What October’s SGX Earnings Could Mean for Your Portfolio: REITs, Blue Chips, and Your Next Move

T-bill yields have collapsed to 1.35%. We analyze if the 5%+ yields from REITs and deep value from blue chips are worth the risk.

Singapore investors face a rare moment. T-bill yields have dropped to 1.35%. REITs are reporting earnings all month. And some blue chips are trading at massive discounts. The question is simple: What should you do with your money right now?

October brings a wave of Singapore REIT results that could reshape where money flows next. Frasers Centrepoint Trust reports its Northpoint City consolidation numbers. Keppel DC REIT shows if AI demand is real or hype. And CapitaLand’s giants reveal whether retail and offices can still deliver. At the same time, names like Hongkong Land are trading at 0.45 times book value. With T-bills paying less than 1.5%, the math has changed. This article breaks down what the October earnings season means for your CPF, SRS, and cash allocations, with clear strategies to limit downside while capturing upside.

In This Article:

• Singapore’s Energy Reality Check

• The Bigger Picture: The 6 GW Target

• The Sarawak Hydropower Deal

• Sembcorp Industries: The Stock to Watch

• Is Sembcorp A Buy Right Now?

• Investment Recommendation

• Beyond Sembcorp: Other Ways To Play

• Major Risks That Could Derail The Plan

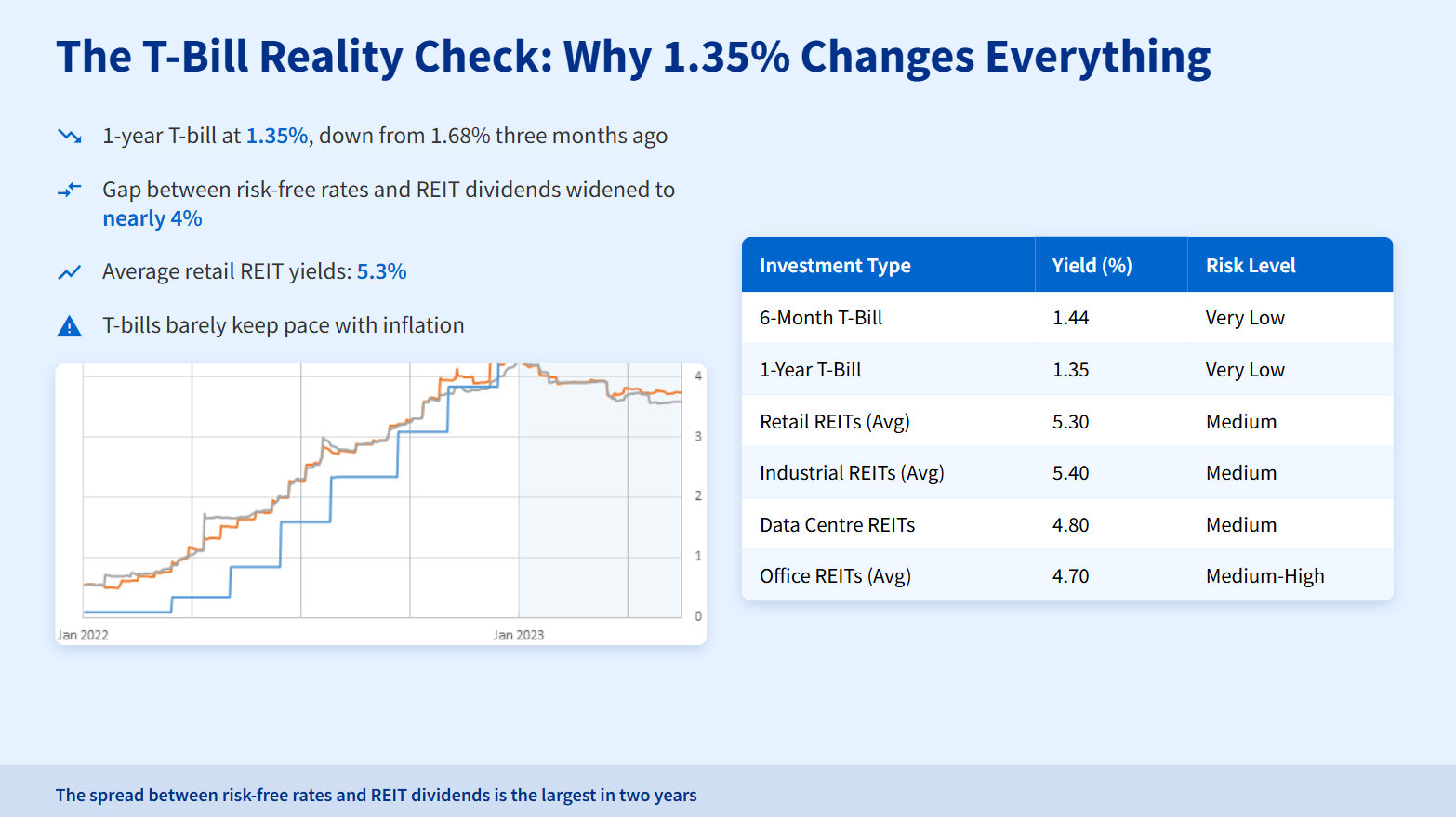

• Final TakeawaysThe T-Bill Reality Check: Why 1.35% Changes Everything

The latest 1-year T-bill auction closed at 1.35%. That is down from 1.68% just three months ago. The 6-month T-bill sits at 1.44%. Fixed deposits top out at 1.60% for 12 months. Singapore Savings Bonds offer 1.56% for the first year.

These numbers matter because they set your baseline. If you park cash in T-bills or fixed deposits, you lock in returns below 2%. That barely keeps pace with inflation. Meanwhile, the average retail REIT in Singapore yields 5.3%. Industrial REITs yield 5.4%. Even data centre REITs, which trade at premium valuations, yield around 4.8%.

The gap between risk-free rates and REIT dividends has widened to nearly 4%. That spread is the largest in two years. It creates pressure. Investors chasing income will look at REITs. But REITs come with risks. Occupancy can drop. Rental reversions can turn negative. Debt costs matter. And capital values fluctuate.

Table: The Yield Gap: Why Investors Are Being Pushed Into REITs

This table shows the trade-off. T-bills are safe but yield little. REITs yield more but carry volatility. The October earnings will show whether those REIT dividends are sustainable.

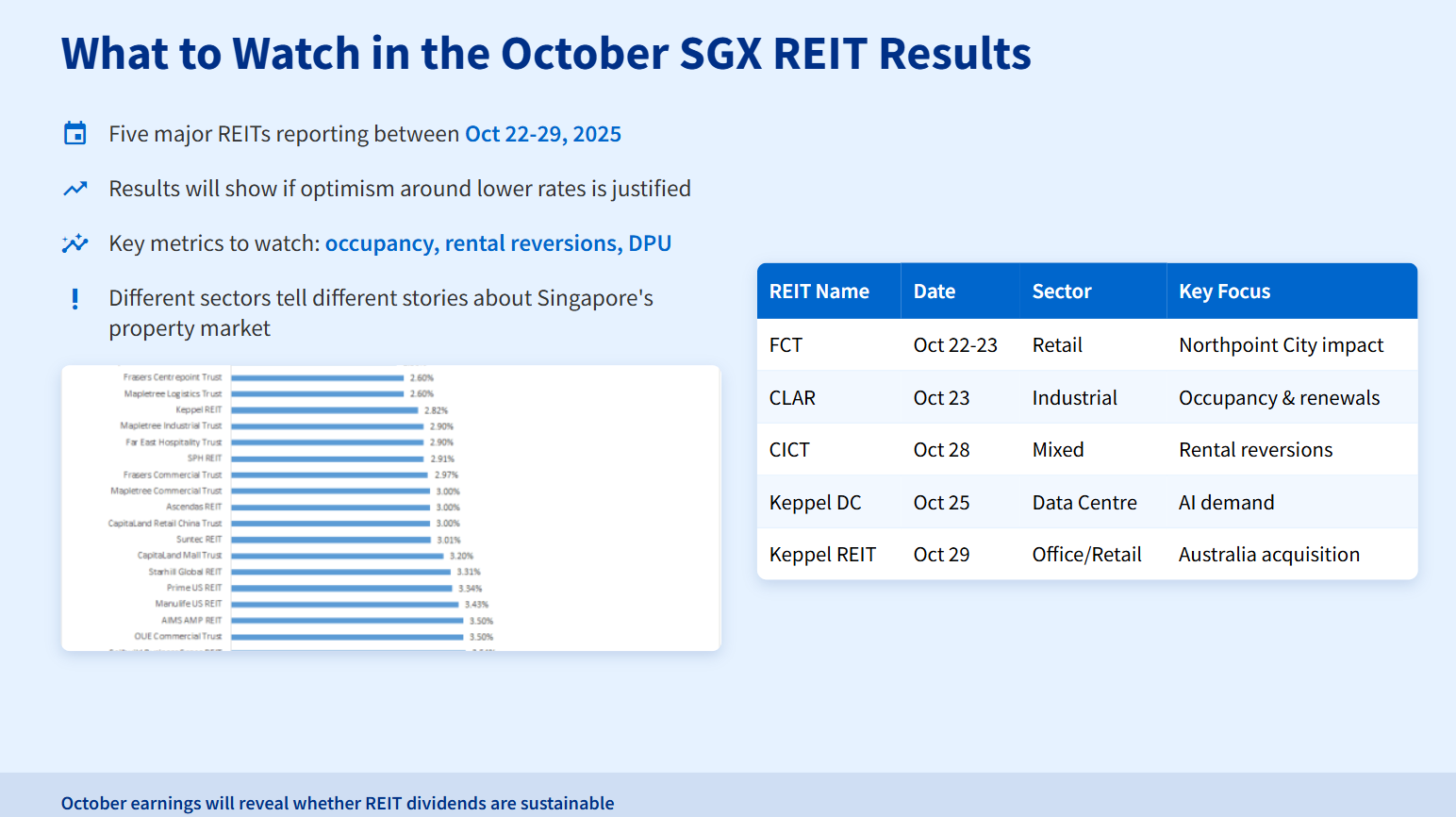

What to Watch in the October SGX REIT Results

October is packed with REIT earnings. Five major names report between October 22 and October 29. Each one tells a different story about Singapore’s property market.

Table: Your REIT Earnings Calendar: Key Dates to Watch

Mark these dates. The results will show whether the optimism around lower interest rates is justified.

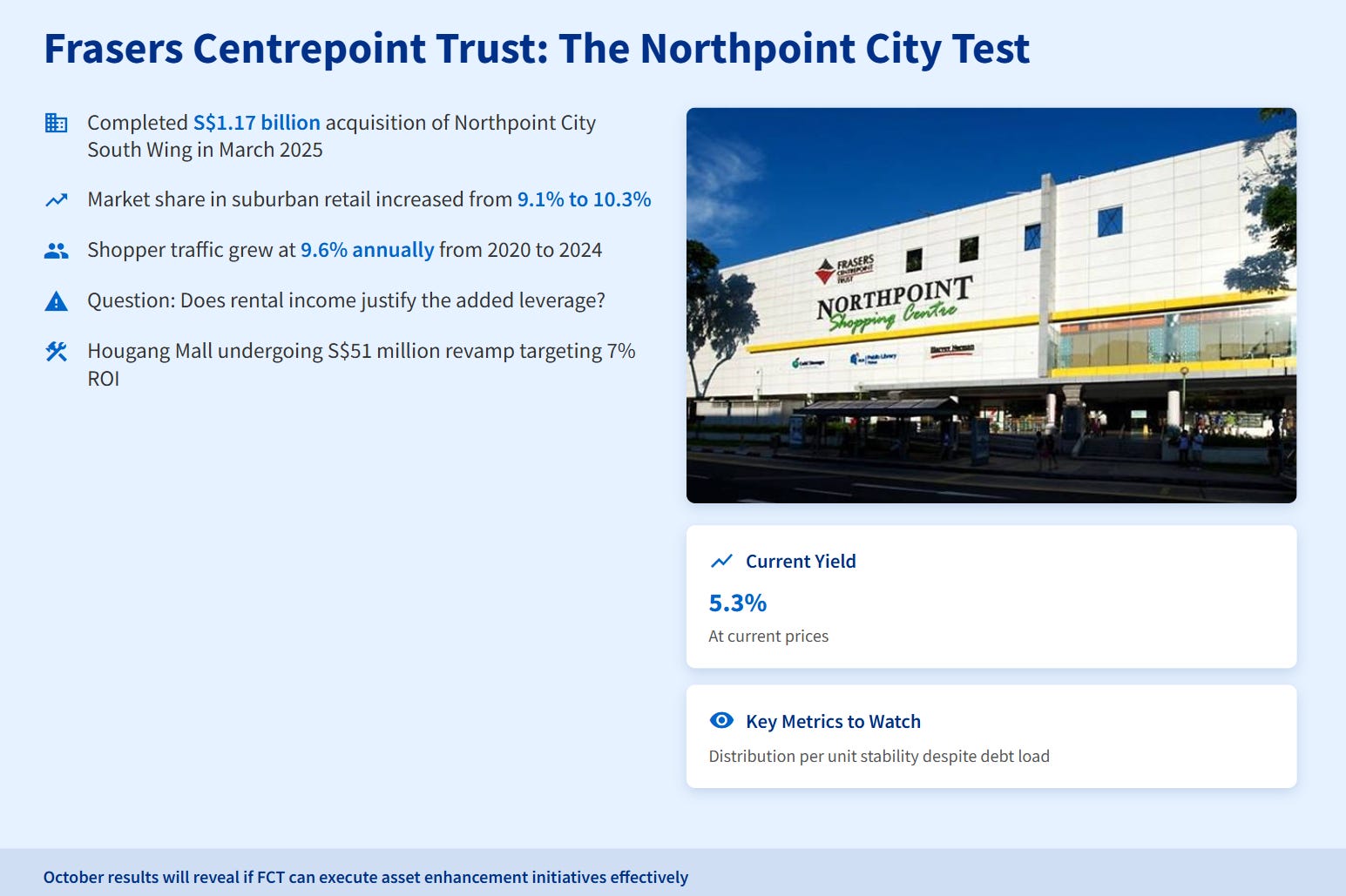

Frasers Centrepoint Trust: The Northpoint City Test

FCT completed its biggest-ever acquisition in March 2025. It bought the South Wing of Northpoint City for S$1.17 billion. This gave FCT full control of the largest suburban mall in northern Singapore. The move increased FCT’s market share in suburban retail from 9.1% to 10.3%.

The October results will reveal the impact. Investors want to see if FCT can execute asset enhancement initiatives now that it owns both wings. The mall is at full occupancy. Shopper traffic grew at 9.6% annually from 2020 to 2024. But FCT took on debt to fund the purchase. The question is whether the rental income justifies the added leverage.

FCT yields around 5.3% at current prices. The REIT has been active in upgrading its properties. Hougang Mall is undergoing a S$51 million revamp targeting 7% return on investment. If FCT shows stable or rising distribution per unit despite the Northpoint debt load, that signals strength. If DPU declines, investors will question whether the acquisition was worth it.

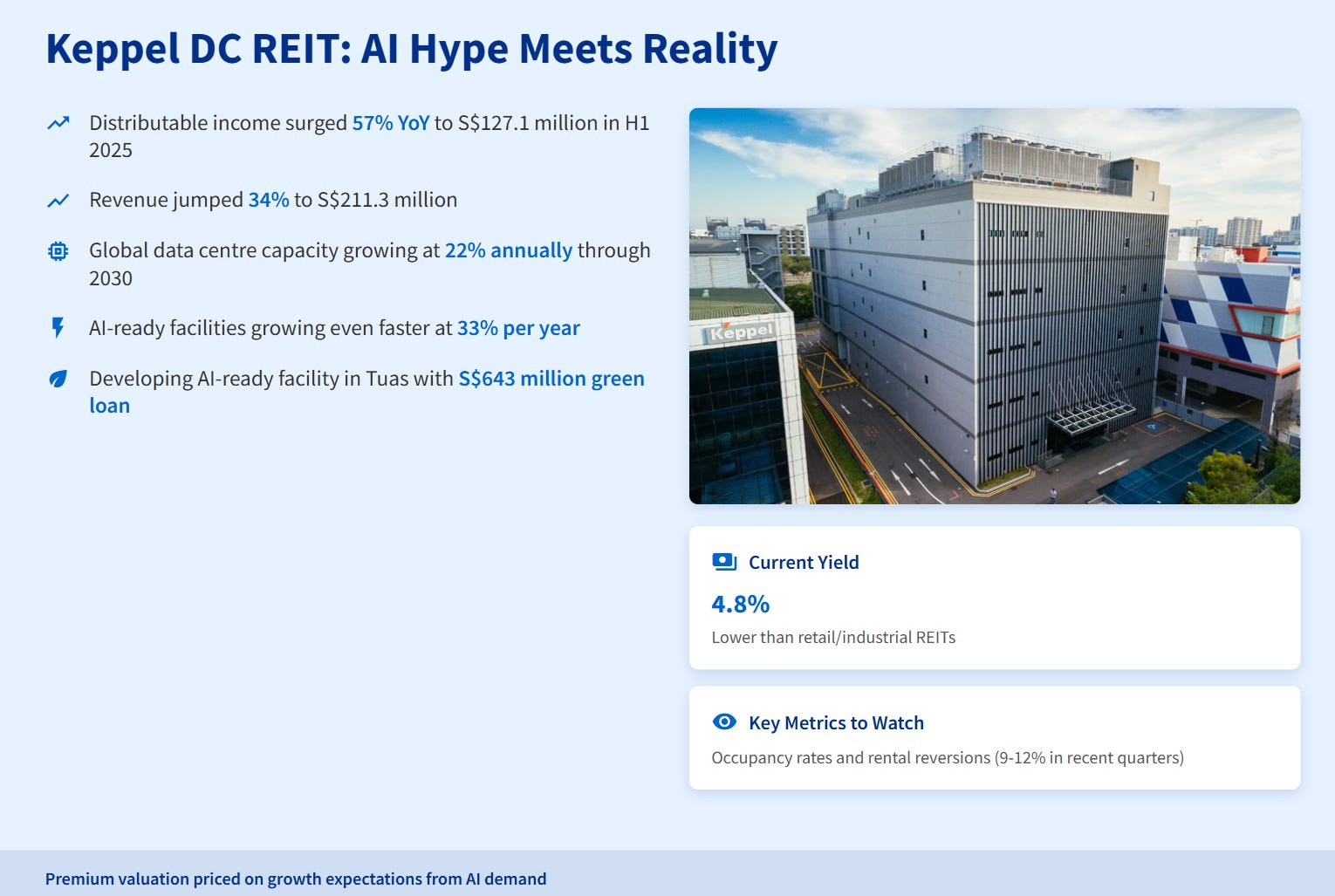

Keppel DC REIT: AI Hype Meets Reality

Keppel DC REIT posted strong numbers in the first half of 2025. Distributable income surged 57% year-on-year to S$127.1 million. Revenue jumped 34% to S$211.3 million. The REIT benefited from acquisitions in Singapore and Tokyo. It also saw higher contributions from contract renewals and escalations.

The October update will show if this momentum continues. Data centre REITs are the darlings of the AI boom. Global data centre capacity needs are expected to grow at 22% annually through 2030. AI-ready facilities are growing even faster at 33% per year. Singapore is positioning itself as a key digital hub in Asia.

But Keppel DC REIT faces challenges. Singapore has limited power supply. The government paused new data centre approvals in 2019 due to energy constraints. It has since allowed limited expansion for green operators. Keppel DC REIT is developing an AI-ready facility in Tuas with a planned 2026 opening. It secured a S$643 million green loan for the project.

Investors will watch occupancy rates and rental reversions. Keppel DC REIT achieved positive rental reversion of around 9-12% in recent quarters. If that holds, it supports the bull case. If occupancy softens or renewals disappoint, the high valuation becomes harder to justify. Keppel DC REIT trades at a premium to book value. Its yield of 4.8% is lower than retail or industrial REITs. That premium is priced on growth expectations.

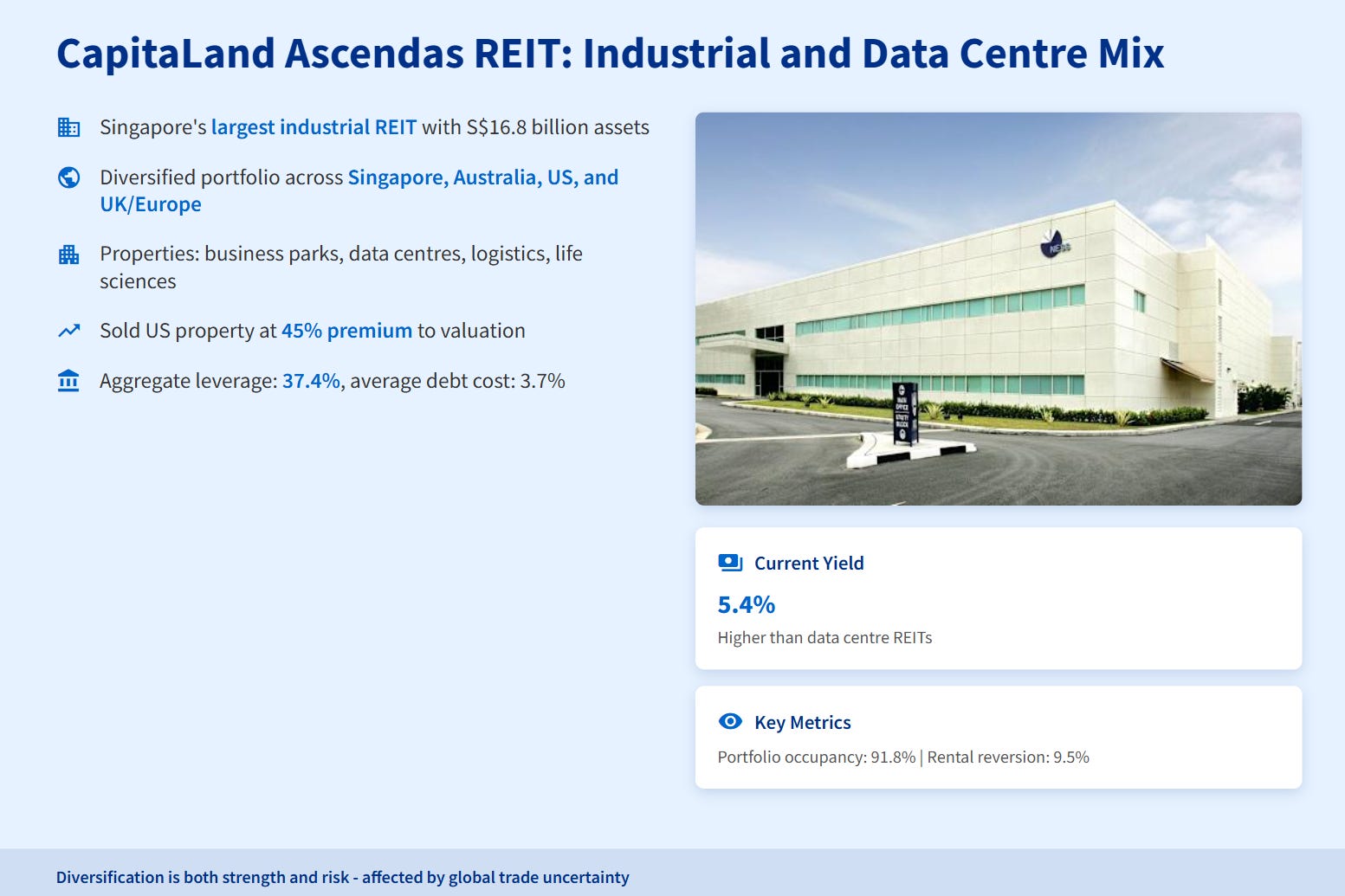

CapitaLand Ascendas REIT: Industrial and Data Centre Mix

CLAR is Singapore’s largest industrial REIT. It owns S$16.8 billion of assets across Singapore, Australia, the US, and UK/Europe. The portfolio includes business parks, data centres, logistics facilities, and life sciences properties.

CLAR posted modest results in the first half of 2025. Gross revenue dipped slightly due to earlier divestments. But portfolio occupancy remained healthy at 91.8%. Rental reversion was positive at 9.5%. The REIT sold one US property at a 45% premium to valuation. It used the proceeds to fund new acquisitions, including two properties at Science Park Drive in Singapore.

October’s update will show if CLAR can maintain its 5.4% yield. The REIT’s aggregate leverage stands at 37.4%. Its average debt cost is 3.7%. With 76% of borrowings on fixed rates, CLAR has some protection against further rate hikes. But if occupancy slips or renewals weaken, the distribution could come under pressure.

CLAR’s diversification is both strength and risk. Its exposure to multiple geographies and property types spreads risk. But it also means CLAR is affected by global trade uncertainty and currency movements. Investors will look for stability in Singapore assets and positive news from overseas holdings.

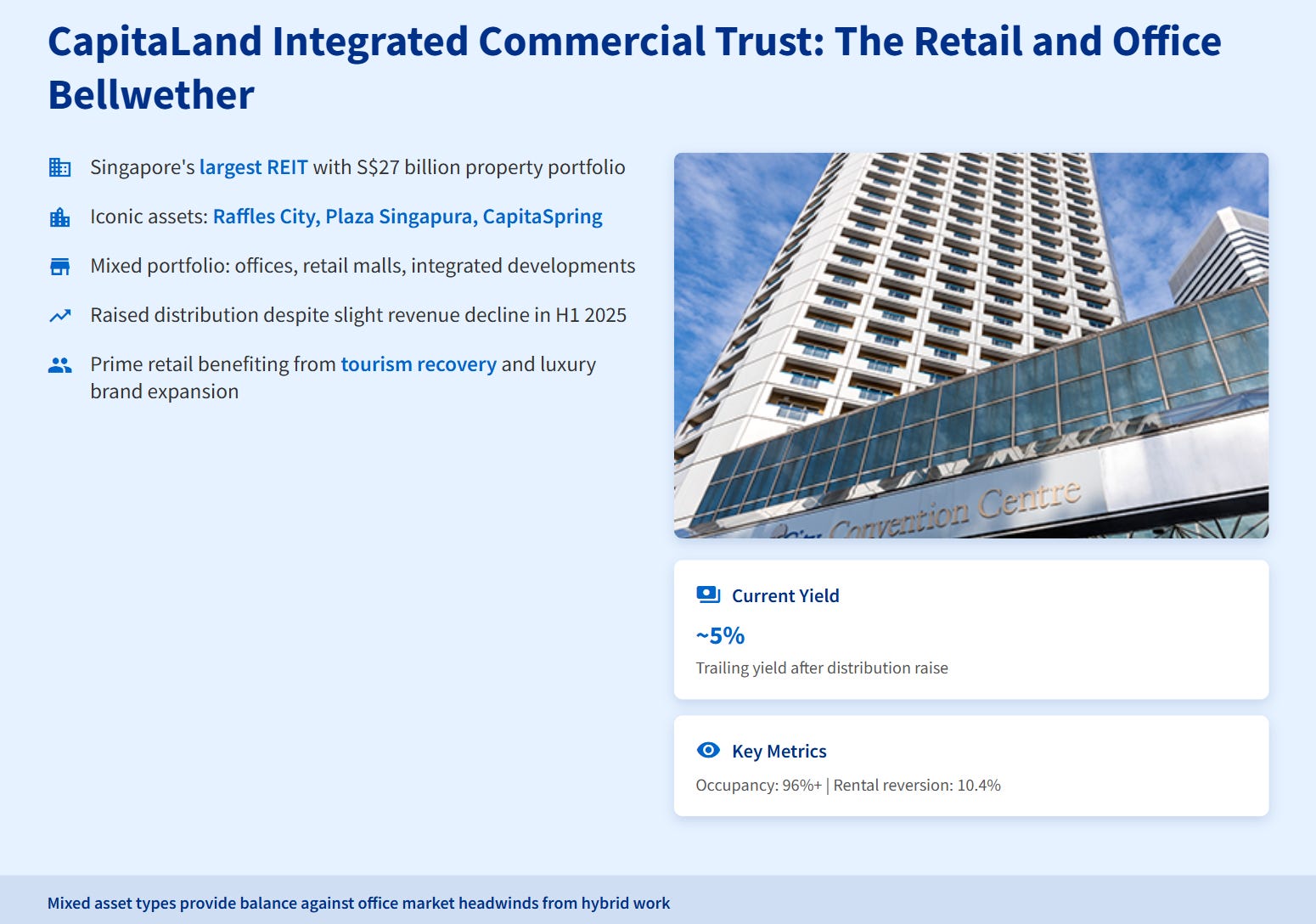

CapitaLand Integrated Commercial Trust: The Retail and Office Bellwether

CICT is Singapore’s largest REIT. It owns S$27 billion of properties, mostly in Singapore. The portfolio includes iconic assets like Raffles City, Plaza Singapura, and CapitaSpring. CICT has a mix of offices, retail malls, and integrated developments.

CICT reported a slight revenue decline in the first half of 2025. Revenue fell 0.5% year-on-year to S$787.6 million. Net property income dipped 0.4% to S$579.9 million. But CICT raised its distribution, pushing its trailing yield close to 5%. The REIT achieved rental reversion of 10.4% in the first quarter of 2025.

The October results will reveal if CICT can sustain this performance. Singapore’s office market faces headwinds from hybrid work. Companies are downsizing office space. But prime retail malls are seeing strong tenant demand driven by tourism recovery and luxury brand expansion. CICT’s mix of asset types provides some balance.

Investors will watch for updates on asset enhancement initiatives. CICT has been active in refreshing its properties to attract higher-paying tenants. If occupancy holds above 96% and rental reversions remain positive, CICT’s distribution should be safe. If office leasing weakens further, the retail assets will need to carry more weight.

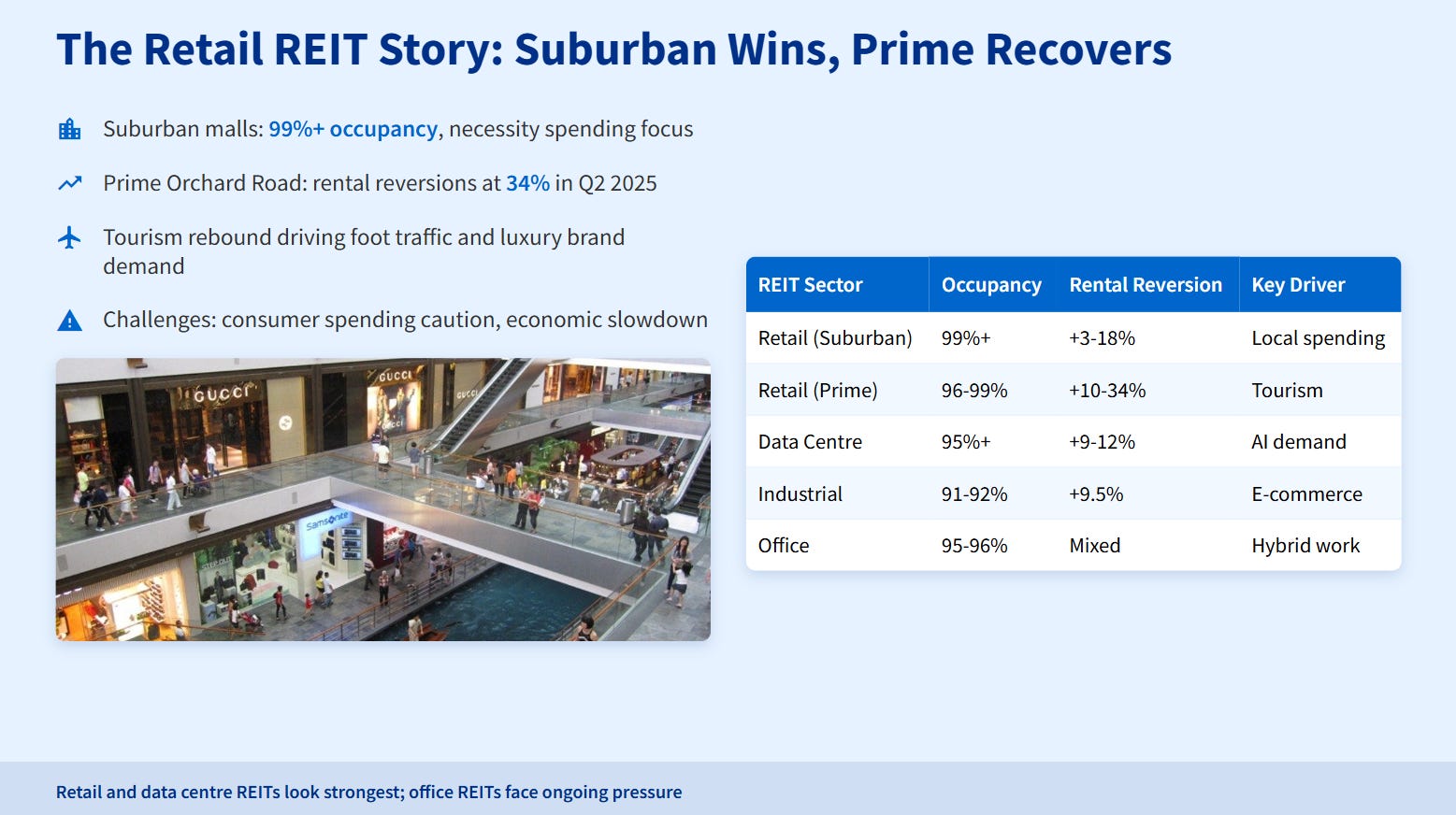

The Retail REIT Story: Suburban Wins, Prime Recovers

Retail REITs have been resilient. Suburban malls like those owned by FCT and CICT have high occupancy rates above 99%. They benefit from necessity spending. Tenants include supermarkets, clinics, banks, and food outlets. These categories held up well even during the pandemic.

Prime malls on Orchard Road are recovering. Rental reversions at properties like Mandarin Gallery hit 34% in Q2 2025. Orchard Road retail rents grew modestly, but demand from luxury brands is strong. Tourism has rebounded. International visitors drive foot traffic and sales for high-end retailers.

Shopper traffic at major malls is up. Tenant sales are improving. VivoCity, owned by Mapletree Pan Asia Commercial Trust, saw tenant sales grow 14% quarter-on-quarter despite ongoing basement renovations. FCT’s portfolio recorded positive shopper traffic growth across its nine suburban malls.

But challenges remain. Consumer spending is cautious. Singapore’s economy is slowing. Global uncertainties around trade and tariffs weigh on sentiment. Retail REITs must balance rental growth with tenant viability. Push rents too high, and tenants struggle. Keep rents flat, and distributions stagnate.

The October results will show how retail REITs are navigating this. Investors should look for stable or rising distribution per unit, occupancy above 98%, and positive rental reversions of at least 3-5%. Those metrics signal health.

Table: Iggy’s Take: REIT Sector Outlook & Key Drivers

This table summarizes the state of play. Retail and data centre REITs look strongest. Office REITs face ongoing pressure.

The Data Centre Opportunity: Real or Overhyped?

Data centre REITs are the growth story everyone talks about. The rise of artificial intelligence is driving demand for computing power. Companies like OpenAI, Google, and Microsoft are racing to build AI models. Those models require massive data centres packed with GPUs.

Singapore is a beneficiary. The city-state is a key hub for cloud computing in Asia. Major players like Amazon Web Services, Microsoft Azure, and Google Cloud have presence here. Keppel DC REIT and CapitaLand Ascendas REIT own data centre assets in Singapore and globally.

But there are limits. Singapore faces power constraints. The government paused new data centre approvals in 2019. It has since allowed selective expansion for operators using green energy. Keppel DC REIT’s new Tuas facility will use renewable power and efficient cooling systems.

The October results from Keppel DC REIT will test the thesis. If the REIT shows continued strong occupancy, high rental renewals, and forward bookings for new capacity, the bull case holds. If there are signs of oversupply or weakening demand, the premium valuation becomes questionable.

Data centre REITs trade at lower yields than other REIT sectors. Keppel DC REIT yields around 4.8%. That compares to 5.3% for retail REITs and 5.4% for industrial REITs. Investors pay a premium for growth. But growth is not guaranteed. The AI boom could slow. Hyperscale clients could shift spending. Power costs could rise.

Investors should be selective. Data centre REITs with long-term contracts, high-quality clients, and green energy credentials have the best outlook. But don’t chase the hype blindly. Wait for results that confirm the narrative.

Blue Chips Trading at Deep Discounts: Worth a Look?

While REITs grab attention for income, patient investors can find a very different opportunity in some of Singapore’s overlooked blue chips. These are contrarian plays, not quick wins, focused on deep value.

Hongkong Land is the prime example. The stock trades at a staggering 0.45 times book value—meaning the market values its portfolio of premium properties at less than half its stated worth. The company is actively working to close this gap. It’s executing an asset-light strategy, marked by the HK$6.3 billion sale of One Exchange Square in April.

In its first-half 2025 results, underlying profit rose 11% to US$320 million, and its capital recycling program is 33% complete. The stock also pays a dividend yield of around 4%. The risk? The discount exists for a reason. Hongkong Land’s assets are concentrated in Hong Kong, which faces economic headwinds and soft office rents. The bet is that management’s capital recycling and a long-term recovery will force the market to re-rate the stock.

For a more Singapore-focused play, UOL Group trades at just 0.58 times book value. As a major property developer and hotel operator, UOL owns a trove of prime land and commercial properties. At this price, investors are effectively buying those assets for significantly less than their replacement cost.

Finally, consider a name like Wilmar International. As a leading agribusiness, the stock has been tossed aside due to commodity price volatility. While its price-to-book ratio isn’t the main story, the long-term fundamentals for global food processing and distribution remain solid.

Iggy’s Take: These stocks are the polar opposite of T-bills. They require a long time horizon (think 3-5+ years) and a strong stomach. The ‘catch’ is that ‘cheap’ can always get ‘cheaper,’ and these assets can stay undervalued for years. This is not an income strategy for your CPF funds; it’s a deep value play for the patient, cash portion of your portfolio.

Table: Value Hunting: SG Blue Chips Trading at Deep Discounts

This table highlights deep value plays. These stocks are not without risk. Hongkong Land depends on Hong Kong’s recovery. UOL faces a soft Singapore property market. Wilmar is exposed to commodity cycles. But for patient investors with a long horizon, the margin of safety is high.

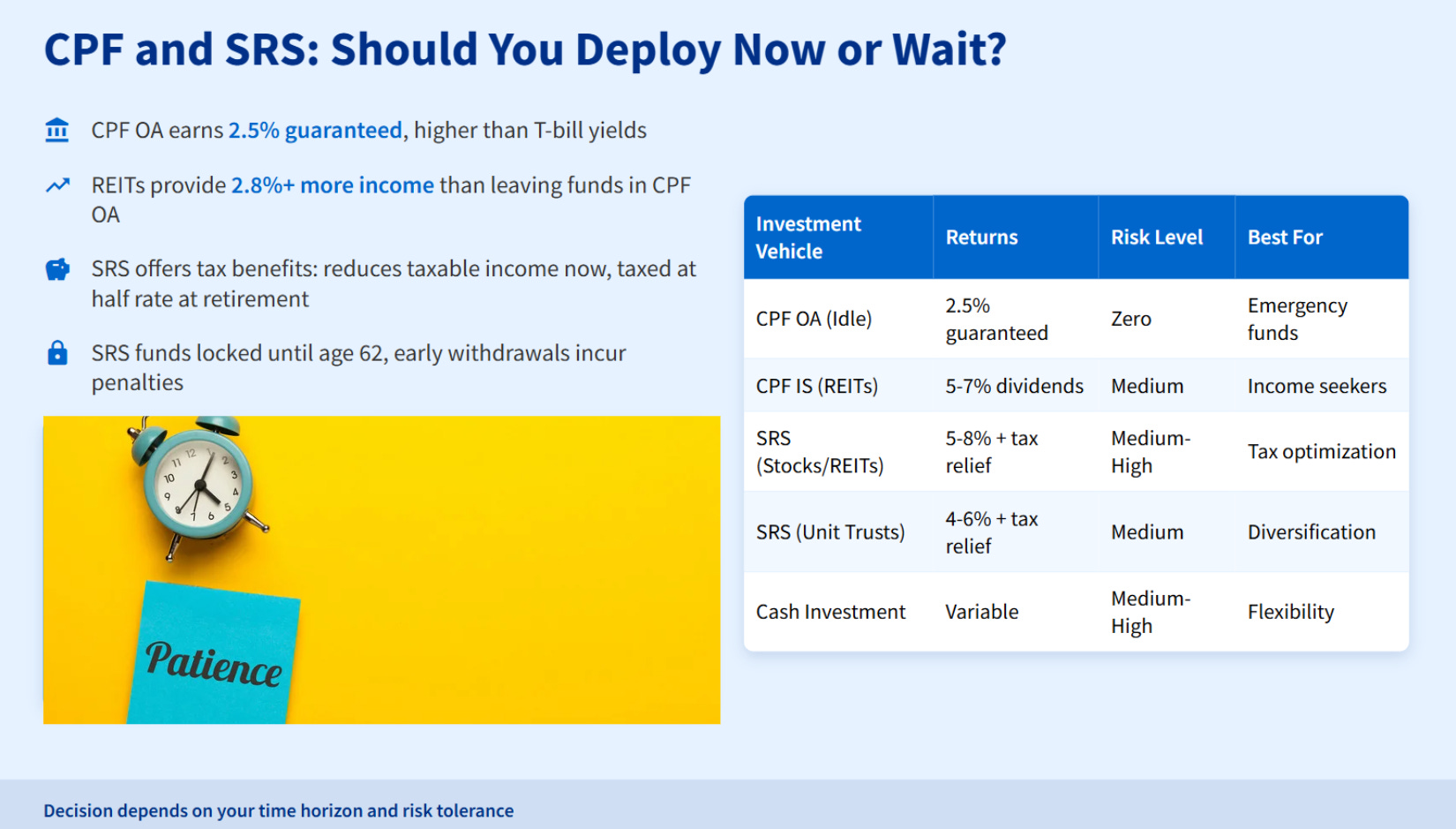

CPF and SRS: Should You Deploy Now or Wait?

Many Singapore investors hold funds in CPF Ordinary Account and SRS. The question is whether to deploy those funds into REITs or stocks, or leave them idle.

CPF OA earns 2.5% guaranteed. That is higher than current T-bill yields. If you invest CPF OA funds into stocks or REITs via the CPF Investment Scheme, you give up the guaranteed 2.5%. Your investment must beat that to make sense.

At current REIT yields of 5-5.4%, there is a cushion. A retail REIT yielding 5.3% provides 2.8% more income than leaving funds in CPF OA. Over time, that compounds. But there is risk. REIT prices can fall. Dividends can be cut. If you buy a REIT at S$2.50 and it falls to S$2.00, you need the dividend income to make up the capital loss.

SRS offers tax benefits. Contributions to SRS reduce your taxable income. Withdrawals at retirement are taxed at half your income at that time. For high earners, the tax savings can be substantial. But SRS funds are locked until age 62. Early withdrawals incur penalties.

Investing SRS funds into REITs makes sense if you don’t need the liquidity. You benefit from tax relief on contributions and tax-deferred growth. Dividends compound within the SRS account. At retirement, you withdraw at a lower tax rate.

Table: The CPF/SRS Decision: Comparing Your Options

This table lays out the trade-offs. CPF OA is safe but low return. CPF Investment Scheme and SRS offer higher potential but come with constraints. Cash investment gives full flexibility but no tax benefits.

The decision depends on your time horizon and risk tolerance. If you are young with decades until retirement, deploying CPF and SRS into well-chosen REITs can build wealth. If you are close to retirement or need liquidity, the guaranteed 2.5% in CPF OA may be wiser.

Timing matters. Buying REITs after they report strong earnings and yields compress may limit upside. Waiting for results and assessing valuations could be prudent. The October earnings will provide clarity.

Strategic Moves for Singapore Investors: A Framework

Here is a practical framework for allocating your portfolio in the current environment.