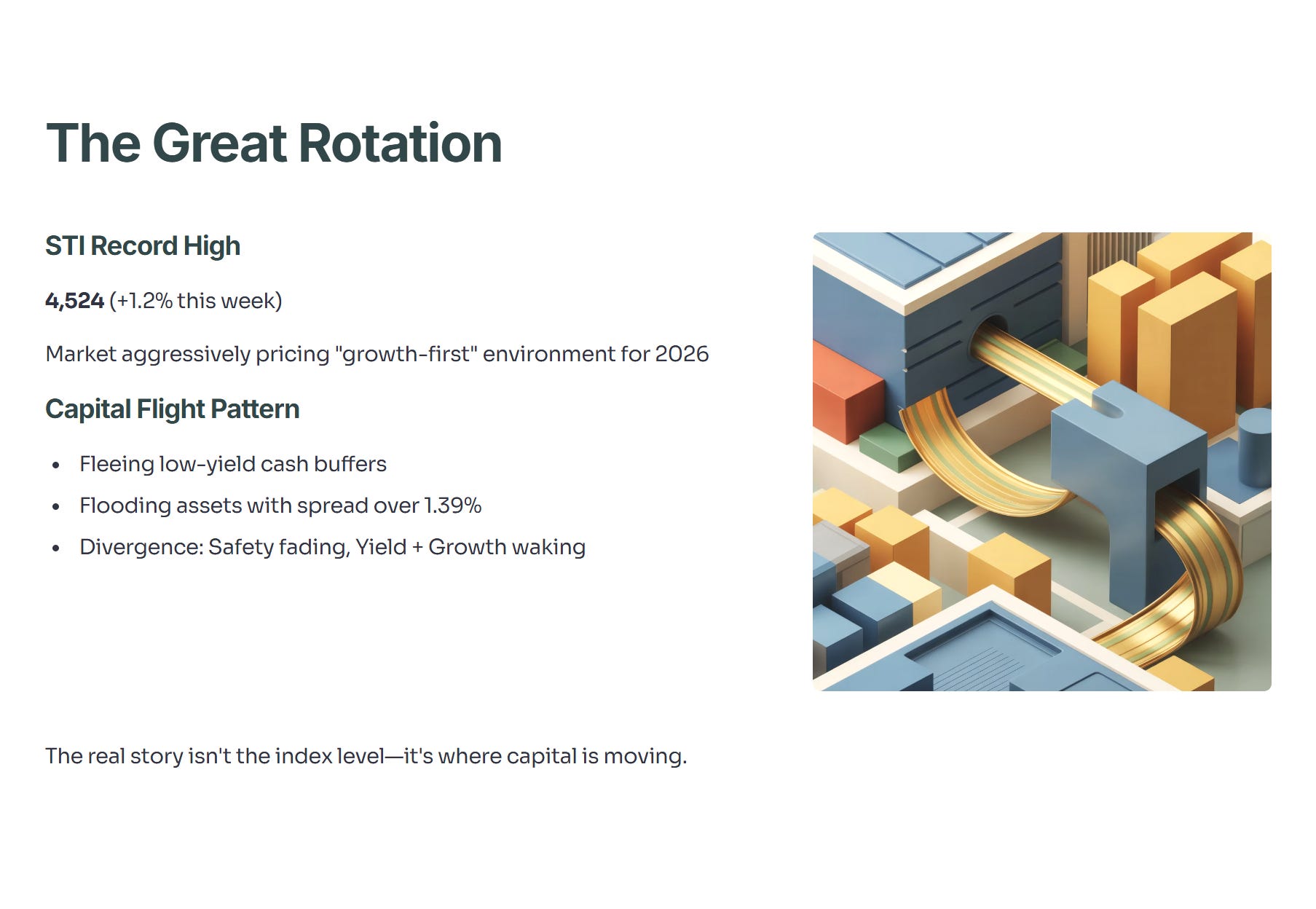

While the headlines are celebrating the Straits Times Index (STI) hitting a record high of 4,524 (+1.2% this week), the real story isn’t the index level. It’s the Great Rotation. The market is aggressively pricing in a “growth-first” environment for 2026. Capital is fleeing low-yield cash buffers and flooding into assets that offer a spread over that meager 1.39% risk-free rate.

We are seeing a divergence: The “Safety Trade” is fading, and the “Yield + Growth Trade” is waking up.

In This Article:

• The Data: Winners, Losers, and The Yield Gap

• Top Gainers (Week Ending 29 Nov 2025)

• Deep Dive: Iggy’s Stock-by-Stock Analytics

• 1. Frasers Logistics & Commercial Trust (FLCT)

• 2. Jardine Matheson (J36) & Jardine Cycle & Carriage (C07)

• 3. Keppel Ltd (BN4)

• The Laggards: Value Trap or Deep Value?

• 1. UOL Group (U14) – The “50-Cent Dollar”

• 2. Lendlease Global Commercial REIT (JYEU) – The “Income Vacuum”

• Conclusion: The New Rules of EngagementThe Data: Winners, Losers, and The Yield Gap

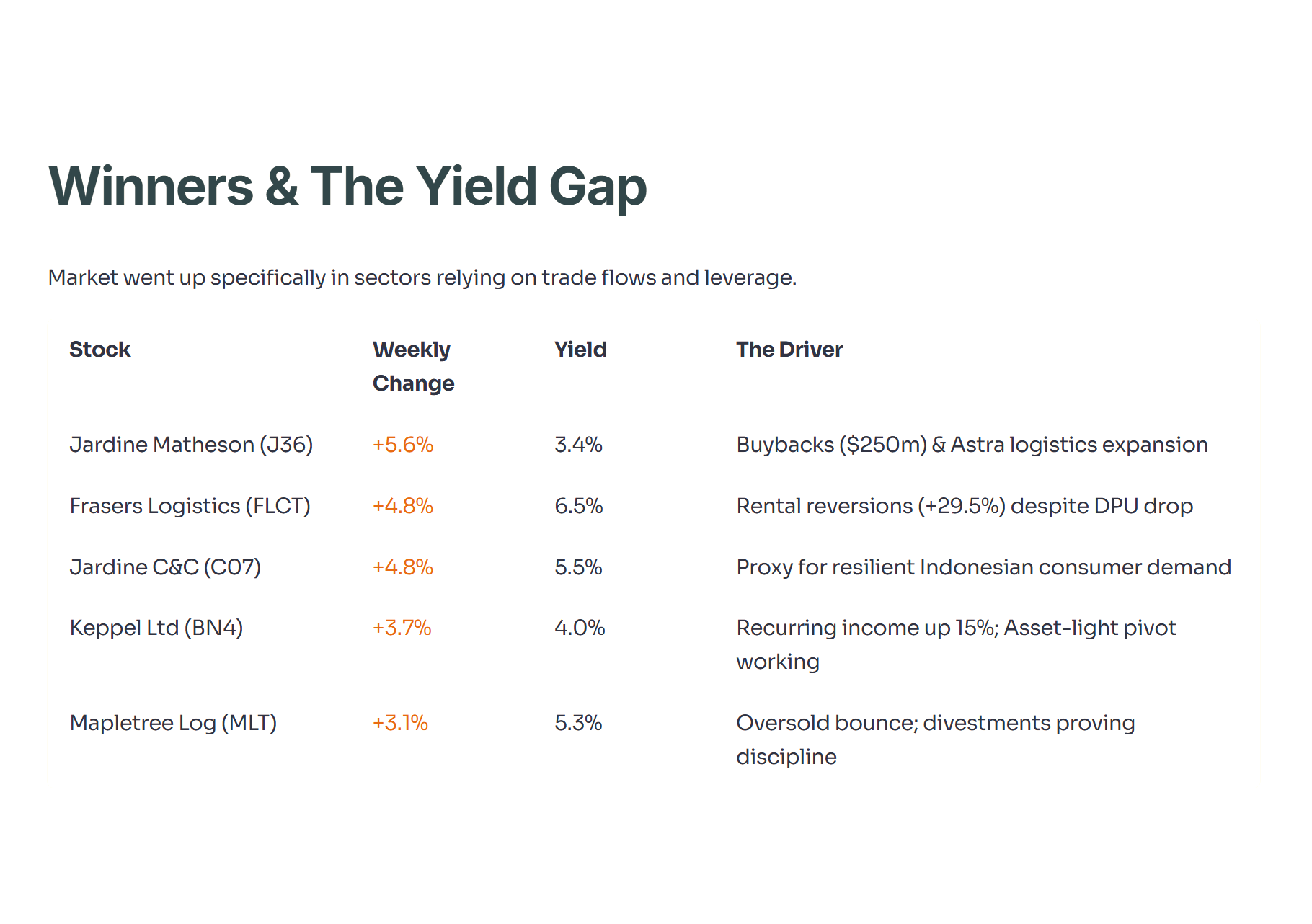

The market didn’t just go “up.” It went up specifically in sectors that rely on trade flows and leverage. Here is the breakdown of the week’s significant movers based on SGX data.

Top Gainers (Week Ending 29 Nov 2025)

Deep Dive: Iggy’s Stock-by-Stock Analytics

You asked for the details—here is the raw analysis on the key movers.

1. Frasers Logistics & Commercial Trust (FLCT)

The Data: Revenue +5.6% (FY25), but DPU -12.5% due to higher finance costs.

The Narrative: This is the classic “Look Forward, Not Backward” trade. Retail investors saw the DPU drop and got scared. Institutional investors saw the +39.6% rental reversion in their logistics portfolio and the 99.7% occupancy. They know that as interest rates fall in 2026, FLCT’s finance costs will stabilize, and that massive rental growth will flow straight to the bottom line.

Key Metric: Aggregate Leverage (35.7%). This is low for a REIT, giving them massive debt headroom to acquire assets while competitors are stuck.

Iggy’s Insight:

This is my highest conviction pick for the “Rotation Trade.” The market is realizing that FLCT trading at ~1.1x P/B with a 6.5% yield is a steal compared to a 1.39% T-Bill. I am buying the “Logistics” story and tolerating the “Commercial” weakness. The 4.8% jump this week is just the start of the re-rating.

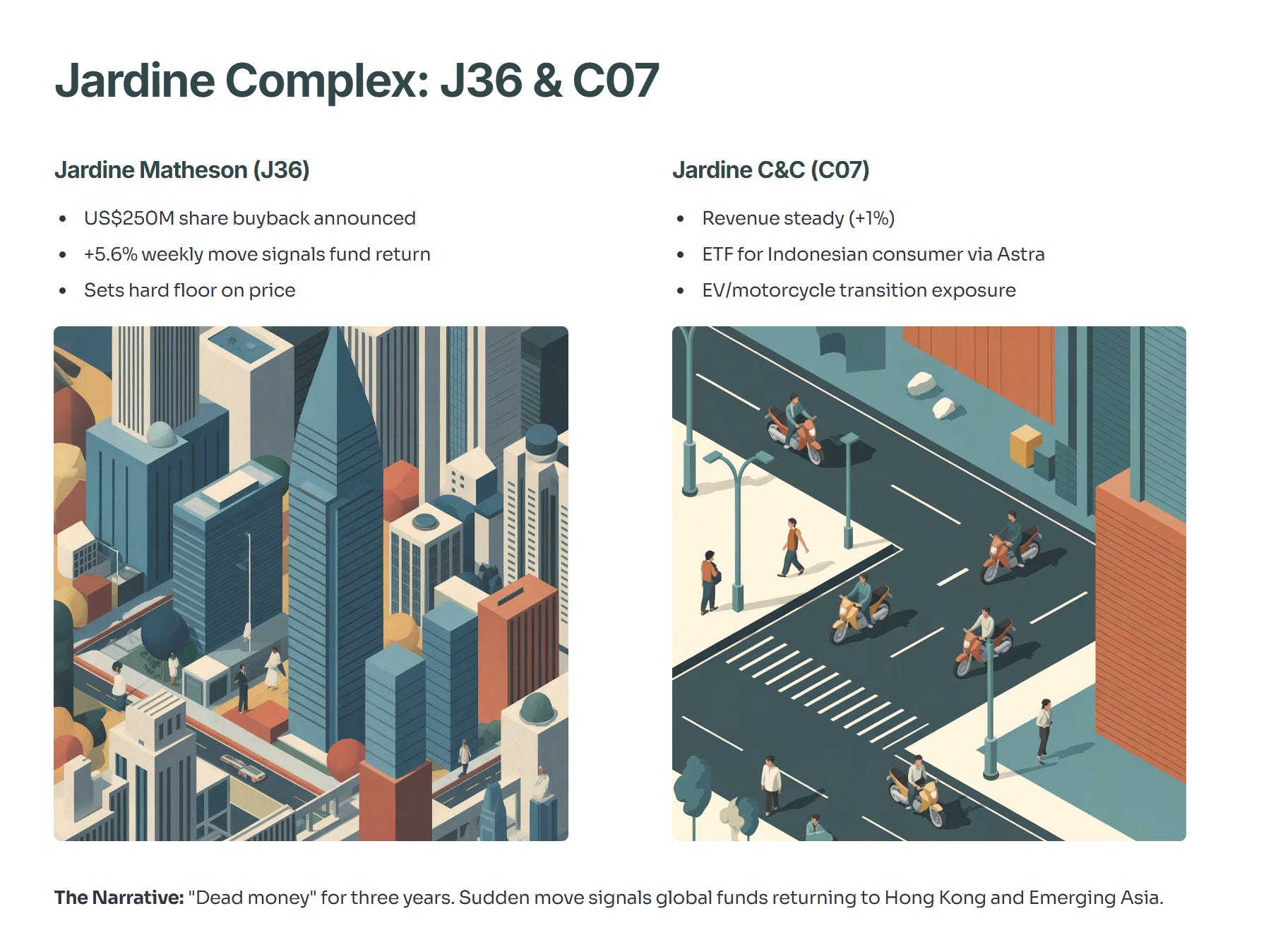

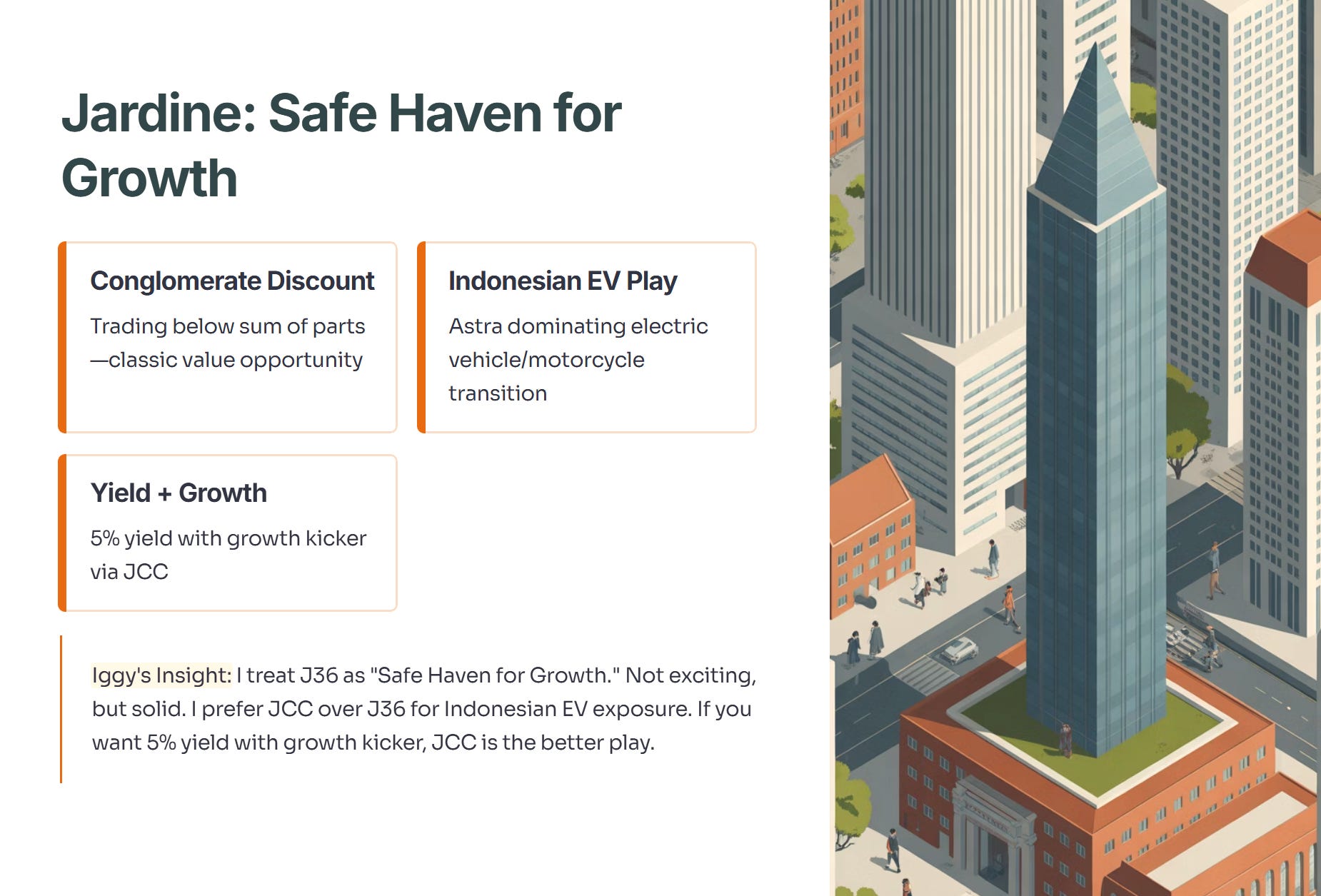

2. Jardine Matheson (J36) & Jardine Cycle & Carriage (C07)

The Data: J36 announced a US$250M share buyback; JCC revenue held steady (+1%) despite a 23% drop in net profit due to non-cash items.

The Narrative: The Jardine complex has been “dead money” for three years. The sudden +5.6% move is a signal that global funds are returning to Hong Kong and Emerging Asia. JCC is effectively an ETF for the Indonesian consumer (via Astra). When the USD weakens (as it is doing now), Emerging Market assets like JCC outperform.

Key Metric: Share Buyback Volume. J36 buying back shares at these valuations sets a hard floor on the price.

Iggy’s Insight:

I treat J36 as a “Safe Haven for Growth.” It’s not exciting, but it’s a conglomerate trading at a discount to its parts. I prefer JCC over J36 specifically because I want exposure to the Indonesian electric vehicle/motorcycle transition, which Astra is dominating. If you want a 5% yield with growth kicker, JCC is the better play.

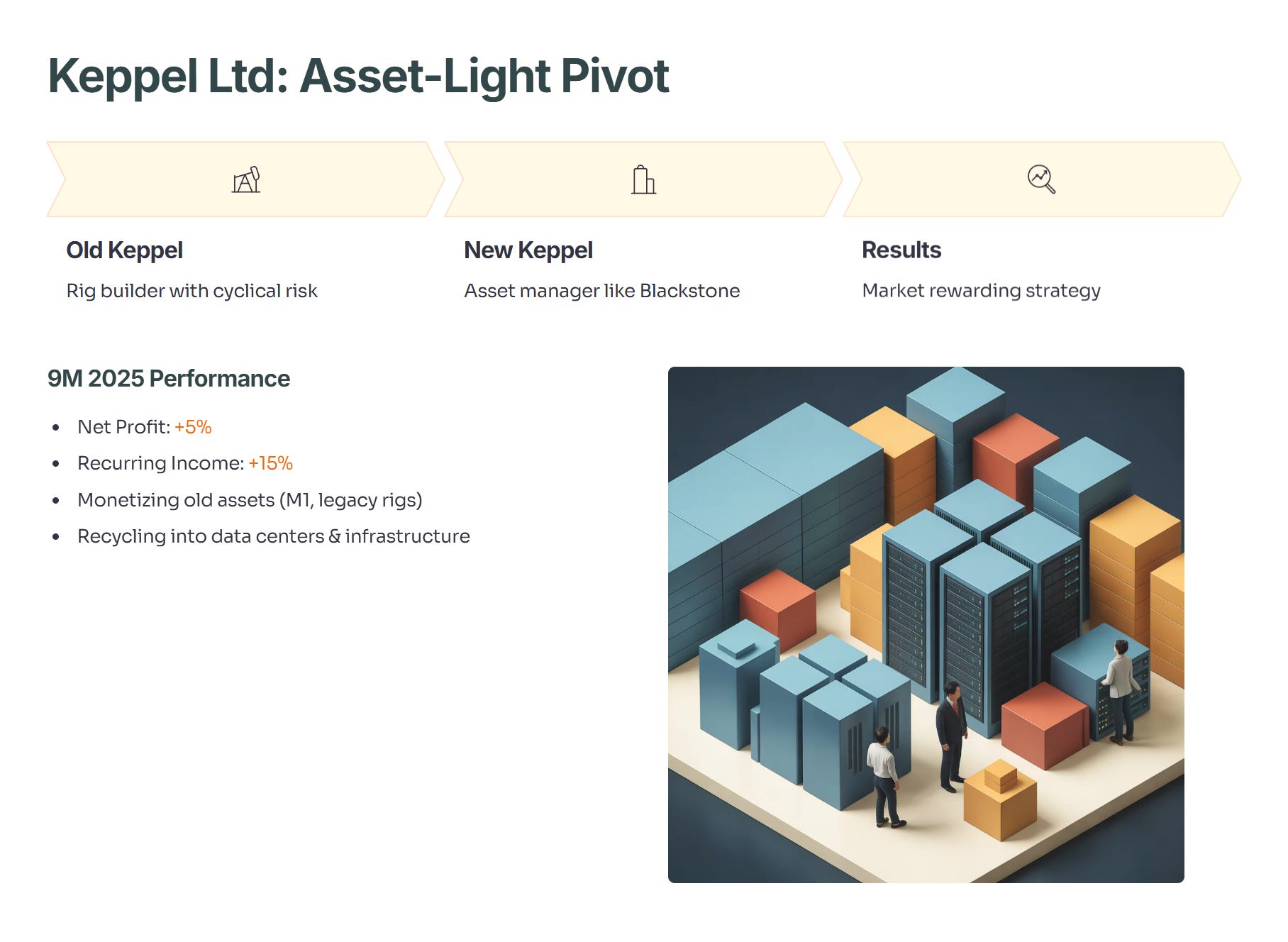

3. Keppel Ltd (BN4)

The Data: 9M 2025 Net Profit up >5%; Recurring Income up 15%.

The Narrative: Keppel is no longer a rig builder; it is an asset manager like Blackstone. The market is finally rewarding them for this “Asset-Light” strategy. They are monetizing old assets (selling M1, legacy rigs) and recycling that cash into data centers and infrastructure.

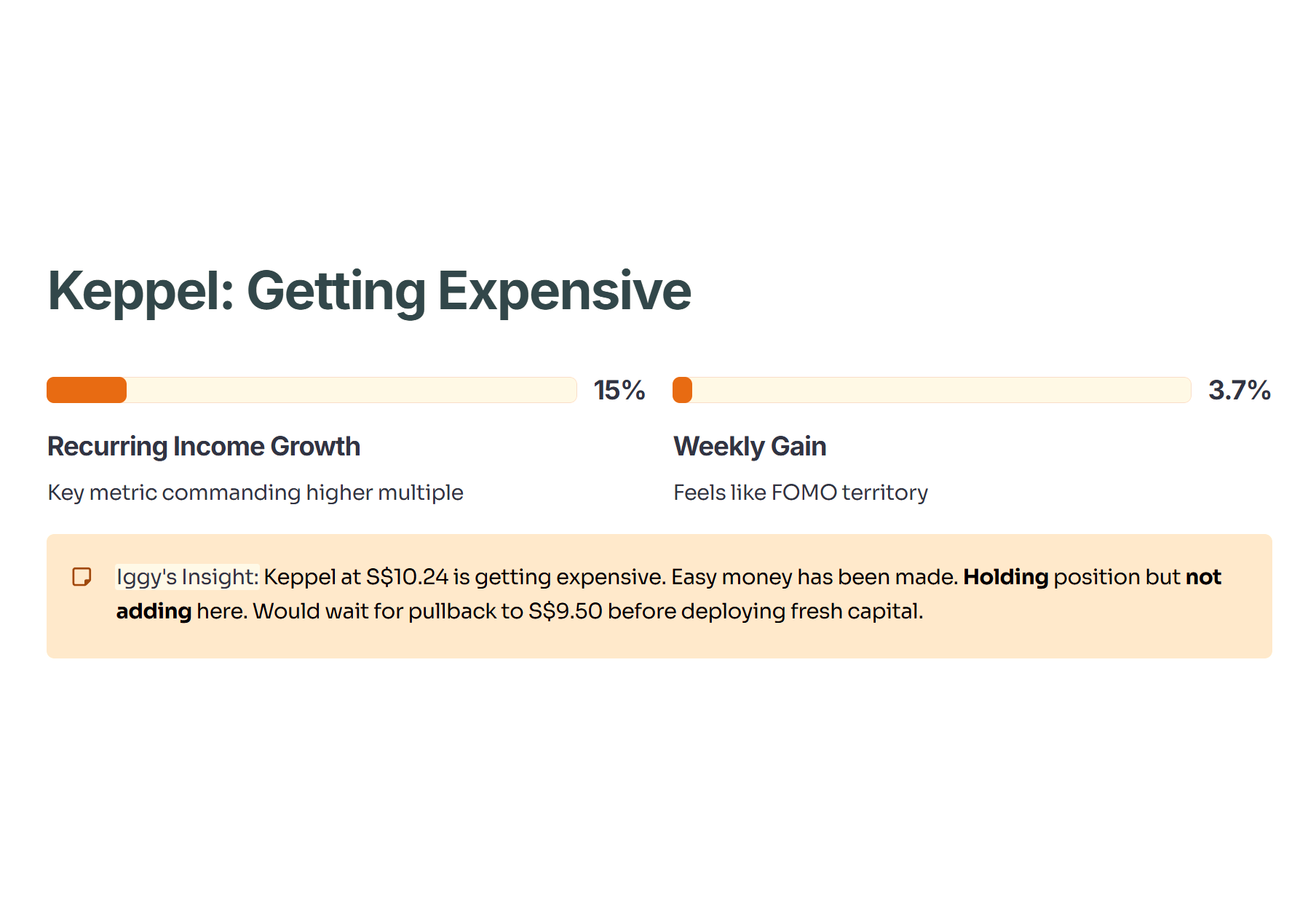

Key Metric: Recurring Income Growth. As long as this stays double-digit (+15%), the stock commands a higher multiple.

Iggy’s Insight:

Keppel at S$10.24 is getting expensive. The easy money has been made. I am **holding** my position but I am **not adding** here. The 3.7% gain this week feels like FOMO (Fear Of Missing Out). I would wait for a pullback to S$9.50 before deploying fresh capital.

The Laggards: Value Trap or Deep Value?

This is where the easy money has already been made in the Gainers. But the real “Alpha” for December lies in the stocks that the market left behind this week.

Is the dip in UOL Group a buying opportunity or a warning sign? Is Lendlease REIT cheap, or is it a value trap due to its Milan exposure?

Below, I break down the 2 Laggards I am watching closely, including one I am aggressively buying at these levels.

Subscribe to read the full Laggard Analysis and my December Strategy Verdict.