When $1 Trillion Meets Reality: Why US Regional Bank Troubles Should Matter to Singapore Investors

Why Local Investors Aren't as Insulated as They Think

The banking world is flashing warning signs again. US regional banks are struggling under massive commercial real estate exposure, fraud losses, and rising delinquencies. For Singapore and Malaysian investors, this isn’t just distant noise—it’s a masterclass in risk management and a reminder of why our CPF guardrails and dividend-focused strategies matter more than ever.

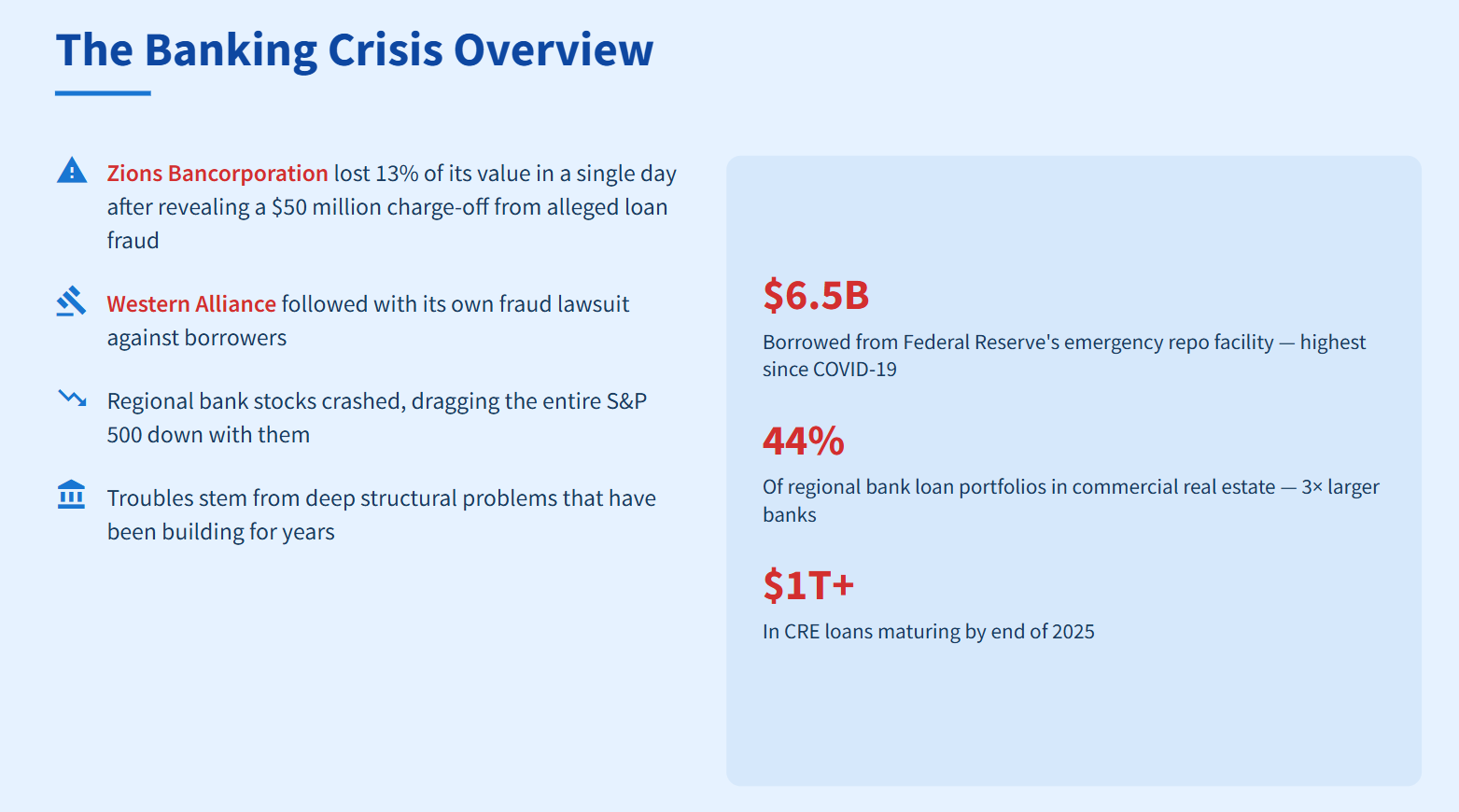

The alarm bells started ringing loud in mid-October 2025. Zions Bancorporation lost 13% of its value in a single day after revealing a $50 million charge-off from alleged loan fraud. Western Alliance followed with its own fraud lawsuit against borrowers. Regional bank stocks crashed, dragging the entire S&P 500 down with them. The situation got so tense that banks borrowed $6.5 billion from the Federal Reserve’s emergency repo facility—the highest since COVID-19.

This wasn’t random panic. The troubles stem from deep structural problems that have been building for years.

In This Article:

• The Mean Reversion Setup: Quality Beaten Down by Rates

• Strategic Sector Pivots: Betting on Asia’s Growth Engines

• Interest Rate Reversal: The Tailwind Finally Arrives

• Conservative Financial Management: How They Survived the Storm

• The Green Advantage: ESG as Competitive Edge

• My Take: The Patience Play (But Don’t Chase the Party)

• Action Steps for Singapore InvestorsThe Commercial Real Estate Time Bomb

Regional banks in America have an enormous problem. They hold 44% of their loan portfolios in commercial real estate—more than three times the 13% exposure of larger banks. Over $1 trillion in CRE loans will mature by the end of 2025. Most of these loans were written when interest rates were near zero. Now borrowers need to refinance at rates that are multiples higher.

The office sector is in crisis. Delinquency rates on office loans have spiked to 10.4%, approaching 2008 financial crisis levels. The national office vacancy rate hit 19.4% in 2025, with some cities far worse. San Francisco, Austin, and Seattle all clocked vacancy rates above 27%—with some cities topping 29%.

Table 1: US Office Market Distress by Major Metro (2025)

Caption: High-growth metros like San Francisco and Austin, once darlings of the tech boom, now face the sharpest vacancy spikes. Banks with heavy loan concentration in these specific markets are most at risk of default

Empty office buildings mean property values have collapsed. Property owners can’t generate enough rental income to service their debts. When loans mature, banks face a brutal choice: extend the loan and pretend everything is fine, or force the borrower into default and take massive losses.

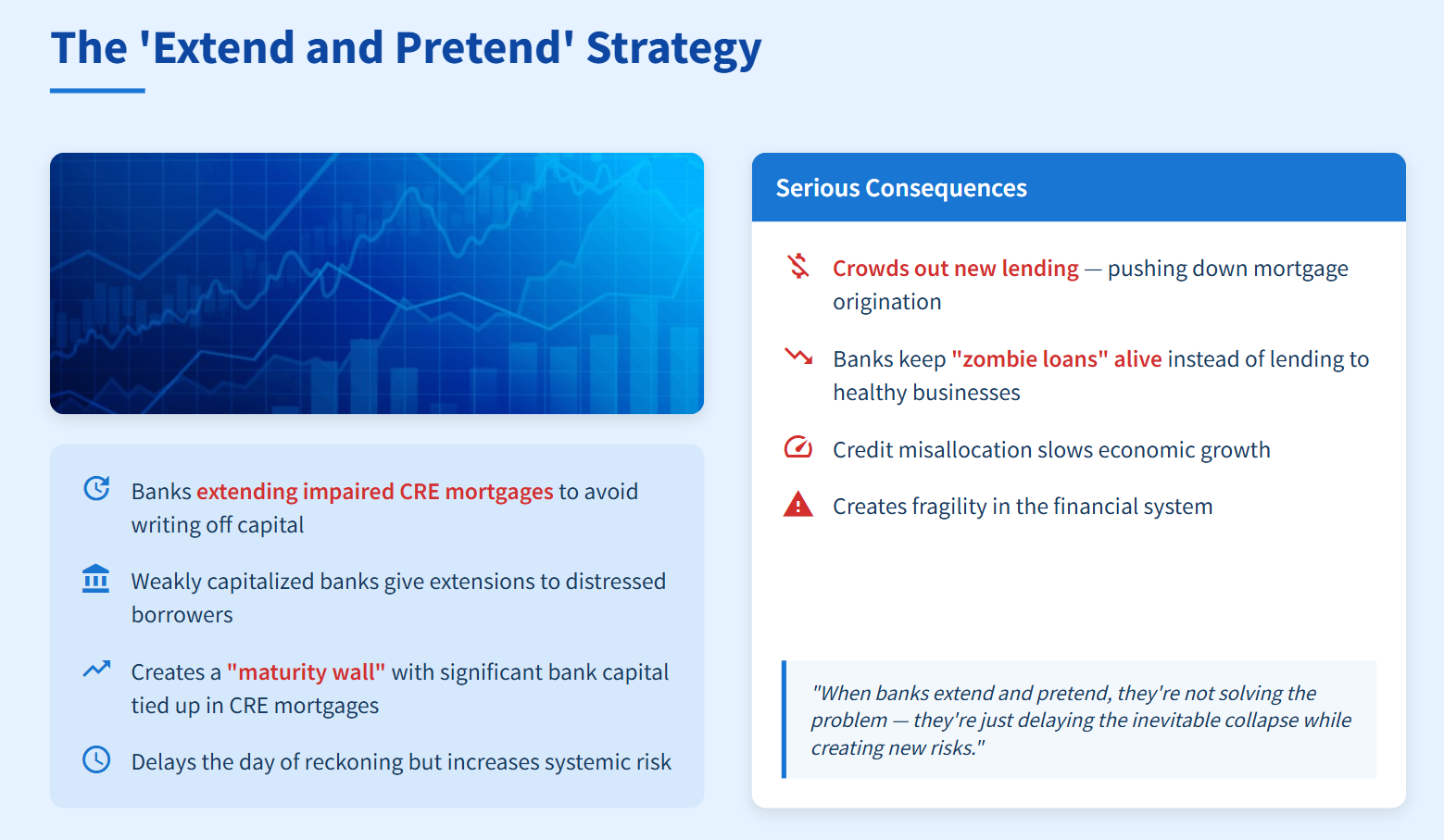

The “Extend and Pretend” Strategy

Banks have been “extending and pretending” their impaired CRE mortgages to avoid writing off capital. Weakly capitalized banks give extensions to distressed borrowers, delaying the day of reckoning. This behavior has created a “maturity wall” with a significant part of bank capital tied up in CRE mortgages maturing soon.

The extend-and-pretend strategy has serious consequences. It crowds out new lending, pushing down mortgage origination. Banks are keeping zombie loans alive instead of lending to healthy businesses and property projects. This credit misallocation slows economic growth and creates fragility in the system.

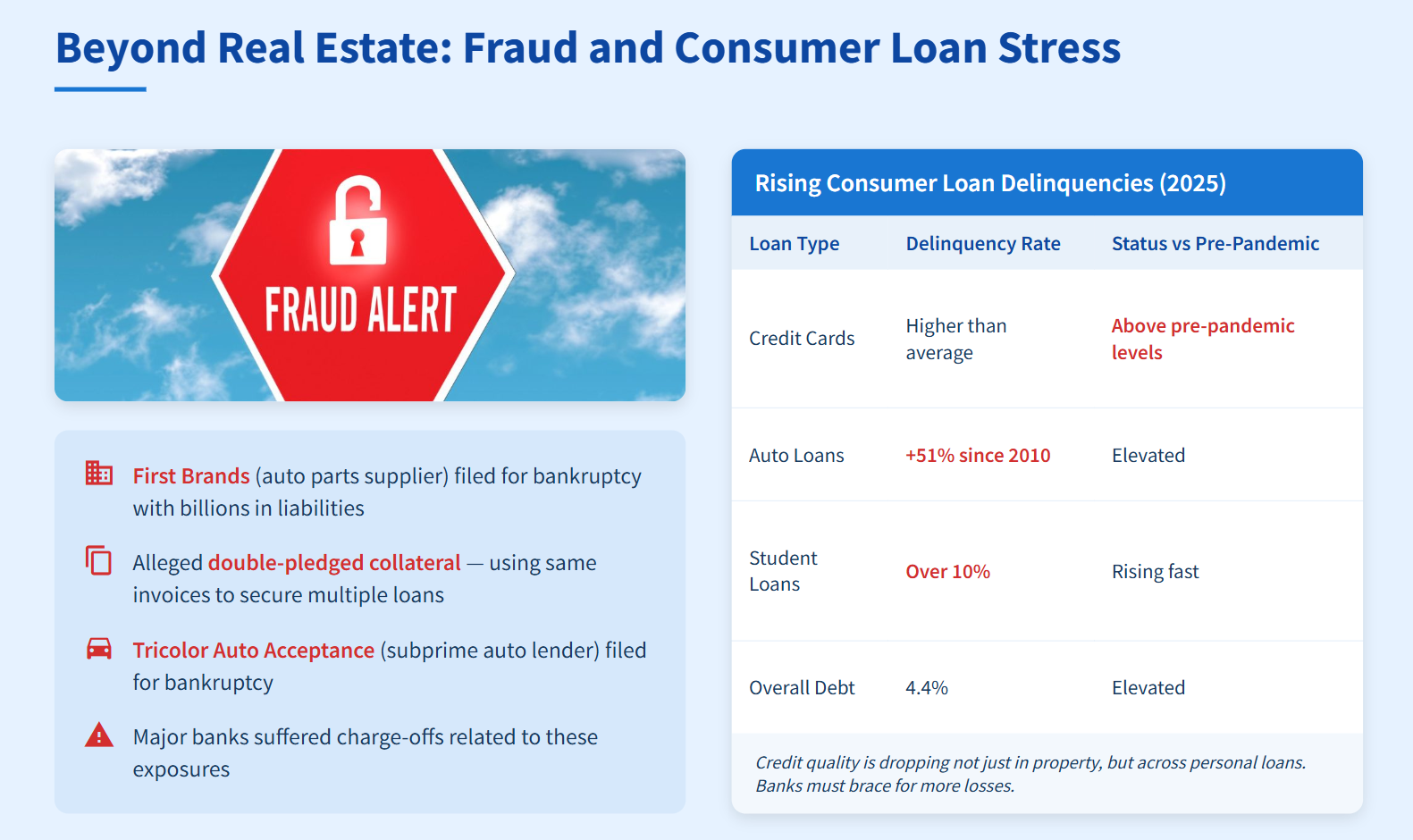

Beyond Real Estate: Fraud and Consumer Loan Stress

The problems aren’t limited to commercial real estate. Recent bankruptcies exposed fraud in the lending system. First Brands, an auto parts supplier, filed for bankruptcy with billions in liabilities. The company allegedly double-pledged collateral—using the same invoices to secure loans from multiple lenders.

Tricolor Auto Acceptance, a subprime auto lender, filed for bankruptcy after lenders found another round of fraudulent activity with double-pledged collateral and data irregularities. Major banks suffered charge-offs related to these exposures.

Consumer loan delinquencies are rising across the board. Credit card and auto loan delinquencies now exceed pre-pandemic averages. Auto loan delinquencies (60+ days past due) jumped over 50% compared to the start of the last decade. Student loan delinquency rates surged as federal loan reporting resumed.

Table 2: Rising Consumer Loan Delinquencies (2025)

Caption: Credit quality is dropping not just in property, but across personal loans. Banks must brace for more losses.

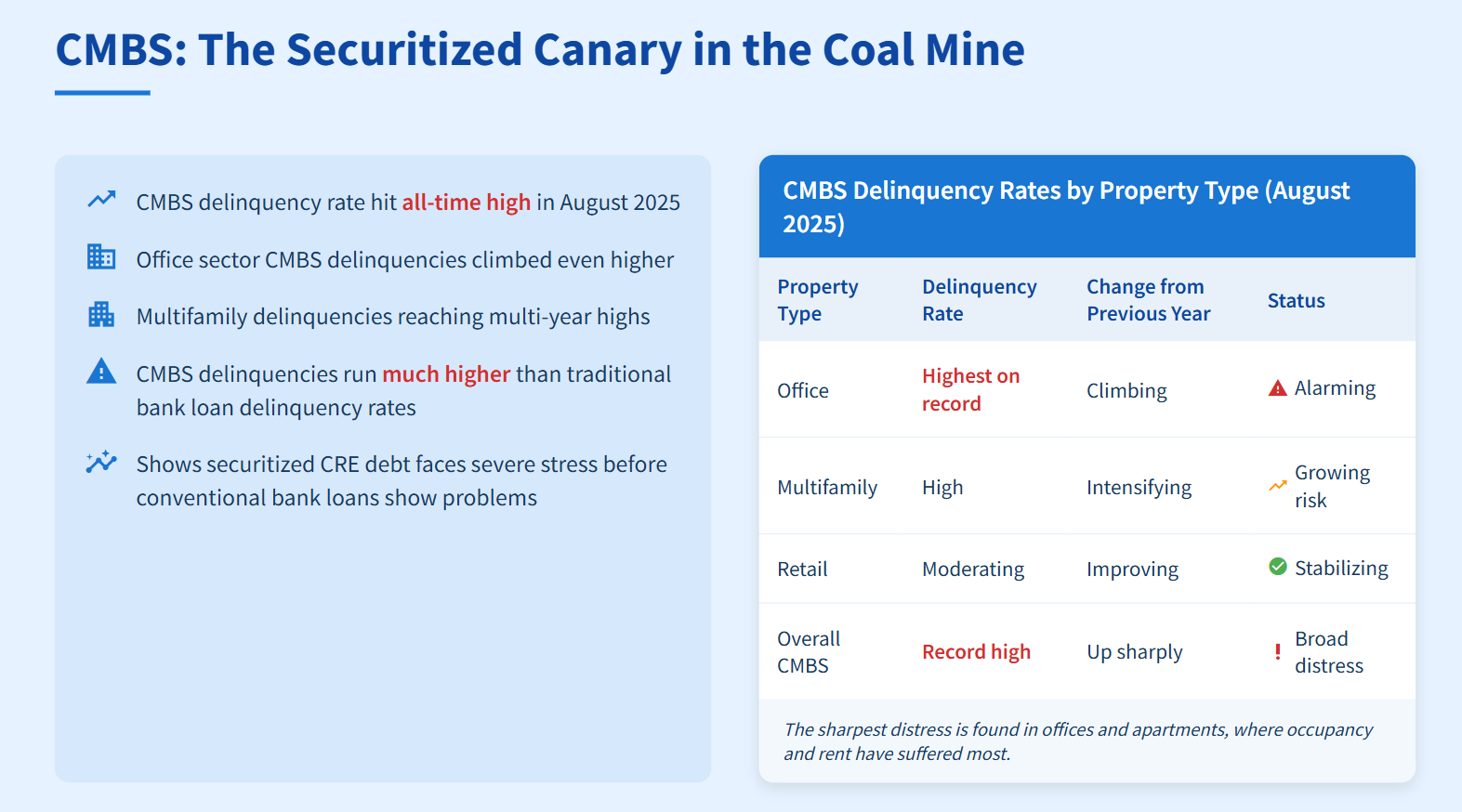

CMBS: The Securitized Canary in the Coal Mine

Commercial mortgage-backed securities show just how bad things have gotten. The CMBS delinquency rate hit an all-time high in August 2025. Office sector CMBS delinquencies climbed even higher, with multifamily delinquencies also reaching multi-year highs.

CMBS delinquencies are particularly concerning because they run much higher than traditional bank loan delinquency rates. This gap shows how securitized commercial real estate debt faces severe stress, often before conventional bank loans show problems.

Table 3: CMBS Delinquency Rates by Property Type (August 2025)

Caption: The sharpest distress is found in offices and apartments, where occupancy and rent have suffered most.

Which Banks Are Most at Risk?

The problem isn’t uniform; it’s concentrated. The key issue is commercial real estate (CRE) exposure.

Think of it this way: investing all your savings in just one company’s stock is incredibly risky. If that company crashes, you take a massive hit. Some US regional banks have done the equivalent with their loan books. They have loaned so much money to property owners (offices, shops, and malls) that a downturn in that single sector threatens their entire capital base.

Summary Table (US banks most at risk):

Investors should watch for banks with:

High ratios of CRE loans versus their capital—a sign of taking on outsized risk.

Geographic concentration in cities with high office vacancies (like those in Table 1).

Recent news of rising loan losses, charge-offs, or fraud cases.

Recent research reveals:

Valley National Bank has the highest CRE exposure among all US banks. Nearly 475% of its capital is tied up in CRE loans, which is far above what regulators consider safe.

Flagstar Bank, owned by New York Community Bancorp (NYCB), has also drawn attention after serious loan losses related to CRE.

Zions Bancorporation saw its stock drop 13% in a single day due to a large charge-off from loan fraud. Office properties in cities like Austin and San Francisco add to its risk.

Other notable banks with high CRE risk:

Western Alliance Bancorp: Recently hit by fraud lawsuits and downgrades.

Citizens Bank: Identified for above-average office exposure.

Fulton Financial, First Merchants, Old National Bank Corp, PacWest, and Gladstone: All cited by Moody’s for credit rating downgrades due to their CRE portfolios.

Even larger banks face challenges:

US Bank and PNC Bank have CRE loans that make up about 14–15% of their total portfolios. While they are better diversified, analysts still keep a close eye on their exposure.

Why does this matter? High concentration of bad property loans can trigger sudden losses, credit downgrades, and confidence shocks—not just for these banks, but for investors worldwide.

Key trends and stats:

Office vacancy rates in places like San Francisco and Austin are above 27%.

Hundreds of regional banks are vulnerable due to high CRE concentrations and rising consumer loan defaults.

Most risk is centered in banks where CRE loans are more than three times their capital reserves.

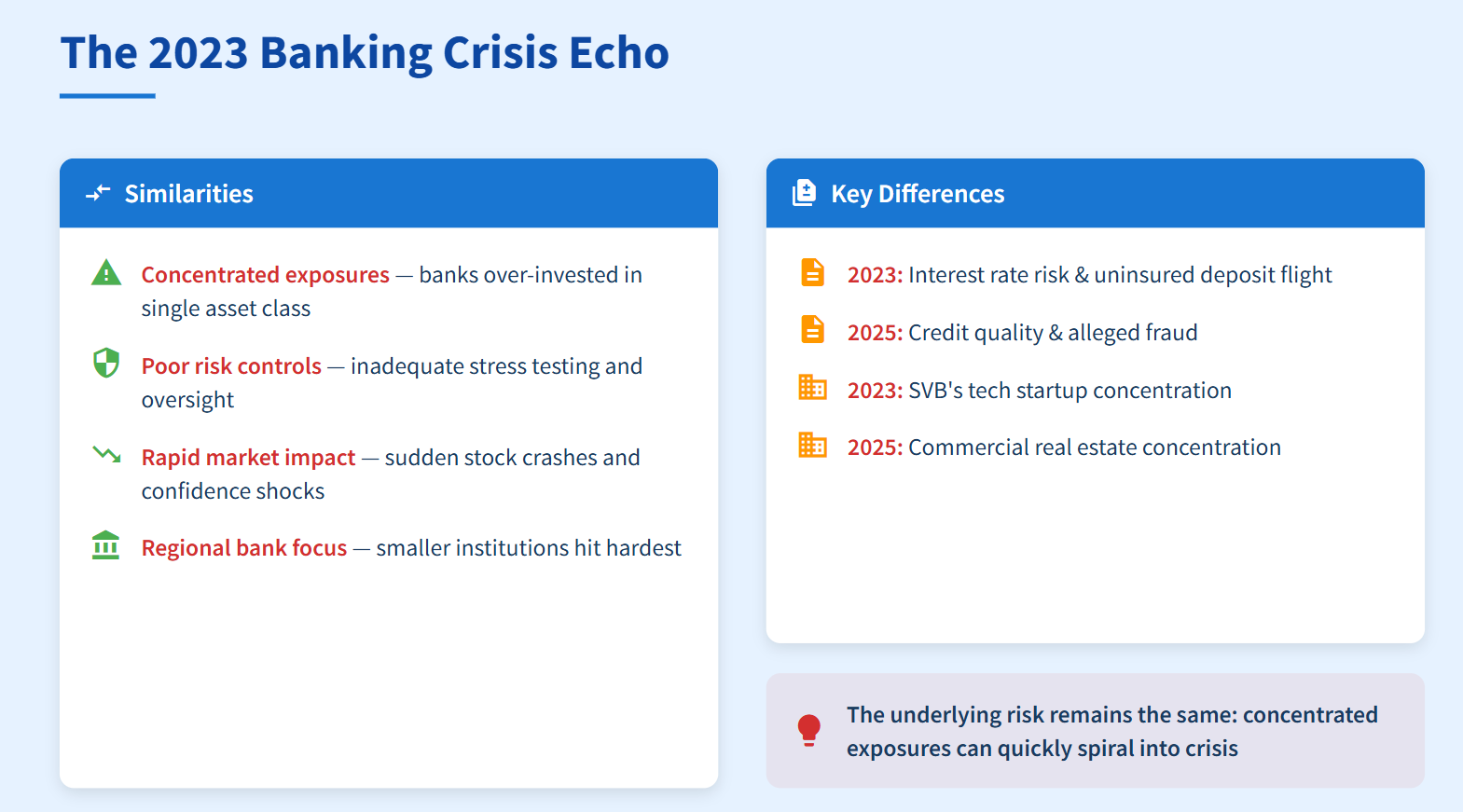

The 2023 Banking Crisis Echo

The crisis echoes the 2023 regional banking meltdown, when Silicon Valley Bank collapsed after a devastating bank run. SVB was crippled by interest rate risk and uninsured deposit flight. Signature Bank and First Republic failed soon after, marking the biggest bank failures since the Great Financial Crisis.

This time, the problem focuses more on credit quality—actual loans going bad—combined with alleged fraud. But the underlying risk remains the same: concentrated exposures and poor risk controls can quickly spiral into crisis.

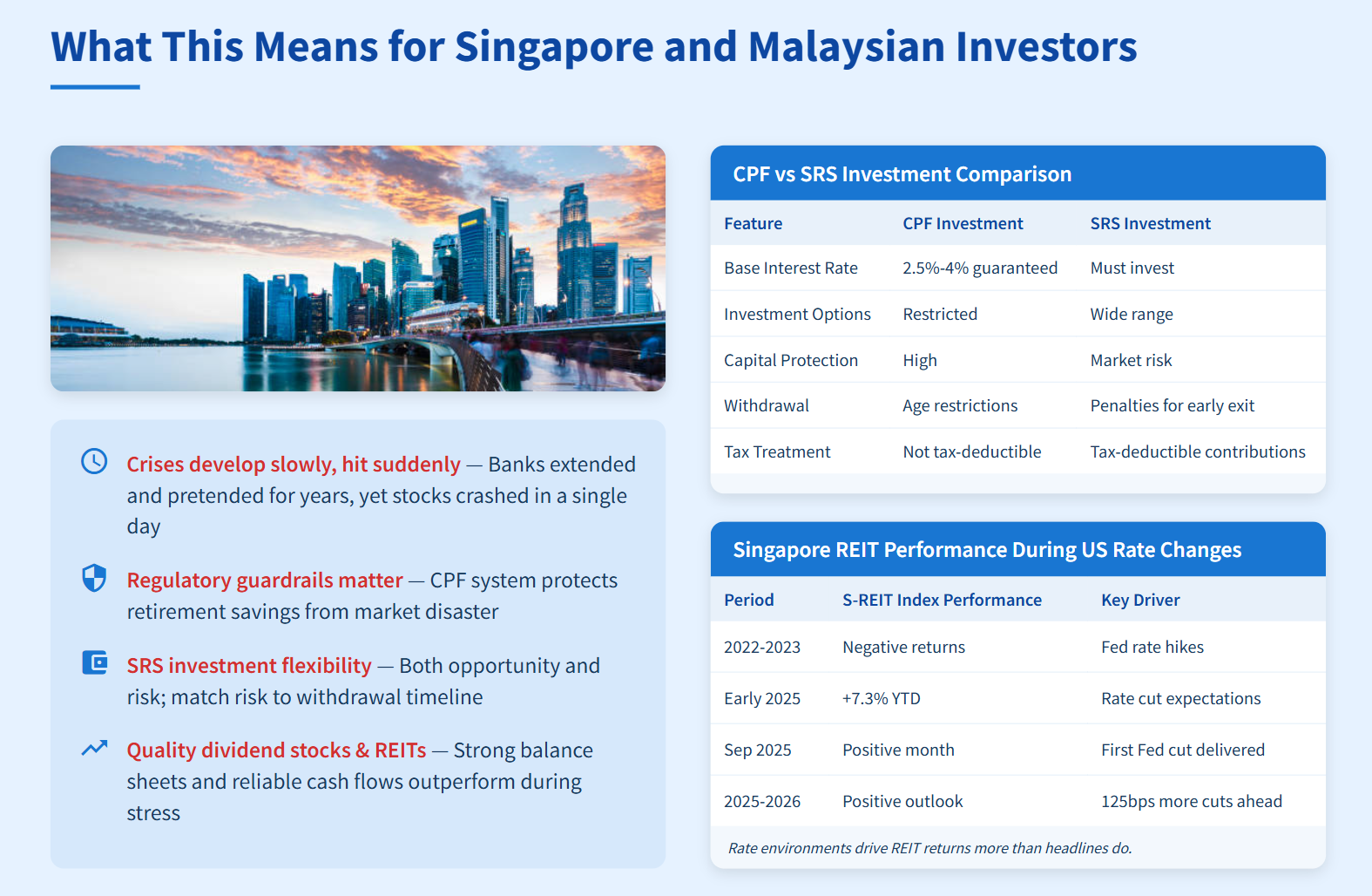

What This Means for Singapore and Malaysian Investors

For investors in Singapore and Malaysia, the US regional banking crisis offers big lessons.

First: Financial crises can develop slowly, but hit suddenly. Banks extended and pretended for years, yet a fraud reveal caused regional bank stocks to crash in a single day.

Second: Regulatory guardrails matter. Singapore’s CPF system and Malaysia’s EPF protect retirement savings. They can’t make you rich quickly, but they keep your core savings insulated from market disaster.

CPF Ordinary Account earns a guaranteed interest, with additional bonuses for certain balances. Your Special Account and MediSave are even safer. These returns won’t vanish overnight, no matter the market mood.

When US banks are failing, CPF savings remain safe, thanks to government protection and smart restrictions on risky assets.

Third: SRS investment flexibility brings both opportunity and risk. You can choose stocks, bonds, and REITs within SRS. Returns can be great—but losses are possible. Match your investment risk to your withdrawal timeline and goals.

Table 4: CPF vs SRS Investment Comparison

Caption: CPF offers safety, SRS offers choice. Know the difference before you act. Rate environments drive REIT returns more than headlines do.

Fourth: The banking crisis validates focus on quality dividend stocks and REITs. Companies with strong balance sheets and reliable cash flows outshine during times of stress. Singapore REITs benefited from expected US rate cuts in 2025, with sector indexes posting solid gains through the year.

Rate cuts help REITs by lowering borrowing costs and making their yields more attractive. Major Malaysian banks and blue chip dividend payers offer steady income with sustainable payout ratios.

Diversification across regions and sectors is critical. If you concentrated assets in US regional banks, losses would be severe. If you held a diversified portfolio of Singapore blue chips, Malaysian dividend stocks, and regional REITs, the impact is much less.

Pay attention to bank exposure when picking individual stocks. Singapore banks are well capitalized, but global credit stress can raise non-performing loans. Always check whether your bank investments are exposed to property and expect ripple effects when the US tightens up.

Maintain an emergency cash buffer. CPF offers long-term security, but liquid cash helps you weather short-term storms. Aim for a minimum buffer in a savings account or Singapore Savings Bonds.

Avoid leverage and margin trading. Some investors borrow money to chase returns, but this can wipe out portfolios when markets drop. The risks that cripple regional banks can hit individuals just as hard.

Crises create opportunities for patient investors. Banking stress pushes some quality stocks to attractive valuations. Buy only what you understand, and focus on strong fundamentals, not market moods.

Key Lessons from the US Banking Crisis

The US regional bank saga isn’t just news; it’s a masterclass in risk management. Here are the core lessons for your own portfolio:

Concentration Risk Kills. This is the #1 lesson. The regional banks are in trouble because they bet the farm on one asset class: commercial real estate. For us, the takeaway is clear: diversify across sectors and regions to ensure one bad bet can’t sink your portfolio.

Credit Risk is Real. The “extend and pretend” strategy and the surge in fraud cases show that you can’t just trust a company’s story. Always look at the balance sheet. Invest in companies with strong financials and manageable debts, not “zombie” firms hoping for a bailout.

Liquidity Risk is a Ticking Bomb. When the crisis hit Silicon Valley Bank, liquidity was the only thing that mattered. Deposits fled, and the bank couldn’t sell its assets fast enough. Always have a cash buffer and include investments (like Singapore Savings Bonds) that you can access quickly in an emergency.

Interest Rate Risk is Evergreen. The 2023 crisis was sparked by rates rising too fast. The 2025 S-REIT rally was sparked by the expectation of rate cuts. This risk never goes away. Match your bond and REIT holdings to the rate environment and understand how changes will affect their value.

Regulatory Risk Can Reshape Markets Overnight. Bank capital requirements, new rules on lending, or even a change in deposit insurance can alter a company’s entire profit model. Don’t get blindsided—stay vigilant and understand how new rules can impact your investments.

What to Watch Going Forward